At its heart, the choice between these two loans comes down to a simple trade-off. A conventional loan is built for borrowers with a strong financial picture—think good credit and a decent amount of savings—who want to minimize their borrowing costs over the long haul. On the other hand, an FHA loan is designed to open the door to homeownership for those with less-than-perfect credit or a smaller down payment.

The right path for you really depends on what you value more: long-term savings or getting into a home sooner.

Conventional vs FHA Loans: Key Differences at a Glance

Deciding between a conventional and an FHA loan is a pivotal moment for any homebuyer. The best mortgage for you is a direct reflection of your financial situation—your credit score, how much you’ve saved for a down payment, and your feelings about long-term costs. FHA loans, which are insured by the Federal Housing Administration, create a much-needed opportunity for buyers who might otherwise be locked out of the market.

Conventional loans, by contrast, are geared toward borrowers on more solid financial ground. These loans often reward a strong credit history with major long-term savings, primarily because they allow you to eventually get rid of mortgage insurance. You can dive deeper into these traditional mortgage options to see if a conventional loan fits your profile.

Core Requirement Showdown

The most immediate differences you'll notice are the credit score and down payment rules. FHA loans are quite flexible here; you generally need a credit score of just 580 to qualify for the popular 3.5% down payment option. If your score is between 500 and 579, you can still get a loan, but you'll need to put down 10%.

Conventional loans, including the well-known Conventional 97 program, are a bit stricter. They typically require a minimum score of 620 and allow for a 3% down payment. This often makes FHA the go-to choice for first-time buyers who are still building their credit.

The core trade-off is simple: FHA loans offer leniency on the front end with easier qualification, while conventional loans provide flexibility and cost savings on the back end by allowing you to cancel mortgage insurance.

Getting a handle on these fundamental distinctions is the first step toward choosing a mortgage that truly works for you. This quick comparison table breaks down the most critical differences to help you see where you might fit.

Quick Comparison Conventional Loan vs FHA Loan

This table provides a side-by-side summary of the fundamental differences between Conventional and FHA mortgage products to help you quickly grasp the main distinctions.

| Feature | Conventional Loan | FHA Loan |

|---|---|---|

| Minimum Credit Score | Typically 620 or higher | As low as 580 (or 500 with 10% down) |

| Minimum Down Payment | As low as 3% | As low as 3.5% |

| Mortgage Insurance | Required under 20% down; cancellable | Required on all loans; often for the life of the loan |

| Loan Limits | Generally higher loan limits | More restrictive loan limits, varying by county |

| Property Types | Primary, secondary, and investment properties | Primarily for a primary residence only |

| Best For | Borrowers with strong credit and savings | Borrowers with lower credit or minimal savings |

As you can see, the "best" loan isn't universal—it’s entirely personal. The right choice hinges on balancing immediate accessibility against long-term financial benefits.

How Credit Scores and Down Payments Shape Your Choice

When you're weighing a conventional loan against an FHA loan, it really boils down to two key numbers: your credit score and how much you've saved for a down payment. These aren't just hurdles to clear; they fundamentally shape your loan's eligibility, interest rate, and what you'll pay over the long haul. Getting a handle on how they interact is the first step to making a smart choice.

There’s a common myth that FHA loans are only for buyers with bad credit. While they're certainly more forgiving, plenty of borrowers with great credit choose an FHA loan for its other benefits. On the flip side, conventional loans aren't just for people with huge savings—you can often get into one with as little as 3% down.

Unpacking the Credit Score Requirements

The minimum credit score is probably the starkest difference between these two loan types. But the minimum score is just the beginning of the story.

For an FHA loan, the government sets the floor. You'll need a credit score of at least 580 to qualify for the popular 3.5% down payment option. This lower bar is a game-changer for many people who are still building their credit. If your score falls between 500 and 579, you might still get approved, but you'll need to bring a larger 10% down payment to the table.

Conventional loans, on the other hand, typically start with a minimum credit score of 620. While that's higher, a stronger score really pays off here. With a conventional loan, a great credit score directly earns you a lower interest rate and, just as importantly, cheaper Private Mortgage Insurance (PMI). Lenders see you as less of a risk, and they pass those savings on to you.

Here's a critical distinction: FHA mortgage insurance costs are the same for everyone. A borrower with a 780 score pays the same FHA premium as someone with a 580. With a conventional loan, that 780 score would get you a significantly lower PMI rate, saving you real money every single month.

How Your Down Payment Influences the Decision

On the surface, the down payment difference seems small: 3% for conventional vs. 3.5% for FHA. But the real story is in how that money works with your credit score and impacts your mortgage insurance.

With a conventional loan, you can get in with 3% down, but putting down more—even just 5% or 10%—can unlock better interest rates and reduce your PMI. The ultimate goal for many is hitting that 20% down payment mark, which completely eliminates the need for PMI.

FHA loans are fantastic for buyers with limited cash, requiring just 3.5% down. The trade-off is that you'll always pay mortgage insurance. This comes in two parts: an Upfront Mortgage Insurance Premium (UFMIP) paid at closing and an annual premium paid monthly. If you put 10% or more down on an FHA loan, the annual mortgage insurance will drop off after 11 years, but you can't avoid it entirely at the start like you can with a conventional loan.

The Role of Gift Funds

Good news—both loan programs let you use gift funds from family for your down payment. The rules are pretty similar, but there are a few nuances.

Both will require a formal gift letter confirming the money isn't a loan you have to repay, which is crucial for keeping your debt-to-income ratio accurate.

- FHA Loans: The FHA has very clear and flexible guidelines for gift funds, making it a very reliable route for buyers getting family help.

- Conventional Loans: These also welcome gift funds, but individual lenders can sometimes have their own specific documentation rules, which we call "overlays."

Ultimately, choosing between a conventional and an FHA loan is a strategic decision based on your personal financial picture. If you have a solid credit score and a decent down payment, a conventional loan will almost always be cheaper over time. But if you need more flexibility on credit, an FHA loan is an incredible tool for achieving homeownership.

To dig deeper into this, you can learn more about how your credit influences your mortgage approval and what you can do to put yourself in the best possible position.

The True Cost of Mortgage Insurance: PMI vs. MIP

Let's talk about one of the most misunderstood and financially impactful parts of getting a mortgage: mortgage insurance. It's a cost that protects the lender, not you, but how it's handled on a Conventional versus an FHA loan can change your monthly payment and total cost by tens of thousands of dollars over time.

For many buyers, this is the single most important detail to get right. The real story isn't just about the monthly cost, but how long you're stuck paying it.

Understanding FHA Mortgage Insurance Premium (MIP)

FHA loans come with a mandatory, two-part insurance called the Mortgage Insurance Premium (MIP). This structure is unique to FHA loans and you can't get around it, no matter how great your credit score is.

First up is the Upfront Mortgage Insurance Premium (UFMIP). It's a one-time charge of 1.75% of your loan amount, due at closing. Most people just roll this into their loan balance, but remember, that means you're paying interest on it for decades.

Then, you have the annual MIP. This premium is divided into 12 monthly payments and baked right into your mortgage bill. The rate typically falls between 0.15% to 0.75% of the loan amount per year.

The most crucial thing to understand about FHA MIP is that it’s usually permanent. If you put down less than 10%, you will pay that annual MIP for the entire life of the loan. Only a down payment of 10% or more lets you remove it after 11 years.

How Conventional Private Mortgage Insurance (PMI) Works

Conventional loans take a completely different approach. If your down payment is less than 20%, you’ll pay for Private Mortgage Insurance (PMI). But unlike the FHA's MIP, PMI is designed to be temporary.

The cost of your PMI isn't one-size-fits-all; it’s based on your financial picture. The main factors are:

- Your Credit Score: The higher your score, the lower your PMI payment. It’s a direct reward for good credit.

- Your Down Payment: Putting down 10% instead of 3% will earn you a noticeably cheaper monthly PMI bill.

- Loan-to-Value (LTV) Ratio: This is just a measure of your loan balance against your home's value.

The best part? PMI goes away. You can request to cancel it once your loan balance hits 80% of your home's original appraised value. Even better, lenders are required by law to automatically drop your PMI once your balance gets down to 78%.

A Real-World Cost Comparison

Let's make this real. Imagine you're buying a $350,000 home and see how the numbers shake out.

FHA Loan Scenario:

- Down Payment: 3.5% ($12,250)

- Upfront MIP (1.75%): $5,910 (usually financed into the loan)

- Annual MIP (at 0.55%): About $155 per month

- Total MIP Paid Over 30 Years: Over $55,000 (because it lasts for the life of the loan)

Conventional Loan Scenario (for a buyer with good credit):

- Down Payment: 5% ($17,500)

- Upfront PMI: $0

- Annual PMI (at 0.50%): About $138 per month

- PMI Duration: Gone in about 8-9 years once you hit 20% equity.

- Total PMI Paid: Roughly $15,000

In this head-to-head comparison, the conventional borrower saves over $40,000 simply because they can cancel their mortgage insurance. This perfectly illustrates why buyers with solid credit and a plan to build equity often find the conventional loan is the smarter financial choice long-term. The easy entry of an FHA loan can come with a very steep price tag down the road.

When you get past the big-ticket items like credit scores and down payments, the real nitty-gritty of choosing between a conventional and an FHA loan often comes down to two numbers: your debt-to-income (DTI) ratio and the maximum loan limit. These figures define your borrowing power and can quickly make one loan the obvious choice for your financial situation.

Your DTI is a straightforward calculation lenders rely on to see how well you can manage a new mortgage. It’s the percentage of your gross monthly income that’s already spoken for by existing debts—think car loans, student debt, and credit card payments. A low DTI tells a lender you've got plenty of financial wiggle room. A high one can raise a red flag.

This is exactly where FHA loans step in and offer a crucial lifeline for borrowers with other financial obligations.

FHA's Breathing Room for Debt-to-Income

The FHA guidelines are famously more forgiving when it comes to DTI. While every lender sets its own internal rules, it’s not uncommon to see an FHA loan approved with a DTI ratio as high as 50%. With strong compensating factors, like a great credit score or a healthy savings account, some lenders might even push that a little higher.

This flexibility is a game-changer for a lot of people. If you're carrying a heavy student loan burden or a hefty car payment, the FHA's higher DTI threshold might be the only reason you can get into a home. It provides a level of understanding that conventional loans just don't offer.

Key Insight: The FHA's approach to DTI acknowledges that life is complicated. It allows lenders to see past a single number and evaluate the whole person, opening the door for creditworthy buyers who would otherwise be shut out by rigid conventional rules.

Conventional loans, by comparison, play by a much stricter rulebook. Most lenders draw a hard line at a 43% DTI, and you'll need to be a top-tier applicant for them to even consider stretching it to 45%. That tight margin means even one extra credit card bill can be the difference between getting approved and getting denied.

This isn't just a theoretical difference; it has a massive real-world impact. In fact, recent data shows that roughly 25% of all FHA loans approved had DTI ratios above 43%. For conventional loans? That number was less than 10%. To see how lenders make these decisions in practice, you can watch this insightful video on loan qualifications.

How Loan Limits Can Shape Your Home Search

The other major factor is the loan limit—the maximum amount of money you can borrow. Both FHA and conventional "conforming" loans have caps that are adjusted each year and vary from one county to the next to account for local home prices.

In this arena, conventional loans usually come out on top, especially if you’re shopping in a more expensive area.

FHA Loan Limits:

- Established by the Department of Housing and Urban Development (HUD).

- Are almost always lower than conventional limits for a given area.

- Can be a major roadblock in high-cost cities, effectively capping the price of homes you can look at.

Conventional Loan Limits:

- Set by the Federal Housing Finance Agency (FHFA).

- Are generally much higher, giving you significantly more purchasing power.

- Offer the flexibility needed for larger homes or properties in competitive metro areas.

Let’s say you're in a typical county where the FHA limit is maxed out, but the home you want is priced just above it. A conventional loan suddenly becomes your only path forward, as long as you can meet its tougher qualification standards. This makes the decision pretty clear-cut: if the FHA loan limit in your county is lower than the price of the home you want to buy, you'll have to go conventional.

Interest Rates vs. Total Cost: What Really Matters?

When you’re shopping for a mortgage, it’s easy to get fixated on the interest rate. But with Conventional and FHA loans, that single number doesn't tell the whole story. While an FHA loan might catch your eye with a slightly lower rate, you have to look deeper to see which loan is actually cheaper.

The real number to focus on is the Annual Percentage Rate (APR). Think of the APR as the "all-in" cost of your loan—it bundles the interest rate with the various fees and, most importantly, the mortgage insurance. For FHA loans, that insurance can be a game-changer, often pushing its total cost well above a conventional loan, even one with a higher starting interest rate.

How a Lower FHA Rate Can End Up Costing You More

The hidden culprit here is the FHA Mortgage Insurance Premium (MIP). As we've discussed, FHA loans hit you with a double whammy: a big upfront premium that gets tacked onto your loan balance and a monthly premium that, in most cases, you'll be paying for the life of the loan. That never-ending monthly cost can quickly erase any savings you thought you were getting from the lower interest rate.

On the other hand, conventional loans offer a clear path to savings. Once you've built up 20% equity in your home, you can request to have your Private Mortgage Insurance (PMI) removed. Getting rid of that monthly PMI payment is a huge win, significantly lowering your monthly obligation and the total amount you pay over the long haul—a key advantage FHA borrowers simply don't have.

Don't get tunnel vision on the interest rate. The lifetime cost of FHA mortgage insurance can easily make a conventional loan with a slightly higher rate the far more affordable choice over time.

Using Your Loan Estimate to See the Truth

So, how do you make a true apples-to-apples comparison? Your secret weapon is the Loan Estimate. Lenders are required to give you this standardized document, and it lays out all the costs in a clear format.

When you have a Loan Estimate for both a Conventional and an FHA loan, here’s what to zero in on:

- Page 1 (Loan Terms): Look right at the "Interest Rate" and the "APR." Is the FHA loan's APR way higher than its interest rate? That’s your red flag. It’s a dead giveaway that the mortgage insurance is inflating the true cost.

- Page 2 (Closing Cost Details): Find the "Upfront Mortgage Insurance Premium" on the FHA estimate. This is a hefty fee—typically 1.75% of your loan amount—that’s usually rolled right into your total loan balance. That means you'll be paying interest on it for the next 30 years.

- Page 3 (Comparisons): This page is gold. It shows a five-year cost comparison and confirms the APR. The loan with the lower APR is almost always the better deal in the long run.

The Impact of Closing Costs and Financed Premiums

While many closing costs like appraisal and title fees are similar for both loans, the FHA's upfront MIP is a massive difference-maker. Most people choose to finance this premium instead of paying it out of pocket, which feels easier at the moment but has long-term consequences.

By adding that premium to your loan, you’re not just borrowing more—you’re increasing your principal balance from day one and paying more in interest every single month for decades. A conventional loan doesn't have this specific upfront insurance cost, which helps keep your initial loan balance smaller and closer to the actual price of your home.

Making the Final Decision Conventional or FHA

So, how do you actually choose between a conventional and an FHA loan? It all comes down to a clear-eyed look at your finances and what you want to achieve. There’s no single "better" loan—just the one that fits your reality right now, whether that means getting into a home sooner or saving more money in the long run.

Your decision really hinges on three key numbers: your credit score, how much you have for a down payment, and your debt-to-income (DTI) ratio. Let's break down when each loan type pulls ahead.

When an FHA Loan Is Your Best Move

Think of an FHA loan as a powerful tool for opening the door to homeownership, especially if you're still building your financial profile. It's specifically designed to give borrowers who don't fit the perfect conventional mold a fair shot.

An FHA loan is probably the right call if you find yourself nodding along to these points:

- Your credit score is below 680. While you might technically qualify for a conventional loan with a 620 score, the interest rate and mortgage insurance premiums will likely be sky-high. FHA is far more forgiving in this range.

- Your down payment is the bare minimum of 3.5%. This is the FHA’s most famous feature. It’s what makes buying a home possible for so many people who haven't had years to save up.

- Your DTI ratio is on the higher side. If things like student loans or a car payment push your DTI past 43%, FHA’s more flexible guidelines can give you the wiggle room needed to get approved.

For many first-time buyers, the FHA loan isn’t just an option; it's the key that unlocks the door to homeownership. You can learn more about our dedicated FHA loan programs and see if you qualify at: https://mtg7.com/FHA.html

When a Conventional Loan Makes More Sense

On the other hand, if your finances are on solid ground, a conventional loan is almost always the smarter long-term financial decision. The biggest reason? You can eventually get rid of your mortgage insurance, which adds up to massive savings over the years.

A conventional loan is the clear winner if this sounds more like you:

- You have a credit score of 680 or higher. A stronger score doesn't just get you a better interest rate; it directly lowers your monthly Private Mortgage Insurance (PMI) cost.

- You can put down at least 3-5%. While a 20% down payment is the gold standard for avoiding PMI altogether, even putting down 5% or 10% will result in a lower PMI payment compared to the FHA's costly MIP.

- You want to ditch mortgage insurance. This is the killer feature. Once you hit 20% equity in your home, you can request to have PMI removed. That's a permanent reduction to your monthly payment that FHA loans just don't offer.

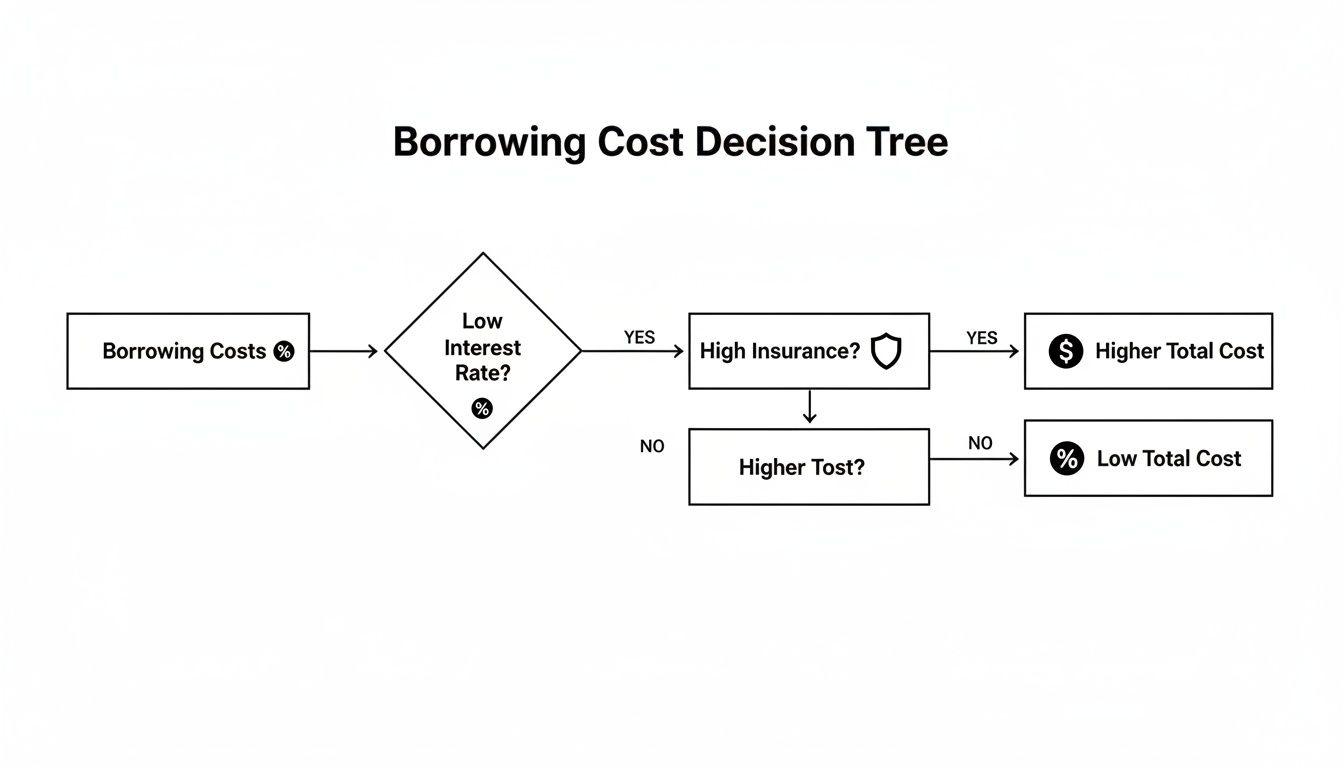

This decision tree helps visualize how an FHA loan, even with a seemingly low interest rate, can end up costing you more because of its mortgage insurance.

The chart makes it pretty clear: that FHA mortgage insurance premium sticks around and really inflates the total cost of borrowing over time.

Once you've made your loan choice, you'll want to stay organized through the entire buying process. Using a detailed real estate transaction checklist is a great way to make sure nothing falls through the cracks.

Common Questions About FHA vs. Conventional Loans

Even after comparing these loans side-by-side, you probably still have a few questions. That's completely normal. Here are some straightforward answers to the questions we hear most often.

Can I Refinance from an FHA Loan to a Conventional Loan?

Yes, and it’s a very popular move for homeowners. The main reason people switch from FHA to conventional is to get rid of the FHA Mortgage Insurance Premium (MIP). Once you've built up 20% equity in your home, refinancing into a conventional loan can eliminate that extra monthly cost for good.

Making this switch can save you a significant amount on your monthly payment and over the life of the loan. Just keep in mind, you'll need to meet the stricter credit and income standards required for a conventional loan.

Do Sellers Really Prefer Conventional Loans Over FHA?

In many cases, yes. It's not personal; it's usually about the appraisal process. FHA loans come with minimum property standards set by the government, and if an FHA appraiser flags mandatory repairs, it can slow down the sale or create headaches for the seller.

Conventional loans don't have these same government-mandated property rules. For a seller, that often means a smoother, faster, and more predictable path to the closing table.

In a hot market with multiple offers, your financing can be a tie-breaker. A conventional pre-approval letter might give you an edge with a seller who’s nervous about potential FHA repair requirements.

Can I Get an FHA Loan If I've Owned a Home Before?

Absolutely. A lot of people think FHA loans are only for first-timers, but that's a myth. The program is open to any qualified buyer, whether it's your first home or your fifth.

The goal of the FHA program is to make homeownership accessible, and its perks—like low down payments and flexible credit rules—are just as helpful for repeat buyers. The main catch is that you typically can't have more than one FHA loan at a time, and the house must be where you live.

Is It Possible to Get a Conventional Loan with Less Than 20% Down?

Definitely. The whole "you need 20% down" idea is a bit outdated. While putting down 20% is the magic number to avoid Private Mortgage Insurance (PMI) from the start, many lenders offer great conventional loan options with much less.

Here are a couple of popular choices:

- 3% Down Programs: Both Fannie Mae and Freddie Mac have programs designed for buyers with good credit who can put down as little as 3%.

- 5% Down: This is another common option that makes buying a home much more attainable.

If you put down less than 20%, you'll just have a monthly PMI payment for a while. Once you hit that 20% equity mark, you can request to have it removed.

Figuring out whether a conventional or FHA loan is right for you is a lot easier when you have an expert in your corner. At Mortgage Seven LLC, our team dives into your financial picture to find the loan that truly fits your goals. Ready to get clear answers? Schedule a personalized consultation with Mortgage Seven LLC today!