Picture this: you've found the perfect rental property in Virginia, a real cash cow. But your personal tax returns, with all their business write-offs, don't exactly scream "perfect mortgage candidate." This is where a DSCR loan in Virginia changes the game. It’s a financing tool built specifically for real estate investors, and it focuses on one thing: the property's ability to pay for itself.

Unlocking Virginia Real Estate With A Different Kind of Loan

A Debt Service Coverage Ratio (DSCR) loan isn't your typical home mortgage. It's more like a business loan where the "business" is your investment property.

Conventional loans put your personal finances under a microscope. They demand W-2s, pay stubs, and tax returns to scrutinize your debt-to-income ratio. A DSCR loan in Virginia flips that script entirely. Instead, the lender asks a simple, powerful question: will the rent this property generates cover its own mortgage and expenses? This shift in focus makes it a fantastic tool for investors who don't fit into the traditional lending box.

Who Is This Loan For?

This property-centric approach is a breath of fresh air for many sharp investors across the Virginia market. The people who get the most out of a DSCR loan usually fall into a few categories:

- Self-Employed Investors: If you're an entrepreneur, you know tax returns don't tell the whole story. DSCR loans look past personal income documents, which is a major advantage.

- Portfolio Builders: Trying to scale your portfolio? Traditional lenders often cap the number of mortgages you can have. DSCR loans don't have those limits, letting you grow without restriction.

- Investors Needing Speed: With less personal paperwork to sift through, DSCR loans often close much faster. In hot markets like Northern Virginia or Richmond, that speed can be the difference between winning and losing a deal.

Think of it this way: a DSCR loan shifts the entire focus from your ability to pay the mortgage to the property's ability to pay its own way. It treats your rental as the business it is, making it a go-to for serious investors.

DSCR Loans vs. Conventional Loans At A Glance

To really understand the difference, let's break it down. A conventional loan feels like a personal financial audit. A DSCR loan, on the other hand, is more like making a business pitch for the property itself—the lender is essentially backing your investment's profit potential.

This table highlights the fundamental differences in how these two loan types operate for an investor in Virginia.

| Feature | DSCR Loan | Conventional Loan |

|---|---|---|

| Primary Focus | Property's rental income and cash flow | Borrower's personal income (W-2s, tax returns) |

| Income Verification | Lease agreements and/or market rent appraisal | Pay stubs, tax returns, employment history |

| Property Type | Investment properties only (1-4 units, multi-family) | Primary residences, second homes, investment properties |

| Number of Properties | Typically no limit | Usually capped at 10 financed properties |

| Down Payment | Typically 20-25% or more | Can be as low as 3-5% for primary homes; higher for investments |

| Interest Rates | Generally slightly higher than conventional rates | Generally lower, especially for primary residences |

| Closing Speed | Often faster due to streamlined documentation | Can be slower due to extensive personal underwriting |

Ultimately, the choice depends on your specific situation. While a conventional loan might offer a lower rate, the DSCR loan provides flexibility and scalability that many investors find invaluable.

Your personal income from a 9-to-5 or another business takes a backseat. The property's performance is what truly matters. To see where DSCR loans fit in the bigger picture, checking out a complete guide to real estate financing options is a great next step. And as you weigh your choices, you can dive deeper into the specifics of the DSCR loan program to see how it can help you grow your Virginia real estate portfolio.

How to Calculate Your DSCR for Virginia Properties

Alright, let's get into the nuts and bolts. To unlock DSCR financing for your next Virginia investment, you need to master one simple calculation. This isn't high-level calculus; it’s a straightforward formula that tells a lender one thing: can this property pay for itself?

The formula at the heart of it all is:

Gross Rental Income / Total Housing Expense = DSCR

Think of it as the property's financial health check. A high score means the property is a great candidate for a loan, and your path to approval gets a whole lot smoother.

Breaking Down the Two Sides of the DSCR Equation

To get an accurate DSCR, you first need to understand what numbers go where.

Gross Rental Income: This is the top-line number—the total rent you expect to collect before taking out a single penny for expenses. If you have a tenant with a lease, it’s simply the annual rent. If the property is vacant, the lender will rely on an appraiser's market rent analysis to project the income.

Total Housing Expense: This is what the pros call PITIA. It’s the all-in cost of owning the property. It includes the Principal and Interest on the mortgage, property Taxes, homeowner’s Insurance, and any Association (HOA) fees.

Let’s Run the Numbers: A Virginia Example

Let's make this real. Say you’re looking at a single-family rental in a Richmond suburb that can realistically pull in $2,500 a month in rent.

Your annual gross rental income is easy to figure out: $30,000 ($2,500 x 12 months).

Now, for the expenses (the PITIA):

- Mortgage (Principal & Interest): $1,600/month

- Property Taxes: $250/month

- Homeowner's Insurance: $100/month

- HOA Dues: $50/month

Add it all up, and your total monthly housing expense is $2,000. On an annual basis, that’s $24,000.

The Calculation: $30,000 (Annual Income) / $24,000 (Annual PITIA) = 1.25 DSCR

What does this 1.25 mean? It tells the lender that the property brings in 25% more income than what’s needed to cover its debts. That’s a healthy buffer and a number that gives lenders confidence. In fact, a 1.25 DSCR is often the gold standard for getting the best rates and terms. If your ratio dips below 1.0, it signals that the property can't cover its own expenses, which is a red flag.

How Virginia’s Diverse Markets Change the Math

Keep in mind that your DSCR will look different depending on where you invest in the Commonwealth.

A vacation rental in Virginia Beach might have killer summer income but also much higher insurance premiums due to coastal risks. A property near UVA in Charlottesville could offer steady rent from students, but you’ll need to account for potential vacancy and turnover costs between semesters.

The good news is that lenders understand these nuances. For instance, we recently saw a single-family home in Stafford get approved with a 1.11 DSCR. The loan was for $217,781 on a $352,000 property. This just goes to show that a solid property in a good area can still get funded, even if the DSCR isn't textbook perfect.

Want to crunch the numbers on a deal you're considering? A great first step is to get a handle on your potential monthly payment. You can use our online mortgage calculators to estimate your PITIA and see how your investment stacks up.

DSCR Loan Rates and Terms in Virginia: What to Expect

Let's get down to the brass tacks: what kind of rates and terms are you actually looking at for a DSCR loan in Virginia? This is where these loans really show their unique character. Unlike a conventional mortgage that's all about your personal income, the lender's focus here is squarely on the property's ability to pay for itself.

Because the risk is tied to the investment's performance, you'll generally see slightly higher interest rates than on a primary home loan. But in exchange, you get incredible flexibility. The rate isn't based on your W-2 or pay stubs. Instead, lenders are focused on the key deal metrics: your DSCR, personal credit score, and how much skin you have in the game (your down payment). A strong DSCR and a healthy down payment tell a lender the deal is solid, which can definitely help you land better terms.

Key Financial Factors to Plan For

The biggest number to prepare for is the down payment, which the banks see as the loan-to-value (LTV) ratio. For most DSCR loans in Virginia, lenders want to see a minimum of 20% down. To really get the most competitive rates, though, you should plan on putting down 25-30%.

Beyond that initial investment, here are the other core components of the deal:

- Interest Rates: These aren't one-size-fits-all. They fluctuate with the market and the strength of your specific deal. A cash-flowing property in a hot market like Alexandria is naturally going to look less risky and could command a better rate.

- Loan Term: The good news is you can get long-term stability. The most common structure is a 30-year fixed-rate mortgage, which means your principal and interest payment is predictable for the life of the loan—perfect for a buy-and-hold strategy.

- Origination Fees and Closing Costs: Just like any other mortgage, there are costs to close the deal. You can expect to pay standard fees for things like the appraisal, underwriting, and title work.

What Are Typical Rates in Virginia Right Now?

So, what does this look like in the real world? Recent market data gives us a clear picture. In the second quarter of 2024, the average interest rate for DSCR loans on 77 funded deals right here in Virginia was 8.07%. The average loan amount was $223,062, which shows these are a go-to tool for financing the typical single-family or small multi-family rental. You can see more data on these Virginia DSCR loan trends to get a feel for how different deals are structured.

Real-World Example: An investor recently used a DSCR loan from RCN Capital to finance a duplex portfolio in Petersburg. They locked in a 7.965% fixed rate on a $592,800 loan. This just goes to show that even for larger, more complex investments, you can secure competitive, stable financing when the property's cash flow numbers work. It's all about that balance between risk and reward.

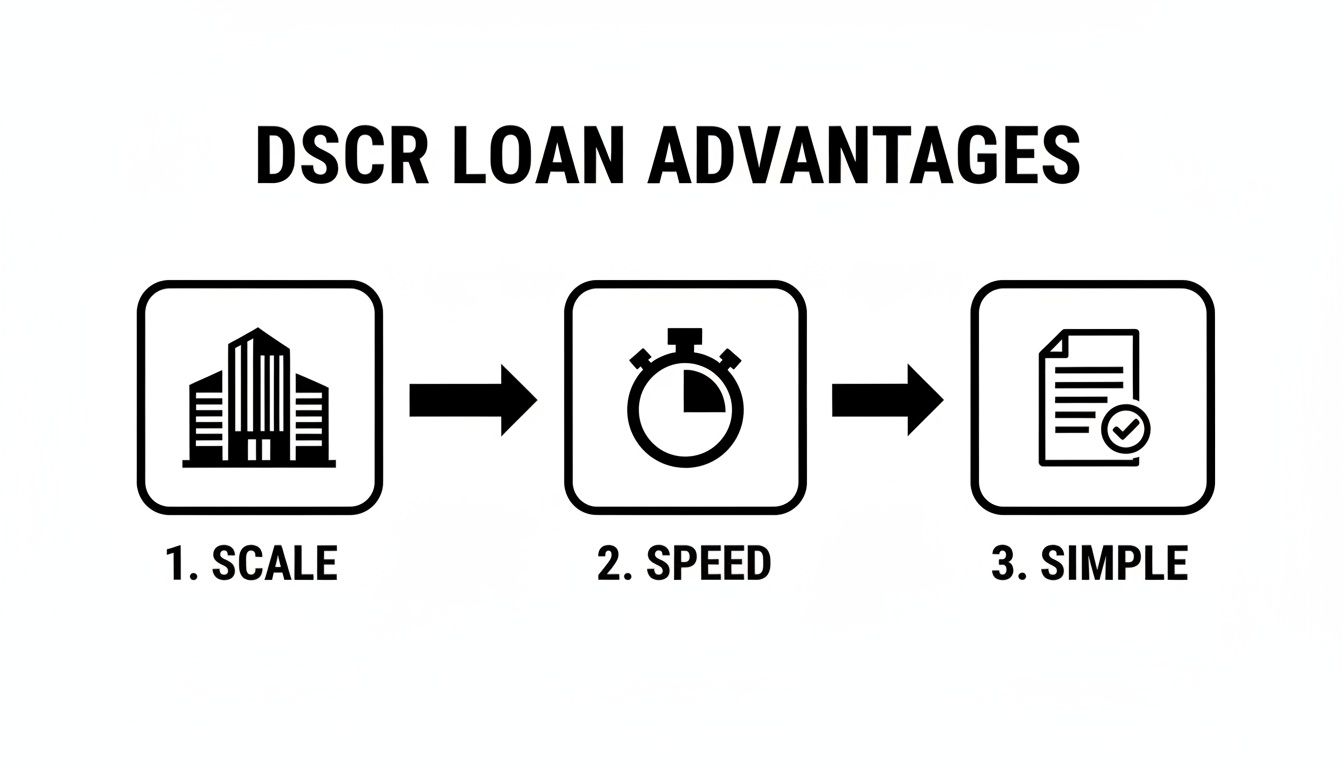

Strategic Advantages of Using a DSCR Loan

For a sharp real estate investor in Virginia, a DSCR loan isn't just another financing option; it's a strategic lever for serious growth. The real magic of these loans lies in how they see your investments—as a business, plain and simple. It’s not about your personal paycheck; it’s about the property's ability to pay for itself.

This fundamental shift opens up doors that conventional mortgages keep firmly shut.

Perhaps the biggest win is the ability to scale your portfolio without hitting an artificial ceiling. Most traditional lenders get nervous and cut you off after you've financed a certain number of properties, often around ten. A DSCR loan in Virginia blows right past that limit. Because the loan is tied to the property’s cash flow, not your personal borrowing capacity, you can keep acquiring profitable rentals as long as the numbers make sense.

Accelerate Your Portfolio Growth

In a hot market like we're seeing in many parts of Virginia, speed is everything. The streamlined underwriting process for a DSCR loan is a game-changer. Instead of digging through years of your personal tax returns and pay stubs, the lender focuses almost entirely on the property itself.

That translates to a much faster closing, giving you a serious edge. You can make stronger offers and lock down deals while other buyers are still drowning in paperwork. This is especially powerful for:

- Self-employed investors: If you're an entrepreneur, your income can look complicated on paper. DSCR loans bypass that headache by focusing on the asset's performance, not your W-2.

- Investors focused on asset protection: You can (and should) secure a DSCR loan through your LLC. This creates a critical firewall between your personal wealth and your investment properties, a non-negotiable for anyone building a real portfolio.

Think of it this way: a DSCR loan lets you operate like a real business. It frees you up to make quick, smart investment decisions based on the deal itself, not the constraints of your personal finances.

The Clear Choice for Rapid Scaling

There's a reason seasoned investors are flocking to these loans. The numbers don't lie: nationwide, 68% of real estate investors now prefer DSCR loans specifically for scaling their portfolios. Why? Because they're seeing growth 3.2 times faster than those sticking with old-school financing.

This isn't just a trend; it's a strategic shift in how smart investors are building wealth. By zeroing in on the property’s viability, a DSCR loan in Virginia offers the most direct and efficient path to building a powerful real estate empire. If you want to dive deeper into how investors are doing this, you can check out the latest DSCR loan statistics for yourself. The data makes it clear: for serious investors, this is the financial vehicle of choice.

Navigating the DSCR Loan Approval Process

Getting a DSCR loan in Virginia is a completely different ballgame compared to a typical mortgage. Instead of putting your personal finances under a microscope, the entire process revolves around one central question: does this property make good business sense? It’s all about the investment's ability to pay for itself.

Your first step is simply understanding what the lender needs to see. And, just as importantly, what they don’t need. Forget digging through years of personal tax returns or hunting down old W-2s. The property is the star of this show.

Core Documentation Requirements

To get the ball rolling, you'll need to gather a handful of documents that tell the story of the investment property itself.

- Purchase Agreement: This is the signed contract to buy the property.

- Property Details: Basic info like the address, property type, and the number of units.

- Lease Agreements: If you have current tenants, their leases are gold. They prove the existing rental income.

- Bank Statements: You'll need to show you have the cash on hand for the down payment and reserves—lenders typically want to see 6 months of mortgage payments (PITIA) saved up.

- LLC Operating Agreement: A must-have if you're buying the property under a business entity for liability protection.

This straightforward approach is exactly why so many investors are drawn to DSCR loans.

As you can see, the simpler paperwork directly translates into closing deals faster and building a rental portfolio more efficiently here in Virginia.

The Underwriting Journey

Once you’ve sent in your documents, the lender’s underwriting team gets to work. Their job is to double-check everything and make sure the deal is solid. They're going to zero in on a few key things.

First, they'll order a professional property appraisal. This isn't just about confirming the sale price; the appraiser will also complete a rental analysis (Form 1007) to establish the property's fair market rent. This is absolutely critical, especially if the property is currently vacant. Next, they'll run the numbers, comparing the rental income to the total mortgage payment (PITIA) to calculate the DSCR. They're looking for a ratio of at least 1.25.

The underwriter's goal is simple: confirm the property can stand on its own financially. A clean appraisal and a strong DSCR are your two most powerful allies in this stage of the process.

Finally, they’ll verify you have enough cash in the bank. Lenders need to see that you can cover the mortgage during a vacancy or handle an unexpected repair without missing a payment. If you're buying a short-term rental, putting together a professional vacation rental business plan can really make your application shine by proving you've thought through the financials.

A common mistake I see is investors getting too optimistic with their rent estimates or not accounting for Virginia's true property tax and insurance costs. These little things can derail a deal fast. This is where working with a broker like us at Mortgage Seven really pays off—we help you get all your ducks in a row from the start, avoiding those common pitfalls and making the whole process feel effortless.

Finding the Right Virginia DSCR Loan Partner

Choosing the right lender for your DSCR loan in Virginia is just as important as finding the right property. You need a partner who gets the local market—someone who understands the difference between the high-turnover rental scene in Northern Virginia and the steady, reliable demand down in Norfolk. Having a real expert in your corner can literally make or break a deal.

At Mortgage Seven, Virginia real estate is what we do, day in and day out. We have a deep-seated understanding of the Commonwealth's unique rental markets, which allows us to help you find financing that genuinely aligns with your investment strategy. We're not just pushing papers; we're helping you build a roadmap for success.

Why Partner with a Virginia-Based Broker?

When you work with a local specialist, you gain a serious edge. We’ve spent years building a network of lenders who actually get DSCR loans, so we can hunt down competitive rates and terms that fit the property you're buying. We know exactly which lenders are bullish on short-term rentals in Virginia Beach and who to talk to for a multi-family property in Richmond.

That kind of on-the-ground knowledge just makes the whole process smoother and faster.

By focusing on the property's performance rather than your personal tax returns, a DSCR loan offers a direct path to scaling your portfolio. With the right guidance, you can close deals faster and build your real estate business with confidence.

Ready to take the next step in your investment journey? Our team is here to give you the personalized, expert guidance you need to make it happen. To explore your options and get your questions answered, schedule a consultation with Mortgage Seven today.

Got Questions About Virginia DSCR Loans? We’ve Got Answers.

As you get deeper into the world of Virginia real estate investing, you're bound to have some specific questions about how DSCR loans fit into your strategy. We hear them all the time. Let's tackle the most common ones head-on.

I'm New to Real Estate Investing. Can I Still Get a DSCR Loan?

Absolutely. While having a portfolio of successful rentals never hurts, plenty of lenders in Virginia are happy to work with first-time investors.

The real star of the show here isn't your resume—it's the property's income potential and your personal credit. If the deal makes sense and the numbers work, a strong DSCR can easily make up for a lack of landlord history. The key is finding the right lender, and that's where a good broker can make all the difference.

What Kind of Properties Can I Buy with a DSCR Loan in Virginia?

You've got a lot of flexibility. These loans are designed for non-owner-occupied residential properties, which covers a wide range of investment types.

Think of things like:

- Single-family homes

- Condos and townhouses

- Small multi-family properties (2-4 units)

You’ll also find lenders who offer programs for bigger multi-family buildings (5+ units). And it’s not just for long-term rentals anymore; DSCR loans are increasingly popular for financing short-term and vacation rentals in hotspots from the Blue Ridge Mountains to the shores of Virginia Beach.

Should I Expect to Put More Money Down for a DSCR Loan?

In most cases, yes. Plan on a down payment of at least 20%, though putting down 25% is often the sweet spot for snagging the best interest rates.

It makes sense when you think about it. The lender is banking on the property's cash flow, not your W-2 income. A larger down payment shows you have serious skin in the game, which reduces the lender's risk and usually gets you a better deal in return.

At Mortgage Seven LLC, our team has deep expertise in the Virginia real estate market and can guide you to the perfect DSCR loan for your investment goals. Start your journey by visiting us at https://mtg7.com.