When you're looking at a DSCR loan, the most important question is a simple one: can the property pay its own way? Lenders aren't digging through your personal pay stubs or tax returns. Instead, they zoom in on the property's cash flow using a key metric called the Debt Service Coverage Ratio (DSCR). A solid ratio is your golden ticket.

Your Guide to Qualifying for a DSCR Loan

For savvy real estate investors, especially those who are self-employed or have multiple income streams, the traditional mortgage process can feel like hitting a wall. The deep dive into personal tax returns and W-2s is often a long, frustrating ordeal.

DSCR loans completely flip that script. The focus shifts from your personal income to the property's ability to generate income.

Think of it like this: the property itself is the loan applicant, and its rental income is its resume. This common-sense approach is fueling major growth in the DSCR loan market. While conventional loans can drag on for 45+ days, private lenders are stepping in to close deals in as little as 10-21 days with more flexible terms.

The Four Pillars of DSCR Loan Qualification

So, what are the fundamental dscr loan requirements that lenders really care about? While the property's cash flow is king, a few other key factors create a full picture for a successful application.

- A Healthy DSCR Ratio: This is the non-negotiable heart of the loan. The lender needs to see that the property brings in more rent than it costs to carry the mortgage.

- A Solid Down Payment (LTV): You'll generally need to bring at least 20% to the table, which translates to a Loan-to-Value (LTV) ratio of 80% or less.

- Good Personal Credit: Your financial habits still matter. Most lenders want to see a minimum credit score, usually around 680 or higher, to show you're a reliable borrower.

- Sufficient Cash Reserves: Lenders need to know you have a safety net. You'll be asked to show enough cash on hand to cover several months of mortgage payments in case of a vacancy.

A DSCR loan is specifically built for non-owner-occupied investment properties. The entire concept rests on the idea that the property is a self-sustaining business that can cover its own debts without help from your personal salary.

This guide is your roadmap to understanding exactly what lenders like Mortgage Seven LLC are looking for. For an even deeper look at the criteria and paperwork involved, check out this excellent resource on Mastering DSCR Loan Requirements for Investors.

Now, let's break down the specific numbers and documents you'll need to get your loan approved.

DSCR Loan Requirements At a Glance

Here’s a quick-reference table summarizing the typical requirements you'll encounter when applying for a DSCR loan.

| Requirement Category | Typical Range or Minimum |

|---|---|

| Minimum DSCR Ratio | 1.0x – 1.25x (varies by lender and loan type) |

| Minimum Credit Score | 680 (some lenders may go as low as 620) |

| Down Payment (LTV) | 20% – 30% (resulting in a 70% – 80% LTV) |

| Cash Reserves | 3 – 6 months of PITI (Principal, Interest, Taxes, Insurance) |

| Property Type | Non-owner occupied, 1-4 unit residential, multifamily, mixed-use |

| Investor Experience | Not always required, but experience can lead to better terms |

This table provides a great snapshot, but remember that every lender has slightly different guidelines. It's always best to discuss your specific scenario with a loan expert.

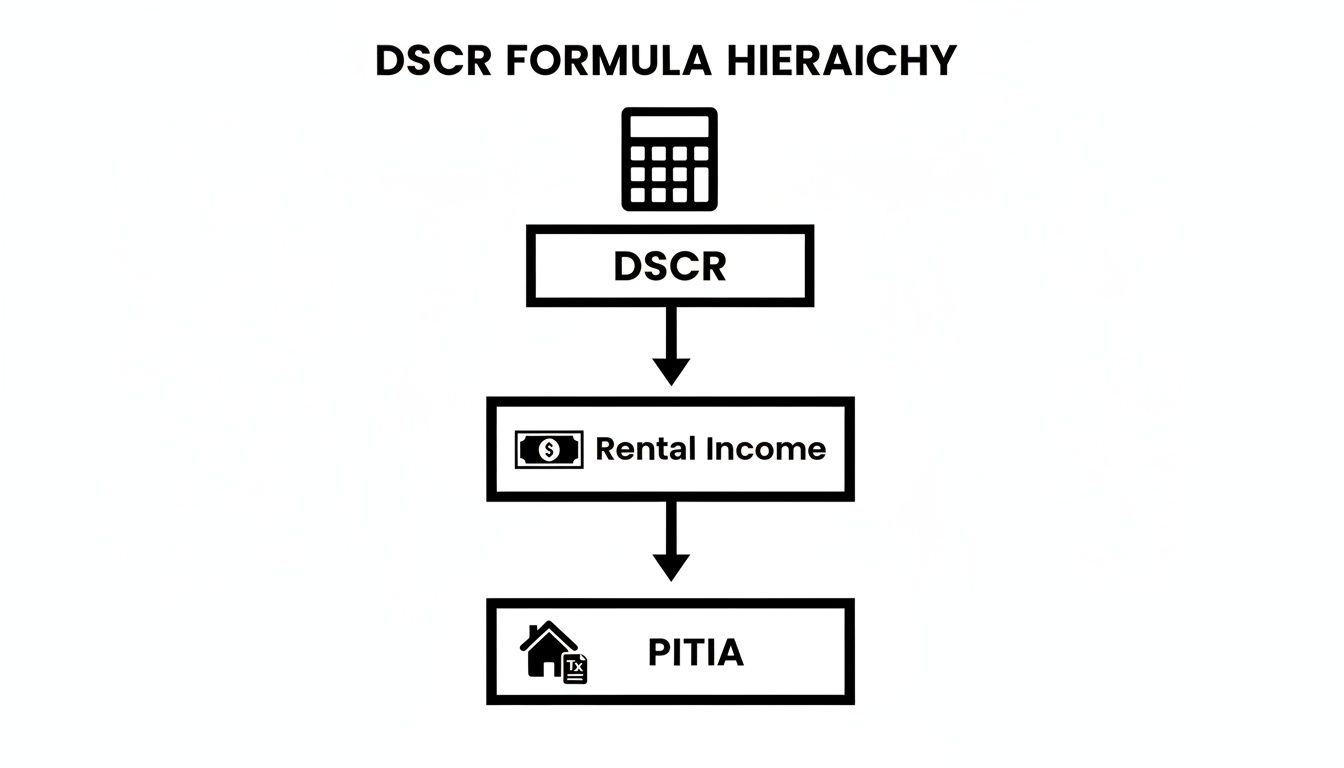

How Lenders Calculate Your DSCR Ratio

So, how do lenders actually figure out if a property makes the cut for a DSCR loan? It all boils down to a simple, yet powerful, formula. There’s no secret algorithm here—just basic math that answers one critical question: does this property’s income cover its expenses?

Getting a handle on this calculation is like seeing your investment property through the lender’s eyes.

The formula is surprisingly straightforward: Gross Rental Income ÷ PITIA = DSCR.

Think of the result as a quick financial check-up for your property. It tells the lender exactly how many times over the rent can cover the full mortgage payment. A ratio above 1.0 means you're in the green. Let's pull back the curtain on each part of this equation.

Figuring Out the Gross Rental Income

First up is Gross Rental Income. This is simply the total rent you collect before taking out any expenses. Lenders have two main ways of determining this number, and it all depends on whether you have a tenant in place.

- For an Occupied Property: If you've got a signed lease, the lender will use the rent amount right from that agreement. It’s a clean, documented income stream they can easily verify.

- For a Vacant Property: If the property is empty or you're buying it, the lender will rely on an appraisal. But it's not just any appraisal; they'll specifically request a Comparable Rent Schedule (also known as Form 1007). An appraiser researches similar local rentals to establish a fair market rent for your property.

It's worth noting that lenders almost always focus on the gross rent from the lease. While you might collect extra cash from things like parking spots or coin-op laundry, the core rental income is what really matters in this calculation.

What is PITIA?

The other side of the equation is PITIA. This little acronym is a big deal in the mortgage world. It stands for the total, all-in monthly cost of owning the property—the "debt" part of the Debt Service Coverage Ratio.

Here’s a quick breakdown:

- P – Principal: The part of your payment that actually reduces your loan balance.

- I – Interest: What you pay the lender for the privilege of borrowing their money.

- T – Taxes: Your annual property taxes, broken down into a monthly amount.

- I – Insurance: The monthly premium for your landlord or hazard insurance policy.

- A – Association Dues: Any required Homeowners' Association (HOA) fees, also figured as a monthly cost.

Lenders are obsessed with PITIA because it represents the absolute, must-pay cost of ownership. Things like repairs or management fees can vary, but PITIA is the fixed monthly obligation you can't escape.

A Real-World Example: Putting It All Together

Okay, let's connect the dots with a real-world scenario to see how this works in practice.

Let's say you're looking at a duplex that brings in $4,000 a month in rent. After your down payment, the lender calculates that the total monthly PITIA payment will be $3,200.

Here's the math:

- Gross Rental Income: $4,000

- Total PITIA: $3,200

- Formula: $4,000 ÷ $3,200 = 1.25 DSCR

A DSCR of 1.25 is solid. It tells a lender that the property's income covers the mortgage payment with a 25% surplus. That's a healthy cash-flow cushion that makes lenders feel confident about the deal.

Want to run the numbers on your own potential investment? Play around with our online mortgage and financial calculators to get a feel for potential payments. It's a great way to estimate your property's DSCR before you even start an application.

Understanding Minimum Ratios and Key Metrics

So, you’ve calculated your property’s DSCR. That's the first big hurdle, but it’s just the starting line. Think of that number as your entry ticket; to actually get the loan, you need to meet the lender's specific benchmarks. These aren't just arbitrary numbers—they're guardrails designed to make sure the deal is a sound investment for everyone involved, including you.

The headline number, of course, is the DSCR ratio itself. If a property has a DSCR of 1.0, it means the income exactly covers the mortgage payment and expenses. It’s breaking even. Lenders, however, are looking for a cushion, a safety net. This is why most won’t even consider a loan unless the DSCR is at least 1.20, and they really prefer to see 1.25 or higher.

A DSCR of 1.25 is the lender's green light. It signals that the property brings in 25% more cash than it needs to cover its mortgage payment (PITIA). That extra cash flow is a crucial buffer against the unexpected, like a tenant moving out or a sudden repair, which dramatically lowers the risk of the loan.

This quick flowchart breaks down the simple logic behind the DSCR calculation.

As you can see, the entire lending decision boils down to whether the property's rental income can comfortably handle its total obligations.

Beyond the DSCR Number Itself

A strong DSCR gets your foot in the door, but lenders will look at a few other key metrics to get the full picture. It's not just about the property; it's also about you as an investor. The good news is these factors often work together—strength in one area can sometimes make up for a slight weakness in another.

Here are the other big-ticket dscr loan requirements lenders will zero in on:

- Minimum Credit Score: While your personal W-2 income is off the table, your credit history definitely is not. Lenders need to see that you have a solid track record of managing debt responsibly. Most programs want to see a minimum FICO score of 680, though some can dip down to 620 if the rest of the application is rock-solid.

- Loan-to-Value (LTV) Ratio: This is just a fancy way of saying "how much are you putting down?" It compares the loan amount to the property's value. For DSCR loans, lenders typically draw the line at a 75-80% LTV, meaning you’ll need a down payment of at least 20-25%. A bigger down payment means a lower LTV, which always makes a lender feel more secure.

- Required Cash Reserves: Lenders want to know you won't be wiped out by the first leaky faucet. You’ll generally need to show you have enough liquid cash on hand to cover 3-6 months of the property’s full mortgage payment (PITIA). This proves you can weather a temporary vacancy or unexpected expense without missing a payment.

How These Metrics Influence Your Loan Terms

These requirements don't exist in a silo. They all interact to determine the final terms of your loan, from the interest rate to how much you can borrow. A top-tier profile—a high DSCR, great credit, and a low LTV—is what unlocks the absolute best financing options.

For instance, an investor with a 1.40 DSCR and a 760 credit score is in a much stronger position to get an 80% LTV loan than someone with a 1.15 DSCR and a 680 score.

The interest rate you get is also tied directly to these factors, plus what's happening in the broader market. DSCR loan rates often fall somewhere between 6.5% to 8.5%, but this can change based on your location. Hot investor markets like Florida and Texas might see more competitive rates, while states with more regulations could be on the higher end of that range. For a deeper dive into how rates vary by market, check out the analysis on DSCR Investors.

The connection between your DSCR and your loan terms is critical. A stronger DSCR doesn't just get you approved; it gets you a better deal.

How Your DSCR Ratio Impacts Loan Terms

| DSCR Ratio | Typical Maximum LTV | Credit Score Tier | Potential Interest Rate Impact |

|---|---|---|---|

| 1.25 or Higher | Up to 80% | Excellent (740+) | Most Favorable Rates |

| 1.10 – 1.24 | Up to 75% | Good (700-739) | Standard Rates |

| 1.00 – 1.09 | 70% or Lower | Fair (680-699) | Higher Rates, Stricter Terms |

The pattern here is crystal clear: the healthier your property's cash flow and your own financial profile, the more power you have at the negotiating table. This is why a solid grasp of all the key metrics is your best tool for securing the most advantageous dscr loan requirements for your next deal.

The Essential Document Checklist for Your Application

One of the best parts about a DSCR loan is how much simpler the paperwork is. If you've ever been through a conventional mortgage, you know the pain of digging up years of personal financial history. The DSCR loan requirements sidestep all that, focusing squarely on the property and your experience as an investor. You can finally stop searching for old W-2s and pay stubs.

Think of it less like a personal audit and more like putting together a business case for your investment. Lenders just need to confirm a few key things: the property's details, your ownership structure, and your financial capacity to close the deal. When you organize your documents around these core areas, the whole process becomes remarkably smooth.

Property-Specific Files

This is the bedrock of your application—the paperwork that proves the property is a solid, income-generating asset. These documents tell the story of the property itself, from its market value to its rental potential. You should expect to provide:

- Fully Executed Purchase Contract: If you're buying, this is the signed agreement detailing the terms of the sale.

- Property Appraisal: The lender will order this to get an independent valuation. Crucially, this often includes the Comparable Rent Schedule (Form 1007), which is vital if the property is currently vacant.

- Lease Agreements: For an occupied property, having the current, signed leases is non-negotiable. It’s the proof of the gross rental income you're claiming.

- Property Insurance Quote: You'll need a quote for a landlord or hazard policy. This is how the "I" in your PITIA (Principal, Interest, Taxes, Insurance, and Association dues) payment gets calculated.

Entity and Personal Files

This part is all about who—or what—is buying the property. Many experienced investors buy properties through an LLC for liability protection, and if that’s your plan, the lender needs to see the paperwork. They need to understand the company's structure and who has the authority to act on its behalf.

- LLC Operating Agreement or Corporate Bylaws: This spells out who owns the entity and who can legally sign the loan documents.

- Articles of Organization: This is the official document filed with the state that brought your company into existence.

- Driver's License or Government ID: Just standard identification for you and any other members of the LLC.

- Credit Report Authorization: While your income isn't the focus, your credit is. Lenders will pull your personal credit, as a strong score (usually 680+) is a key part of the puzzle.

Financial and Reserve Files

So, while lenders aren't combing through your personal tax returns, they absolutely need to see that you have the cash for the down payment, closing costs, and post-closing reserves. This proves you have the financial stability to not only buy the property but also to handle any unexpected vacancies or repairs down the road.

The most liberating aspect of a DSCR loan application is what's missing from the list. You will not be asked for personal tax returns, W-2s, pay stubs, or employment verification letters. This is the game-changer for self-employed investors and those with complex income streams.

To get ready for a smooth underwriting process, have these items on hand:

- Bank Statements: Usually the two most recent months from any account you plan to use for the down payment and closing costs.

- Investment Account Statements: If you're tapping into brokerage or retirement accounts, you'll need recent statements to show the funds are available.

- Gift Letter: If a family member is gifting you some of the funds, you'll likely need a formal letter from them confirming it's a gift, not a loan.

To make things even easier, we've put together a handy list to help you get organized. Check out our complete real estate investor document checklist at https://mtg7.com/checklist.html to make sure you have everything ready. Being prepared upfront helps partners like Mortgage Seven LLC push your application through quickly and lock in the best terms for your investment.

How to Strengthen Your DSCR Loan Application

Just meeting the minimum dscr loan requirements is one thing, but getting the best possible terms is another game entirely. To stand out, you need to present an application that screams "safe bet" to a lender. A little proactive effort can make a huge difference in your financing options.

Think of it this way: a basic application might get you across the finish line, but a truly polished one gets you a spot on the winner's podium with better rates and terms. It's all about showing the lender you're a prepared, financially sound investor they can trust.

Boost Your Down Payment to Lower LTV

One of the most straightforward ways to make your application shine is to bring more cash to the table. Putting down 25% or 30% instead of the bare minimum 20% creates a powerful ripple effect. A larger down payment lowers your Loan-to-Value (LTV) ratio, a critical metric lenders use to gauge risk.

When you have more of your own money invested, you have more skin in the game. This instantly makes you a more committed, less risky borrower in the lender's eyes and can often unlock better interest rates that save you thousands over the life of the loan.

Showcase Deep Financial Reserves

Lenders want to see that you can weather a storm, whether it's an unexpected vacancy or a major repair. While they might only require six months of PITIA payments in reserves, aiming higher demonstrates serious financial stability. Showing 9-12 months of reserves sends a very clear message.

A healthy reserve fund is your property's financial safety net. It tells the lender that a temporary hiccup in rental income won't ever put your mortgage payment in jeopardy, making you a far more reliable partner.

Maximize and Document All Property Income

Don't leave any money on the table when calculating your property's gross rental income. The primary lease is obviously the biggest piece of the puzzle, but other consistent revenue streams can sometimes be included to give your DSCR a nice bump.

- Parking Fees: Do you charge for dedicated parking spots? Make sure that separate, consistent income is documented.

- Storage Units: If the property has storage units that you rent out to tenants, that income counts.

- Pet Fees: Those non-refundable monthly pet fees can add up. Document them!

Properly accounting for these extra income sources can be just the thing to push a borderline DSCR into a much more comfortable—and approvable—zone.

Maintain a Flawless Credit Profile

Your personal credit history is a direct reflection of your financial discipline. Before you even think about applying, pull your credit report and clean up any errors, late payments, or high balances. A strong credit score, ideally 740 or higher, is a cornerstone of qualifying for the best dscr loan requirements. For more tips on keeping your score in top shape, check out our Credit resource page.

After submitting your application, staying on top of the process is key. Learning some effective strategies for following up on loan applications can help you maintain momentum and keep everything moving smoothly toward closing.

Partner with Mortgage Seven for Your Next Investment

Let's be honest, navigating the world of DSCR loans can feel a little overwhelming at first. But when you boil it all down, the concept is beautifully simple: the property’s own income is what gets you the loan, not your personal tax returns. This is a massive advantage for real estate investors, especially if you're self-employed or already juggling a few properties. The focus on the asset itself is what makes the DSCR loan such a powerful tool for building a real estate portfolio.

But knowing the rules of the game is one thing; winning is another. The market is packed with lenders, and every single one has its own unique quirks—different minimum ratios, preferred property types, and tolerance for risk. Finding the lender that's the perfect fit for your specific deal is where the real magic happens, and that's precisely what a good mortgage specialist does.

Your Advocate in a Complex Market

Think of us at Mortgage Seven LLC as your personal guide through this maze. Instead of you spending weeks calling different banks and getting the runaround, we bring our network of lenders directly to your doorstep. We’ve been doing this a long time, so we know which lenders love multifamily properties, who offers the sharpest rates for high-DSCR deals, and who is more willing to work with a first-time investor.

Here’s how we help:

- Access to More Options: We connect you with a whole ecosystem of wholesale lenders, unlocking programs and interest rates you simply can't find by yourself.

- Strategic Guidance: We sit down with you to truly understand your goals. We'll analyze your deal and figure out how to frame it to look as attractive as possible to underwriters.

- We Handle the Headaches: From the initial application all the way to the closing table, we manage the nitty-gritty details. Our job is to make the process smooth, clear, and efficient for you.

Having a broker like Mortgage Seven LLC on your side means you have a dedicated expert fighting for you. We know how to translate your investment vision into the numbers and language that lenders need to see, helping turn a great idea into a closed deal.

Let’s Build Your Portfolio Together

For real estate investors here in Fairfax, Virginia, and across the country, getting the right financing is the fuel for growth. You’ve already done the hard part of finding a great investment property—now let us handle the challenge of funding it. Whether this is your very first rental or you're a seasoned pro adding to your portfolio, we're here to help you get it done.

Don't let the financing process stall your progress. Let us do the heavy lifting and find the perfect DSCR loan for your property, so you can stay focused on what you do best: finding great investments.

Common Questions About DSCR Loans

Even after you get the hang of the basic DSCR loan requirements, it's natural to have questions about how they work in the real world. Real estate investing isn't one-size-fits-all, so let's walk through some of the most common questions I hear from investors.

Getting these details right can be the difference between a smooth closing and a deal that falls apart.

Can I Use a DSCR Loan for a Short-Term Rental Property?

You absolutely can, and this is where DSCR loans really shine. Lenders have gotten incredibly savvy about underwriting properties like an Airbnb or VRBO. They don't just guess; they use specialized appraisals and data to project what a property can earn as a vacation rental.

Instead of needing a signed one-year lease, the appraiser will pull data from platforms like AirDNA to build a solid income projection. This is a game-changer for investors looking to buy high-cash-flow properties in popular vacation spots, which often don't qualify for traditional financing.

Do I Need Prior Real Estate Experience to Qualify?

Not necessarily. While a proven track record as a landlord definitely helps your case, it's not always a deal-breaker. I've seen plenty of lenders happily work with first-time investors.

For a new investor, the lender just needs to see other signs of strength to get comfortable with the deal. Things like a high credit score (think 720+), a larger down payment (25-30%), and plenty of cash reserves go a long way in making up for a lack of experience.

Think of it from their perspective: these factors show you’re financially responsible and serious about making the investment work.

What Types of Properties Are Eligible for DSCR Loans?

DSCR loans are built for residential investment properties, but that category is wider than most people assume. You have a lot of flexibility in the types of assets you can target.

Typically, you can finance these properties with a DSCR loan:

- Single-Family Homes (SFRs)

- Condos and Townhomes

- 2-4 Unit Multifamily Buildings (like duplexes, triplexes, and fourplexes)

- Warrantable Condos

Some lenders will even consider small commercial properties or apartment buildings with 5-8 units, though the underwriting rules might be a bit different. The one hard rule? These loans are strictly for non-owner-occupied properties. You can't live in any of the units yourself.

Ready to see how a DSCR loan can help you land your next investment? The team at Mortgage Seven LLC lives and breathes this stuff. We know how to navigate the requirements and pair your deal with a lender who gets it.