If you're self-employed, you know the drill. Your business is doing great, there's consistent money coming in, but your tax returns don't quite show the whole picture. All those smart, legal deductions you take to minimize your tax bill have an unfortunate side effect: they reduce the income traditional lenders see, often making a conventional mortgage impossible.

This is a huge hurdle for countless entrepreneurs. Lenders who only look at W-2s or tax returns are missing the real story of your financial strength.

What Are Bank Statement Loans and Who Are They For?

Bank statement loans were created to solve this exact problem. Instead of focusing on your tax-filed income, these loans look at the actual cash flow moving through your bank accounts over 12 or 24 months.

It’s a common-sense approach to lending that acknowledges the unique financial reality of being your own boss.

Think of it this way: Your tax return is a single, heavily edited snapshot of your business's profit after deductions. Your bank statements, on the other hand, are like a continuous video of your company's actual cash flow—the real money coming in and going out month after month.

This is the key difference. These programs, which fall under the category of Non-Qualified Mortgages, are built for people whose success doesn't fit into a standard W-2 box.

Who Is the Ideal Candidate?

These loans are a game-changer for professionals who have strong, consistent revenue but don't draw a regular salary. If any of these sound like you, a bank statement loan might be the perfect path to owning a home.

- Entrepreneurs & Small Business Owners: You have solid revenue, but your net income on paper looks low after all your business expenses are deducted.

- Freelancers & Gig Economy Workers: Your income comes from multiple clients and varies from one month to the next.

- Independent Contractors: You’re a consultant, real estate agent, or another 1099 professional with project-based earnings.

Here’s a quick breakdown of how these loans differ from the mortgages most people are familiar with.

Bank Statement Loan vs Traditional Loan At a Glance

| Feature | Bank Statement Loan | Traditional Loan |

|---|---|---|

| Income Verification | 12-24 months of bank statements (personal or business) | Tax returns (1040s), W-2s, and pay stubs |

| Primary Borrower | Self-employed individuals, freelancers, business owners | W-2 wage earners, salaried employees |

| Focus | Consistent revenue and cash flow | Tax-reported net income and debt-to-income ratio |

| Flexibility | More adaptable to non-traditional income streams | Rigid, standardized underwriting rules (Fannie Mae/Freddie Mac) |

As you can see, the entire philosophy is different. It’s about proving your ability to pay based on real-world cash flow, not just what's on a tax form.

Let’s put it into a real-world context. Imagine you're a successful consultant in Fairfax, Virginia. You’ve been running your own firm for three years, and your business accounts show consistent deposits averaging $40,000 a month. But after deductions, your tax returns show an adjusted gross income of only $65,000. A traditional lender sees that $65,000 number and turns you down.

This is exactly where we step in. A bank statement loan allows a lender to see the $40,000 in monthly cash flow, completely changing your borrowing power.

At Mortgage Seven LLC, we live and breathe these scenarios. We specialize in helping self-employed professionals across Fairfax and all of Virginia get the financing they deserve. We believe the hard work you put into your business should be what counts, not just what’s left over after tax season.

How Lenders Figure Out Your Real Income

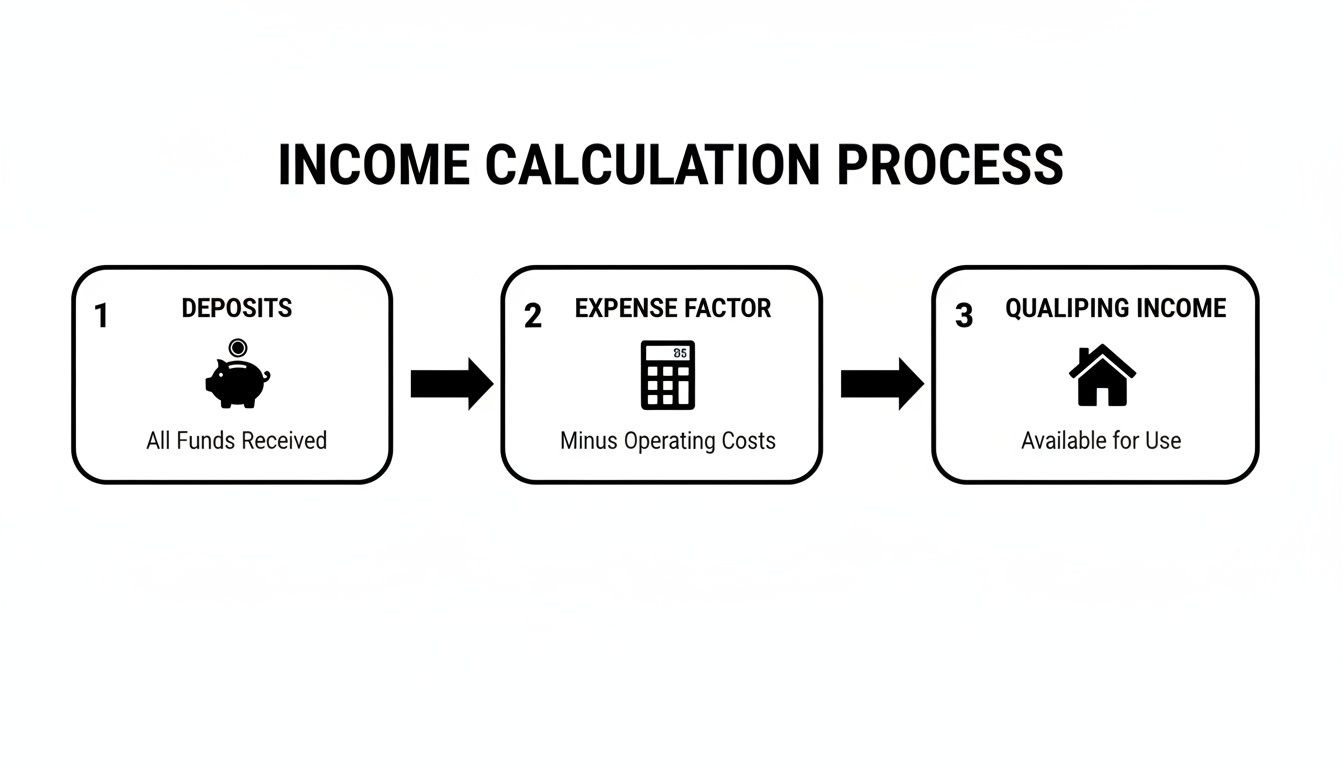

This is where the rubber meets the road. With a bank statement loan, figuring out your qualifying income isn't as simple as glancing at a W-2. It’s more like an investigation—a good one—where the lender pieces together the story of your business's true cash flow from your bank statements.

The whole point is to translate your gross deposits into a solid, dependable income figure that can be used to qualify you for a mortgage. Let's break down exactly how it's done.

The 12-Month vs. 24-Month Decision

First things first, you'll need to decide on a timeframe. Lenders will look at either 12 or 24 consecutive months of your bank statements. This isn't just a random choice; it's a strategic move that can seriously affect your borrowing power.

-

When 24 Months Makes Sense: Got a business with a steady, consistent track record? Using 24 months of statements is a fantastic way to showcase that stability. This longer view gives lenders a ton of confidence and is often preferred for bigger loan amounts or more complex financial situations.

-

When 12 Months Is Your Best Bet: Has your business taken off recently? If the last year was a banner year, a 12-month program is your friend. It lets the lender focus squarely on your most recent—and highest—earnings, which could help you qualify for a much larger loan than a 24-month average would.

Not sure which path is right for you? Your loan officer at Mortgage Seven LLC can help you run the numbers and see which option paints the most accurate and favorable picture of your finances.

The "Expense Factor": A Rule of Thumb for Costs

Lenders know that gross deposits aren't pure profit. Every business has costs, from rent and supplies to payroll and marketing. To account for this, they apply what's called an expense factor—basically, a standardized percentage deduction to estimate your net income.

Think of the expense factor as a general rule for profitability. The industry standard is often a 50% expense factor. This means the lender assumes that for every dollar your business brings in, 50 cents goes right back out to cover expenses.

Let’s see how this plays out with a quick example.

Example Calculation:

- Total Deposits Over 12 Months: $600,000

- Default Expense Factor: 50%

- Calculated Annual Expenses: $600,000 x 0.50 = $300,000

- Qualifying Annual Income: $600,000 (Deposits) – $300,000 (Expenses) = $300,000

- Qualifying Monthly Income: $300,000 / 12 = $25,000

That final number, $25,000 a month, is the income the lender uses to calculate your debt-to-income ratio and figure out how much you can comfortably borrow.

Boost Your Numbers with a CPA Letter

But what if you run a lean operation? A 50% expense factor might feel way off for a consultant, freelancer, or service-based entrepreneur whose actual costs are closer to 20% or 30%.

This is your chance to set the record straight. Most bank statement programs allow you to provide a letter from your CPA or licensed tax preparer verifying your actual, lower expense ratio. This one document can be a total game-changer.

Let's run our example again, but this time with a CPA letter confirming a 25% expense ratio.

Example with CPA Letter:

- Total Deposits Over 12 Months: $600,000

- Verified Expense Factor (from CPA): 25%

- Calculated Annual Expenses: $600,000 x 0.25 = $150,000

- Qualifying Annual Income: $600,000 – $150,000 = $450,000

- Qualifying Monthly Income: $450,000 / 12 = $37,500

Just like that, providing one letter bumped the qualifying monthly income by $12,500. That kind of difference can easily be what gets you into your dream home. A well-organized Profit & Loss statement can also do the trick, and our guide on creating a https://mtg7.com/PandL.html goes into more detail.

Personal vs. Business Bank Accounts

Finally, it matters whether your income flows into a personal or business account. Both are acceptable, but the math changes a little depending on which you use.

-

Business Bank Accounts: This is the most straightforward route. The lender adds up all your eligible business deposits and then applies the expense factor we just talked about. Simple.

-

Personal Bank Accounts: If you run your business income through a personal account, underwriters often change their approach. They will typically count 100% of the business-related deposits as qualifying income, assuming your expenses are paid from somewhere else. This can be a huge advantage, but it requires clean, well-organized statements to work.

To do all this analysis, underwriters need to digitize and process a mountain of data from your statements. Understanding how they convert bank statements to Excel gives you a peek behind the curtain at the detailed work that goes into building a strong case for your loan approval.

Meeting Credit and Down Payment Benchmarks

Once we've figured out your income from your bank statements, the next big pieces of the puzzle are your credit score and down payment. Many self-employed borrowers I talk to think they need a flawless financial profile to get approved, but that’s not really the case. Lenders in this niche are more flexible than traditional banks, though they still need to see you're a responsible borrower.

Think of your credit score and down payment as being on a seesaw. If you have a really strong credit score, you might be able to get by with a smaller down payment. If your score is a little bruised, a larger down payment can help balance things out and show the lender you have skin in the game.

What Credit Score Do You Need?

Forget the rigid, black-and-white rules of conventional loans. For bank statement loans, credit requirements are more of a sliding scale. A higher score will always get you a better deal, but you don't need to be perfect to get your foot in the door.

Most lenders start looking for a minimum credit score somewhere in the 620-640 range, and a few can even go as low as 580. But the real sweet spot starts at 680+, which opens up better rates. If you have a score of 700 or more, you'll be in the best position for the most competitive terms.

Down payments often follow the same pattern. Top-tier credit (720+) could mean a down payment as low as 10%. Most borrowers fall into the standard 15-20% range, while those with lower scores might need to bring 25-30% to the table. You can always discover more insights about these loan qualifications from experienced mortgage experts.

A credit score is the lender's quick snapshot of your financial reliability. A score of 720 or higher tells them you have a long history of managing debt well, which reduces their risk and earns you better terms. A score closer to 640 suggests a few past bumps, so they might ask for a larger down payment to balance that risk.

Ultimately, a strong credit history proves you’re a lower-risk borrower, and lenders will reward that with more attractive loan options.

How Your Down Payment Changes the Equation

Your down payment is your upfront investment in the property, and it’s a huge factor in a bank statement loan. Putting more money down reduces the lender's exposure, which can make all the difference—especially if your credit score isn't perfect.

The amount you'll need to put down is tied directly to a few key things:

- Your Credit Score: Like we discussed, a borrower with a 740 score buying their primary home might only need 10% down. On the other hand, someone with a 640 score should plan on putting down 20-25%.

- Property Type: How you plan to use the property matters a lot. Lenders see investment properties as a higher risk than the home you live in, so they almost always require a larger down payment—often 20-25% at a minimum, regardless of your credit score.

- Loan Amount: For bigger "jumbo" loans that go beyond the standard conventional limits, lenders will almost always ask for at least 20% down to offset the risk of that larger loan amount.

This flowchart gives you a visual of how lenders look at your deposits and apply an expense factor to determine the income they'll use for your qualification.

Seeing this process helps clarify why a solid down payment and a good credit score are so critical—they provide a strong foundation that complements the income side of your application.

Putting Your Full Document Package Together

Once you've got a handle on how your income will be calculated and you know where you stand with your credit and down payment, it's time to gather the paperwork. A strong bank statement loan application isn't just about the statements themselves. It’s about telling a complete financial story that shows lenders your business is the real deal—stable, profitable, and ready to take on a mortgage. Getting this package ready ahead of time is one of the smartest things you can do to keep the process moving smoothly.

Think of it like a business proposal. Your bank statements are the headline numbers, but it’s the supporting documents that provide the crucial context. This is what builds a lender's confidence and gets you to the closing table.

Proving Your Business Is Real and Active

First things first, lenders need to see that you're running a legitimate, ongoing business. This isn't just a box-ticking exercise; it's a core requirement to verify that you are genuinely self-employed.

You'll typically need to show them:

- Business Licenses: A current, valid license for your city or county.

- Proof of Self-Employment: This could be a letter from your CPA, your articles of incorporation, or business registration filings proving you've been operating for at least two years.

- Website or Professional Profile: A link to your business website or even a polished LinkedIn profile can go a long way in establishing your professional presence.

The Profit & Loss Statement

I know the whole point of this loan is to avoid tax returns, but lenders will almost always ask for a simple Profit & Loss (P&L) statement. This doesn't have to be complicated—you or your bookkeeper can likely put it together. It just needs to provide a clear summary of your business revenue and expenses for the last 12-24 months, backing up the numbers they see on your bank statements and supporting your claimed expense ratio.

When pulling these documents, it's helpful to know that tools like bank statement converter software exist, which can make it easier to organize and submit your financial data in a clean format.

The Power of a CPA Letter

As we touched on earlier, a letter from your CPA or licensed tax preparer is your secret weapon. It can dramatically boost your qualifying income by officially verifying an expense ratio lower than the lender’s standard 50% assumption. The letter should clearly state your business name, confirm your self-employment status, and specify the exact expense percentage for the period under review.

Verifying Your Down Payment and Reserves

It’s not just about income. Lenders need to be absolutely sure that the money you’re using for the down payment and closing costs is actually yours, and not a last-minute loan from an undocumented source.

This is what we call "seasoning" your funds in the mortgage world. Lenders will want to see bank statements (usually the last two or three months) for the account holding your down payment. They are looking to see that the money has been sitting there for at least 60-90 days. A large, sudden deposit will raise a major red flag and require a full paper trail to explain where it came from.

On top of that, lenders want to see you have a safety net after you close. These are your cash reserves, and the requirement is usually stated in terms of months of your future mortgage payment (which includes Principal, Interest, Taxes, and Insurance, or PITI).

- For a Primary Residence: Expect to need 3-6 months of PITI in reserves.

- For an Investment Property: This is often higher, typically 6-12 months of PITI.

This buffer shows the lender you can handle the mortgage payments without stress, even if business is a little slow right after you move in. To make sure you have everything in order, our mortgage application document checklist is a great resource to get organized.

How a Mortgage Broker Simplifies the Process

Trying to navigate bank statement loans on your own can feel like wandering through a maze where the walls constantly shift. Unlike standard mortgages with rigid, universal rules, the guidelines for bank statement loans can be wildly different from one lender to the next.

This is exactly why partnering with a savvy mortgage broker isn't just helpful—it's essential.

Think of us as your personal guide in the often-confusing world of lending. Instead of you spending countless hours applying to different lenders—each with their own unique appetite for risk and specific documentation rules—we do all the legwork for you. Here at Mortgage Seven LLC, we’ve already built strong relationships with a whole network of specialized lenders.

We know who’s a good fit for a freelance photographer and who’s better for a general contractor. That insider knowledge alone can save you an incredible amount of time, money, and headaches.

Finding the Right Lender for You

Your financial story is one of a kind, and your loan should be too. A one-size-fits-all approach just doesn't cut it when it comes to bank statement programs. Our entire job is to analyze your specific situation and match you with a lender whose guidelines are a perfect fit.

We routinely find solutions for all sorts of scenarios, including:

- Lower Credit Scores: Some lenders won't look at anything below a 700 score. We work with others who have fantastic programs for borrowers with scores in the 620-640 range. We know exactly who to call.

- Higher Loan-to-Value (LTV): Want to put less money down? We can connect you with lenders who will go up to 90% LTV, meaning you may only need 10% down if you qualify.

- Unique Business Structures: Whether you're a sole proprietor, run an S-corp, or juggle multiple businesses, we find lenders who get it and are equipped to work with your specific financial setup.

This tailored matchmaking is so important. If you go directly to a lender whose programs aren't designed for you, you're likely setting yourself up for a denial that wastes your time and adds an unnecessary inquiry to your credit report.

Your Strategic Partner in the Process

Working with Mortgage Seven LLC means you have a dedicated partner from day one. Our role goes way beyond just finding a lender. We offer hands-on guidance to help you assemble the strongest application possible, creating a clear and confident path to getting approved.

A great mortgage broker is both a translator and an advocate. We translate the lender’s complex jargon into plain English, and we advocate for you, making sure the underwriter sees the true strength of your financial picture.

Our team is here to help you accurately calculate your income to maximize what you can borrow. We’ll also help package your entire file—from the bank statements themselves to any necessary CPA letters—to tell your financial story in the most powerful way.

At the end of the day, our mission is to make this journey simple. We handle the complexity and leverage our lender network to clear the path between you and your home, ensuring the whole experience is as smooth and successful as possible.

Got Questions? We've Got Answers

Even after you've got the basics down, it’s completely normal to have a few more questions pop up about bank statement loans. It’s a specialized mortgage product, after all, and being thorough is just smart business.

Let's clear up any lingering doubts you might have. Below are the most common questions we hear from self-employed homebuyers, with straightforward answers to help you move forward with confidence.

Are the Interest Rates Higher on These Loans?

Yes, that’s generally true. You can expect the interest rate on a bank statement loan to be about 0.5% to 2% higher than what you’d see on a conventional loan. The exact rate depends on your whole financial picture, like your credit score and how much you're putting down.

Why the slightly higher rate? It comes down to risk. Lenders are using a non-standard way to verify your income, which takes more manual work and carries more uncertainty than looking at a W-2. That small premium on the rate is how they balance out that risk.

But for most self-employed borrowers, this is a trade-off that makes perfect sense. The ability to qualify for a mortgage based on your real cash flow—not just what’s left on your tax returns—is what opens the door to homeownership in the first place. At Mortgage Seven LLC, we hunt down the most competitive rates from our network of specialized lenders to make sure you get the best deal possible.

Can I Use a Bank Statement Loan for an Investment Property?

Absolutely. In fact, bank statement loans are a go-to tool for savvy real estate investors. Many successful investors run their portfolios like a business, making them perfect candidates for this kind of financing.

Lenders know this and have created specific bank statement programs just for investment properties. The qualification bar is usually set a bit higher than for a primary home, which is understandable given the nature of the investment.

Here's what that typically looks like:

- Bigger Down Payment: Plan on putting down at least 20-25%.

- More Cash Reserves: You'll likely need to have 6-12 months of mortgage payments (including taxes and insurance) sitting in a liquid account after you close.

These stricter rules give the lender peace of mind, showing you have a solid financial cushion to handle things like vacancies or unexpected repairs. We work with investors all the time and know exactly how to navigate these requirements to help you grow your portfolio.

How Many Months of Bank Statements Will I Need?

The magic numbers are typically 12 or 24 consecutive months. Choosing between them isn't about which one is "better" in general—it's about which one tells the best story about your business right now.

Looking at 24 months is a great way to show a lender long-term stability. It gives them a two-year history of your cash flow, which builds a ton of confidence, especially for larger loans or more complex businesses.

On the other hand, a 12-month program can be a game-changer if your business has really taken off in the last year. It lets the lender focus only on your most recent, higher-earning period, which could help you qualify for a much bigger loan than your 24-month average would support.

The right choice is a strategic one. An expert here at Mortgage Seven LLC can look at your cash flow trends and give you a clear recommendation on which path will get you closer to your goals.

What if My Business Deposits Are All Over the Place?

Welcome to the world of entrepreneurship! Inconsistent monthly income is a reality for most business owners, and lenders who offer these loans get it. They won't disqualify you just because you had a few slow months.

Instead of getting hung up on month-to-month fluctuations, underwriters focus on the big picture. Their job is to calculate a stable and dependable average income over the 12 or 24-month period. They simply add up all your eligible deposits and divide to get your qualifying income.

What matters more than consistent monthly totals is the consistency of your business activity. As long as you can show the business is active and healthy overall, irregular deposits aren't usually a deal-breaker.

A quick heads-up, though: any unusually large, one-off deposits that don't look like typical business revenue will get a second look. You'll probably need to provide a letter explaining where that money came from to prove it wasn't a loan. Transparency is always your best policy.

Figuring out the ins and outs of a bank statement loan can feel like a lot, but you don’t have to do it alone. The right guidance can be the difference between frustration and getting the keys to your new home.

At Mortgage Seven LLC, our team lives and breathes this stuff. We specialize in helping self-employed professionals in Virginia get the financing they’ve earned. We know how to take your unique financial story and present it in the strongest possible way.

Ready to see what’s possible?