An adjustable-rate mortgage, or ARM, is a type of home loan where the interest rate isn't set in stone. It starts with a lower, fixed interest rate for a specific period, but after that, the rate can change based on the market. This means your monthly payment could go up or down over the life of the loan.

Understanding The Adjustable Rate Mortgage

Think of it like an introductory cable or internet deal. You get a fantastic low price for the first year or two, but after that promo period ends, the rate adjusts to whatever the current market price is. An ARM works much the same way, offering a very attractive low payment for the first few years, which can be a game-changer for certain buyers.

This is the key difference between an ARM and the more familiar fixed-rate mortgage. With a fixed-rate loan, your interest rate is locked in for the entire term, usually 15 or 30 years, giving you a predictable payment that never changes. An ARM, on the other hand, is all about trading that long-term certainty for a lower payment right now.

The Trade-Off: Certainty For Flexibility

So, what's the real appeal of an ARM? It all comes down to the upfront savings. For the first few years, your monthly payments will almost certainly be lower than they would be with a fixed-rate loan from the same time. This initial advantage can help you:

- Qualify for a larger loan: That lower initial payment helps your debt-to-income ratio look better to lenders.

- Free up cash flow: You'll have more money in your monthly budget for savings, investments, or home improvements.

- Get into a pricier home: In a competitive market like Fairfax, VA, an ARM can be the key that unlocks the door to a home you might not otherwise afford.

Of course, there’s a catch. This early benefit comes with the risk that your payments will jump once the rate starts adjusting. That's why it's absolutely crucial to have a clear picture of your financial goals and how long you plan to stay in the home before you commit.

A Brief History Of The ARM

Believe it or not, ARMs are a fairly recent invention in the mortgage world. They first gained traction in the U.S. back on April 3, 1980, when regulators gave the green light to variable-rate loans. This was a direct response to a period of wild interest rate swings, where fixed 30-year mortgages had skyrocketed to a staggering average of 16.63% by 1981. For many Americans, the dream of homeownership was simply out of reach, and the ARM was created to offer a more accessible path. For a deeper dive, you can read about the history and economic impact of ARMs.

An ARM is a strategic financial tool designed for specific circumstances. It exchanges the predictability of a fixed-rate loan for a lower initial interest rate and payment, offering flexibility but requiring a clear understanding of its structure and potential risks.

To really see the difference, it helps to put these two loan types side-by-side.

ARM vs Fixed-Rate Mortgage At a Glance

This table breaks down the core differences between an Adjustable-Rate Mortgage and a standard 30-Year Fixed-Rate Mortgage. It’s a quick way to see how they stack up in terms of rate stability, payment structure, and who they’re best suited for.

| Feature | Adjustable-Rate Mortgage (ARM) | 30-Year Fixed-Rate Mortgage |

|---|---|---|

| Interest Rate | Starts low and fixed, then adjusts periodically with the market. | Remains the same for the entire 30-year loan term. |

| Monthly Payment | Lower during the initial period, then can increase or decrease. | Stays consistent and predictable for 30 years. |

| Risk Level | Higher due to potential for future rate and payment increases. | Lower, offering complete certainty and stability. |

| Best For… | Buyers who plan to sell or refinance before the rate adjusts. | Buyers who plan to stay in their home for the long term. |

Ultimately, the choice between an ARM and a fixed-rate mortgage comes down to your personal financial situation, your tolerance for risk, and your long-term plans for the property.

How An Adjustable-Rate Mortgage Actually Works

To really get a handle on an adjustable-rate mortgage, you have to look under the hood. It’s not just one interest rate; it’s a living, breathing number built from a few key parts. Each piece has a specific job in figuring out your monthly payment, both in that initial low-rate honeymoon phase and later on when it starts to change.

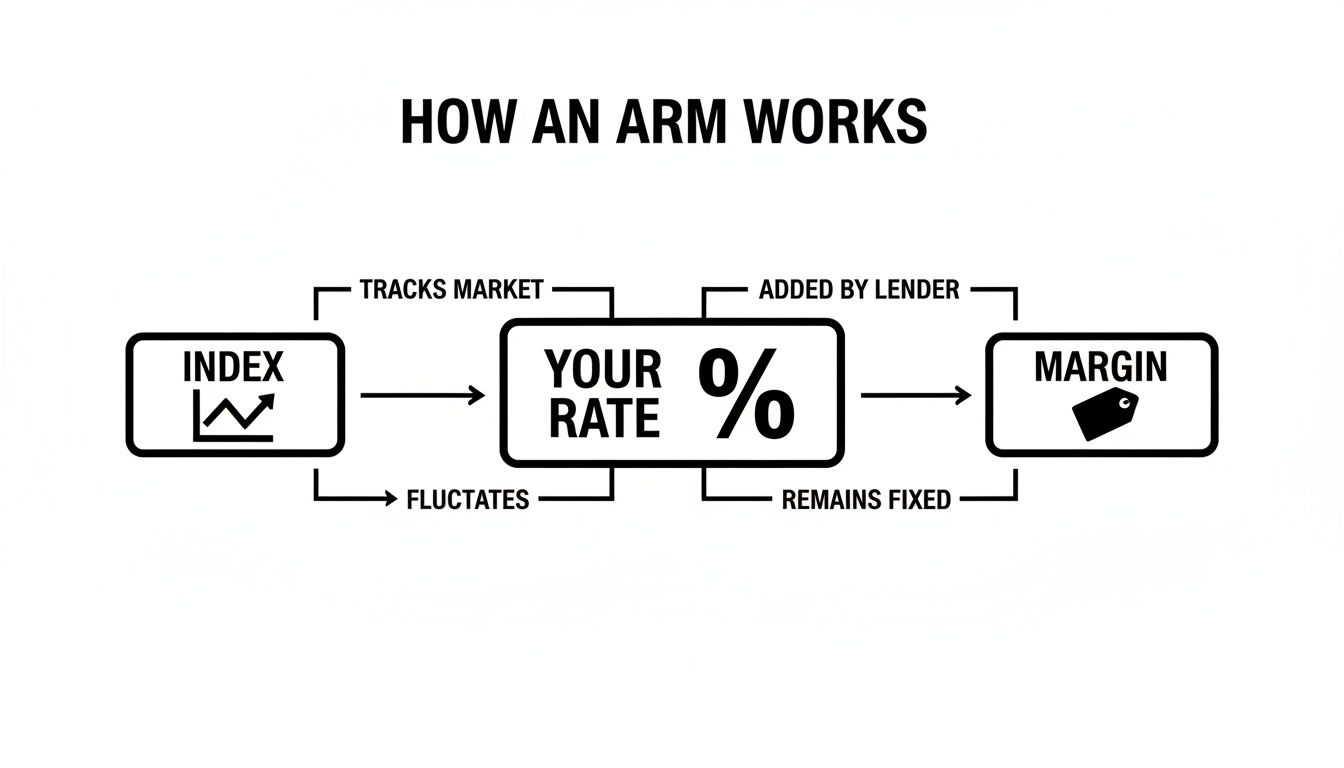

Think of your ARM's interest rate like a simple recipe with two main ingredients: the index and the margin. When you add them together, you get your "fully indexed rate"—the real interest rate you'll pay after that introductory period is over.

Let's pull apart the five pieces that make this all work.

The Index: The Market’s Pulse

The index is the first key ingredient. It’s a benchmark interest rate that moves up and down with the overall economy, and it's completely out of your lender's hands. Think of it like the wholesale price of a raw material, like coffee beans or lumber. When the market price for that material goes up, the index follows suit.

Lenders use several common indexes for ARMs, with the Secured Overnight Financing Rate (SOFR) being a very common one these days. Because the index moves with the market, it’s the part of your loan that actually causes your payment to adjust.

The Margin: The Lender’s Fixed Share

The margin is the second ingredient in our recipe. This is a set number of percentage points that the lender adds on top of the index. If the index is the wholesale cost of the coffee beans, the margin is the coffee shop's fixed markup—it covers their business costs and profit.

Key Formula: Index Rate + Lender's Margin = Your Fully Indexed Interest Rate

This simple math is what determines your interest rate every single time it adjusts. The margin is written into your loan agreement and never changes for the entire life of the loan.

So, if the SOFR index is sitting at 4.5% and your lender’s margin is 2.25%, your fully indexed rate would be 6.75%. Understanding this basic relationship is the key to figuring out how an ARM really operates.

Initial Rate And Adjustment Periods

Before your rate starts to float with the market, you get to enjoy the initial interest rate. This is the lower, "teaser" rate you pay during the fixed part of your loan. How long that period lasts is right in the name of the loan, like a 5/1 ARM or a 7/6 ARM.

What do those numbers mean? It's simpler than you might think:

- A 5/1 ARM means you have a fixed interest rate for the first five years. After that, your rate can adjust once every year for the rest of the loan.

- A 7/6 ARM gives you a fixed rate for the first seven years. After that, the rate can adjust every six months.

The first number always tells you how long the initial fixed-rate period is, in years. The second number tells you how often the rate can change after that period ends.

Rate Caps: Your Financial Safety Net

Maybe the most important feature protecting you from a sudden payment shock is the rate cap. These are built-in limits on how much your interest rate can actually move. Without them, your payments could go through the roof in a volatile market. There are three types of caps you absolutely need to know:

- Initial Adjustment Cap: This limits how much your rate can jump the very first time it adjusts after your fixed period is over.

- Subsequent Adjustment Cap: This controls the maximum increase allowed for every adjustment after that first one.

- Lifetime Cap: This sets the absolute ceiling for your interest rate. It can never go higher than this over the entire life of the loan, period.

For example, a loan with "2/2/5" caps means your rate can't go up by more than 2% at the first adjustment, no more than 2% at any later adjustment, and it can never be more than 5% higher than your original starting rate. These caps provide a crucial layer of predictability. With a clearer picture of how these components work, you can begin to estimate how your payments might change over time using our helpful online mortgage calculators.

Navigating The Different Types Of ARMs

Adjustable-rate mortgages aren't a one-size-fits-all product. Think of it like a toolkit—you wouldn't use a sledgehammer for a finishing nail. Similarly, the mortgage world has different ARMs for different financial jobs. Knowing the difference is crucial to making a smart choice, especially in a competitive market like Fairfax, Virginia.

Let's walk through the three main varieties you're likely to come across.

The Hybrid ARM

The Hybrid ARM is the most popular kid on the block, and for good reason. It's the type we've been talking about mostly—the 5/1, 7/6, and 10/1 ARMs fall into this category. The "hybrid" name perfectly describes its two-part nature: it starts with a fixed-rate period and then transitions into an adjustable-rate period.

For the first few years, your rate and payment are locked in, giving you predictability and peace of mind. Once that initial term is up, your rate will begin to float with the market, adjusting based on its index plus the lender's margin.

This is often a great fit for borrowers who:

- Plan on moving or refinancing before the fixed period ends.

- Anticipate their income growing significantly, making it easier to handle a potentially higher payment down the road.

- Want the lowest possible payment right now to afford more home today.

The Interest-Only (I-O) ARM

Next up is the Interest-Only (I-O) ARM. During its initial phase, your payments only cover the interest accruing on the loan. You're not touching the principal balance at all, which makes for some seriously low monthly payments at the start.

But here's the catch, and it's a big one. When that interest-only period ends, your monthly payment will jump—sometimes dramatically. The loan essentially re-amortizes, meaning you now have to pay back the entire original loan amount, plus interest, over a much shorter remaining term. This "payment shock" can be a real financial jolt.

These are highly specialized loans. You might see a seasoned real estate investor use one to maximize cash flow on a rental property, but they carry significant risk and are rarely a good idea for the average homebuyer.

The Payment-Option ARM

The Payment-Option ARM is the rarest of the bunch, and frankly, you're unlikely to even see one offered anymore. These loans, more common before the 2008 housing crisis, gave borrowers a menu of payment choices each month: a tiny minimum payment, an interest-only payment, or a full principal-and-interest payment.

The danger was in that minimum payment. If you chose it, you often weren't even covering the interest for the month. That unpaid interest would get tacked right onto your loan balance, a scary situation called negative amortization. You could make payments every single month and watch your loan balance go up. Because of how risky they are, these loans have largely disappeared, but they’re a good cautionary tale about understanding exactly how your mortgage works.

This diagram helps visualize how the two key parts of your rate, the index and the margin, work together.

As you can see, your rate is simply the market index (which changes) plus your lender's margin (which doesn't). It's a straightforward formula, but the results can vary.

For the vast majority of borrowers here in Virginia, the Hybrid ARM offers the best balance of low initial payments and manageable risk. To see how these options stack up against more traditional financing, you can learn more about conventional loans in our detailed guide.

The Real Pros And Cons Of Choosing An ARM

Deciding between a fixed-rate mortgage's predictability and an ARM's initial low payments isn't a simple choice. It's a strategic one. An adjustable-rate mortgage isn't a one-size-fits-all solution; it's a specific tool for a specific job, and understanding its pros and cons is crucial to know if it's the right tool for you, especially in a fast-paced market like Northern Virginia.

The whole decision really comes down to a single, fundamental trade-off.

ARMs exchange long-term certainty for short-term affordability. This simple concept is the key to deciding if this type of loan is the right financial move for you.

Let's unpack what that really means by looking at the good and the not-so-good.

The Upside: Potential Benefits Of An ARM

The biggest draw of an ARM is obvious: a lower interest rate at the start. That translates directly into a smaller monthly payment for the first few years, which can be a game-changer for your budget and buying power.

- Increased Purchasing Power: In a competitive, high-priced area like Fairfax, that lower initial payment can make a world of difference. It could be what helps you qualify for a slightly larger loan, getting you into the neighborhood you really want or a home with that extra bedroom you need.

- Significant Initial Savings: The money you save every month during that fixed period is real cash in your pocket. You can use it to beef up your emergency fund, invest, knock out some high-interest credit card debt, or even tackle a few home improvement projects. It’s a chance to build a stronger financial foundation.

- Advantage in a Falling Rate Environment: Here's a neat trick—if interest rates happen to be falling when your loan is scheduled to adjust, your payment could actually go down. You’d get the benefit of better market conditions without having to go through the cost and paperwork of a full refinance.

For someone planning to sell their home before the fixed-rate period ends, an ARM can be a brilliant move. It lets you enjoy homeownership for a few years with a significantly lower cost of borrowing.

The Downside: The Inherent Risks Of An ARM

Of course, that flexibility comes with a flip side. The uncertainty of what your payment will be down the road is the main reason people hesitate, and it's a completely valid concern.

The biggest risk has a name: payment shock. This is what happens when your fixed period ends and your rate adjusts upward for the first time, causing a sudden and sometimes dramatic jump in your monthly payment. If your income hasn't kept pace or you haven't budgeted for the increase, it can put a serious strain on your finances.

Market volatility is the other major factor. While it's possible for your rate to go down, it's just as possible for it to climb if the economic index your loan is tied to spikes. Your rate caps are there as a safety net, but even with those in place, your payment could still rise to a level that feels uncomfortable, or worse, unaffordable.

This unpredictability is why ARMs aren't always the most popular choice. According to the FHFA's National Mortgage Database, ARMs have recently accounted for only 7-10% of new mortgages. That’s a far cry from the 35% share they held back in the mid-1980s when sky-high fixed rates pushed buyers toward any alternative they could find. You can dig into this historical data yourself by exploring the FHFA's public data sets.

Ultimately, an ARM requires an honest look at your own financial situation, your plans for the next five to ten years, and your personal tolerance for risk.

When An ARM Is A Smart Financial Move

Getting how an adjustable-rate mortgage works is one thing. Knowing when to use one is what really separates a savvy homebuyer from someone taking an unnecessary risk.

Think of an ARM not just as a loan, but as a financial tool. It’s built for specific situations, and when your personal timeline lines up with its structure, it can be a powerful way to save money and boost your buying power, especially here in the competitive Northern Virginia market. The trick is to have a clear, intentional plan. An ARM is almost never the right call for someone who plans on staying put for 30 years. It truly shines as a short-term solution for a long-term goal.

Planning To Sell Before The First Adjustment

This is the classic, most common reason to grab an ARM. If you know you're likely to move within the next five to seven years, why would you pay the higher interest that comes with a 30-year fixed loan? You'd be paying a premium for long-term security you'll never actually use.

We see this play out all the time in a few common scenarios:

- Job Relocation: Your career path often involves moving to a new city every few years.

- A Growing Family: You're buying that perfect starter home now but know you'll need more space once the kids get a little older.

- Military Families: Service members stationed in the Fairfax area often have assignments lasting three to five years. A 5/1 or 7/1 ARM fits that timeline like a glove.

In these cases, you get to fully enjoy the lower initial rate, save thousands of dollars on interest, and then sell the house long before the first rate adjustment ever kicks in. It’s a perfect match.

Expecting A Significant Income Increase

Another person who is a great fit for an ARM is a professional early in their career who is on a clear track for a big jump in income. Think medical residents finishing their training, lawyers on the partner track, or entrepreneurs whose businesses are about to take off.

The lower initial payments from an ARM can help you buy the home you really want now, even if a fixed-rate payment would feel a little tight on your current budget. The whole strategy is built on the confidence that when the rate is scheduled to adjust in five or seven years, your higher income will easily handle any potential payment increase. It’s a way to get your foot in the door of the housing market and start building equity sooner.

Betting On A Drop In Interest Rates

Trying to time the market perfectly is always tricky, but when interest rates are high across the board, many homebuyers use an ARM as a strategic bridge. The game plan is simple: get into a home with the ARM's lower starting rate, then refinance into a stable fixed-rate mortgage once the market rates have cooled off.

This approach requires keeping an eye on economic trends. A quick look at historical ARM rate trends shows they often follow the ups and downs of the broader economy. For example, the FRED series on 5/1-Year ARMs shows averages climbed to 6.06% in late 2022. But by early 2024, some ARM products were trending much lower, mirroring shifts in the market. Understanding these patterns helps you decide if an ARM is a smart tactical move while you wait for a better fixed-rate environment to emerge.

An ARM can serve as a calculated placeholder, allowing you to secure your home in a high-rate environment with the clear intention of refinancing into a more stable, lower-rate fixed mortgage when the market improves.

This gives you immediate savings and the flexibility to lock in a better long-term rate later. You aren't stuck with a high fixed rate from day one. For anyone looking to get into a home now, getting a handle on the fundamentals of how to save for a house is the perfect first step on this journey.

Comparing The Savings: A 5-Year Example

Let’s put some real numbers to this to see the impact. Here’s a look at the payments for the first five years on a $500,000 loan, comparing a common ARM to a standard fixed-rate mortgage.

5-Year Payment Comparison On A $500k Loan

| Metric | 5/1 ARM at 5.5% | 30-Year Fixed at 6.75% | 5-Year Savings |

|---|---|---|---|

| Monthly Payment (P&I) | $2,839 | $3,243 | |

| Monthly Savings | $404 | ||

| Total Payments (60 Months) | $170,340 | $194,580 | |

| Total 5-Year Savings | $24,240 |

The difference is crystal clear. The homebuyer who chose the 5/1 ARM would save over $24,000 in just the initial fixed-rate period. That’s a significant amount of money that could be used for investments, home improvements, or just building up your savings before you either sell the home or refinance the loan.

Getting The Right ARM In Virginia

Alright, let's move from the 'what' to the 'how.' You understand the moving parts of an ARM, but how do you actually get one here in Virginia? This isn't just about paperwork; it's about having a game plan to make sure the loan you choose actually fits your life and financial goals.

Getting approved for an ARM is a lot like qualifying for a fixed-rate mortgage, but with one key difference. Lenders will look a little closer at your ability to handle future payment shock. They need to see that you can not only afford the initial, lower payment but also a potentially higher payment once the rate starts adjusting. This means a solid credit score, steady income, and a good debt-to-income (DTI) ratio are non-negotiable.

Your ARM Application Checklist

Want to make the process as smooth as possible? Get your documents in order before you even apply. Think of it as painting a clear financial picture for the lender.

Here’s a quick list of what you'll need to pull together:

- Proof of Income: Grab your most recent pay stubs, the last two years of W-2s, and your federal tax returns.

- Asset Verification: Lenders want to see you've got the cash for a down payment and closing costs, so have recent bank and investment account statements ready.

- Credit History: The lender will pull your credit, of course, but it’s always a smart move to check it yourself first to catch any errors.

- Employment Verification: Be prepared for your lender to confirm where you work and how long you've been there.

For anyone seeing an ARM as a strategic entry into homeownership, getting the fundamentals right is key. That groundwork starts with a solid savings plan, so be sure you know how to save for a house before you dive in.

Common Pitfalls To Avoid

Navigating the world of ARMs means watching out for a few common traps. The biggest mistake we see? People get tunnel vision on that low introductory rate and completely gloss over the rate caps. Those caps—your initial, periodic, and lifetime limits—are your most critical safety feature. They define the absolute worst-case scenario for your payments, and ignoring them is a massive gamble.

Another classic pitfall is not having a concrete exit strategy. Maybe your plan is to sell or refinance before the rate ever adjusts. That's a great strategy, but life happens. What if the market shifts or your plans change? You absolutely need a backup plan in case you're in the home longer than you originally intended.

This is where partnering with a local mortgage broker like Mortgage Seven LLC really pays off. We help our Fairfax borrowers decode everything from the index and margin to the fine print on rate caps, making sure you walk away feeling confident, not confused.

Finding the right ARM takes more than a Google search; it takes careful planning and advice from someone who knows the local market. Our team at Mortgage Seven LLC is here to offer that personalized guidance to Virginia homebuyers. We take the time to really listen to your goals and match you with a loan that truly works for you.

Ready to see what’s possible? Schedule a no-obligation chat with us today and let's take the next step toward your new home, together.

A Few Common Questions About ARMs

It's one thing to understand how an ARM works on paper, but it’s another to feel confident about how it will affect your wallet and your life. That's completely normal.

Let's walk through some of the most common questions we get from homebuyers right here in Fairfax. Think of this as the practical, real-world advice that follows the technical explanation.

What Happens If I Can't Afford My New ARM Payment?

This is, without a doubt, the number one fear for anyone considering an ARM. The good news is that seeing a payment jump on the horizon doesn't have to end in disaster. The trick is to get ahead of the problem.

If you see rates are climbing and know your adjustment is coming up, you have options. Many people choose to refinance their ARM into a stable fixed-rate mortgage. For others, who perhaps only planned to be in the home for a few years anyway, selling the property is a straightforward solution. Sometimes, a loan modification might even be on the table. The most important thing is to call a mortgage expert months before the adjustment hits.

How Is The New Interest Rate Calculated When My ARM Adjusts?

When it's time for your rate to change, the math behind it is surprisingly simple. Your lender uses a formula that's set in stone from the day you sign your loan papers.

Index + Margin = Your New Rate

They'll look at the current value of whatever index your loan is tied to (like the SOFR), add your locked-in margin to that number, and that's it. That's your new interest rate until the next adjustment comes around. This is why paying attention to your index is so critical—it’s the only moving part in the entire equation.

For more detailed answers to other common mortgage questions, you can always explore our comprehensive FAQ page.

Are ARMs Still As Risky As They Were Before 2008?

This is a great question, and the answer is a firm no. The adjustable-rate mortgages on the market today are fundamentally different—and much safer—than the ones that contributed to the 2008 financial crisis.

After 2008, major regulations were put in place to protect borrowers. Protections like the Ability-to-Repay rule force lenders to make sure you can actually afford the loan, even if the rate were to rise significantly. These changes got rid of the riskiest loan products and built a much-needed safety net for homeowners.

Trying to figure out all the fine print on an ARM can feel overwhelming, but you're not in it alone. The team here at Mortgage Seven LLC is all about giving clear, honest guidance to homebuyers in Fairfax and throughout Virginia. We want to make sure you have everything you need to make a smart, confident decision.

If you're ready to see what your options look like, let's talk.