So, you're getting ready to buy a home with an FHA loan. You’ve saved for the down payment, but what about the other major expense: closing costs?

Closing costs for an FHA loan are all the fees you pay to finalize the mortgage and officially take ownership of the property. Expect these to run anywhere from 2% to 6% of the home's purchase price. It's a common misconception that these are part of your down payment—they're a completely separate set of expenses.

Your Quick Guide To FHA Closing Costs

Think of it this way: your down payment is your initial investment in the house itself, building equity from day one. Closing costs, on the other hand, pay for all the professional services required to make the deal happen—the appraisal, title search, loan processing, and more.

These costs aren't one single bill. They’re a collection of individual line items from everyone involved in getting you to the finish line. While both buyers and sellers have costs, the buyer's side is usually much larger. Getting a handle on what each fee is for is the best way to feel in control of your budget.

What Expenses Are Included

The exact amount you'll pay depends on a few things: the price of the home, its location (state and county taxes matter!), and the lender you work with.

As home prices go up, so do closing costs. A 2021 study showed the national average for mortgage closing costs hit $6,905 for a single-family home. That was a sharp 13.4% jump from the year before, mostly because property values were climbing so quickly. You can dig into detailed reports on how these costs vary by state and have shifted over time.

FHA closing costs generally break down into three main categories:

- Lender Fees: These are the charges your bank or mortgage company collects for putting the loan together. Think origination fees for processing your application and underwriting fees for the work of verifying all your financial info.

- Third-Party Fees: These costs go to other companies for essential services. This includes the home appraisal, pulling your credit report, and a flood certification to check if the property is in a flood zone.

- Prepaid Items and Escrow: These aren't technically fees but are upfront payments for ongoing expenses. You'll prepay a certain amount of your property taxes and homeowners insurance to fund an escrow account, which your lender will use to pay those bills on your behalf.

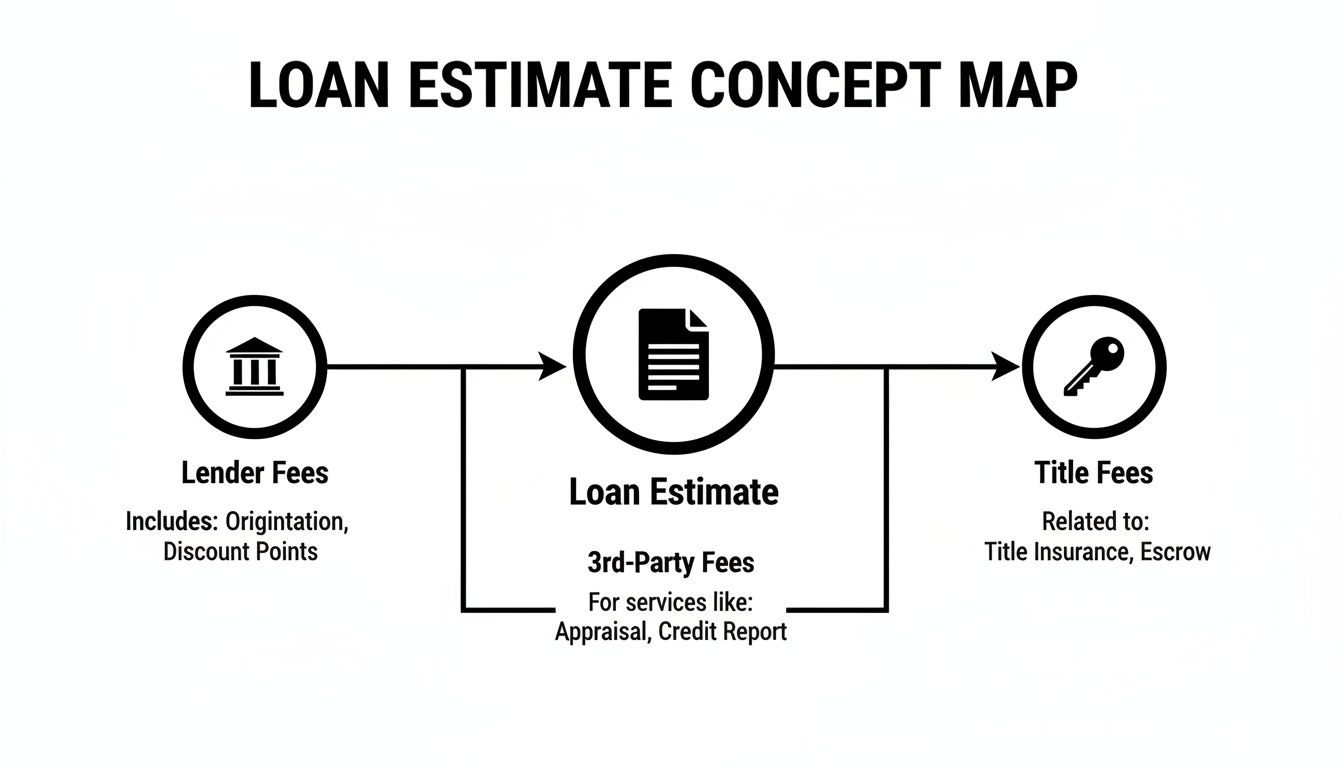

The most important takeaway is that FHA closing costs should never be a surprise. Your lender is required by law to give you a Loan Estimate document within three days of your application. This form clearly lists every single anticipated fee, giving you a detailed financial roadmap right from the start.

Decoding Your Loan Estimate, Line By Line

When you first open your Loan Estimate, it can feel like you're trying to read a foreign language. Lenders are required to send you this document within three business days of your application, and it breaks down every single fee involved in your home loan. Think of it as the final, detailed receipt for buying your home. Getting a handle on each line item is the first step to mastering your FHA closing costs.

These costs usually fall into three main buckets: what you pay the lender, what you pay third-party services, and what you pay for title work. Let's pull back the curtain on each one so you know exactly where your money is going.

Lender Fees For Processing Your Loan

These are the charges that go directly to your mortgage lender for actually putting your loan together. The biggest one you'll likely see is the origination fee, which is basically the lender's fee for processing, underwriting, and funding your loan. Some lenders might break this down further into smaller "application" or "processing" fees, but it all serves the same purpose.

You might also see a line for discount points. This is an optional fee you can pay at closing to "buy down" your interest rate. Paying points upfront can lower your monthly payment and save you a significant amount of money over the life of the loan. Typically, one point costs 1% of your total loan amount. If you want a deeper dive into these charges, you can learn more about what a mortgage origination fee covers.

Third-Party Services That Make The Deal Happen

This next group of fees covers all the other professionals who have to get involved to make your home purchase official. Your lender doesn't set these fees, but they are absolutely necessary to get to the closing table.

- Appraisal Fee: A licensed appraiser has to visit the property and determine its fair market value. This is non-negotiable for an FHA loan; it ensures the home is worth what you're borrowing and meets the FHA's specific safety and soundness standards. This service usually runs between $500 and $800.

- Credit Report Fee: A small but necessary charge for pulling your credit history and scores.

- Flood Certification: This simply determines if the property is located in a flood zone. If it is, you'll be required to get separate flood insurance.

Title Fees: Ensuring Clear Ownership

Title fees can be some of the more confusing—and significant—costs you'll face. These charges cover all the work involved in making sure the property can be legally transferred to you, free and clear of any old claims or debts from previous owners. This includes a deep dive into public records, known as a title search.

A study from the U.S. Department of Housing and Urban Development actually found that FHA borrowers paid, on average, about $1,200 just for title services. This number can swing wildly depending on where you live. For example, in states like New York and California, title costs can easily be $1,000 higher than the national average.

As part of this, you'll also pay for two title insurance policies. The lender’s policy is mandatory and protects your lender's investment. The owner’s policy is technically optional, but it's a smart purchase that protects your ownership rights for as long as you own the home.

Getting to Know FHA Mortgage Insurance

One of the biggest things that sets an FHA loan apart is its mandatory mortgage insurance. It’s easy to get this confused with homeowner's insurance, but they’re completely different. Homeowner's insurance protects your house and your stuff; FHA mortgage insurance protects the lender in case you can't make your payments.

This insurance is the key that allows lenders to feel comfortable offering loans with down payments as low as 3.5%. Think of it as having two parts: a one-time fee to get in the door, and then a smaller, monthly fee for as long as you have the loan (or for a set period). Both are a major part of your total closing costs and your monthly budget.

The Upfront Mortgage Insurance Premium (UFMIP)

First, let's talk about the Upfront Mortgage Insurance Premium (UFMIP). This is a one-time charge you handle at closing, and the rate is currently 1.75% of your base loan amount.

So, if you're borrowing $350,000, the UFMIP would be $6,125.

The good news? You almost never have to write a check for this amount. The vast majority of homebuyers choose to roll the UFMIP into the loan itself. This does bump up your total loan balance and your monthly payment just a tad, but it dramatically lowers the amount of cash you need to bring to the closing table.

It's crucial to understand that even if you finance the UFMIP, it's still considered a closing cost. Factoring it into your loan is a strategic choice to manage your upfront cash needs, not a way to eliminate the cost entirely.

The Annual Mortgage Insurance Premium (MIP)

The second piece of the puzzle is the annual Mortgage Insurance Premium (MIP). The name is a little misleading, because you actually pay it in monthly installments as part of your mortgage payment.

The exact rate for MIP depends on a few factors, including your loan amount, the loan term (like 15 or 30 years), and your loan-to-value (LTV) ratio. For most people using a 30-year FHA loan and making the minimum 3.5% down payment, the annual rate is 0.55%. That 0.55% is calculated on your loan balance, then divided by 12 and added to your monthly house payment.

FHA MIP is a bit different from the Private Mortgage Insurance (PMI) on conventional loans, especially when it comes to canceling it. You can learn more about the distinctions between private mortgage insurance and FHA MIP.

Your Loan Estimate will clearly itemize all your costs, including lender fees, third-party services, and title charges, so you know exactly what to expect.

How long you're on the hook for these monthly MIP payments depends entirely on your original down payment.

- Put down 10% or more: You'll pay MIP for 11 years.

- Put down less than 10%: You'll pay MIP for the entire life of the loan, unless you refinance.

Getting a handle on both the UFMIP and the monthly MIP is absolutely essential. They have a direct impact on how much cash you need for closing and what your monthly housing payment will look like for years to come.

Using Seller Concessions To Lower Your Cash To Close

Coming up with the cash for a down payment and closing costs is hands-down the biggest challenge for most aspiring homeowners. But what if the seller could chip in and cover a big chunk of those fees? It’s not just a nice idea—with an FHA loan, it's a built-in feature designed to get more people into homes.

This fantastic tool is called a seller concession. In simple terms, it's an agreement where the seller pays for some (or even all) of your closing costs. You negotiate this right into the purchase contract, and it directly slashes the amount of cash you need to bring to the closing table.

How FHA Seller Concessions Work

The FHA has a pretty straightforward rule here: sellers can contribute up to 6% of the home’s sales price toward your closing costs. That's a generous cap, and it can make a massive difference in your out-of-pocket expenses. We're talking about potentially covering most, if not all, of your fees.

Let’s put that into perspective. If you’re buying a $350,000 home, a 6% seller concession works out to $21,000. The seller doesn't just hand you a check; this amount is credited directly to you on the final settlement statement, paying off specific closing costs on your behalf.

Heads up: This 6% limit isn't just for the seller. It includes contributions from any "interested party," which could be your real estate agent or the home builder. Your lender will be tracking this to make sure the total doesn't go over the FHA’s line.

Naturally, you're more likely to see sellers offering concessions in a buyer's market when they need to sweeten the deal to attract offers. But don't rule it out in a hotter market. A motivated seller who wants a quick, smooth closing might still be willing to help out.

What Costs Can Concessions Cover?

So, where can all that money go? The seller’s contribution can be used for a whole host of closing costs fha, giving you some serious financial breathing room.

- Lender Fees: Think loan origination, processing, and underwriting charges.

- Third-Party Fees: This covers expenses like the appraisal, credit report, and flood certification.

- Title and Escrow Charges: All the costs for the title search and insurance policies can be paid for.

- Prepaid Items: You can use the funds to kickstart your escrow account for property taxes and homeowners insurance.

- Discount Points: The seller can even pay for mortgage points to buy down your interest rate for the life of the loan.

The sky-high cost of buying a home is a hot topic right now. Combined buyer and seller closing costs can gobble up 7-11% of a home's price, and there's a growing push to bring these numbers down. Proposed reforms targeting title insurance and real estate commissions could slash these expenses, which really shows how powerful negotiated concessions are for FHA buyers. You can discover more insights about the national focus on closing costs and see how it might impact future home sales.

How To Estimate Your FHA Closing Costs

Alright, let's move past the percentages and talk about real dollars. The best way to get a handle on what you’ll actually need to bring to the closing table is to walk through a quick, back-of-the-napkin estimate.

We'll build a sample scenario to show you how all these different costs stack up. This isn't just a math exercise—it’s about giving you a realistic budget so there are no surprises on closing day.

Let's imagine you've found a home for $400,000. You’re planning to use an FHA loan with the minimum 3.5% down payment, which comes out to $14,000. That means your starting loan amount, before any other costs are added, is $386,000.

Calculating Your Upfront Mortgage Insurance

First up is the big one: the FHA’s Upfront Mortgage Insurance Premium (UFMIP). This is a mandatory, one-time fee of 1.75% of your base loan amount.

- Here's the math: $386,000 (Loan Amount) x 0.0175 (UFMIP Rate) = $6,755

Now, the good news is you don’t have to pay this out of pocket. Most borrowers choose to roll this cost directly into their mortgage. If you do that, your total loan amount bumps up to $392,755. For our example, we'll assume you finance it to keep your upfront cash needs as low as possible.

Estimating Lender and Third-Party Fees

Next, we have the standard closing costs that cover the lender’s work and all the third-party services required to get the deal done. A good rule of thumb is to budget between 2% and 3% of the home's purchase price for these.

Let's split the difference and use 2.5% for our estimate.

- Here's the math: $400,000 (Home Price) x 0.025 = $10,000

So, what does that $10,000 actually cover? It’s a bucket of different fees, and the breakdown might look something like this:

- Loan Origination Fee: Typically around 1% of the loan amount (~$3,860).

- Appraisal Fee: A standard FHA appraisal runs about $600.

- Title Search & Insurance: This can vary a lot by state, but let's budget $2,500.

- Miscellaneous Fees: This is a catch-all for smaller items like the credit report, flood certification, and county recording fees (~$3,040).

Budgeting for Prepaids and Escrow

Last but not least, you need to set up your escrow account. Think of this as a savings account your lender manages to pay your property taxes and homeowners insurance on your behalf. To get it started, you have to prepay a few months' worth of these expenses at closing.

These costs are hyper-local, but let's make some reasonable assumptions. If annual property taxes are 1.1% of the home price ($4,400/year) and homeowners insurance is $1,800/year, the lender will need a cushion.

- Property Taxes: Let's say 3 months are needed upfront ($1,100).

- Homeowners Insurance: You'll also likely need 3 months upfront ($450).

- Total Prepaids: That's roughly $1,550 to fund your initial escrow account.

To pull this all together, here is a simple table that lays out our example.

Sample FHA Closing Cost Estimate On A $400,000 Home

The table below provides an example breakdown of potential closing costs for a $400,000 home purchase with an FHA loan, illustrating typical fees and expenses.

| Cost Item | Estimated Cost | Notes |

|---|---|---|

| UFMIP | $6,755 | Financed into the loan; not a direct cash-to-close expense. |

| Lender & Third-Party Fees | ~$10,000 | Includes origination, appraisal, title, and other charges. |

| Prepaids & Escrow Funding | ~$1,550 | Covers your initial property tax and insurance payments. |

| Total Estimated Cash to Close | ~$11,550 | This is the cash you'd need in addition to your $14,000 down payment. |

Seeing it laid out like this really helps clarify where the money is going. Remember, this is just an estimate! Your actual costs will be detailed on your official Loan Estimate form from your lender.

Frequently Asked Questions About FHA Closing Costs

Diving into an FHA loan for the first time? It's completely normal to have a ton of questions, especially about the money you'll need at the finish line. Let's clear up some of the most common questions we hear about FHA closing costs.

Can All FHA Closing Costs Be Rolled Into The Loan?

This is probably the number one question people ask, and it's a great one. While it would be nice to finance everything, the short answer is no.

The only FHA-specific cost you can actually roll into the loan principal is the Upfront Mortgage Insurance Premium (UFMIP). In fact, most people do exactly that to keep their out-of-pocket expenses down. All the other standard costs—things like lender fees, the appraisal, and title insurance—need to be paid at closing. You'll need to cover these with your own funds, help from the seller, or a down payment assistance program.

How Do FHA Closing Costs Compare To Conventional Loans?

They're actually more similar than you might think, but the differences are important. For both FHA and conventional loans, you'll see charges for the same third-party services, like the appraisal and title search, and the lender's origination fees are usually in the same ballpark.

The real difference boils down to one thing: mortgage insurance.

- FHA Loans: You have the UFMIP (1.75% of the loan amount) due at closing (which can be financed) plus a monthly MIP payment, which usually sticks around for the life of the loan.

- Conventional Loans: You only pay for Private Mortgage Insurance (PMI) if you put down less than 20%. The best part? PMI automatically drops off once you hit enough equity.

So, while many of the line items look the same, the mortgage insurance structure makes the FHA loan's upfront costs feel a bit heavier.

What Is The Best Way To Get An Accurate Estimate?

Online calculators are a great starting point for a ballpark figure, but they can't predict your exact situation.

For a truly accurate, personalized breakdown of your FHA closing costs, there's no substitute for getting an official Loan Estimate from a lender. This is a standardized, legally required document that itemizes every single fee you can expect. Think of it as your financial road map for the home purchase—it’s the most reliable tool you'll have.

Putting It All Together: Your Next Steps

Getting a handle on your FHA closing costs is really the last major hurdle before you get the keys to your new place. As you've seen, it's not just about the final number—it's about understanding what goes into that number so you can make smarter decisions.

We've covered the three big strategies that give you control:

- Breaking down your fees so you know exactly what you’re paying for.

- Negotiating with the seller to get concessions that can seriously reduce the cash you need.

- Rolling your UFMIP into the loan to free up cash for moving day and beyond.

Think of these as the key moves in your homebuying playbook. But knowing the plays is one thing; executing them is another. That’s where having the right person in your corner comes in.

Why Working With a Broker Is a Game-Changer

This is where a good mortgage broker really shines. Instead of being stuck with whatever one bank or lender offers, a broker does the legwork for you, shopping your loan application around to a whole network of different lenders.

This forces lenders to compete for your business, which is great news for you—it often means better rates and lower fees. A broker is your advocate, focused on finding the FHA loan that actually makes sense for your budget and goals. To see how this works in practice, check out our guide on how to compare mortgage lenders.

Ready to turn all this knowledge into action? The team at Mortgage Seven LLC is here to give you the clear, straightforward advice you need to close on your FHA loan without any surprises. Apply online or schedule your free consultation today!

Leave a Reply