For entrepreneurs, freelancers, and small business owners, the path to securing a home loan can feel uniquely challenging. Traditional mortgage underwriting heavily relies on W-2s and pay stubs, which don't accurately reflect the financial reality of a self-employed individual. Your tax returns, often optimized for deductions, can show a lower net income than your actual cash flow, making it difficult to qualify for the loan you deserve.

This is a common frustration, but it is not a dead end. The solution lies in finding the right lender, one that specializes in non-traditional income verification and understands the nuances of entrepreneurial finances. This guide is designed to cut through the complexity and directly connect you with the best mortgage companies for self employed borrowers. We will explore the critical differences between standard (QM) and non-standard (Non-QM) loans, focusing on powerful tools like bank statement loans, P&L programs, and DSCR loans for investors.

Compiling extensive financial records is a key step in this process. To streamline document preparation and ensure all your financial data is organized and ready for underwriter review, consider utilizing bank statement converter software, which can simplify an otherwise time-consuming task.

Instead of facing rejection from conventional banks, you can partner with companies that are built to serve you. We've curated a detailed list of the top lenders in this space, complete with screenshots and direct links. For each company, we break down their unique strengths, specific loan programs, and who they serve best, so you can confidently move from business owner to homeowner.

1. Mortgage Seven LLC

Mortgage Seven LLC distinguishes itself as a premier mortgage brokerage, particularly for self-employed individuals, real estate investors, and those with complex financial profiles. Rather than operating as a direct lender with a limited menu of loan products, Mortgage Seven functions as a strategic partner, leveraging its extensive network of wholesale lenders. This broker model is a significant advantage for entrepreneurs and business owners, providing access to a much broader and more flexible array of financing solutions than a traditional bank can offer.

The firm, based in Fairfax, VA (NMLS #2124799), excels in navigating the unique documentation challenges that self-employed borrowers face. Instead of relying solely on traditional tax returns, which often don't reflect a business owner's true cash flow due to deductions and write-offs, they specialize in alternative income verification methods. This expertise makes them one of the best mortgage companies for self employed borrowers seeking tailored financing.

Core Strengths for Self-Employed Borrowers

The primary advantage of working with Mortgage Seven is its deep expertise in Non-Qualified Mortgages (Non-QM). These loans are designed for borrowers who don't fit the rigid criteria of conventional financing. For the self-employed, this means access to specialized programs that can make homeownership achievable.

Key Loan Programs Offered:

- Bank Statement Loans: Allows borrowers to qualify based on business or personal bank statement deposits over a 12 or 24-month period, bypassing the need for tax returns.

- Profit & Loss (P&L) Statement Loans: Utilizes a P&L statement, often prepared by a CPA, to demonstrate income and business profitability.

- Debt-Service Coverage Ratio (DSCR) Loans: Ideal for real estate investors, this loan qualifies borrowers based on the rental property's income potential, not personal income.

- ITIN Loans: Provides financing options for non-permanent resident aliens who have an Individual Taxpayer Identification Number.

- Jumbo and Construction Loans: Offers solutions for high-value properties and new construction projects that often require more complex underwriting.

This diverse product suite ensures that Mortgage Seven can find a viable path to financing for nearly any well-qualified but non-traditional applicant. You can find more details about their Non-QM loan options to see how these programs work.

User Experience and Process

Mortgage Seven emphasizes a client-first approach characterized by personalized guidance and efficient processing. Client testimonials frequently praise the firm, and specifically loan officer Amer Samman, for responsiveness, deep industry knowledge, and the ability to close loans quickly. The process is designed to be transparent, with loan officers taking the time to explain all costs, terms, and potential hurdles so borrowers can make informed decisions.

While specific pricing isn't listed on their website (as rates and fees vary by lender and loan scenario), their value proposition is clear: they shop the wholesale market on your behalf to secure competitive terms that are often better than what borrowers could find on their own.

Pros and Cons

| Pros | Cons |

|---|---|

| Exceptional Loan Diversity: Access to bank statement, P&L, DSCR, and other Non-QM loans tailored for entrepreneurs. | Variable Pricing: As a broker, final costs and compensation are not standardized and depend on the chosen lender. |

| Broker Advantage: Ability to shop multiple wholesale lenders to secure competitive rates and favorable terms. | Third-Party Dependency: Final approval and timelines are subject to the underwriting processes of external lenders. |

| Personalized Service: High-touch, transparent guidance from application to closing with a focus on education. | |

| Proven Track Record: Consistently high client satisfaction and positive reviews highlighting speed and expertise. |

Website: https://mtg7.com

2. LendingTree

LendingTree isn't a direct lender but a powerful online marketplace. For self-employed borrowers, its primary value is efficiency. Instead of applying to multiple lenders one by one, you can fill out a single, streamlined form and receive competing offers from a network of lenders, some of which are among the best mortgage companies for self employed individuals seeking both traditional and alternative documentation loans.

This approach is particularly useful for finding specialized Non-QM products like bank statement loans. Because LendingTree’s network is so broad, you are more likely to connect with lenders who have an appetite for this type of underwriting without having to search for them individually. The platform is free for borrowers; lenders pay to be part of the network and compete for your business.

Why It’s Great for Self-Employed Borrowers

The biggest advantage is comparison shopping at scale. A self-employed applicant might get a "no" from a conventional bank but a "yes" from a Non-QM lender. LendingTree puts both types of lenders in front of you, providing a clear view of your available options and a competitive landscape for interest rates and fees.

The initial prequalification process often uses a soft credit check, which means you can explore potential offers without an immediate impact on your credit score. This is a critical feature when you're in the early stages of rate shopping.

Key Features and Offerings

| Feature | Description for Self-Employed Borrowers |

|---|---|

| Loan Comparison | Access multiple offers for conventional, FHA, VA, Jumbo, and Non-QM loans (including bank statement and P&L programs). |

| Prequalification | Typically uses a soft credit inquiry to provide initial quotes, protecting your credit score during the shopping phase. |

| Educational Resources | The site provides articles and guides explaining the complexities of self-employed income calculation and documentation. |

| User Experience | The online form is intuitive and guides you through the necessary financial inputs required for a mortgage application. |

Pros and Cons

- Pro: Saves significant time by submitting your information once to reach multiple lenders.

- Pro: Broadens your access to a mix of national banks, credit unions, and specialty Non-QM lenders.

- Con: Expect a high volume of calls and emails from lenders once you submit your information.

- Con: The initial offers are estimates; you must still complete a full application and provide documentation to the specific lender you choose.

Best For:

LendingTree is ideal for the self-employed borrower who wants to cast a wide net and quickly compare real-world interest rates from multiple sources. It’s perfect for those who are comfortable with receiving outreach from several lenders and want to ensure they aren't missing out on a better deal.

Website: LendingTree for Self-Employed Mortgages

3. Bankrate

Bankrate is not a lender but an authoritative financial publisher that provides meticulously researched guides and "Best Of" lists. For self-employed individuals navigating the mortgage process, Bankrate acts as an essential educational hub and a launchpad for identifying potential lenders. Its value lies in its transparent editorial process, offering vetted shortlists of the best mortgage companies for self employed borrowers, complete with detailed methodologies.

Unlike marketplaces that send your information to multiple lenders, Bankrate empowers you with knowledge first. It publishes in-depth guides on topics like using bank statements to qualify and provides practical documentation checklists. This allows self-employed applicants to prepare their financial files thoroughly before ever speaking with a loan officer, significantly improving their chances of a smooth approval process.

Why It’s Great for Self-Employed Borrowers

The primary advantage is preparation. Bankrate’s content demystifies the complex requirements for self-employed mortgages, explaining how underwriters view your income and what documents you'll need. By reviewing their lender comparisons, which often include minimum credit scores and down payment requirements, you can pre-screen potential partners and avoid applying with institutions that are unlikely to approve your loan type.

This educational approach helps you understand the landscape of both conventional and Non-QM loans before you commit to a hard credit pull. It gives you the confidence to ask lenders the right questions and evaluate their offerings more effectively.

Key Features and Offerings

| Feature | Description for Self-Employed Borrowers |

|---|---|

| Vetted Lender Lists | Curated "Best Mortgage Lenders" lists often highlight companies offering bank statement or other Non-QM programs. |

| In-Depth Guides | Provides detailed articles and checklists explaining how to prepare your application, calculate income, and what to expect. |

| Lender Comparisons | Side-by-side comparisons of lender requirements, including minimum credit scores and down payment options. |

| Transparent Methodology | Explains the criteria used to rank and score lenders, building trust and providing clarity on why a lender is recommended. |

Pros and Cons

- Pro: Excellent primer content helps you prepare a strong application before engaging with lenders.

- Pro: Transparent editorial process and scoring offer an unbiased starting point for your research.

- Con: Bankrate does not originate loans, so you must still apply directly with the lenders it features.

- Con: Its "Best Of" lists are a snapshot in time and may not reflect the most competitive day-to-day pricing for niche Non-QM loans.

Best For:

Bankrate is ideal for the self-employed borrower who is in the research and preparation phase. It’s perfect for anyone who wants to understand their options, organize their documentation, and create a shortlist of qualified lenders before starting the application process.

Website: Bankrate Best Mortgage Lenders

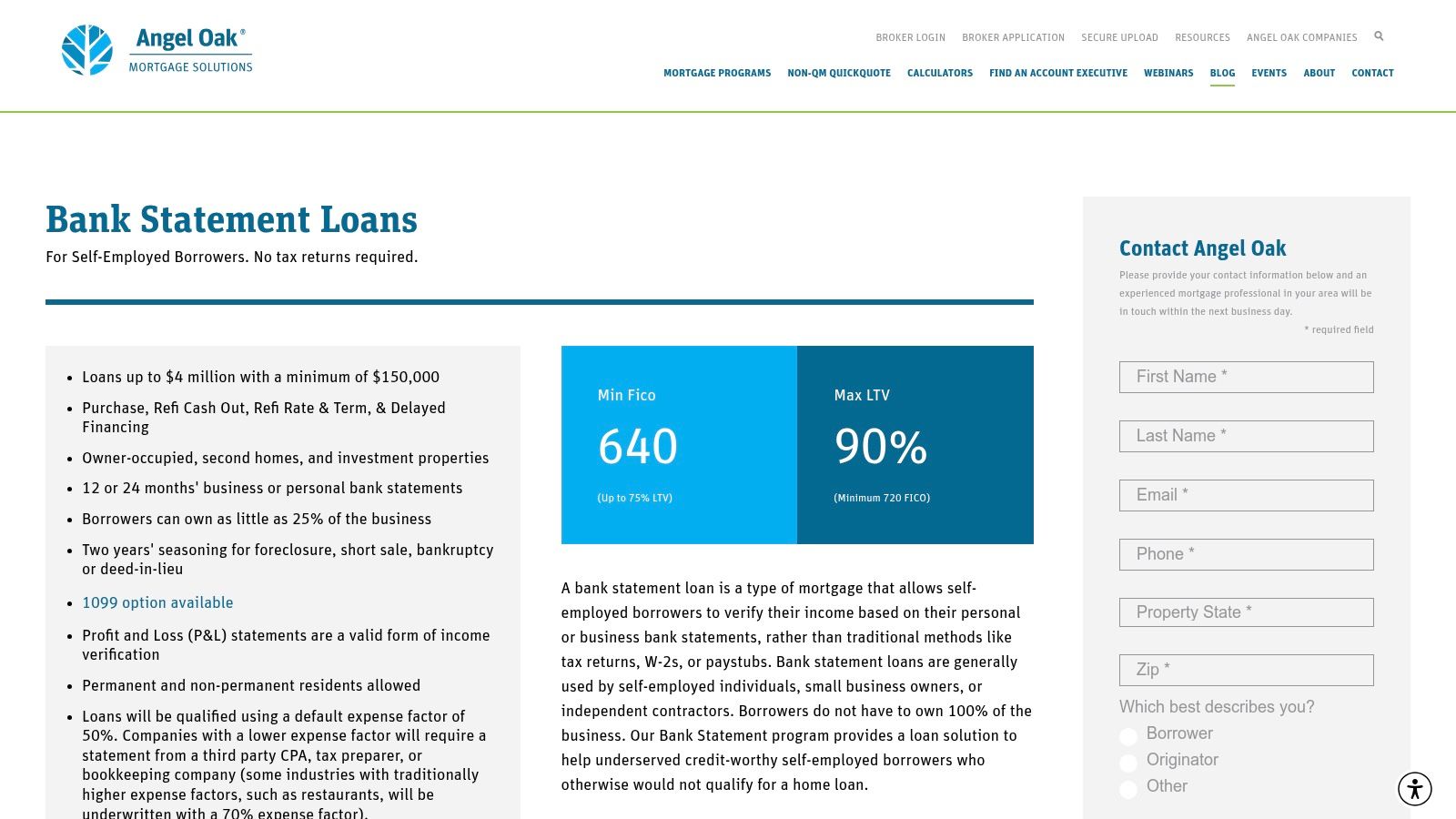

4. Angel Oak Mortgage Solutions / Angel Oak Home Loans

Angel Oak is a prominent direct lender specializing in Non-Qualified Mortgages (Non-QM), a product category built for borrowers outside the traditional underwriting box. For self-employed individuals, Angel Oak is a go-to name because its entire business model is designed to evaluate income beyond tax returns, making it one of the best mortgage companies for self employed borrowers who need alternative documentation.

Unlike conventional lenders who are often rigid about W-2s and tax transcripts, Angel Oak's core strength is its suite of bank statement loan programs. They understand that a business owner's true cash flow is not always reflected in their taxable income after deductions. By focusing on the actual revenue moving through business or personal accounts, they provide a viable path to homeownership for entrepreneurs and freelancers.

Why It’s Great for Self-Employed Borrowers

Angel Oak's deep specialization means their loan officers and underwriters are experts in analyzing complex, non-traditional income streams. They are comfortable working with 12 or 24 months of bank statements to derive a qualifying income, a process that would halt an application at a traditional bank. This expertise translates into a smoother, more predictable closing process.

Furthermore, Angel Oak offers a range of products tailored to this niche, including a Bank Statement HELOC, which allows self-employed homeowners to tap into their equity using the same flexible documentation. Their willingness to consider recent credit events (with proper seasoning) also provides a second chance for borrowers who may not have a perfect credit history.

Key Features and Offerings

| Feature | Description for Self-Employed Borrowers |

|---|---|

| Bank Statement Programs | Use 12-24 months of personal or business bank statements to qualify for a mortgage, bypassing the need for tax returns. |

| High Loan Limits | Offers jumbo loan amounts up to $4 million for purchase, refinance, and cash-out transactions. |

| Flexible Product Suite | Provides fixed-rate, adjustable-rate (ARM), and interest-only options to match different financial strategies. |

| Bank Statement HELOC | A unique offering that allows self-employed individuals to access home equity without traditional income verification. |

Pros and Cons

- Pro: Deep expertise in Non-QM underwriting specifically for the self-employed, leading to higher approval rates.

- Pro: Offers a diverse set of flexible documentation products, including a valuable Bank Statement HELOC.

- Con: Interest rates and fees are generally higher than conventional loans due to the increased risk profile.

- Con: Product availability and specific qualifying terms can vary significantly by state and individual borrower profile.

Best For:

Angel Oak is the ideal choice for a self-employed borrower with strong, consistent cash flow demonstrated through bank statements but significant tax write-offs that reduce their net income. It is perfect for those who need a lender that specializes in this exact scenario and want access to a broader product set, including high-balance loans and home equity lines of credit.

Website: Angel Oak Mortgage Solutions Bank Statement Program

5. New American Funding

New American Funding is a direct lender and servicer that stands out for its robust suite of Non-QM loan products specifically designed for entrepreneurs and business owners. Unlike some conventional lenders who struggle with non-traditional income, New American Funding has built dedicated pathways for self-employed individuals, making them one of the best mortgage companies for self employed borrowers seeking flexibility.

Their approach is transparent, publishing typical minimum credit scores and down payment requirements directly on their website. This allows self-employed applicants to quickly assess their potential eligibility for programs like bank statement loans, which use 12 or 24 months of business or personal bank statements to calculate income instead of tax returns. This method is ideal for business owners who have significant cash flow but also legitimate tax deductions that reduce their net taxable income.

Why It’s Great for Self-Employed Borrowers

New American Funding excels by offering multiple alternative documentation options under one roof. A borrower who doesn't qualify with a 12-month bank statement program might be a perfect fit for their 1-year tax return option or an asset-depletion loan. This flexibility avoids the all-or-nothing approach of many traditional banks.

The company also pairs its online application process with a nationwide network of loan officers. This hybrid model provides the convenience of digital tools alongside the personalized guidance of a human expert who can help navigate the complexities of self-employed income documentation. Their educational resources, including documentation checklists, further empower borrowers to prepare a strong application.

Key Features and Offerings

| Feature | Description for Self-Employed Borrowers |

|---|---|

| Bank Statement Programs | Use 12 or 24 months of personal or business bank statements to qualify, bypassing the need for tax returns. |

| Alternative Documentation | Offers 1-year tax return options, asset-depletion programs, and even Profit & Loss statement loans. For more details on these, you can explore P&L and other non-traditional loan types here. |

| Qualification Transparency | Publishes typical minimum credit scores (often starting in the mid-600s) and down payment ranges for its Non-QM products. |

| Educational Resources | Provides guides and checklists specifically for self-employed borrowers to help them understand the qualification process. |

Pros and Cons

- Pro: Multiple documentation paths (bank statements, 1-year returns, assets) provide a solution for various self-employed scenarios.

- Pro: Transparent about general qualification guidelines, helping borrowers set realistic expectations.

- Con: Non-QM loans inherently come with higher interest rates and fees compared to conventional mortgages.

- Con: The minimum down payment for bank statement loans is often higher, typically starting at 20% or more.

Best For:

New American Funding is best for the self-employed borrower who wants to work with a direct lender offering a clear, diverse menu of Non-QM options. It is an excellent fit for business owners who appreciate upfront information on qualification criteria and want the choice between a digital experience and hands-on guidance from a loan officer.

Website: New American Funding Bank Statement Loans

6. CrossCountry Mortgage

CrossCountry Mortgage is a national retail lender known for its robust suite of Non-QM products tailored specifically for entrepreneurs. Their "Signature Expanded Bank Statement" program is a standout offering for self-employed individuals and 1099 earners who need to bypass traditional income verification. This makes them one of the best mortgage companies for self employed borrowers seeking flexible underwriting.

Unlike some lenders who only offer one narrow alternative documentation path, CrossCountry provides a well-defined menu of options. Borrowers can qualify using either personal or business bank statements, with clear guidelines on how income will be calculated. The company’s approach is designed to accommodate the financial realities of business owners, allowing for higher debt-to-income ratios and larger loan amounts for a variety of property types.

Why It’s Great for Self-Employed Borrowers

The primary advantage is the program's flexibility and transparency. CrossCountry clearly outlines how they can use 12 or 24 months of bank statements to establish a qualifying income, removing the reliance on tax returns that may not reflect true cash flow due to business deductions. This direct approach simplifies the application process for borrowers who have strong, consistent revenue but complex tax situations.

Furthermore, their programs are not limited to just primary residences. They extend their bank statement loans to second homes and investment properties, making them a valuable partner for entrepreneurs looking to build real estate portfolios. The ability to secure financing with up to 90% LTV provides significant leverage.

Key Features and Offerings

| Feature | Description for Self-Employed Borrowers |

|---|---|

| Bank Statement Programs | Qualify using 12 or 24 months of personal or business bank statements instead of traditional tax documents. |

| Flexible Underwriting | Program guidelines allow for debt-to-income (DTI) ratios up to 50% in some cases, recognizing the unique financial profiles of business owners. |

| Broad Property Support | Financing is available for primary residences, second homes, and investment properties, with loan amounts reportedly up to $3 million. |

| Alternative Non-QM Options | In addition to bank statements, offers P&L-only programs, asset-based lending, and interest-only payment options for qualified borrowers. |

Pros and Cons

- Pro: The website provides clear, borrower-facing explanations of their bank statement program requirements.

- Pro: Programs are versatile, covering purchase, refinance, and investment strategies across different property types.

- Con: Non-QM loans typically come with interest rates that are 1% to 3% higher than conventional mortgages.

- Con: Final eligibility, rates, and terms are state-specific and require direct consultation with a loan officer for accurate pricing.

Best For:

CrossCountry Mortgage is an excellent choice for the established self-employed borrower or real estate investor who has strong and consistent cash flow documented in their bank statements but cannot qualify using tax returns. It's ideal for those who need a flexible, clearly defined alternative documentation path to secure financing for primary, vacation, or investment properties.

Website: CrossCountry Mortgage Bank Statement Loans

7. Carrington Mortgage Services

Carrington Mortgage Services is a direct retail lender known for its robust suite of Non-QM loan programs designed for borrowers who don't fit into the traditional underwriting box. For entrepreneurs and business owners, their "Flexible Advantage" series of loans offers a vital alternative to standard tax-return-based income verification, solidifying their place among the best mortgage companies for self employed individuals.

These programs are specifically structured to accept bank statements as the primary method of proving income. Carrington’s tiered approach, which includes offerings like the Flexible Advantage, Advantage Plus, and Prime Advantage, allows them to serve a wide spectrum of credit profiles, from those with near-perfect credit to those who may have experienced a recent credit event. This flexibility is a significant advantage for self-employed applicants whose financial picture is more complex than a W-2 employee's.

Why It’s Great for Self-Employed Borrowers

Carrington’s strength lies in its specialized Non-QM product lineup. Instead of treating alternative documentation as an afterthought, it's a core part of their business. This means their loan officers and underwriters are experienced in evaluating business cash flow from bank statements, which can lead to a smoother and more predictable approval process for self-employed borrowers.

The tiered system provides clear pathways for different financial situations. A borrower with a lower credit score or a more complicated income history might qualify for one tier, while a borrower with a strong credit profile could access more favorable terms through another. This tailored approach increases the likelihood of finding a workable solution.

Key Features and Offerings

| Feature | Description for Self-Employed Borrowers |

|---|---|

| Flexible Income Verification | Allows the use of 12 or 24 months of personal or business bank statements to qualify, avoiding the need for tax returns. |

| Tiered Non-QM Programs | Offers multiple program levels (Flexible Advantage, Advantage Plus, etc.) to cater to various credit scores and loan-to-value ratios. |

| Loan Purpose Variety | Supports purchase, rate-and-term refinance, and cash-out refinance options across its Non-QM products. |

| Credit Event Seasoning | Provides options for borrowers with recent credit events like bankruptcy or foreclosure, provided certain timeframes have passed. |

Pros and Cons

- Pro: Multiple Non-QM tiers cater to a wide range of credit and income profiles, increasing approval chances.

- Pro: Deep expertise in bank statement underwriting provides a streamlined process for self-employed applicants.

- Con: Interest rates and fees on Non-QM loans are inherently higher than those for conventional mortgages.

- Con: Program availability and specific terms can differ; borrowers should confirm details for their specific scenario directly.

Best For:

Carrington Mortgage Services is an excellent choice for the self-employed borrower who needs a specialized Non-QM lender with a clear, structured process for bank statement loans. It's particularly well-suited for those with less-than-perfect credit or a complex income history who can benefit from a tiered program designed to find a path to "yes."

Website: Carrington Flexible Advantage Loan Program

Top 7 Mortgage Companies for Self-Employed: Comparison

| Provider | Implementation complexity 🔄 | Resource requirements ⚡ | Expected outcomes ⭐📊 | Ideal use cases 💡 | Key advantages ⭐ |

|---|---|---|---|---|---|

| Mortgage Seven LLC | 🔄 Moderate — broker coordinates multiple wholesale lenders | ⚡ Moderate — documentation for nonstandard programs; broker support speeds process | ⭐⭐⭐⭐ — high chance for tailored, competitive terms; strong service/turnaround 📊 | Self‑employed, investors, complex/nontraditional profiles | Broker access to many wholesale programs; personalized guidance; fast processing |

| LendingTree | 🔄 Low (single submission) → Variable (multiple lender follow‑ups) | ⚡ Low initial — one form & soft pull; additional docs if lender chosen | ⭐⭐⭐ — broad quote visibility; efficient rate‑shopping 📊 | Early market research and comparing multiple lender offers | One‑stop marketplace; free to consumers; wide lender access |

| Bankrate | 🔄 Very low — editorial research & lists | ⚡ Minimal — reading guides and checklists | ⭐⭐ — good shortlist and preparation resources; not a lender 📊 | Researching lenders; preparing documentation before applying | Transparent methodologies; practical checklists and guides |

| Angel Oak Mortgage Solutions | 🔄 Moderate — retail Non‑QM underwriting specifics | ⚡ High — 12–24 months bank statements; higher fees typical | ⭐⭐⭐⭐ — strong fit for bank‑statement borrowers; high loan limits 📊 | Self‑employed preferring bank statements; high‑balance loans | Deep Non‑QM specialization; high loan limits; HELOC options |

| New American Funding | 🔄 Moderate — multiple non‑QM paths with retail underwriting | ⚡ Moderate — bank statements or 1‑yr tax options; possible higher down payment | ⭐⭐⭐ — flexible qualification paths; nationwide retail support 📊 | Self‑employed needing alternative documentation options | Multiple doc paths; published score/down‑payment guidance; borrower education |

| CrossCountry Mortgage | 🔄 Moderate — branch/loan‑officer driven Non‑QM programs | ⚡ Moderate — bank statements accepted; can allow higher DTIs | ⭐⭐⭐ — supports purchase/refi/investment with higher LTVs 📊 | 1099/self‑employed, investors, higher‑DTI borrowers | Clear borrower guidance; supports investment properties and higher loan amounts |

| Carrington Mortgage Services | 🔄 Moderate — tiered Non‑QM product set | ⚡ Moderate‑High — varied tiers require specific documentation | ⭐⭐⭐ — flexible across credit tiers; accepts recent credit events with seasoning 📊 | Borrowers with credit quirks or nonstandard income | Multiple Non‑QM tiers; options without mortgage insurance on some products |

Your Next Step: Partnering with the Right Expert for Your Self-Employed Mortgage

Navigating the mortgage landscape as a self-employed individual can feel like an uphill battle. Traditional lending models, designed for W-2 employees with predictable paychecks, often fail to capture the true financial strength of a thriving business. This article has showcased some of the best mortgage companies for self employed borrowers, each offering unique strengths and specialized loan programs designed to bridge this gap.

We've explored a range of options, from direct lenders with deep expertise in non-traditional income to powerful online marketplaces. Angel Oak Mortgage Solutions and New American Funding stand out for their dedicated bank statement and P&L loan programs, offering a lifeline to entrepreneurs. Meanwhile, CrossCountry Mortgage and Carrington Mortgage Services provide robust platforms with diverse non-QM offerings. Marketplaces like LendingTree and Bankrate can be excellent starting points for comparing initial rates and getting a broad view of potential lenders.

However, the key takeaway is that the "best" company is not a one-size-fits-all answer; it's the one that best aligns with your specific financial picture. The most crucial factor isn't just the lender's name, but their specific underwriting guidelines for your unique situation.

From Information to Action: Your Personalized Strategy

The difference between a smooth approval and a frustrating denial often comes down to how your financial story is presented. This is where a strategic partnership becomes invaluable. Instead of approaching each lender individually and repeating the entire application process, a specialized mortgage broker can act as your advocate and strategist.

Consider these critical points when moving forward:

- Documentation is Key: Begin organizing your documents now. Whether you plan to use a bank statement loan (12-24 months of statements) or a P&L program (P&L prepared by a CPA), having these ready will significantly speed up the process.

- Understand Your Cash Flow: Lenders offering bank statement loans apply an "expense factor" to your deposits to estimate net income. This factor can vary dramatically from 50% down to 10%. Knowing your true business expenses helps you understand which lenders will give you the most accurate assessment of your qualifying income.

- Don't Go It Alone: The most efficient path forward is to work with an expert who already has established relationships with the wholesale divisions of these top-tier lenders. A broker who specializes in self-employed mortgages can analyze your specific income, credit, and asset profile and immediately identify the most suitable lending partner, saving you time, money, and stress.

Key Insight: Choosing the right mortgage partner is about more than finding a lender who offers bank statement loans. It's about finding a partner who understands the nuances of self-employed cash flow and can package your application for the highest probability of success at the most competitive terms.

Ultimately, securing a mortgage as an entrepreneur is a strategic financial move. Your income isn't standard, so your mortgage strategy shouldn't be either. By leveraging the expertise of a specialist, you transform from just another applicant into a well-qualified borrower, ready to make your homeownership dream a reality. You've built a successful business; now it's time to build your home equity with the same level of expert guidance.

Ready to turn your self-employed income into a home approval? The team at Mortgage Seven LLC specializes in crafting mortgage solutions for entrepreneurs, real estate investors, and business owners. We navigate the complexities of bank statement, P&L, and DSCR loans so you can focus on what you do best. Contact Mortgage Seven LLC today to get a clear, actionable plan for your home financing journey.