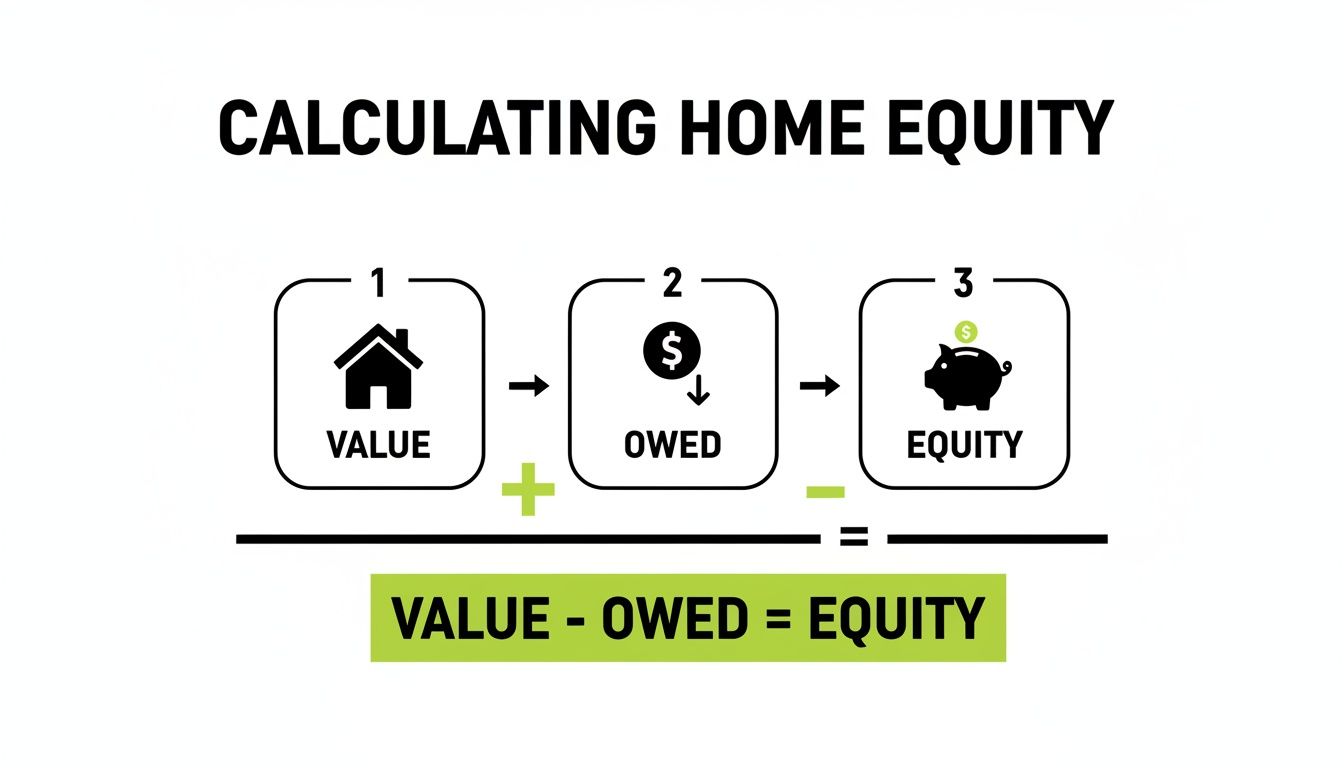

Imagine you've been paying down your mortgage for years, and your home's value has climbed. The difference between what your home is worth and what you still owe is your home equity. Think of it like a nest egg you've been building inside your home.

A cash out refinance is simply a way to crack that nest egg open. You’re not taking out a second loan; instead, you’re replacing your current mortgage with a new, slightly larger one. That new loan pays off your old mortgage in full, and you get the leftover amount in a lump sum of cash.

What Is a Cash Out Refinance in Simple Terms

At its core, a cash out refinance lets you turn your home's equity into liquid cash without selling your house. It’s a popular move for homeowners who need a significant amount of money for things like major home renovations, consolidating high-interest debt, or funding a college education.

This is different from a standard "rate-and-term" refinance, where the main goal is just to get a lower interest rate or change the loan's length. With a cash out refi, you're intentionally increasing your loan balance to pull money out. It’s a strategic financial decision that taps into the wealth you've built up over time.

The Core Mechanics

So, how does it actually work? The process really comes down to three things: your home's current market value, your remaining mortgage balance, and the lender's rules.

Most lenders will let you borrow up to 80% of your home's appraised value. This 80% limit is a crucial safeguard. It prevents you from borrowing against every last dollar of your equity, ensuring you still have a solid ownership stake in your property, which protects both you and the lender.

Here’s the basic flow:

- A New, Bigger Loan: First, you apply for a new mortgage that’s larger than what you currently owe.

- Paying Off the Old Loan: Once approved, the first thing the new loan does is completely pay off and close out your original mortgage.

- Cash in Your Pocket: The remaining money—the difference between the new loan amount and what you owed—is given to you at closing.

It's important to remember that a cash out refinance is not a second mortgage or a home equity loan (HELOC). It's a complete replacement of your primary mortgage. You end up with just one home loan and one monthly payment.

A Quick Glance at the Process

Let’s put some numbers to it. Suppose your home is now worth $400,000, and you have $200,000 left on your mortgage.

Your lender has a policy allowing you to borrow up to 80% of the home's value, which in this case is $320,000 (80% of $400,000). You decide to take out a new loan for that full amount.

From that $320,000, the first $200,000 goes directly to your old lender to pay off that mortgage. The remaining $120,000 (minus any closing costs) is wired to your bank account. That’s your cash out.

To make it even clearer, here’s a quick breakdown of the key terms you'll encounter.

Cash Out Refinance at a Glance

This table simplifies the main components of the process.

| Component | Simple Explanation |

|---|---|

| Home Equity | The part of your home you truly own (its value minus what you owe). This is what you borrow against. |

| New Loan | A brand-new mortgage that replaces your old one for a higher amount. |

| Loan-to-Value (LTV) | The percentage of your home's value you're borrowing. Lenders usually cap this at 80%. |

| Cash Out | The tax-free cash you receive after your original mortgage and closing costs are paid. |

Ultimately, this strategy provides a structured path to accessing a large sum of money, often at a much lower interest rate than you'd find with credit cards or personal loans. This is precisely why it remains a go-to option for homeowners with equity to their name.

How to Unlock Your Home's Hidden Value

The engine that powers a cash-out refinance is your home equity. Think of it as the financial stake you've built in your property over time—partly from paying down your mortgage and partly from your home's value going up. It’s the hidden value stored within your walls, just waiting for a purpose.

But before you can tap into it, you need to know exactly how much you have. The math is pretty simple: it’s your home’s current market value minus what you still owe on your mortgage. This simple formula is the key to unlocking a powerful financial tool.

Calculating Your Available Equity

Let's walk through a real-world example. Imagine you bought your home five years ago for $350,000. You've been making payments like clockwork, and your remaining mortgage balance is now $280,000. On top of that, the local market has been hot, and a recent appraisal shows your home is now worth $450,000.

Here’s how the numbers break down:

- Current Home Value: $450,000

- Remaining Mortgage Balance: -$280,000

- Total Home Equity: $170,000

This $170,000 is your ownership stake. It’s the portion of your home that’s truly yours, free and clear of the bank’s loan. Figuring this out is the first step, and learning how to calculate home equity accurately is a must before you even talk to a lender.

From Total Equity to Tappable Equity

Now, just because you have $170,000 in total equity doesn't mean you can pull out every last dollar. Lenders need you to keep some skin in the game, which is where the concept of Loan-to-Value (LTV) ratio comes in.

LTV is just a percentage that compares your loan amount to your home's appraised value. For a cash-out refinance, most lenders cap the LTV at 80%. This means your new, bigger mortgage can't be more than 80% of what your home is currently worth.

The 80% LTV rule is a critical safeguard. It protects both you and the lender by making sure you keep at least 20% equity in your home. This cushion reduces financial risk and keeps a significant chunk of your asset safe.

Let's apply this to our example:

- Maximum Loan Amount: Your home is valued at $450,000. 80% of this is $360,000. This is the most you can borrow.

- Pay Off Existing Mortgage: From that new $360,000 loan, you first have to pay off your old $280,000 mortgage.

- Calculate Your Cash Out: $360,000 (New Loan) – $280,000 (Old Mortgage) = $80,000 (Potential Cash Out).

So, in this scenario, your $170,000 in total equity translates into $80,000 of tappable equity—the actual cash you can walk away with. This dynamic has completely supercharged the mortgage market. With U.S. homeowners sitting on record amounts of equity, we saw a 15% year-over-year jump in Q1 cash-out originations, even with higher rates. In fact, this segment made up a whopping 59% of all refinances in Q2, as many people decided a higher rate was a fair trade for accessing cash to renovate or pay down other debt. You can dig into these mortgage origination trends on the St. Louis Fed's economic data site.

This process takes an abstract idea—your home's value—and turns it into a real financial resource you can use. Once you understand how to calculate both your total and tappable equity, you can see exactly how a cash-out refinance might help you hit your goals.

A Step-by-Step Guide to the Cash Out Refinance Process

Getting a cash-out refinance can seem complicated, but it's really just a series of clear, predictable steps. Once you understand the roadmap, the whole thing feels much more manageable. Generally, you can expect the entire process, from your first call to a lender to getting your cash, to take about 30 to 60 days.

Think of it like planning a home renovation. You start with a clear vision (your financial goal), get your budget in order, hire the right contractor, and oversee the project until it's complete.

Step 1: Pinpoint Your "Why"

Before you even think about filling out an application, you need to get crystal clear on why you need this money. A cash-out refi isn't just a simple loan; it's a complete replacement of your mortgage. The reason for doing it should be just as substantial.

Are you looking to wipe out high-interest credit card debt that's been dragging you down? Maybe you're funding a major kitchen remodel that will boost your home's value. Or perhaps the goal is to cover college tuition or grab an investment property.

Having a specific, well-defined purpose is crucial. It will be your north star for every decision that follows, from how much cash to pull out to what kind of loan term best fits your future.

Step 2: Get Your Financial Ducks in a Row

With your goal set, it's time to prep your finances for a lender's microscope. They're going to want to see that you can comfortably handle the new, larger mortgage payment, so you need to have your documentation and financial stats ready to go.

This is where home equity comes into play. It’s the portion of your home you actually own, and it's the well you'll be drawing from.

Simply put, the equity you’ve built is the asset that makes a cash-out refinance possible. Here’s what lenders will focus on:

- Credit Score: You’ll generally need a score of at least 620 to qualify. But to get the best interest rates on the market, you'll want to aim for 740 or higher. Pull your credit report and clean up any errors you find.

- Debt-to-Income (DTI) Ratio: This is a big one. It’s your total monthly debt payments divided by your gross monthly income. Lenders really want to see this number at 43% or lower, and that includes the payment for your proposed new loan.

- Paperwork: Get your documents together now to save yourself a headache later. You’ll need recent pay stubs, W-2s or tax returns for the last two years, bank statements, and your current mortgage statement.

Step 3: Find the Right Lender and Apply

Don't just go with the first lender you find. Rates, fees, and service can vary wildly between national banks, your local credit union, and independent mortgage brokers. Get quotes from at least three.

When you get their Loan Estimates, don’t get fixated on just the interest rate. The Annual Percentage Rate (APR) is the number that tells the real story, as it rolls in most of the loan fees. Our guide on understanding the refinancing journey breaks this down in more detail.

After you’ve picked your lender, you'll submit the formal application with all the documents you've already gathered. This gives them the green light to pull your credit and get the ball rolling.

Step 4: The Underwriting Gauntlet and Home Appraisal

This is the "wait and see" part of the process. Your file now goes into underwriting. A professional underwriter will comb through every detail of your financial life—income, assets, debts, credit—to make sure you're a solid borrower who meets all their lending criteria. Don't be surprised if they ask for an extra document or two; just respond as quickly as you can.

The home appraisal is one of the most critical steps in a cash out refinance. An independent appraiser will assess your property's current market value, which directly determines the maximum amount of money you can borrow.

The lender will schedule an appraisal to get an official valuation of your home. This number is everything. It's used to calculate your loan-to-value (LTV) ratio and ultimately decides how much cash you can actually get. If the appraisal comes in lower than you hoped, it will likely reduce the amount of money you can walk away with.

Step 5: Closing Day and Getting Your Funds

Once the underwriter gives the final thumbs-up, you're in the home stretch. You’ll get a Closing Disclosure at least three business days before you sign. This is the final, official breakdown of your loan terms, rate, payment, and total cash needed to close.

Read this document line by line. Match it against your original Loan Estimate to make sure nothing has changed unexpectedly. At the closing appointment, you'll sign a stack of papers, and then the clock starts on a mandatory three-day "right of rescission." This is a cooling-off period where you can legally cancel the deal.

After those three days pass, your loan is official. The lender will disburse your cash, typically as a wire transfer right into your bank account, and you're ready to put that money to work.

Is a Cash-Out Refinance Really the Right Move for You?

Tapping into your home equity with a cash-out refinance can feel like a powerful financial move. But let's be clear: it’s not for everyone. Before you even think about replacing your current mortgage, you need to step back and take a hard look at the real pros and cons. This isn't just about getting a check; it's about fundamentally changing the biggest debt you have.

Seeing the potential for a big cash payout is exciting, but you have to balance that against the long-term impact on your monthly payment, the total interest you’ll pay, and the equity you've worked so hard to build. Let's break down both sides of the coin so you can make a smart, informed decision.

The Upside: What Makes It So Appealing?

One of the biggest draws is the interest rate. When you compare a cash-out refinance to other ways of borrowing, like personal loans or credit cards, the mortgage rate is almost always going to be lower. A lot lower.

That lower rate can save you a mountain of money over the years, especially if you're using the cash to consolidate other, more expensive debts. Imagine swapping out multiple high-interest credit card payments for one predictable, fixed-rate mortgage payment. That alone can bring a lot of financial peace of mind.

Here’s a quick rundown of the main benefits:

- A Lump Sum of Cash: You get a significant amount of money all at once. This is perfect for big-ticket items like a major home renovation, the down payment on a rental property, or funding a college education.

- Lower Borrowing Costs: Mortgage rates are secured by your home, making them far cheaper than unsecured debt. It’s one of the most cost-effective ways to borrow a large sum.

- Possible Tax Advantages: The interest you pay on a mortgage can sometimes be tax-deductible. It's a bit complicated, especially with the cash-out portion, so you'll definitely want to chat with a tax advisor to see how it applies to you.

It's no surprise this strategy has become incredibly popular. As home values have climbed, people are realizing just how much wealth is sitting in their property. The numbers tell the story: in the first quarter of one recent year, cash-out refinances shot up 15%. By the second quarter, they accounted for a whopping 59% of all refinance transactions, with homeowners often taking a slightly higher rate just to access that equity. You can dig into these kinds of consumer credit trends in the TransUnion Q2 insights report.

The Downside: The Risks You Can't Ignore

Now for the other side of the story. A cash-out refinance comes with some serious risks that you absolutely cannot gloss over. The biggest one? You're piling more debt onto your house.

If life throws you a curveball and you suddenly can't make that new, bigger mortgage payment, you could be at risk of foreclosure. That's the crucial difference between this and running up a credit card bill—with a cash-out refi, your home is the collateral.

Don't forget, a cash-out refinance also resets your mortgage clock. If you’re 10 years into a 30-year loan and refi into a new 30-year term, you're essentially starting over. You'll be making payments for a much longer period and will pay far more in total interest over the life of the loan.

Here are the key drawbacks to consider:

- You'll Pay Closing Costs: Refinancing isn't free. Expect to pay closing costs, which typically run between 2% to 5% of your new loan amount. These fees can be rolled into the loan, but make no mistake, it's still money you're paying.

- Your Payment or Rate Could Go Up: Depending on the market, you might end up with a higher interest rate than you have now. A higher rate on a larger loan balance is a surefire recipe for a bigger monthly payment.

- You're Cashing Out Your Equity: You're literally borrowing against your ownership stake in your home. This shrinks the equity buffer you've built, which could put you in a tough spot if property values dip.

As you weigh these points, it's helpful to think about how this move affects your overall financial health. A concept like the debt-to-equity ratio can give you a clearer picture of the financial leverage you're taking on. This is a major decision, and looking at it from every possible angle is the only way to protect your financial future.

Cash Out Refinance vs Other Financing Options

To put it all in perspective, let's see how a cash-out refinance stacks up against two other common options for accessing cash: a home equity line of credit (HELOC) and a personal loan. Each has its own place, and the best choice really depends on your specific needs.

| Feature | Cash-Out Refinance | HELOC | Personal Loan |

|---|---|---|---|

| Loan Type | Replaces your entire mortgage with a new, larger one | A separate, second mortgage that acts like a credit card | An unsecured loan not tied to your home |

| How You Get Funds | One lump-sum payment at closing | Draw funds as needed up to a credit limit | One lump-sum payment at closing |

| Interest Rate | Fixed rate, typically lower than HELOCs or personal loans | Variable rate, often starts low but can rise over time | Fixed or variable rate, almost always higher than mortgages |

| Best For | Large, one-time expenses (renovation, debt consolidation) | Ongoing or uncertain costs (staged projects, emergencies) | Smaller, short-term needs when you don't want to use home equity |

| Biggest Risk | Foreclosure if you can't pay the new, larger mortgage | Foreclosure if you can't pay; rising rates increase payments | Damage to credit score; high interest costs |

Ultimately, a cash-out refinance is a powerful tool for major financial goals, a HELOC offers flexibility for ongoing needs, and a personal loan provides quick cash without putting your home on the line, albeit at a higher cost.

Calculating the True Costs and Potential Returns

It's easy to get excited about the idea of a big cash payout, but a cash-out refinance is a major financial decision, not a lottery win. It comes with its own set of costs, and understanding them is the only way to know if this move truly makes sense for you. Think of it less like tapping into "free money" and more like a strategic financial tool where the upfront investment determines the long-term payoff.

Just like your original mortgage, a refinance has closing costs. You can generally expect these to run between 2% and 5% of your new, larger loan amount. So, if you're taking out a new $350,000 mortgage, you're looking at anywhere from $7,000 to $17,500 in fees.

Most people choose to roll these costs right into the new loan. It’s convenient because you don't need cash on hand, but remember, it chips away at the net cash you’ll receive and adds to the total you'll owe over time.

Breaking Down the Common Fees

When you get your Loan Estimate, you'll see a list of charges. Knowing what they are ahead of time takes the sticker shock out of the equation and makes it much easier to compare offers from different lenders.

You'll almost always see these line items:

- Origination Fee: This is what the lender charges for the administrative work of putting your loan together. It's often around 1% of the loan amount.

- Appraisal Fee: A licensed appraiser has to confirm your home's current value to justify the new loan. This typically costs $400 to $600.

- Title Insurance: A necessary policy that protects you and the lender from any old claims or liens against your property title popping up.

- Credit Report Fee: A minor charge for pulling your credit scores and history.

- Recording Fees: Your county or local government charges this to make the new mortgage official public record.

Getting a handle on these expenses is the first real step in figuring out if a cash-out refi works for your budget.

A Practical Example of Calculating Your Cash Out

Let's put some real numbers to this to see how it all shakes out. Say this is your current situation:

- Current Home Value: $500,000

- Remaining Mortgage Balance: $250,000

- Closing Costs (estimated at 3%): We'll calculate this.

First, the lender will cap your new loan at a certain loan-to-value ratio, usually 80%. In this case, 80% of $500,000 is $400,000. Let’s assume you want to borrow the maximum.

- New Loan Amount: $400,000

- Pay Off Old Mortgage: -$250,000

- Calculate Closing Costs: 3% of your new $400,000 loan is -$12,000

- Net Cash to You: $400,000 – $250,000 – $12,000 = $138,000

As you can see, the final cash-in-hand is quite a bit less than the raw equity you started with. You can run your own numbers for different scenarios with our collection of handy mortgage calculators.

Finding Your Break-Even Point

The most important calculation you'll do is finding your break-even point. This tells you exactly how long it will take for the monthly savings from your refinance (like paying off high-interest credit cards) to completely pay back the closing costs.

To find your break-even point, divide your total closing costs by your total monthly savings. For example, if your closing costs were $9,000 and you save $300 a month by paying off high-interest debt, your break-even point is 30 months ($9,000 / $300).

This simple math is your best friend when making this decision. If you know you'll be in your home for much longer than 30 months, the refinance is probably a smart financial play. But if you think you might sell before you hit that mark, you could end up losing money.

Even in a higher-rate environment, the demand for this kind of financing is strong. Forecasts show refinance originations are expected to climb 9.2% to $737 billion, proving just how many homeowners see value in accessing their equity this way.

Is a Cash-Out Refinance the Right Move for You?

Figuring out if a cash-out refinance is right for you is about more than just crunching the numbers. It’s about making sure this powerful financial tool actually lines up with your real-life goals. Understanding how it works is half the battle; knowing why you’re doing it is the part that truly matters.

Are you looking to build long-term wealth, get your finances in order, or maybe jump on a new opportunity? The answer isn't one-size-fits-all. What’s a brilliant move for your neighbor could be a terrible one for you. Let’s walk through a few common situations to see where you might fit in.

Strategic Uses for Your Home Equity

The smartest ways to use a cash-out refinance are almost always tied to getting a solid return on your investment or solving a major financial headache. Think of it less as "getting cash" and more as "repositioning your assets" to put yourself in a better financial spot.

Here are a few scenarios where a cash-out refi can be a real game-changer:

-

Funding Value-Adding Home Renovations: Pouring that money back into your house for a kitchen overhaul, a new bathroom, or a finished basement can directly boost your property value. You're essentially taking equity out in the form of cash, then putting it right back into the home to make it worth even more. It's a classic reinvestment strategy.

-

Consolidating High-Interest Debt: This is a big one. If you’re drowning in credit card debt with rates pushing 20% or more, using your mortgage to wipe those balances clean can be transformative. You’re trading cripplingly expensive debt for a single, low-rate mortgage payment. The move can slash your monthly outflows and save you a fortune in interest over time.

-

Investing in Another Property: For aspiring real estate investors, a cash-out refinance can be the key that unlocks your next purchase. The cash can serve as the down payment on a rental property, letting you use the equity in your home to acquire an asset that generates its own income.

When to Think Twice

For all its benefits, this isn't a magic bullet. A cash-out refinance means taking on a bigger mortgage, and you’re often hitting the reset button on your loan term. Most importantly, you are putting your home up as collateral for the cash you're taking out—a fact that deserves serious consideration.

The big question you have to ask yourself is this: will taking on this new debt create a clear, positive financial outcome?

If the plan is to fund a vacation, buy a car, or cover general lifestyle spending, you’re on shaky ground. You're essentially converting your home's hard-earned equity into a pile of unsecured debt, which is a risky play.

You also have to think about your timeline. Do you see yourself staying in the home for a long while? If you think you might sell in the next couple of years, the closing costs associated with the refinance could easily wipe out any savings you hoped to gain. To make sure you've thought of everything, our detailed mortgage refinance checklist covers all the bases. An informed decision is the best way to protect your most valuable asset.

Your Top Cash-Out Refinancing Questions, Answered

Even after getting the basics down, you probably still have a few specific questions. It's only natural. Let's tackle some of the most common ones we hear from homeowners every day.

Can I Do a Cash-Out Refinance if I Have Bad Credit?

It’s tougher, but not always impossible. While a strong credit score is your best ticket to a great rate, some lenders will consider scores as low as 620.

If your credit is on the lower end, lenders will be looking for other signs of financial strength to balance things out. Think a low debt-to-income (DTI) ratio or a ton of equity built up in your home. These factors can help reassure them that you're a reliable borrower.

Is the Cash I Get from a Refinance Taxable Income?

Great question, and the answer is usually no. Because the money you receive is technically a loan, the IRS doesn't see it as income. So, you typically won't owe income tax on the cash you pull out.

That said, tax rules can get tricky, especially when it comes to deducting mortgage interest. You might only be able to deduct the interest on the part of the loan used to buy, build, or make significant improvements to your home. It's always a smart move to chat with a tax professional to see how this applies to your specific situation.

What's the Real Difference Between a Cash-Out Refinance and a HELOC?

This is a big one. A cash-out refinance completely replaces your old mortgage with a new, larger one. You get the difference in cash all at once, as a lump sum.

A Home Equity Line of Credit (HELOC), on the other hand, is a second mortgage that sits alongside your current one. It acts more like a credit card secured by your home, giving you a revolving line of credit you can draw from as needed and pay back over time. Your original mortgage stays exactly as it is.

At Mortgage Seven LLC, our job is to make complex home financing simple. Whether this is your first home or your fifth, we’re here to help you navigate your options and find the right solution. Start exploring what's possible by visiting our expert team at https://mtg7.com.