Ever heard of a bank statement loan? It's a type of mortgage that lets you qualify based on your actual cash flow—the real money flowing into your bank accounts—instead of your tax returns. This loan was created specifically for self-employed professionals, freelancers, and business owners whose tax documents often don't tell the whole story about their income, thanks to all those necessary business write-offs.

Your Path to Homeownership Without Tax Returns

If you're an entrepreneur, looking at a standard mortgage application can be frustrating. The little boxes for W-2s and pay stubs just don't apply to how you earn a living. You know your business is healthy and pulling in consistent revenue, but your tax returns—carefully prepared with every legitimate deduction—paint a much leaner picture for a conventional lender. It’s a classic Catch-22 for some of the hardest-working people out there.

This is exactly the problem that bank statement loans were designed to solve.

Think of it less like a rigid tax audit and more like a real-world business performance review. Instead of fixating on your net taxable income, lenders look at your bank statements over a 12 or 24-month period. This gives them a clear, honest view of your actual cash flow and a much more accurate sense of what you can truly afford.

Who Truly Benefits from This Mortgage Solution

This kind of loan is a game-changer for a specific group of borrowers who don't fit the traditional 9-to-5 mold. If any of these descriptions sound like you, a bank statement loan could be the key to getting that mortgage.

- Self-Employed Professionals: Consultants, entrepreneurs, and sole proprietors whose income might vary month-to-month but shows a strong, consistent pattern of deposits over the year.

- Small Business Owners: People whose tax returns show a modest profit after business expenses are factored in, even though their gross revenue is more than enough to support a mortgage.

- Freelancers and Gig Workers: Creative professionals, digital marketers, and rideshare drivers who get paid from multiple clients and don't have a single, standard W-2.

- Independent Contractors: Professionals who work on a contract basis and have an income stream that's tough to verify with just pay stubs.

At its core, a bank statement loan recognizes a simple truth: for a modern business owner, consistent cash flow is often a much better measure of financial strength than the bottom line on a tax form.

For these borrowers, the issue isn't a lack of income; it's that the traditional paperwork doesn't fit. At Mortgage Seven LLC, we specialize in translating your real-world business success into a compelling mortgage application. We help Fairfax-area entrepreneurs show lenders their true financial picture, turning a common roadblock into a clear path to owning a home.

Working with a broker who really gets these specialized non-QM loan programs means you can move forward with confidence, knowing you have an expert in your corner.

How Lenders Calculate Your Income Using Bank Statements

So, how does a stack of bank statements transform into a clear, mortgage-ready income figure? It's not magic, and it's certainly not guesswork. Lenders who specialize in bank statement loans have a well-defined process for analyzing your cash flow to understand the real financial pulse of your business.

First things first, they need to see the big picture. That’s why they’ll ask for 12 or 24 months of consecutive bank statements. This long-term view helps them look past a single stellar month or a seasonal dip, giving them a reliable average of your company's revenue stream.

What they're hunting for is a consistent pattern of business-related deposits. This is the raw data they'll use to build your qualifying income.

From Gross Deposits to Qualifying Income

Once an underwriter has your statements, the real work begins. They don't just add up every credit in your account. Their job is to sift through the transactions and filter out anything that isn’t actual business revenue.

Common exclusions include things like:

- Transfers you've made from other personal or business accounts.

- Large, one-off deposits that are clearly out of the ordinary (like a capital injection, loan, or gift).

- Tax refunds and other credits that have nothing to do with your operations.

The whole point is to isolate the true gross income your business generates day in and day out. Lenders often use a secure bank statement converter to digitize and organize this data, making the analysis much more efficient and accurate. This initial scrub ensures the final calculation is based purely on your operational cash flow.

The Critical Role of the Expense Factor

After tallying up your average monthly gross deposits, the lender applies what's called an expense factor (or expense ratio). This is the absolute key to the whole calculation. The expense factor is a flat percentage the lender uses to account for your business's operating costs without ever needing to comb through your tax returns.

A standard expense factor for most business accounts is 50%. This means the lender simply assumes that for every dollar your business brings in, 50 cents goes right back out to cover things like inventory, marketing, rent, and payroll.

It's a straightforward, conservative approach. While your actual expenses might be higher or lower, lenders use this default ratio to determine your net operational profit. For certain industries, this ratio might be adjusted—especially if you can get a letter from your CPA—but 50% is the most common starting point. This method differs quite a bit from other programs, and our guide on how P&L statement loans offer another alternative is a great read if you want to compare the two.

A Practical Example of Income Calculation

Let's walk through a simple example to see how this plays out. Imagine you're a freelance consultant using 12 months of business statements for your loan application.

- Total Deposits: Over the last year, you deposited $240,000 from client payments into your account.

- Average Monthly Deposits: The lender divides that total by 12, which comes out to an average of $20,000 per month.

- Apply Expense Factor: Next, they apply the standard 50% expense factor. So, $20,000 x 50% = $10,000.

- Final Qualifying Income: Your final qualifying monthly income for the mortgage is $10,000.

This is the number the lender uses to calculate your debt-to-income (DTI) ratio and figure out just how much you can comfortably borrow.

This methodical approach is becoming more important as the financial world adapts to a new economy. The rise of bank statement loans reflects the massive growth in the self-employed workforce, now estimated at 15-20% of all U.S. workers, who are often shut out of traditional lending.

The table below gives you a month-by-month look at how this process unfolds, turning raw deposit figures into a solid, mortgage-ready income stream.

Sample Income Calculation from Business Bank Statements

This table illustrates how a lender might calculate qualifying monthly income for a self-employed borrower based on 12 months of business bank statement deposits.

| Month | Total Deposits | Calculated Monthly Income (with 50% Expense Ratio) |

|---|---|---|

| January | $18,000 | $9,000 |

| February | $22,000 | $11,000 |

| March | $19,500 | $9,750 |

| April | $21,000 | $10,500 |

| May | $23,000 | $11,500 |

| June | $17,500 | $8,750 |

| July | $24,000 | $12,000 |

| August | $20,000 | $10,000 |

| September | $18,500 | $9,250 |

| October | $25,000 | $12,500 |

| November | $26,500 | $13,250 |

| December | $25,000 | $12,500 |

| 12-Month Average | $21,667 | $10,833 |

As you can see, even with fluctuating monthly deposits, the lender arrives at a stable, predictable qualifying income—$10,833 in this case—by averaging it out over the full year.

Comparing Your Mortgage Options Side-by-Side

Picking the right mortgage can feel like staring at a wall of tools, wondering which one will actually get the job done. Every loan program is built for a specific kind of borrower, so knowing the key differences is everything. This is especially true for entrepreneurs, investors, and anyone else who doesn't fit neatly into a W-2 box—your options are far better and more flexible than you might think.

This breakdown is designed to cut through the jargon and stack up bank statement loans against the other common players. By looking at who they're for, what they demand, and how they function, you’ll be able to see exactly which path makes sense for your financial story.

The Four Main Paths to Financing

For the self-employed and property investors, the mortgage world isn't a one-size-fits-all game. Lenders have developed several distinct ways to evaluate your ability to pay back a loan, and most of them look far beyond your tax returns.

- Bank Statement Loans: This is the lifeline for business owners who show strong, consistent cash flow but also have significant tax write-offs. Lenders simply use 12-24 months of bank deposits to prove your income. It's a real-world approach.

- Conventional Loans: The gold standard for salaried employees. These loans live and die by your tax returns, W-2s, and pay stubs to calculate what you can afford.

- P&L Statement Loans: A great middle-ground option. Here, a Profit & Loss statement prepared by your CPA is used to demonstrate your business's health, often with less paperwork than a conventional loan.

- DSCR Loans: Built exclusively for real estate investors. This loan doesn't care about your personal income at all. The only question it asks is: does the property's rent cover the mortgage payment?

Choosing the right loan isn't about which one is "best"—it's about which one best reflects your financial reality. A conventional loan is perfect for a salaried employee, while a bank statement loan is a game-changer for a thriving entrepreneur.

It's no surprise these alternative loans are gaining serious traction. Bank statement loans have become a go-to for entrepreneurs and gig workers who are shut out by traditional income verification. In fact, industry trends suggest that non-qualified mortgage (non-QM) products like these could soon account for 10-15% of all new mortgages. We're seeing a 25% year-over-year jump in applications from self-employed borrowers alone.

Yes, the rates can be a bit higher—often 1-2% above conventional loans—but the approval rates for qualified entrepreneurs have hit 75% in recent years. You can discover more insights about the rise of bank statement loans to see just how much the market is shifting.

Loan Program Comparison for Self-Employed Borrowers and Investors

To make it even clearer, this table breaks down the crucial differences between these mortgage types. Use it to quickly pinpoint which program aligns with your financial profile, whether you're buying a home to live in or an asset to grow your portfolio.

| Feature | Bank Statement Loan | Conventional Loan | DSCR Loan |

|---|---|---|---|

| Ideal Borrower | Self-employed, freelancers, small business owners | W-2 employees with stable, documented income | Real estate investors (for investment properties only) |

| Income Verification | 12-24 months of business or personal bank statements | Tax returns, W-2s, pay stubs | Property's rental income (or projected rent) |

| Primary Advantage | Qualifies based on cash flow, not taxable income | Lowest interest rates and fees available | No personal income verification required |

| Common Use Case | Buying a primary residence or second home | Standard home purchase for traditional employees | Purchasing or refinancing rental properties |

| Typical Down Payment | 10% – 25% | As low as 3% | 20% – 30% |

This comparison really highlights the trade-offs. A conventional loan gets you the best rates, but its rigid paperwork rules out millions of successful business owners. A bank statement loan closes that gap, offering a direct path to homeownership by focusing on what truly matters for an entrepreneur: consistent cash flow.

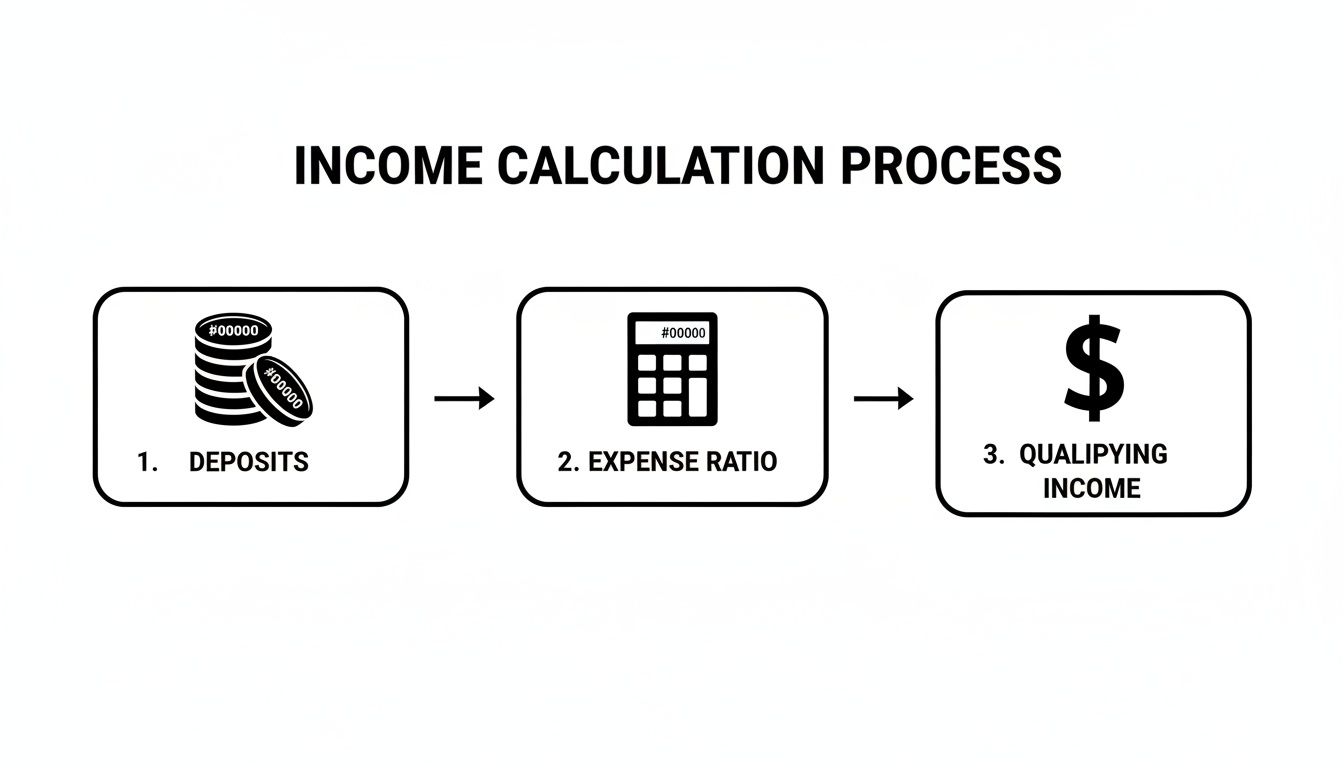

And how do lenders turn that cash flow into an income figure they can use? It’s simpler than you think.

As the flowchart shows, the lender takes your total deposits, applies a standard expense ratio, and arrives at a final qualifying income. It’s a logical process that turns raw revenue into a bankable number.

Navigating these options takes experience. At Mortgage Seven LLC, we don't just push paper; we act as your strategic partner. We're here to guide you through these choices and help you build the financial story that gets your loan approved.

Navigating the Application Process From Start to Finish

Embarking on the bank statement loan journey might seem daunting, but when you know the key milestones, it's a very predictable path. Think of it like a well-managed project with clear phases, each one bringing you closer to closing day. An expert broker from Mortgage Seven LLC essentially acts as your project manager, guiding you through each step to make sure nothing falls through the cracks.

The whole process is designed to be thorough, yet it’s often faster than people expect. We see strong demand for these specialized loans, even as the broader market shifts. Investment-grade bank loan volumes hit $244 billion in the first quarter of this year, and a 25% jump in refinancing points to real stability in these niche mortgage products. For our clients in Fairfax, getting to the closing table in under 30 days is a huge plus. You can learn more about bank loan market trends and how they shape what we do.

Phase 1: Initial Consultation and Pre-Approval

Everything starts here. This is our chance to sit down and talk about your goals, your financial picture, and what you’re looking to borrow. The main objective is to make sure we're on the same page and that a bank statement loan is genuinely the right tool for the job.

You'll give us a high-level overview of your income and credit, and we’ll run a soft credit check. This lets us issue a solid pre-approval, which is exactly what you need to make a strong, confident offer on a home.

Phase 2: Gathering Your Core Documents

Once we have a strategy, it's time to gather your paperwork. This is where you really build the financial story for the lender. Forget W-2s and tax returns; your bank statements are the star of the show.

Here’s what your document package will almost always include:

- 12 or 24 Months of Bank Statements: These can be from your business or personal accounts—whichever best reflects your true income.

- Business License or Proof of Self-Employment: This simply confirms that your business is legitimate and operational.

- Photo Identification: A standard requirement for any home loan.

- Letter from a CPA (If Applicable): Sometimes, a quick letter from your accountant verifying your business expense ratio can help you qualify for a larger loan.

Having these documents ready to go from the start makes a world of difference. To make it easy, we put together a complete mortgage application checklist that lists out everything you'll need.

Phase 3: Underwriting and Conditional Approval

With your file complete, it moves on to the underwriter. This is the person who has the final say. They will meticulously review your bank statements, calculate your average monthly income, and assess your overall credit profile. Their job is to verify that your cash flow is consistent enough to comfortably support the new mortgage payment.

After this deep dive, you’ll receive a conditional approval. This is a huge milestone. It means the lender is on board with your loan as long as we can satisfy a few final conditions, like a good home appraisal.

Phase 4: Appraisal and Final Approval

With that conditional approval locked in, the lender orders an independent appraisal of the property. The appraiser’s sole focus is to confirm that the home’s market value aligns with the loan amount you’re requesting. While that’s happening, you’ll work with your broker to check off any final items the underwriter asked for.

Once the appraisal comes back clean and all conditions are met, you get the two best words in real estate: "clear to close." That’s the official green light. Your bank statement loan is fully approved, and all that's left is to schedule the closing, sign the papers, and get the keys to your new home.

Weighing the Pros, Cons, and Costs of a Bank Statement Loan

Like any specialized financial tool, a bank statement loan has its own unique mix of powerful advantages and potential trade-offs. Getting a clear picture of both sides of the coin is the key to making a confident, smart decision about your mortgage. It’s not just about finding a loan; it's about finding the right one for your life and business.

At Mortgage Seven LLC, we believe in total transparency. Our job is to empower you to weigh these factors clearly, so let’s break down exactly what you can expect—from the game-changing benefits to the practical costs you'll need to plan for.

The Major Advantages: A Lifeline for Entrepreneurs

The biggest win here is obvious: these loans finally open the door to homeownership for millions of successful business owners who are shut out of the traditional mortgage market.

- Income Verification That Reflects Reality: Forget tax returns that are strategically (and legally) minimized with deductions. These loans look at your actual cash flow, allowing you to qualify based on the true financial muscle of your business.

- Access to Higher Loan Amounts: Because your income is calculated from gross deposits, you can often qualify for a much larger loan than you would with a conventional mortgage. That can make all the difference in a competitive real estate market like Fairfax.

- Keeps Your Financials Private: Your detailed business expenses and tax strategies stay between you and your accountant. The lender’s focus is squarely on your revenue, not a line-by-line audit of your tax filings.

For a self-employed person, a bank statement loan isn't just about financing—it's about validation. It acknowledges that consistent cash flow is the real heartbeat of a healthy business and gives you a direct path to leveraging that success.

The Trade-Offs: What to Expect on the Other Side

While bank statement loans are a fantastic solution, they do come with certain trade-offs that reflect the lender’s increased risk. It's crucial to go into the process with your eyes wide open to these realities.

First, interest rates are typically higher than those for conventional loans. You can generally expect rates to be somewhere in the range of 1% to 2.5% higher, depending on your credit profile and down payment. Think of this premium as the lender's way of balancing the risk of using a non-traditional way to verify your income.

Second, a larger down payment is almost always required. While some conventional loans let you get in the door with as little as 3% down, most bank statement loan programs require a minimum of 10% to 20% of the purchase price. A bigger down payment proves your financial stability and gives the lender more security.

Finally, credit score requirements are often stricter. Lenders need to see a strong history of responsible credit management. While some programs have minimums in the low 600s, a credit score of 720 or higher is what will get you access to the very best terms and rates available.

Breaking Down the Associated Costs

Beyond the down payment, you'll also need to budget for closing costs. Many of these are standard for any mortgage, but a few can be slightly different with a non-QM loan.

- Origination Fees: This is the fee the lender charges for processing your loan. It can sometimes be a bit higher for bank statement loans simply because the underwriting process is more hands-on.

- Appraisal and Title Fees: These are standard costs you'd find in any real estate transaction and will be very similar to what you’d pay for a conventional loan.

- Points: In some cases, you might have the option to buy "points" to lower your interest rate. This is a strategic financial choice that your loan officer can help you evaluate to see if it makes sense for you.

Understanding these pros, cons, and costs right from the start allows you to plan effectively. At Mortgage Seven LLC, we make it a point to walk you through a detailed cost analysis, ensuring there are absolutely no surprises on your way to the closing table.

Why Partner With Mortgage Seven for Your Loan

Let's be honest: navigating the world of bank statement loans can feel like a maze, especially when you're self-employed. But it doesn't have to be. Choosing the right guide is just as critical as choosing the right loan, and that's where we come in. Here at Mortgage Seven LLC, we don’t just process paperwork; we build winning homeownership strategies for entrepreneurs right here in the Fairfax, Virginia, community.

Our team lives and breathes non-qualified mortgages (non-QM). We get the unique rhythm of a freelancer's income or a small business owner's cash flow because we work with people like you every single day. This isn't just another loan product on a long list for us—it's our specialty.

Your Advocate in a Complex Market

Think of us as your personal advocate in the lending world. We’ve spent years building strong relationships with a network of lenders who actually get the self-employed story. So, instead of you cold-calling banks hoping to find one that understands your finances, we bring the right lenders directly to the table.

This access is a game-changer. It means we can:

- Shop for genuinely competitive rates on your behalf, making sure you get the best terms out there.

- Pinpoint programs with flexible guidelines that actually fit your unique financial picture.

- Frame your application to highlight its strengths for underwriters who specialize in these exact loans.

We essentially translate your business success into a language that lenders respect. Our job is to help you sidestep the common pitfalls that trip up so many self-employed borrowers, building a rock-solid case for your approval right from the start.

Partnering with an expert broker means you’re not just submitting a form; you're presenting a professionally crafted financial narrative. We make sure your true borrowing power shines through, turning what could be a roadblock into a clear path forward.

From Consultation to Closing Day

Whether you're a first-time homebuyer ready to put down roots or a seasoned investor looking to grow your portfolio, our specialized knowledge makes a real, tangible difference. We're with you for the entire journey, from figuring out which documents you need all the way to signing the final papers on closing day.

Your homeownership dream isn't a long shot. It just needs a clear plan.

Ready to see what a bank statement loan can do for you? Schedule your no-obligation consultation with our team today. Let's map out a strategy to turn your vision of owning a home into a reality.

Got Questions? We've Got Answers.

Even after you've got the basics down, a few questions about bank statement loans might still be bouncing around in your head. That's completely normal. Let's tackle some of the most common ones we hear from entrepreneurs and freelancers just like you.

Can I Use a Bank Statement Loan to Refinance?

Yes, absolutely. Bank statement loans aren't just for buying a new home—they're a fantastic tool for refinancing, too.

Self-employed homeowners often use them for two main reasons:

- A rate-and-term refi: This is where you swap out your old mortgage for a new one, usually to get a lower interest rate or change the loan's length (like going from a 30-year to a 15-year). The goal is typically to lower your monthly payment.

- A cash-out refi: This lets you pull cash from your home's equity. It's a popular move for funding a business expansion, tackling a major home renovation, or paying off higher-interest debt.

No matter which path you choose, the qualification process is the same. We'll look at your business's cash flow through your bank statements, not your tax returns.

What's the Minimum Credit Score I Need?

While every lender is a bit different, a good rule of thumb is a minimum credit score somewhere between 620 and 680. A few lenders might dip into the low 600s, but honestly, it’s best to aim higher.

A strong credit score—think 720 or above—is your golden ticket. It dramatically boosts your chances of approval and helps you lock in a much better interest rate. For a non-traditional loan like this, lenders really want to see that you've got a great track record of managing your finances.

Are the Interest Rates Way Higher?

Let's be upfront: yes, interest rates on bank statement loans are typically higher than what you'd find on a conventional mortgage. You can generally expect them to be anywhere from 1% to 2.5% higher. This extra bit is how lenders balance the risk they take by not using standard W-2s or tax returns to verify your income.

But that rate isn't set in stone. It's a moving target influenced by your credit score, how much you put down, your debt-to-income ratio, and your overall financial health. A good broker will take your loan profile to multiple lenders to hunt down the most competitive rate out there for you.

What Happens If I Have a Large, One-Time Deposit?

Underwriters are trained to spot patterns. They’re looking for the regular, predictable income that flows from your day-to-day business activities. A sudden, unusually large deposit—like an inheritance, a loan from a family member, or money from selling a major asset—is going to raise a red flag.

More often than not, these one-off deposits will be excluded from the final income calculation. You'll definitely be asked to write a letter of explanation and show paperwork proving where the money came from. The strongest applications always show a consistent, steady stream of business revenue.

Ready to see what's possible? The team at Mortgage Seven LLC lives and breathes this stuff—we specialize in helping self-employed borrowers navigate their home financing options. Let us give you a clear, no-pressure look at where you stand and find the right loan for your goals.

Start your journey by visiting us at https://mtg7.com today.