A DSCR loan is a unique kind of mortgage designed specifically for real estate investors. The big difference? Lenders qualify you based on the property's rental income, not your personal salary or W-2s.

It’s essentially a business loan for your rental property. If the property itself can generate enough cash flow to cover the mortgage and its own expenses, you’re in a great position to get approved.

What a DSCR Loan Actually Means for Investors

Think about it this way: imagine you wanted to buy a small local business, like a laundromat. A bank using a similar approach wouldn't start by asking for your personal pay stubs. Instead, they'd ask a much more relevant question: "Does this laundromat make enough money each month to cover its own rent, utility bills, and our loan payment?"

A DSCR loan applies that exact same logic to a rental property. The property is the "borrower," not you personally. Lenders are laser-focused on its financial performance, which is a real game-changer for many investors.

Who Benefits Most from This Loan Type

While a traditional mortgage is the go-to for buying a primary home, DSCR loans are built for very specific investor profiles. You'll find they work especially well if you are:

- Self-Employed or a Business Owner: Your tax returns probably show a lot of legitimate write-offs. While great for lowering your tax bill, this can make it tough to qualify for a conventional loan. DSCR loans sidestep this completely by not requiring personal income documents.

- A Real Estate Portfolio Builder: Conventional lending rules often cap the number of mortgages you can hold at one time. Since DSCR loans assess each property on its own merits, they give you a clear path to scale your portfolio without hitting that personal financing ceiling.

- An Investor with Complex Finances: If your income is a mix of different sources or isn't easily proven with standard W-2s, a DSCR loan offers a much more direct route to financing your next investment property.

The entire approval process hinges on the Debt Service Coverage Ratio (DSCR). It’s the key metric that tells lenders if a property's income is strong enough. As we see all the time here at Mortgage Seven LLC, this one number makes DSCR loans incredibly powerful for the right investor.

At its heart, a DSCR loan answers one question: Can this investment stand on its own two feet financially? If the answer is yes, the door to financing opens, regardless of what your personal W-2 income looks like.

This is why so many savvy investors use DSCR loans as a strategic tool. When the primary goal is to acquire cash-flowing properties and maximize passive income from rental properties, this type of financing aligns perfectly with that business objective.

How to Calculate Your Debt Service Coverage Ratio

The entire concept of a DSCR loan hangs on one powerful calculation. This formula is what lenders use to quickly gauge the financial health of an investment property, and it's your key to getting approved. It answers a simple question: does the property make enough money to pay its own mortgage?

The formula itself is pretty straightforward:

DSCR = Net Operating Income (NOI) / Total Debt Service

Think of the result as a safety cushion. A DSCR of 1.0 means the property’s income exactly covers its mortgage payment—it breaks even. Anything above that is profit. For instance, a DSCR of 1.25 tells a lender the property generates 25% more income than it needs to cover its debt, which is a very healthy sign.

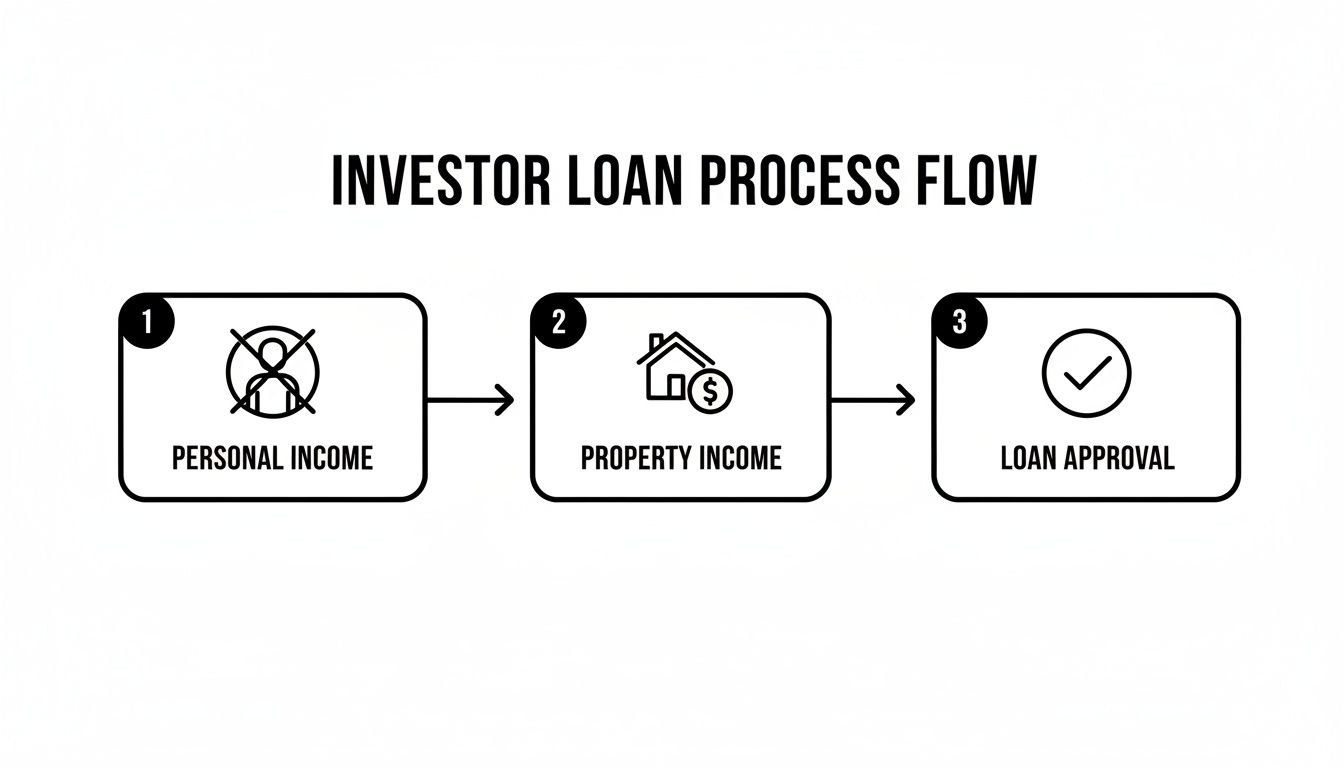

This flowchart shows how the DSCR loan process flips traditional lending on its head. It’s all about the property, not your personal paycheck.

As you can see, your W-2s and tax returns take a backseat. The star of the show is the property’s income-generating potential.

Step 1: Figure Out Your Net Operating Income (NOI)

First things first, you need to calculate your Net Operating Income, or NOI. This number represents the property's pure, unleveraged profit before you even think about the mortgage.

You'll start with the Gross Rental Income—the total rent you expect to collect in a year. From there, you subtract all the costs of running the property.

These operating expenses typically include:

- Property Taxes

- Homeowners Insurance

- Maintenance and Repairs

- Property Management Fees

- Utilities (if you're covering them)

- HOA Dues

A solid grip on understanding real estate cash flow is non-negotiable here. Be realistic with your expenses; underestimating them will give you a falsely high NOI and an inaccurate DSCR that won't hold up under scrutiny.

Step 2: Tally Up Your Total Debt Service

The other half of the equation is your Total Debt Service. This is simply the grand total of your mortgage payments for the year.

Most investors know this by its acronym, PITI:

- Principal: The part of your payment that actually pays down your loan balance.

- Interest: The fee you pay the lender for borrowing the money.

- Taxes: Your annual property taxes, broken down into monthly payments.

- Insurance: Your yearly homeowner's insurance premium, also paid monthly.

These four components make up your total housing payment. If you're trying to forecast this for a new property, you can get a good estimate by using one of our handy mortgage calculators available here: https://mtg7.com/Calculators.html.

DSCR Calculation Examples

To see how this all plays out in the real world, let's look at a few different scenarios. The table below shows how varying income and expenses can dramatically change a property's DSCR and, consequently, how a lender will view the deal.

| Scenario | Gross Annual Rent | Annual Expenses (NOI) | Annual Debt Service (PITI) | DSCR Calculation | Lender's View |

|---|---|---|---|---|---|

| Strong | $60,000 | $18,000 | $32,000 | ($60k – $18k) / $32k = 1.31 | Excellent candidate. Strong cash flow and low risk. |

| Acceptable | $50,000 | $15,000 | $32,000 | ($50k – $15k) / $32k = 1.09 | Likely approved, but might need a larger down payment. |

| Weak | $45,000 | $16,000 | $32,000 | ($45k – $16k) / $32k = 0.91 | Unlikely to be approved. Property does not cover its own debt. |

As you can see, a ratio above 1.25 is ideal, but many lenders will still consider loans with a DSCR closer to 1.0. Anything below 1.0 is almost always a hard stop, as it means the property is losing money each month.

Meeting Lender Requirements for a DSCR Loan

Figuring out your property's ratio is the first big hurdle. The next logical question, of course, is: what number do lenders actually want to see? Knowing the specific benchmarks is critical, as your DSCR directly impacts whether you get approved, what interest rate you'll pay, and the overall loan terms.

Think of the DSCR as your property's financial report card. While every lender has its own grading scale, there are some common thresholds you'll run into time and again.

A ratio of 1.0 is the bare minimum. This means the property's income is just enough to cover the mortgage payments, with nothing left over. It’s a break-even scenario. While that might sound okay on paper, lenders see it as walking a tightrope with no safety net.

The Magic Number for DSCR Loans

For most investors, the real target should be a DSCR of 1.25 or higher. This tells a lender the property generates 25% more income than it costs to carry the mortgage. That surplus cash flow is the safety cushion that makes an investment far more attractive and less risky in a lender's eyes.

A higher DSCR isn't just about getting the green light—it's about getting better terms. A ratio of 1.25 or more often unlocks more competitive interest rates and lower down payment options, saving you a serious amount of money over the life of the loan.

You really can't overstate the importance of that cushion. Financial institutions confirm that while most programs require at least a 1.0, the best rates and terms are reserved for properties hitting that 1.25 mark. A ratio hovering near 1.0 leaves an investor exposed; even a minor dip in income from a short vacancy could put the loan at risk of default. You can discover more about how major lenders view these critical ratios and their associated risks.

Beyond the Ratio: What Else Lenders Look For

While the DSCR is definitely the star of the show, it’s not a solo act. Lenders still need to verify you're a responsible borrower, even if they aren't digging through your personal pay stubs. They look at the whole picture to build a complete risk profile.

To get approved, you'll generally need to meet a few other key requirements:

- Minimum Credit Score: This varies, but most lenders want to see a personal credit score somewhere in the mid-600s or higher. A score above 700 will put you in a much stronger position to get better terms.

- Down Payment: These aren't low-down-payment loans. You should expect to put down at least 20% of the purchase price. For properties with a tighter DSCR or for investors with less experience, that number could easily climb to 25-30%.

- Liquidity Reserves: Lenders need to know you have cash on hand for a rainy day. You'll have to show proof of liquid assets—enough to cover several months of the property's PITI (Principal, Interest, Taxes, and Insurance) payments.

- Real Estate Experience: While it's not always a dealbreaker, some lenders feel more comfortable with borrowers who have a track record of owning and managing rental properties. If you're a first-timer, having a strong application in all other areas is that much more important.

DSCR Loans vs. Traditional Mortgages

Choosing the right loan for an investment property is a lot like picking the right tool for a job. A conventional mortgage might be the trusty hammer everyone knows, but for a real estate investor, a DSCR loan is often the specialized power tool that makes everything faster and more efficient.

So, what's the big difference? It all comes down to what the lender is looking at.

With a traditional mortgage, the spotlight is entirely on you, the borrower. Lenders dive deep into your personal finances, asking for W-2s, tax returns, and pay stubs to calculate your debt-to-income (DTI) ratio. Essentially, they need proof that your personal salary can handle the new mortgage payment on top of all your existing debts.

A DSCR loan flips the script completely. Instead of putting you under the microscope, the lender focuses on the investment property itself. The main question isn't about your personal income; it's whether the property can generate enough rent to cover its own mortgage. Your personal DTI becomes a non-issue.

The Key Difference: What Qualifies?

This isn't just a minor detail—it's a game-changer for many investors. If you're self-employed, a business owner, or part of the gig economy, proving your personal income in a way that satisfies a conventional lender can be a massive headache. DSCR loans create a path to financing that sidesteps this common roadblock.

The philosophy behind a DSCR loan is simple: a good investment should pay for itself. A traditional loan, on the other hand, operates on the idea that a good borrower should be able to pay for the investment, no matter how it performs.

This leads to two totally different application experiences. Applying for a conventional loan feels like a deep audit of your personal financial history. Applying for a DSCR loan is all about the property's numbers, focusing on documents like lease agreements and market rent appraisals.

Comparing Investment Loan Options

To really see where DSCR loans fit in, it helps to compare them not only to conventional loans but also to another popular option for entrepreneurs: the Bank Statement Loan. Each one serves a different purpose for a different type of borrower.

Here’s a quick breakdown to help you see which tool might be right for your toolbox.

| Feature | DSCR Loan | Conventional Loan | Bank Statement Loan |

|---|---|---|---|

| Primary Qualification | Property's Rental Income | Borrower's Personal DTI | Borrower's Business Deposits |

| Best For | Scaling rental portfolios | W-2 employees buying an investment | Self-employed with strong cash flow |

| Personal Income Docs | Not required | Required (W-2s, tax returns) | Not required (uses bank statements) |

| Loan Limits | Fewer restrictions | Limited to 10 financed properties | Varies by lender |

| Down Payment | Typically 20-25% | Can be as low as 15% | Usually 10-20% |

Ultimately, there's no single "best" loan—it all depends on your financial situation and investment goals. If you have a stable, easily documented W-2 income, a conventional loan might get you a slightly lower interest rate.

But for investors who want to scale their portfolio based on the performance of their properties, not their personal pay stubs, the DSCR loan is built for the business of real estate. It offers a level of speed and flexibility that traditional loans just can't match.

The Pros and Cons of Using DSCR Loans

A DSCR loan can be a fantastic tool for a real estate investor, but it's not a silver bullet. Like any financing option, it comes with its own set of advantages and potential trade-offs. This isn't a one-size-fits-all solution, so weighing the good against the not-so-good is the only way to know if it fits your investment strategy. Understanding what a DSCR loan really means requires looking at the complete picture.

The single biggest draw for most investors? No personal income verification. Lenders are laser-focused on the property's ability to generate cash flow, not your W-2s or last year's tax returns.

The Clear Advantages of DSCR Financing

This property-first approach unlocks some major benefits that can make growing your portfolio much simpler and faster. For many investors, these perks are total game-changers.

- Faster Closings: Think about it: when the lender doesn't have to comb through years of your personal tax documents and employment history, the whole underwriting process moves a lot quicker than a typical conventional loan.

- Ability to Close in an LLC: DSCR loans let you buy property under a business name, like an LLC. This is huge for liability protection, as it puts a wall between your personal assets and your investment business.

- Unlimited Portfolio Growth: Many conventional loan programs put a hard cap on how many properties you can finance. DSCR loans, on the other hand, look at each deal on its own merits, giving you a clear and scalable path to building a much larger portfolio.

These loans have become so popular for a simple reason: they skip the traditional income hoops and instead ask one simple question—does the property pay for itself? This shift has opened up real estate investing for countless people.

One of the most freeing aspects of a DSCR loan is its business-like approach. It treats your rental property like the asset it is, empowering you to scale your investments based on performance, not personal paperwork.

Potential Drawbacks to Consider

Of course, all that flexibility has to be balanced out somewhere. It’s critical to go in with your eyes open and understand the potential downsides before you commit.

The most significant trade-offs usually come down to cost and stricter qualification standards for the property itself. These loans just aren't designed for every deal or every investor.

Here are the main disadvantages to keep in mind:

- Higher Interest Rates: To offset the perceived risk of not verifying your personal income, lenders typically charge slightly higher interest rates on DSCR loans compared to conventional investment property mortgages.

- Larger Down Payments: Get ready to bring more cash to the table. Most lenders will require a down payment of at least 20-25%, and that number can climb even higher if your property's DSCR is cutting it close.

- Strict Property Requirements: The property is the star of the show, so it has to perform. If a deal has thin profit margins or a DSCR below 1.0, it simply won't get approved.

The demand for these loans has shot up recently, which tells you a lot about the changing world of investor financing. Market data shows they're playing a bigger and bigger role in real estate. You can dig deeper into the trends driving DSCR loan activity and see exactly how other investors are putting them to work.

How to Apply for Your DSCR Loan

So, you're ready to make a move. The good news is that applying for a DSCR loan is often a lot more straightforward than a traditional home loan. Why? Because the lender is laser-focused on the property's income potential, not your personal pay stubs.

Getting a handle on the process early on will make everything feel less daunting. It really boils down to an initial chat with a loan expert to discuss your strategy, followed by a deep dive into the property's numbers and paperwork before heading to the closing table.

Assembling Your Application Package

Forget about digging up old W-2s and personal tax returns. For a DSCR loan, the required paperwork is all about the asset itself and your business structure. Gathering these documents beforehand is the single best thing you can do to keep the process moving quickly.

Lenders will almost always ask for the following:

- A Signed Purchase Agreement: This is the official contract detailing the terms of your purchase.

- Current Lease Agreements: If the property is already rented, these leases prove its income. If it's vacant, the lender will rely on an appraiser's market rent analysis.

- An Itemized List of Property Expenses: This means pulling together the figures for property taxes, insurance, and any HOA dues. These are crucial for calculating the NOI.

- LLC Formation Documents: Many investors buy property under an LLC for asset protection, so you'll need to provide your company's organizing documents if that's your plan.

This is where having an expert on your side, like the team at Mortgage Seven, really pays off. We don't just find a lender; we find the right lender for your specific deal. We'll help you package your application to highlight the property's strengths, making sure every document paints a clear picture of a solid investment.

To get a head start, take a look at this helpful document checklist for mortgage applications. Walking in with your paperwork in order is the fastest way to turn an application into a closed deal.

DSCR Loan FAQs: Your Questions, Answered

Even with a solid grasp of the basics, real estate investors usually have a few lingering questions. It's totally normal. These loans work a bit differently, so let's tackle some of the most common things people ask before they dive in.

Getting these details straight is the final piece of the puzzle in deciding if a DSCR loan is the right move for your next investment.

Can I Use a DSCR Loan for My Primary Residence?

This one's a hard no. DSCR loans are built from the ground up for one thing: non-owner-occupied investment properties. Think of them as business loans where the "business" is the rental property itself.

Because the entire approval process revolves around the property's cash flow, not your personal paycheck, lenders strictly prohibit their use for a home you plan to live in. For your primary residence, you'll want to look at traditional financing like Conventional, FHA, or VA loans.

What Happens If My Property's DSCR Is Below 1.0?

A DSCR below 1.0 is a red flag for lenders. It means the property’s rental income isn't enough to cover the mortgage payment, which is the exact opposite of what this loan is designed for.

While most lenders won't touch a deal with a ratio under 1.0, some have niche programs that might consider a DSCR as low as 0.80. But be prepared—these are seen as much riskier deals. To get one approved, you'll need to show serious strength in other areas.

Lenders call these "compensating factors," and they usually include:

- A much larger down payment, often 30% or more.

- An excellent personal credit score.

- Hefty cash reserves sitting in your bank account.

You should also expect to pay a noticeably higher interest rate to compensate the lender for taking on that extra risk.

While a lower ratio is sometimes possible, the fundamental dscr loan meaning is tied to positive cash flow. A property that cannot support itself financially goes against the core principle of this loan type, making approval much more challenging.

Do I Need Landlord Experience to Get a DSCR Loan?

Not always. While having a history of successfully managing rentals certainly helps your case, many lenders are happy to work with first-time investors.

If you’re new to the game, a lender will just put more weight on other parts of your application. A strong credit score, a solid down payment, and a property with a great projected DSCR can often be more than enough to get you approved, even without prior landlord experience.

Ready to see if a DSCR loan is the right tool to grow your investment portfolio? The experts at Mortgage Seven LLC can analyze your deal, answer your specific questions, and connect you with the right financing for your goals. Explore your options today at https://mtg7.com.