When you decide to refinance your mortgage, one of the first things your lender will likely order is a home appraisal. This isn't just a box-ticking exercise; it’s a professional, third-party opinion on what your home is worth right now, in the current market. Think of it as the lender's way of verifying that the asset—your home—is valuable enough to secure the new loan you’re asking for.

This appraisal directly impacts everything from your approval chances to the interest rate you'll get, and even how much cash you can pull out.

What a Refinance Appraisal Is and Why It Matters

Picture a refinance appraisal as an updated report card for your home. When you first bought it, the original appraisal confirmed its value. But markets change, neighborhoods evolve, and you’ve likely made improvements. The lender needs to know what your property is worth today to make a smart lending decision.

At its core, the appraisal is all about calculating your Loan-to-Value (LTV) ratio. It’s a simple but powerful formula: your loan amount divided by the home's appraised value. For instance, if you're looking to refinance a $300,000 mortgage and your home appraises for $400,000, your LTV is 75%. The lower that percentage, the less risky you look to the lender, which can open the door to some serious financial perks.

The Power of an Accurate Valuation

Getting a strong, accurate appraisal isn't just about getting the loan approved. It can fundamentally change the terms of your mortgage for the better.

- Better Interest Rates: Lenders save their best rates for borrowers with lower LTVs, usually below 80%. A solid appraisal that reflects your home's true value helps you clear that hurdle.

- PMI Elimination: If your LTV dips below that magic 80% mark, you can finally say goodbye to expensive Private Mortgage Insurance (PMI), which could save you a significant amount each month.

- Access to Equity: For anyone considering a cash-out refinance, the appraisal is everything. A higher valuation means more available equity, giving you more cash to work with for things like home renovations or paying down other debts.

An appraisal serves as the foundation of the refinance process. It validates the property as adequate collateral for the new loan, ensuring the lender’s investment is secure and confirming the homeowner's equity position in a fluctuating market.

The importance of a solid appraisal becomes even clearer when you look at market trends. For example, in Q2 2025, refinance applications jumped by a staggering 43% compared to the previous year. This spike highlights just how crucial a timely home appraisal is for establishing an updated LTV that can make or break a deal in a competitive market. You can read more on housing trends like these in the Milliman mortgage market report.

To put it simply, here's a quick look at why the appraisal plays such a central role in your refinance.

Why Your Refinance Appraisal Matters

| Purpose | Impact on Your Loan | Potential Benefit |

|---|---|---|

| Verify Collateral | Confirms your home's value is sufficient to secure the new loan. | Increases likelihood of loan approval and favorable terms. |

| Calculate LTV | Determines your Loan-to-Value ratio. | A lower LTV can unlock better interest rates. |

| Assess Equity | Establishes the amount of equity you have in your home. | Allows for PMI removal and determines cash-out potential. |

In the end, the appraisal provides a clear, data-backed picture that both you and the lender can rely on to move forward confidently.

How Is Value Determined?

So, how does an appraiser land on that final number? It's a mix of art and science. They start by physically inspecting your property—noting its condition, size, features, and any recent upgrades.

Then, they dive into the data, looking for recently sold homes in your immediate area that are as similar to yours as possible. These are known in the industry as "comparables" or "comps." By blending their on-site observations with hard market data, they create an unbiased and defensible opinion of value. To get a feel for the technology behind modern valuations, check out this comprehensive guide to real estate valuation software.

A favorable appraisal is truly a cornerstone of a successful refinance. Our detailed guide on refinancing your mortgage can walk you through the entire journey, from application to closing day.

Walking Through the Refinance Appraisal Process

The refinance appraisal can seem like a bit of a black box, but it’s really a clear, step-by-step evaluation. Once your refinance application is in, your lender gets the ball rolling. But here’s something most people don’t realize: your lender doesn’t just call up their favorite appraiser. To keep everything fair and unbiased, they have to order the appraisal through a neutral, third-party firm called an Appraisal Management Company (AMC).

The AMC then finds a licensed appraiser who knows your specific area and assigns them the job. Within a few days, that appraiser will reach out to you directly to schedule the on-site inspection. This is their chance to see your home in person, so having it tidy and easy to get around can only help.

The On-Site Inspection

When the appraiser walks through your door, they aren't there to critique your furniture choices. Their mission is to gather cold, hard facts about the property. The whole visit usually takes between one and two hours, and they're laser-focused on a specific checklist.

Here’s what they’re actually doing during that time:

- Measuring and Sketching: They'll walk the perimeter of your home, measuring it to confirm the total square footage and sketch out a basic floor plan. This is a critical piece of the value puzzle.

- Counting Rooms: An appraiser will do a physical count of bedrooms and bathrooms. A home with three bedrooms and two baths is valued differently than one with two bedrooms and one bath.

- Assessing Condition: They'll give your home a once-over, looking at the structural integrity—the roof, foundation, and windows—and the condition of major systems like your HVAC and plumbing.

- Noting Upgrades: This is your chance to shine. Any major improvements you’ve made, like a renovated kitchen, new flooring, or updated bathrooms, will be carefully noted. These can have a real impact.

The appraiser will also snap photos of every room, the front and back of your house, and a shot from the street. These images are required for the final report to give the lender a complete picture.

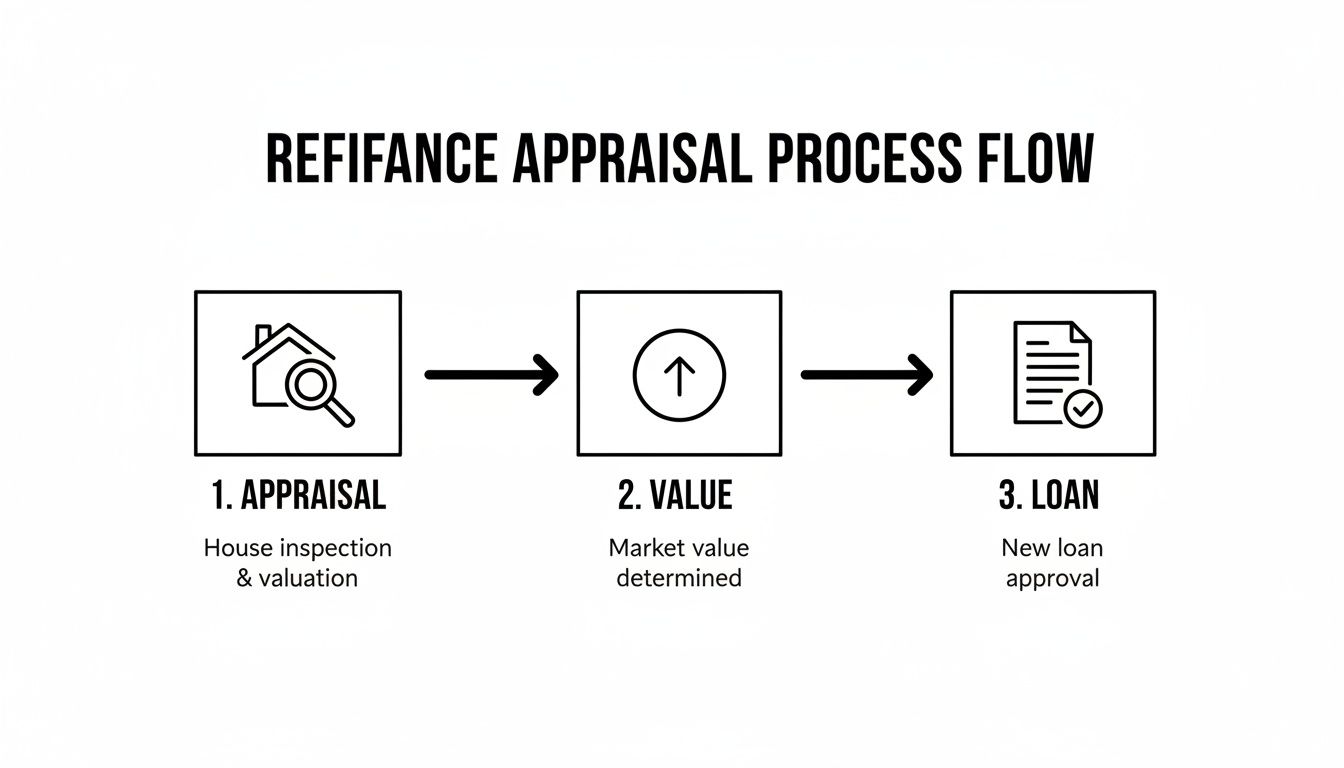

This flowchart maps out how these stages fit together, from the initial inspection to the lender's final decision.

As you can see, the physical appraisal directly feeds the valuation, which is the number your lender uses to structure your new loan.

Off-Site Analysis and Comparable Sales

Once the appraiser leaves your property, their work is only half done. Now comes the real analysis. They take all the data they collected and start digging into recent sales of similar homes in your immediate area. This is the search for comparable sales, or "comps," and it’s arguably the most important part of the process.

An appraiser’s final opinion of value isn’t just about your home in a vacuum. It’s about how your home stacks up against what other buyers have recently been willing to pay for similar properties nearby.

The goal is to find at least three homes that are a lot like yours, have sold in the last six months, and are ideally within a one-mile radius. From there, they make adjustments. For instance, if a comp sold for $500,000 but has a brand-new kitchen and yours doesn't, they'll adjust that comp's price down to make a fair comparison. If your home has an extra bathroom, they'll adjust the comp's price up.

Timelines and Costs You Can Expect

Knowing what to expect in terms of timing and cost can help you plan. The entire process, from the day the appraisal is ordered until the final report lands on your lender’s desk, typically takes about seven to ten business days. Of course, this can shift a bit depending on how busy local appraisers are or if your property is particularly complex.

The cost is also pretty standard. For a typical single-family home, you can expect the appraisal fee to be somewhere between $400 and $700. This is a fee you, the borrower, will pay—usually upfront when the appraisal is ordered. These steps are a core part of getting a mortgage, and you can get a better sense of the bigger picture by reviewing the steps in our mortgage approval processes. Think of it as an investment in getting the independent, professional opinion your lender needs to sign off on your new loan.

Key Factors That Influence Your Home's Value

When an appraiser comes to your home, they aren't just pulling a number out of a hat. Their job is to come up with an objective, well-supported opinion of value based on a mix of factors—some you can control, and some you absolutely can't.

Getting a handle on what appraisers look for is the best way to see your home through their professional eyes. Think of your property's value as a combination of three core elements: its interior features, its exterior condition, and its place in the local market.

What Matters Most Inside Your Home

Appraisers are trained to see past simple cosmetic touches. That fresh coat of paint in the living room is nice, but it won’t move the needle on your home's value nearly as much as a functional, long-lasting improvement.

The real heavy hitters are the kitchen and bathrooms. An outdated kitchen can drag down a home's value, while a modern one with quality countertops, updated appliances, and smart cabinetry is a major plus. The same goes for remodeled bathrooms—contemporary fixtures and finishes are always a solid investment.

Here are a few other interior features that pack a punch:

- A Smart Layout: An open, logical floor plan is a huge selling point. Homes with awkward, choppy layouts often feel smaller and less functional, which can negatively impact the valuation.

- Finished Living Space: If you've converted an unfinished basement into a family room, home office, or guest suite, you've directly increased the home's gross living area. That's a big deal.

- Major System Upgrades: A new HVAC system, a modern electrical panel, or updated plumbing might not be flashy, but they signal a well-maintained home. Appraisers see these as crucial indicators of a property's overall health and reliability.

These are the kinds of upgrades that provide a real return because they improve the fundamental livability of the house.

Exterior Condition And Curb Appeal

An appraiser’s evaluation starts the second they pull up to the curb. That first impression, what we call curb appeal, really does matter. A well-kept exterior sends a powerful message that the rest of the home has likely been cared for with the same level of detail.

But it’s about more than just a manicured lawn. The appraiser is also doing a serious assessment of the home's structural integrity.

A home's exterior is its first line of defense against the elements. An appraiser will carefully examine the roof, foundation, and windows to assess their age and condition, as these are some of the most expensive components to replace.

Putting off major maintenance here can lead to significant deductions in your appraised value. A roof that’s clearly at the end of its life is a major financial liability that the appraiser has to factor in. The same is true for a cracked foundation or old, drafty windows.

To help you distinguish between the big-ticket items and the smaller details, here’s a quick breakdown of what appraisers focus on.

Appraisal Value Factors At-a-Glance

| Factor Category | High-Impact Examples | Lower-Impact Examples |

|---|---|---|

| Interior Features | Updated kitchen & baths, finished basement, new HVAC system, logical floor plan | New paint, light fixtures, updated hardware, flooring |

| Exterior & Structure | Age/condition of roof, foundation integrity, updated windows, siding condition | Landscaping, fencing, deck/patio condition, fresh paint |

| Location & Market | Recent comparable sales ("comps"), school district rating, proximity to amenities | Neighborhood aesthetics, traffic patterns, specific street |

| General Property | Square footage (gross living area), number of beds/baths, functional garage | Walk-in closets, high-end appliances, smart home tech |

While cosmetic touches certainly improve a home's appeal, it's the high-impact, functional, and structural elements that truly drive the final number.

Location And The Power Of Comps

You can renovate a kitchen or replace a roof, but there's one thing you can't change: your home's location. The neighborhood, school district, and convenience to amenities play an enormous role in determining its value.

But the single most important factor in any appraisal for refinance is the data from comparable sales, or "comps." An appraiser’s final opinion of value is anchored in what similar homes in your immediate area have actually sold for recently. They’ll hunt for at least three properties that have sold in the last six months, ideally within a one-mile radius of your own.

From there, it becomes a process of adjustments. If a comp has a two-car garage and you only have one, the appraiser will adjust its sale price downward to normalize the comparison. If your home has an extra bathroom, they’ll adjust its value upward. It's a methodical, data-driven approach that ties your home’s value directly to the current market.

If you want to dig deeper into the professional techniques appraisers use, it's worth exploring the different real estate property valuation methods. Understanding these concepts gives you a clear picture of what really drives your home’s worth.

How to Prepare for a Successful Home Appraisal

Getting ready for a home appraisal isn’t about trying to pull a fast one on the appraiser. It's about making sure your home's true value is easy to see. A bit of prep work can make a world of difference, ensuring that every feature contributing to your home's worth is front and center. Think of it as setting the stage for one very important visitor whose opinion really matters.

This is especially true in a busy market. Just recently, refinance loan originations hit 688,502 in a single quarter—that's a 12% jump from the previous year. For every one of those homeowners, a solid appraisal was the key that unlocked a better mortgage. Your goal is simply to give the appraiser a clear, unobstructed, and positive view of your property.

Make a Powerful First Impression

Believe it or not, the appraiser’s evaluation starts the moment they pull up to the curb. Good curb appeal sends an immediate signal that the property is cared for. You don't need to hire a professional landscaper; small, thoughtful touches are often all it takes.

- Tidy the Yard: A freshly mown lawn, trimmed bushes, and a weed-free garden bed show you care.

- Clear the Path: Make sure walkways are swept and easy to navigate.

- Add a Pop of Color: A few cheerful flowers in a pot by the door or a fresh layer of mulch can make a huge impact.

These simple things communicate pride of ownership before the appraiser even knocks on the door, setting a positive tone for the whole visit.

Address Minor Repairs and Maintenance

An appraiser isn't a home inspector, but their trained eye will definitely catch signs of neglect. A handful of small, unresolved issues can create a general impression of a home that isn't properly maintained, which can subtly chip away at their final valuation.

Do a walkthrough of your own home and play detective. Look for these common culprits:

- Fix Leaky Faucets: That constant drip, drip, drip can be a red flag for potential plumbing problems.

- Check Doors and Windows: Make sure they open and close without a struggle.

- Replace Burned-Out Lightbulbs: A well-lit space feels bigger, brighter, and more inviting.

- Secure Loose Handrails: This is a basic safety item that appraisers are required to note.

Taking care of these little fixes shows that your property is in good working order and has been kept in great shape.

Declutter and Deep Clean

A clean, organized home just feels bigger and better maintained. Piles of clutter can shrink a room and, more importantly, might hide the very features the appraiser is there to see, like the condition of your floors and walls.

An appraiser's job is to see past your personal belongings and evaluate the property itself. A clean, open space lets them focus on the home’s "bones"—the layout, size, and structural condition—which leads to a far more accurate valuation.

Before they arrive, focus on creating a sense of openness. Clear off the kitchen and bathroom counters, tidy up closets, and maybe move a bulky piece of furniture to the garage for the day. A good, deep clean will make every surface shine and reinforce that feeling of a well-cared-for home.

Compile a Brag Sheet of Your Upgrades

Never assume the appraiser will automatically notice and appreciate every improvement you’ve poured your time and money into. They see dozens of houses a week, so it’s up to you to connect the dots for them. Create a simple, clear list of all the major upgrades you’ve made since you bought the home.

Your list should include:

- The Project: What you did (e.g., "Complete kitchen remodel," "New architectural shingle roof").

- The Date: When the work was completed.

- The Cost: What you spent, if you have the receipts handy.

Have this list ready to hand to the appraiser when they arrive. This isn't being pushy; it's being helpful. This documentation gives them concrete proof of the investments you've made that add real, measurable value, ensuring those big-ticket items are fully considered in the final appraisal for refinance. For more help getting organized, you can download our free homeowner's pre-appraisal checklist.

Navigating a Low Appraisal Without Panic

Getting your home appraisal back and seeing a number lower than you expected can feel like hitting a brick wall. It’s a genuinely frustrating moment, but it's important to remember this is often just a hurdle, not a dead end for your refinance. While your first reaction might be disappointment, your next move should be calm, strategic action.

A low appraisal can feel particularly frustrating when the market seems to be moving in the right direction. For instance, when the average 30-year fixed mortgage rate fell to 6.23% by late 2025—a nice drop from 6.81% a year earlier—it sparked a lot of interest in refinancing. In fact, that environment led to a 43% spike in refinance applications in Q2 2025. You can find more insights on these kinds of shifts in 2025 mortgage trends on FoundationMortgage.com. In a market like that, the appraisal plays a huge role, making it even more crucial to know your options if the value comes in low.

First Step: Review the Report for Errors

Before you do anything else, get a copy of the appraisal report and go through it with a fine-tooth comb. Appraisers are human, and mistakes absolutely happen. You’re not looking for opinions to argue with; you're looking for hard, factual errors that could have dragged down the valuation.

Check for these common slip-ups:

- Incorrect Square Footage: Is the gross living area listed correctly?

- Wrong Room Counts: Did they miss a bedroom or count only two bathrooms when you have three?

- Missing Major Features: Did the report leave out the brand-new deck, the finished basement, or the central air conditioning you just installed?

If you find a clear, data-based mistake, you have a solid foundation for a dispute.

Request a Reconsideration of Value

If you've spotted errors or feel the appraiser used weak comparable sales (we call them "comps"), your next step is to request a Reconsideration of Value (ROV). This is the formal process for presenting new evidence to the lender that suggests the first valuation was off the mark.

A successful Reconsideration of Value isn't about arguing your opinion; it's about providing better data. Your goal is to give the lender and appraiser new, compelling information they may have overlooked.

To build a strong case, you'll need to do a little homework. Look for recent sales of homes in your immediate neighborhood that are a much better match for your own than the ones in the report. For example, if the appraiser used a comp that was a foreclosure or is located on a much busier street, that's a legitimate point to raise. Present your findings clearly and professionally to your loan officer.

Explore Other Practical Solutions

So what happens if an ROV doesn't work out? Don't worry, you still have other cards to play. The best path forward really depends on your financial goals and the flexibility of your lender.

Here are a few other routes to consider:

- Negotiate with Your Lender: At the end of the day, the lender wants your business. If the appraisal is only slightly below the target, they might be willing to tweak the loan amount or terms to make the deal work.

- Bring Cash to the Table: For a cash-out refinance, a lower value directly impacts how much equity you can pull out. You may just need to lower your cash-out goal to fit within the lender's LTV requirements.

- Order a Second Appraisal: While it means paying another fee, getting a second opinion from a different appraiser is an option. Just be aware that many lenders have policies against "appraisal shopping," so it's critical to discuss this with your mortgage broker first. A professional at Mortgage Seven LLC can help you figure out if this is a worthwhile strategy for you.

A low appraisal for refinance is definitely a challenge, but with the right game plan, it's one you can almost always overcome.

When Can You Skip the Traditional Appraisal?

A full, in-person home appraisal has been a fixture of the mortgage process for decades, but it's not always a requirement anymore. Thanks to smarter technology and new ways of assessing risk, lenders now have several tools that can make your refinance appraisal faster and cheaper. For a growing number of homeowners, this means you might be able to skip the traditional appraisal completely.

The whole idea is to streamline the process for lower-risk loans. When a lender can confidently verify your home's value without sending someone out to measure the rooms, it saves everyone time and money. For you, that means a lower closing cost and a much quicker path to finalizing your new loan.

What is an Appraisal Waiver?

The best-case scenario is getting an appraisal waiver, sometimes called a Property Inspection Waiver (PIW). It’s exactly what it sounds like—your lender simply waives the need for an appraisal. Instead of having a person assess your home, they rely on a powerful algorithm known as an Automated Valuation Model (AVM).

Think of an AVM as a super-smart real estate database. It crunches huge amounts of public data in seconds, looking at things like:

- Recent, comparable home sales in your neighborhood

- Public property records and tax assessments

- Historical price trends for your specific area

If the AVM's valuation lines up with what the lender expects and your loan application is solid, they may just grant the waiver.

An appraisal waiver is essentially a vote of confidence from your lender. It means they see your property's value as a sure thing and your financial profile as low-risk, making a formal appraisal an unnecessary step.

Who Actually Gets a Waiver?

Appraisal waivers aren't handed out randomly; they're reserved for slam-dunk refinance scenarios where the lender sees very little risk.

You're a strong candidate for a waiver if you check these boxes:

- You Have a Low Loan-to-Value (LTV) Ratio: If you have a good chunk of equity in your home—typically an LTV of 80% or less—you’re in a great position.

- Your Credit History is Excellent: A high credit score shows you’re a reliable borrower, which lowers the lender's overall risk.

- You Have a Conventional Loan: Waivers are most common on conventional loans that are eligible for sale to Fannie Mae or Freddie Mac.

- Your Property is a Standard Type: Single-family homes and some condos with plenty of recent sales data are the easiest to value automatically.

If your loan application fits this profile, the lender's automated underwriting system might flag you for a waiver. This can easily save you a few hundred dollars and shave a week or more off your closing timeline.

Other Ways to Avoid a Full Appraisal

What if you don't qualify for a full waiver? You might still be in luck. Lenders often use other modern, less intrusive methods that fall somewhere between a full waiver and a traditional appraisal.

Here are a couple of common alternatives:

- Drive-By Appraisals: This is just what it sounds like. An appraiser drives by your home to confirm it's still standing and check its exterior condition from the street, but they never come inside. They then use that visual confirmation along with market data to come up with a value.

- Desktop Appraisals: The entire process is handled remotely from the appraiser's desk. They use AVM data, public records, tax information, and photos from past MLS listings to determine the value without ever setting foot near your property.

These options provide a nice middle ground. They give the lender the verification they need without the hassle and expense of scheduling a full interior inspection. Knowing they exist can help you have a more productive conversation with your loan officer about what to expect.

Got Questions About Your Refinance Appraisal? We've Got Answers.

When you're getting ready to refinance, the appraisal process can bring up a lot of "what ifs." Thinking through the practical side of things—like cost, timing, and how to prepare—is just as important as understanding the big picture.

Let's clear up some of the most common questions homeowners ask us.

Cost, Payment, and Timing

How much will a refinance appraisal set me back, and who pays for it?

You can typically expect an appraisal to cost somewhere between $400 and $700. This isn't a hard and fast rule, though; the price can tick up or down depending on your home's size, its unique features, and what appraisers are charging in your area. As the borrower, this fee is your responsibility, and it's usually paid upfront when the lender orders the report.

How long does an appraisal stay valid?

Most lenders will honor an appraisal report for 90 to 120 days. If your refinance closing gets pushed past that timeframe for any reason, don't be surprised if your lender asks for an updated appraisal. They need to be sure the value they're lending against still holds up in the current market.

Your Property and Past Appraisals

Will my messy house hurt my appraisal?

A little bit of everyday clutter isn't going to tank your home's value. But, if things are messy to the point where it looks like the home isn't well-maintained, it can send the wrong signal. A tidy, clean space simply makes it easier for the appraiser to do their job and shows your home in its best light.

Think of it this way: an appraiser is there to assess the property's bones—the layout, the fixtures, the overall condition—not your personal belongings. Helping them see those core features clearly just makes the whole process smoother and more accurate.

I just bought my house. Can't I just use the appraisal from my purchase?

Unfortunately, no. Lenders almost always require a brand new appraisal for a refinance. The real estate market is always in motion, and your home’s value could have easily changed since you first bought it. A fresh appraisal gives everyone an accurate, up-to-the-minute valuation for your new loan.

Navigating these details is what makes a refinance feel straightforward instead of stressful. The team at Mortgage Seven LLC is here to walk you through every part of the process, so you're never left guessing.

Ready to see what's possible? Schedule a consultation with our team today.