For most people trying to buy a home, the biggest hurdle isn't finding the right house—it's coming up with the cash for the down payment. That's where down payment assistance programs come in. They're specifically designed to bridge the gap between what you've saved and what you need to get the keys to your new home.

The Down Payment Hurdle and How to Clear It

The dream of owning a home can feel agonizingly close, yet stalled by one major financial challenge: the down payment. For decades, the standard advice has been to save up a 20% down payment. On a $375,000 house, that's a whopping $75,000 you'd need sitting in the bank.

That one number can feel like an impossible wall to climb, especially if you're a first-time homebuyer, saddled with student loans, or just starting to build a solid financial footing. But what if you could get over that wall years sooner than you ever imagined?

Think of down payment assistance (DPA) programs as a leg up. They give you the boost you need to reach the next level—homeownership—much faster than you could on your own. These aren't obscure loopholes. They are established, widely available programs created to make buying a home a reality for more people.

Debunking Common Homebuying Myths

One of the most persistent myths out there is that you have to put 20% down. While a bigger down payment certainly lowers your monthly mortgage payment and helps you avoid private mortgage insurance (PMI), it’s not the only way forward. The truth is, many conventional and government-backed loans allow for down payments as low as 3-5%.

Another common misconception is that DPA programs are only for very low-income families. While income is a factor, the limits are often surprisingly generous and are tied to the Area Median Income (AMI) of a specific county or city. This means many teachers, firefighters, nurses, and other moderate-income professionals are often eligible.

The real purpose of down payment assistance is to level the playing field. These programs are an investment in stable communities, helping responsible, mortgage-ready buyers achieve their goals without needing to spend a decade or more just saving up.

Mapping Your Path to Homeownership

Believe it or not, there are more than 2,500 different down payment assistance programs scattered across the country. They’re offered by state housing authorities, county and city governments, and even nonprofit organizations. This guide is your map to navigating that landscape.

We’re going to break down everything you need to know, from the different kinds of help you can get to what it takes to qualify. Getting a handle on your options is the first real step toward making your dream of owning a home happen.

Want to see how different down payment amounts could impact your monthly budget? Play around with our user-friendly mortgage calculators to get a better sense of the numbers. Armed with this guide and the right tools, you can confidently clear the down payment hurdle and walk through the door of your new home.

What Exactly Are Down Payment Assistance Programs?

Let's cut through the jargon. At its heart, a down payment assistance (DPA) program is just what it sounds like: a program designed to help you cover the hefty upfront costs of buying a home. Think of it as a financial bridge that gets you from "saving up" to "homeowner" much faster than you thought possible.

These programs aren't some secret handshake. They're typically offered by state and local governments, housing finance agencies, and even some nonprofits. Their mission is simple: help responsible, mortgage-ready buyers clear the biggest hurdle in their path—the down payment.

Instead of spending the next five or ten years pinching pennies for that big initial payment, DPA provides a direct shot of funds right when you need it. This does more than just get you the keys; it lets you start building equity and personal wealth right now.

The Real Purpose Behind These Programs

The big idea behind down payment assistance programs is to lower the amount of cash you need to bring to the closing table. It’s a game-changer for so many people who have good credit and a steady income but haven't had the chance to save up a massive lump sum.

But it’s also an investment in our communities. When more people can buy homes, neighborhoods become more stable, local economies get a boost, and families can plant permanent roots. DPA is all about creating a pathway to financial security for people who are otherwise completely ready for a mortgage.

The core function of DPA is to make homeownership more equitable. It provides the necessary boost to help creditworthy buyers who have a steady income but haven't yet accumulated the large lump sum needed for a traditional down payment.

And these programs are everywhere. The number of DPA programs in the U.S. recently hit a record high of 2,624. With the average benefit hovering around $18,000, they are a seriously powerful tool, especially when the median U.S. home price is pushing $375,000. You can explore more data on how DPA programs are expanding to meet the needs of today's buyers.

So, How Does It Actually Work?

Down payment assistance isn't a one-size-fits-all solution. It comes in a few different flavors, and we’ll dive deeper into those soon. For now, just know that this assistance is layered on top of your main home loan.

You'll still get your primary mortgage from a lender, but the DPA program provides a separate chunk of money to cover your down payment or even closing costs. It's not free money (usually), but it’s the next best thing.

Here’s a quick look at the most common structures:

- Grants: This is the unicorn—it’s essentially a gift that you never have to repay.

- Forgivable Loans: This is a loan that disappears over time. As long as you live in the home for a set number of years (say, five or ten), the loan is completely forgiven.

- Deferred Payment Loans: You get the money now but don’t have to pay it back until you sell the house, refinance your mortgage, or pay it off entirely. No monthly payments required.

The specific type of help you can get depends on the program and your personal situation. Getting familiar with these options is the first, most important step toward finding the perfect program to unlock the door to your new home.

To make this even clearer, here's a simple breakdown of how these programs help.

Down Payment Assistance At a Glance

| Benefit Type | How It Helps You | Common Provider |

|---|---|---|

| Grants | Provides funds for down payment/closing costs that never need to be repaid. | State/Local Housing Agencies, Nonprofits |

| Forgivable Loans | A loan that is forgiven over a set period if you remain in the home. | Government Agencies, Community Lenders |

| Deferred Loans | A zero-interest loan with no monthly payments; repaid upon selling or refinancing. | Housing Finance Authorities |

| Matched Savings | The program matches a portion of the funds you've saved for a home purchase. | Nonprofits, Government Programs (IDAs) |

| Employer Assistance | Your employer offers a loan or grant to help you buy a home, often locally. | Private Companies, Universities, Hospitals |

As you can see, the goal is always the same: to make the initial cost of buying a home manageable. The key is finding the right fit for your long-term plans.

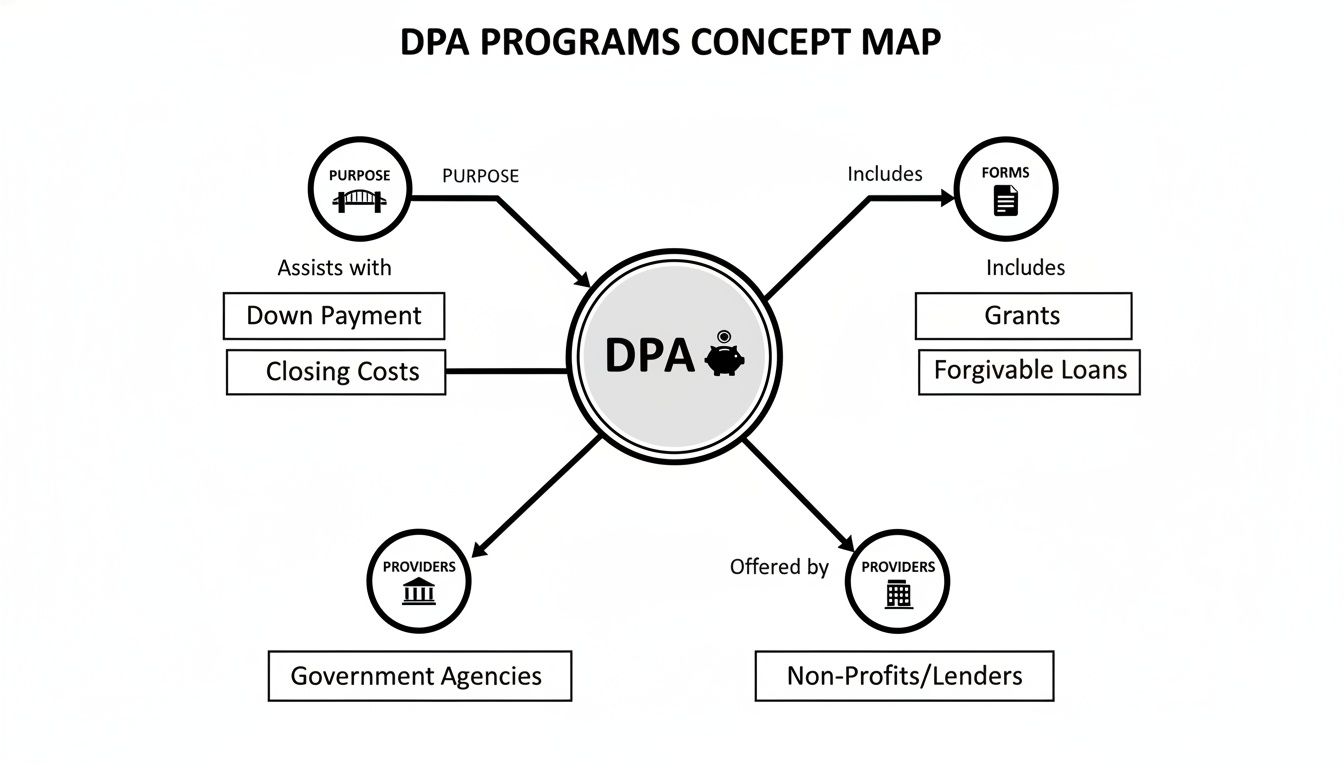

A Closer Look at the Main Types of DPA

So you know what down payment assistance is, but what does it actually look like? It's not a one-size-fits-all solution. Think of DPA like a toolbox—each tool is designed for a specific job, and the right one for you depends on your finances and what you're looking for in a home.

These programs generally fall into a few key categories. The biggest difference between them is how—or even if—you have to pay the money back. Getting a handle on these distinctions is the first step to finding a program that truly works for you.

This concept map breaks down how DPA programs connect, showing their main purpose, the different forms they take, and who typically provides them.

As you can see, DPA is all about bridging the gap to homeownership. It comes in various flavors, from outright grants to different kinds of loans, offered by everyone from state governments to local nonprofits.

Grants: The "Free Money" Option

Let's start with the fan-favorite: the grant. It’s the simplest and most sought-after type of DPA for one big reason—it’s a gift. A grant is money for your down payment or closing costs that you never have to repay.

It’s basically a scholarship for buying a house. Just like a student might get a scholarship for tuition, a homebuyer gets a grant to make their purchase more affordable. It’s that simple.

Because it’s essentially free money, competition can be stiff, and the eligibility rules are often stricter than for other DPA types.

Forgivable Loans: The Disappearing Debt

Next up are forgivable loans, which are a very popular option. With these, you receive a loan that gets completely wiped away as long as you meet certain conditions. The most common requirement is that you have to live in the house as your primary residence for a specific number of years, usually somewhere between five and ten.

Think of it as a loyalty bonus. Stay in the home for the required period, and the loan is forgiven. Vanishes. If you sell the home, refinance, or move out before that time is up, you’ll typically have to pay back a portion (or all) of the loan.

This is a fantastic deal for anyone planning to put down roots and stay in their new community for a while.

Deferred Payment Loans: The "Pay-Later" Plan

Another common DPA is the deferred payment loan. This is a loan you do have to repay, but not right away. In fact, you won’t make any monthly payments on it at all.

These loans usually have a 0% interest rate, and the balance only comes due when you sell the home, refinance your main mortgage, or pay it off completely. It’s designed to keep your monthly housing payment as low as possible in those first several years of homeownership.

A deferred payment loan takes the pressure off. It gives you the upfront cash you need to buy the home without adding another monthly bill to your budget, letting you focus solely on your primary mortgage payment.

This type of assistance pairs really well with certain mortgage products. If you're still figuring out your main loan, our guide comparing FHA and Conventional loans can help you see which one might be a better fit alongside a deferred DPA.

Matched Savings Programs: Rewarding Your Hard Work

Finally, there are matched savings programs, sometimes called Individual Development Accounts (IDAs). While not as common, they can be incredibly powerful for buyers who have some time to plan.

Here’s the deal: you open a special savings account and make regular deposits. The organization running the program then matches your savings, often contributing $2 or $3 for every $1 you put in, up to a set limit.

It’s like a 401(k) match for your down payment. Your dedication to saving is rewarded with a serious financial boost, helping you hit your down payment goal much faster. These programs are often run by nonprofits and are built to help people develop strong financial habits.

Getting to Grips With DPA Eligibility

Alright, you know what kind of help is out there. The next big question is pretty obvious: "Do I actually qualify?" This is the exact point where a lot of would-be homeowners talk themselves out of even trying. You might be surprised to learn that the qualifications for down payment assistance programs are often a lot more flexible than most people think.

Try to see the eligibility rules not as roadblocks, but as guardrails. They exist to make sure the funds go to the people these programs were created to help in the first place. With over 2,500 DPA programs scattered across the U.S., each one has its own unique rulebook. Still, most of them are built on a similar foundation. If you understand the core criteria, you're halfway there.

Let's walk through the requirements you'll most likely run into.

Let's Bust the Income Limit Myth

Your household income is almost always the biggest factor, but there's a huge myth that these programs are only for people with very low incomes. That's just not true. In reality, the income limits are usually calculated as a percentage of the Area Median Income (AMI) for your specific county or city.

What does that mean for you? In places with a higher cost of living, the income ceiling can be surprisingly high. It's common for a program to set its limit anywhere from 80% to 120% of the AMI. Depending on where you live, that range can easily include teachers, firefighters, nurses, and plenty of other working professionals.

Don't ever assume you make too much to qualify for down payment help. These limits change dramatically from one town to the next, and you might be shocked to discover you're well within the range for a local program.

The Most Common Eligibility Checkpoints

Beyond your paycheck, most down payment assistance programs will look at a few other key things to make sure you're a good fit. These benchmarks are there to help confirm you're ready for the long-term commitment of owning a home.

Here are the usual suspects you should be prepared for:

- Credit Score Minimums: While DPA programs want to make homeownership more accessible, they still need to see a solid credit history. The exact number will vary, but you’ll often need a score in the low-to-mid 600s to get your foot in the door.

- First-Time Homebuyer Status: This is a big one. Many (though not all) programs are geared toward first-timers. The U.S. Department of Housing and Urban Development (HUD) defines this pretty broadly: if you haven't owned your main home in the last three years, you generally qualify.

- Property and Purchase Price Limits: The program will also have rules about the house itself. There are often limits on the type of property (like a single-family home or a condo) and a cap on the purchase price to ensure the funds are used for modest, affordable housing.

The Homebuyer Education Requirement

One of the most common—and frankly, most valuable—requirements is completing a homebuyer education course. Seriously, don't think of this as a chore. It's a massive benefit. These courses are specifically designed to get you ready for the real-world experience of owning and taking care of a house.

Usually offered online, these classes cover the stuff you really need to know:

- Budgeting for Homeownership: It’s about more than the mortgage. You’ll learn about property taxes, homeowners insurance, and planning for repairs.

- Navigating the Mortgage Process: The course will demystify all the steps, from filling out the application to finally getting the keys at closing.

- Post-Purchase Responsibilities: You’ll learn the basics of home maintenance, how to handle unexpected repairs, and what it takes to be a financially savvy homeowner.

Finishing the course doesn't just check a box for the DPA program. It arms you with the confidence and knowledge you need to succeed as a homeowner for the long haul.

A Step-by-Step Guide to the DPA Application Process

Knowing you might be eligible for down payment assistance is a great feeling. But getting from that realization to actually securing the funds? That's where the real work begins. It’s a bit like assembling furniture—you have all the right pieces, but you still need a clear set of instructions to put them together correctly.

This guide is your set of instructions. The application process isn't just about filling out a single form. It's a journey that involves some research, a bit of paperwork, and working closely with the right people. Let’s break it down into simple, manageable steps.

Step 1: Find the Right Programs for You

First things first: you need to see what’s out there. Your search for down payment assistance programs should start with your state's Housing Finance Agency (HFA). These are the official sources, managing a ton of assistance options and keeping everything up-to-date.

Don't stop there, though. Many cities and counties have their own local programs with unique perks for residents. A quick web search for "[Your City] down payment assistance" can uncover some hidden gems you might otherwise miss.

Step 2: Gather Your Financial Documents

Once you've zeroed in on a few promising programs, it’s time to get your paperwork in order. The people who run these programs need to see proof of your income, assets, and job history to confirm you meet their guidelines. This is where being organized really pays off.

You'll almost certainly need to provide:

- Proof of Income: Your last 30-60 days of pay stubs and your W-2s from the last two years.

- Tax Returns: Be ready to hand over your federal tax returns from the past two years.

- Asset Information: Recent bank statements are a must. They show you have some skin in the game and can cover any required contributions.

To make this part easier, our home loan document checklist is a fantastic tool to make sure you’ve got all your ducks in a row.

Step 3: Complete Your Homebuyer Education

As we touched on earlier, most DPA programs insist that you complete an approved homebuyer education course. This isn't just a hoop to jump through; it’s genuinely designed to set you up for success as a homeowner.

These courses are usually offered online, so you can tackle them at your own pace. When you're done, you’ll get a certificate of completion—a non-negotiable part of your application. Just make sure the course you take is one that's accepted by the specific DPA program you're aiming for.

Partnering with a knowledgeable mortgage professional is not just a suggestion—it's essential. They act as your guide, ensuring you meet every deadline, submit the correct paperwork, and coordinate seamlessly between the DPA provider and your primary mortgage lender.

Step 4: Partner with a DPA-Approved Lender

This final step might be the most important one. Not every mortgage lender can work with every DPA program. You absolutely have to find a lender who is approved by, and has experience with, the specific DPA provider you've chosen.

An experienced lender, like our team at Mortgage Seven, knows the ins and outs of various down payment assistance programs. We can help you weave the DPA application seamlessly into your main mortgage application, making it one smooth process. That expert coordination is what helps you sidestep the common pitfalls that could otherwise throw a wrench in your home purchase.

Let's Find the Right DPA Program for You

Whew, that was a lot of information. We've walked through everything from grants that don't need to be repaid to forgivable loans and the rules that come with them. If there's one thing to take away from all this, it's that you have options—far more than most aspiring homeowners realize.

But knowing about these programs and actually getting one are two different things. The world of DPA is always shifting. New local programs pop up, state-level ones change their funding, and the rules get updated. Trying to track all of this on your own while also house hunting? It’s a recipe for a massive headache. That's why having an experienced guide in your corner makes all the difference.

Why You Need a Pro on Your Side

Think of a mortgage advisor as your DPA sherpa. Our job isn't just to crunch numbers for your loan. We're constantly keeping an eye on the huge variety of assistance programs out there, especially the niche, hyper-local ones that a simple Google search will almost certainly miss. We're your advocate, finding the perfect match between your financial picture and the available aid.

This isn't a one-size-fits-all process. We dig in to understand exactly what you need. Specifically, we'll help you:

- Pinpoint the Best Fit: We’ll look at your income, credit, and what you’re looking for in a home to zero in on the DPA programs that give you the strongest chance of approval.

- Get the Paperwork Right: We make sure your DPA application and your main mortgage application are perfectly aligned and submitted correctly, avoiding the common snags that cause frustrating delays.

- Keep Everything Moving Smoothly: We handle the back-and-forth between you, the lender, and the DPA agency. It’s our job to make sure all the moving parts come together without a hitch.

Your goal is to get the keys to your new home, not to become an expert on housing finance bureaucracy. Let a dedicated mortgage partner handle the complex details so you can focus on finding a place you love.

Your Direct Path to Owning a Home

For so many people, that down payment is the last major hurdle standing between them and homeownership. With the right help, what feels like a roadblock can become just another step in the process. We're here to help you see the possibilities, feel confident in your choices, and make a smart financial decision.

Here at Mortgage Seven, we specialize in this. We have deep roots and a ton of experience with the down payment assistance programs available right here in Virginia, as well as national options. We don't just find you a loan; we build a complete strategy to make your dream of owning a home actually happen.

Ready to see what you might be eligible for? Let's talk. Together, we can turn a vague idea of "someday" into a concrete plan, and I can't wait to see you at the closing table.

A Few Lingering Questions About DPA

It’s completely normal to have questions swirling around as you navigate the world of home financing. Even after learning about the different types of assistance and who qualifies, a few things might still be on your mind. Let's tackle some of the most common questions we hear about down payment assistance programs.

Can I Use DPA Funds for Closing Costs, Too?

Yes, in many cases, you absolutely can. While the name puts the spotlight on the "down payment," a lot of these programs are designed to be flexible. They often allow you to put the funds toward both your down payment and your closing costs, which usually add up to about 2% to 5% of the home's purchase price.

Of course, this isn't a universal rule. Every program has its own playbook, so you'll need to read the fine print to see exactly how the money can be spent. When a program does offer that flexibility, it can be a massive help, freeing up your own savings for moving day, new furniture, or other projects.

Do I Have to Be a First-Time Homebuyer?

Not always! It's a common misconception that DPA is only for people who have never owned a home. While many programs are certainly created to give first-timers a leg up, plenty of options are available for repeat buyers.

It all comes down to the official definition of a "first-time homebuyer."

The U.S. Department of Housing and Urban Development (HUD), for example, generally considers you a first-time homebuyer if you haven't owned your primary residence in the last three years. So, if you sold a house a while back and have been renting since, you might be back in the game.

The bottom line is to always check the specific rules for each program. Don't automatically assume you're out of the running just because you've had a mortgage in the past.

How Do I Find DPA Programs in My Area?

Hunting for the right program can feel a bit overwhelming, but you don't have to search blindly. There are a few key places you can look to find exactly what's available near you.

Here’s where to start your search:

- Your State's Housing Finance Agency (HFA): This is your best first stop. Every state has an HFA website that serves as the official hub for all state-sponsored programs.

- The HUD Website: The federal government's HUD website maintains a helpful resource page that points you to local homebuying programs all over the country.

- A Mortgage Expert: Honestly, this is usually the quickest and easiest path. A good mortgage broker is already an expert on the local DPA landscape and can pinpoint the programs that are a perfect match for your financial situation.

Knowing which programs are out there and how they fit your life is what we're here for. The team at Mortgage Seven LLC keeps a close eye on all the latest local and state programs so we can connect you with the right one. Let us take the guesswork out of it and guide you straight to the closing table.

Learn more and get started by visiting us at https://mtg7.com.

Article created using Outrank