Refinancing your FHA loan isn't about starting from scratch. Think of it more like a tune-up for your mortgage—a chance to adjust the terms to better fit where you are in life right now. The FHA has built-in guidelines that create clear paths for homeowners to lower their payments, tap into their home's equity for cash, or simply get a better loan structure.

Understanding Your FHA Refinance Options

Whether you're trying to free up some cash flow each month, pay off your home faster, or fund a big project, there's an FHA refinance program designed for that exact purpose. Each one comes with its own set of rules and is built for a specific financial goal. The first step is figuring out which one matches what you're trying to accomplish.

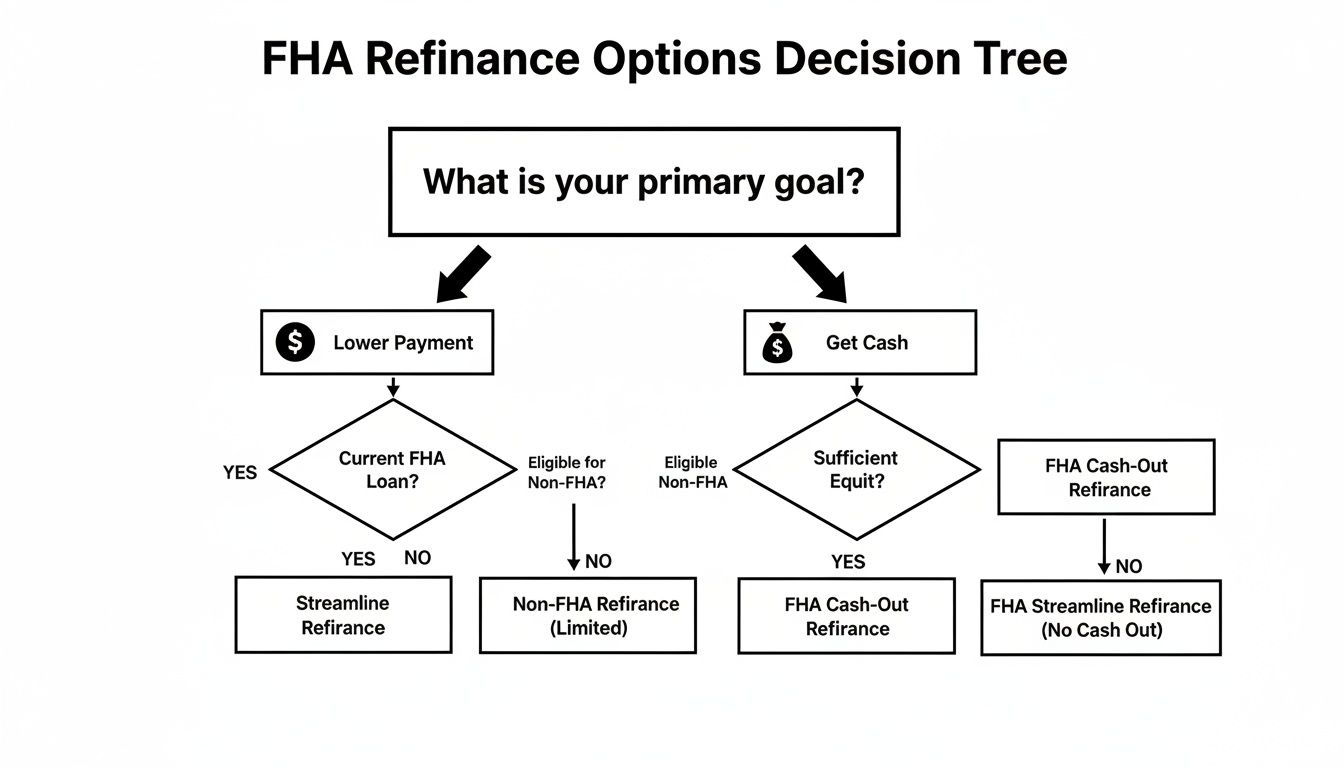

You really have three main options: the FHA Streamline, the FHA Cash-Out, and the classic Simple Rate-and-Term refinance. Each one is a different tool for a different job.

Mapping Your Refinance Journey

Let's imagine you're at a fork in the road. One path is a straight shot, a high-speed expressway. Another is a bit more involved but lets you pick up some much-needed cash along the way. The third is just a simple repaving project for the road you're already on. This is a great way to think about your FHA refinance choices.

- FHA Streamline Refinance: This is your expressway. It's designed to be fast and efficient, getting you a lower interest rate and monthly payment with as little paperwork as possible. In many cases, you won't even need a new appraisal. If all you want is a better rate, this is your go-to.

- FHA Cash-Out Refinance: This is the path where you can grab some funds. You'll replace your current mortgage with a new, larger loan and get the difference in cash. It's the perfect tool for financing major home improvements or consolidating high-interest credit card debt.

- Simple Rate-and-Term Refinance: This is the road improvement project. It lets you tweak the terms of your loan without taking cash out. You can lock in a better interest rate, switch from a 30-year to a 15-year mortgage to pay it off sooner, or do both at the same time.

This decision tree gives you a quick visual of which path makes sense based on what you're trying to achieve.

As you can see, your main motivation—whether it's saving money on your monthly payment or needing cash now—is what points you toward the right program. A lot of homeowners find that refinancing your mortgage to consolidate debt is a smart move, helping them bundle multiple payments into one and often lowering their overall interest costs.

Which FHA Refinance Path Is Right for You

To make it even simpler, here’s a quick comparison to help you match your financial goal with the correct FHA refinance program.

| Refinance Type | Primary Goal | Appraisal Usually Required? | Can You Get Cash Back? |

|---|---|---|---|

| Streamline | Lower your interest rate and monthly payment | No | No |

| Cash-Out | Access your home's equity as cash | Yes | Yes |

| Simple Rate-and-Term | Change your loan's rate and/or term | Yes | No (or very limited) |

This table should give you a clear starting point.

Knowing your options is the most important part of the process. Our team at Mortgage Seven LLC is here to walk you through the full scope of our FHA loan programs. This overview gives you the map—now let's dive into the specific rules for each route.

The FHA Streamline Refinance: Your Fast Track to Savings

If there's an express lane for refinancing, this is it. The FHA Streamline Refinance was built for one simple, powerful purpose: to help you lock in a lower interest rate and slash your monthly payment with the least amount of hassle.

Think of it this way: the FHA already backs your current loan. Since you're a known quantity, they've created a shortcut to help you take advantage of better rates without making you jump through all the hoops of a brand-new mortgage application. The whole idea is to reward responsible FHA borrowers with a straightforward way to save money.

What Puts the "Streamline" in Streamline?

The program absolutely earns its name by trimming away the most time-consuming parts of a typical refinance. Because the FHA is already insuring your loan, the lender's risk is lower, which allows them to cut a lot of the usual red tape.

Here's what you generally get to skip:

- No New Appraisal: This is a huge one. In most cases, you won't need a new appraisal. Lenders can often use your home's original purchase price as its value, which is a massive relief if property values in your area haven't shot up.

- Minimal Credit Check: While some lenders might do a quick credit review (a "credit-qualifying" streamline), many offer a "non-credit qualifying" option that doesn't require a deep dive into your credit report.

- Less Paperwork: You can stop searching for last year's tax returns. Since the main goal isn't to re-verify your income from scratch, the documentation needed is significantly lighter.

This simplified process is exactly why FHA Streamlines became a go-to option when interest rates hit historic lows. In fact, during the 2020-2021 rate dip, these refinances surged by over 200% year-over-year. The FHA has long offered this path, but it comes with important timing rules, like waiting 210 days from your original closing and having at least six on-time payments under your belt. You can discover more insights about refinance requirements on Amerisave.com.

The "Net Tangible Benefit" Test

While the process is simplified, it isn't a free-for-all. The FHA has a key consumer protection rule built in, known as the Net Tangible Benefit (NTB) test. This rule is there to make sure the refinance actually helps you. It's not enough to just get a new loan—it has to be a measurably better one.

The Net Tangible Benefit test is a critical safeguard. It prevents homeowners from getting talked into a refinance that doesn't provide a real, concrete financial advantage. It’s the FHA’s way of asking, "Is this new loan truly helping you?"

To pass this test, your new loan must accomplish at least one of the following:

- Lower Your Monthly Payment: The most common goal. Your new combined principal, interest, and mortgage insurance payment must drop by at least 5%.

- Switch to a Fixed-Rate Mortgage: If you're currently in an Adjustable-Rate Mortgage (ARM), moving into a stable, predictable fixed-rate loan automatically qualifies as a tangible benefit.

This requirement ensures every single FHA Streamline has a clear, positive purpose behind it.

Critical Timing and Payment History Rules

That speed and simplicity come with a few firm rules about your timing and payment history. These guidelines are non-negotiable and confirm you've been a reliable borrower before you can access the program's benefits.

- The 210-Day Rule: You must wait at least 210 days from the day you closed on your current FHA loan before you can close on a Streamline refinance.

- Six On-Time Payments: You need to have made at least six full, on-time monthly payments on the mortgage you're looking to refinance.

- Recent Payment History: All your mortgage payments over the last six months must have been on time. Lenders will also check the last 12 months, where you're allowed no more than one payment that was 30 days late.

Lenders will verify your payment history directly with your current servicer to make sure you're eligible. Here at Mortgage Seven LLC, our team can help you review your loan's history to confirm you meet these crucial FHA refinance guidelines before you even start an application.

Accessing Equity With An FHA Cash Out Refinance

Your home is more than just a place to lay your head—it's a powerful financial tool. As you pay down your mortgage and property values rise, you build wealth in the form of home equity. An FHA Cash-Out Refinance is a popular way for homeowners to turn that on-paper wealth into real, usable cash.

The process is pretty straightforward: you take out a new, larger FHA loan that completely replaces your current mortgage. The new loan pays off your old one, and the difference between the two is yours to keep, tax-free. Think of it as hitting a financial reset, giving you access to your home's value without having to sell.

The 80 Percent LTV Rule Explained

When it comes to FHA cash-out guidelines, one number is king: 80%. This is the maximum Loan-to-Value (LTV) ratio the FHA allows, meaning your new loan amount cannot exceed 80% of your home's current appraised value. This rule is the single biggest factor determining how much cash you can actually pull out.

This isn't just an arbitrary number. By capping the LTV at 80%, the FHA ensures you maintain a solid 20% equity stake in your home. It’s a built-in safety net that protects both you and the lender, keeping the loan on secure footing.

This 80% limit is a relatively recent, but significant, change. Back in September 2019, the Department of Housing and Urban Development (HUD) lowered the maximum LTV from 85% down to the current 80%. This adjustment still shapes how much equity homeowners can access today and applies nationwide, provided you've owned and lived in the home for at least 12 months.

A Practical Cash Out Calculation

Let's put this into practice. Say your home just appraised for $400,000, and your remaining mortgage balance is $250,000.

Find Your Max Loan Amount: First, you'll calculate 80% of your home's appraised value.

$400,000 (Appraised Value) x 0.80 = $320,000 (Max FHA Loan)

Subtract Your Current Mortgage: Next, you subtract what you still owe on the house.

$320,000 (Max FHA Loan) - $250,000 (Current Mortgage) = $70,000

In this case, you could get a new loan for up to $320,000. After paying off the old $250,000 mortgage, you’d walk away with $70,000 in cash. That's a substantial sum you could use for anything from a major kitchen remodel to wiping out high-interest credit card debt. For a closer look at the numbers, explore our full guide on cash-out refinance requirements.

Stricter Property and Borrower Rules

Unlike an FHA Streamline, a Cash-Out refinance is treated as a brand-new loan. That means you're going through a full underwriting process, and the requirements are much more thorough.

An FHA Cash-Out refinance is not a shortcut. It requires a full appraisal to establish your home's current market value and a thorough review of your credit, income, and debt to ensure you can comfortably handle the new, larger loan payment.

You'll need to check a few key boxes to meet FHA refinance guidelines:

- Ownership and Occupancy: You must have owned the property for a minimum of 12 months and used it as your primary home for that entire time.

- Payment History: A clean mortgage payment history for the last 12 months is non-negotiable. No late payments.

- Credit Score: While the FHA is known for being flexible, most lenders will want to see a credit score of 620 or higher for a cash-out loan.

- Income and Debt-to-Income (DTI): Be prepared to provide full income documentation, like pay stubs and tax returns. Lenders will closely examine your DTI ratio to make sure the new payment fits comfortably within your budget.

These rules are tighter for a good reason—a cash-out loan increases your total debt, which adds a layer of risk for the lender. If this sounds like the right path for you, the team at Mortgage Seven LLC can run the numbers, see if you qualify, and show you exactly how much equity you could tap into.

Meeting the Core FHA Eligibility Rules

No matter which FHA refinance path you take—Streamline, Cash-Out, or anything in between—it all starts with the same fundamental eligibility requirements. Think of these as the ground rules for playing in the FHA's ballpark. Getting these right is your first big step, putting you on solid footing before you worry about the specifics of each program.

These core rules look at three key parts of your financial picture: your credit history, how your income stacks up against your debts, and the physical condition of your home. The FHA needs this 360-degree view to make sure a new loan is a good fit for you. Let's dig into what they're looking for.

Unpacking FHA Credit Score Guidelines

One of the biggest draws of an FHA loan has always been its flexible stance on credit scores. It’s what makes these loans so accessible. But there's a common misunderstanding between the FHA's official minimum and what lenders actually require.

The FHA handbook says you can get a loan with a credit score as low as 500. On paper, that opens the door for a lot of people. In the real world, though, finding a lender willing to approve a refinance with a 500 score is next to impossible. Most lenders have what are called "overlays"—their own internal rules that are stricter than the FHA's baseline.

A lender overlay is like a velvet rope at a club. The club's official policy might be "everyone's welcome," but the bouncer at the door has their own standards for who actually gets inside. For FHA loans, that usually means a higher credit score.

For most FHA refinances, you'll discover that lenders are looking for a minimum credit score somewhere in the 580 to 640 range. A stronger score not only boosts your approval odds but can also unlock a better interest rate. Even with overlays, FHA guidelines are still much more forgiving than conventional loans, which usually demand a score of at least 620. This difference is a game-changer for homeowners who might not qualify otherwise. You can learn more about how FHA loan flexibility helps more borrowers on NeighborsBank.com.

Calculating Your Debt to Income Ratio

Your Debt-to-Income (DTI) ratio is easily one of the most critical numbers in your refinance application. It’s a straightforward calculation that compares your total monthly debt payments against your gross (pre-tax) monthly income, giving lenders a quick snapshot of your financial health.

Lenders actually look at two different DTI figures:

- Front-End DTI: This just covers your housing expenses—the new mortgage payment, property taxes, homeowners insurance, and FHA mortgage insurance premiums.

- Back-End DTI: This includes all of that plus all your other recurring monthly debts, like car payments, student loans, and the minimum payments on your credit cards.

As a general rule, the FHA prefers a front-end DTI of 31% or less and a back-end DTI of 43% or less. But these aren't iron-clad limits. If you have what are called "compensating factors"—things like a high credit score, substantial cash reserves, or a long, stable job history—lenders often have the flexibility to approve loans with a DTI as high as 50%.

Meeting FHA Property Standards

Finally, the home itself has to pass muster. If your refinance requires a new appraisal (which Cash-Out and Simple Rate-and-Term loans do), an FHA-approved appraiser will inspect the property to ensure it meets minimum health and safety standards.

They aren't there to nitpick cosmetic flaws like scuffed paint or an outdated kitchen. The appraiser's job is to flag major issues that could impact the home's safety, security, or structural integrity.

Here are some common red flags that must be fixed before an FHA refinance can close:

- A damaged or actively leaking roof

- Unsafe electrical systems or exposed wiring

- No functioning, permanent heat source

- Evidence of termites or other wood-destroying insects

- Significant foundation damage or structural problems

Nailing these core FHA guidelines is your first major checkpoint on the road to a successful refinance. If you feel good about your credit, DTI, and your home's condition, you're off to a great start. The team at Mortgage Seven LLC can give you a free, no-obligation assessment to see exactly where you stand and help you map out the next steps.

Navigating the Refinance Process Step by Step

The journey from thinking about refinancing to actually signing the final papers can feel a little intimidating. But don't worry, it's a well-traveled road with very clear signposts along the way. When you understand what happens at each stage, the whole thing feels much less like a huge project and more like a series of simple, manageable tasks.

It’s a lot like putting together a piece of furniture. You wouldn't just start grabbing random screws and hope for the best, right? You follow the instructions, step-by-step. An FHA refinance is the same kind of deal—each stage builds on the one before it, leading to a smooth finish.

Let's walk through that roadmap together.

Stage 1: The Initial Consultation and Document Gathering

This is where we map everything out. It all starts with a simple conversation with a loan officer to pinpoint exactly what you want to achieve. Are you trying to lock in a lower monthly payment? Do you need to pull some cash out for a home project? Or maybe you just want to change your loan term? This initial chat helps us figure out which FHA refinance program is the right fit and gives us a quick gut check on your eligibility.

Once we have a game plan, it’s time to gather your financial paperwork. Think of this as laying the foundation for your loan application; a little organization here goes a long way.

Here’s what you’ll typically need to round up:

- Proof of Income: Usually your most recent pay stubs covering the last 30 days, plus your W-2s from the past two years.

- Tax Returns: You'll want to have your complete federal tax returns from the last two years handy, which is especially important if you're self-employed.

- Asset Statements: The latest statements for all your bank accounts (checking and savings) and any investment accounts.

- Current Mortgage Statement: This gives the lender all the nitty-gritty details on your existing home loan.

Stage 2: Application, Underwriting, and Appraisal

With all your documents ready, you'll fill out the official loan application. After you submit it, your file heads over to the underwriting department. An underwriter is basically a financial detective. Their job is to double-check that every piece of information is accurate and that you meet all the specific FHA guidelines for the loan you’re applying for.

This is the most detailed part of the process. The underwriter will be taking a close look at your credit report, making sure your income is stable, and calculating your debt-to-income ratio before giving the final thumbs-up.

The underwriting stage is where your financial story gets a thorough review. Patience is the name of the game here. It's not uncommon for an underwriter to ask for a bit more information or an extra document to make sure every "i" is dotted and "t" is crossed according to FHA standards.

If you’re doing a Cash-Out or a Simple Rate-and-Term refinance, this is also when the home appraisal gets scheduled. An FHA-approved appraiser will come out to assess your property's current market value and overall condition. For a deeper dive, you can learn more about what to expect during an appraisal for a refinance in our detailed guide. A solid appraisal is a major milestone on the path to approval.

Stage 3: The Final Approval and Closing

Once the underwriter gives their blessing and the appraisal comes back clean, you'll get the three magic words you've been waiting for: "clear to close." That’s the green light! It means all the conditions have been met and your loan is ready to be finalized.

From there, your loan officer coordinates with a title company or an attorney to schedule your closing appointment. At closing, you'll sit down and sign the final loan documents, including the all-important Closing Disclosure, which breaks down every single cost associated with your loan.

After you sign, there's usually a three-day "right of rescission" period, which is a window where you can still change your mind and cancel the whole thing. Once that time passes, your new loan is officially funded, your old mortgage gets paid off, and you can celebrate—your FHA refinance is complete

Frequently Asked Questions About FHA Refinancing

Even with all the details laid out, you probably still have a few specific questions. That’s completely normal. Getting straight answers is the only way to feel confident about moving forward. Let's tackle some of the most common things people ask about FHA refinancing.

Can I Get an FHA Refinance If My Current Loan Isn't an FHA Loan?

Yes, you absolutely can. This is a huge point of confusion for many homeowners, but the answer is simple. The only program reserved exclusively for current FHA borrowers is the FHA Streamline Refinance.

If you have a conventional loan, a VA loan, or even a USDA loan, the door is still wide open. You can use the FHA Simple Rate-and-Term or the FHA Cash-Out refinance options. This flexibility is one of the FHA's best features, allowing homeowners from all sorts of loan backgrounds to tap into its more forgiving credit and qualification standards.

How Does FHA Mortgage Insurance Work with a Refinance?

Mortgage Insurance Premium (MIP) is part of the deal with any FHA loan, and refinancing is no different. When you refi into a new FHA loan, you’ll see MIP in two forms.

First, there's the Upfront MIP (UFMIP). This is a one-time premium that most people just roll right into their new loan balance so they don't have to pay it out of pocket. Then, you have the Annual MIP, which is the more familiar monthly charge that gets added to your mortgage payment.

It's crucial to run the numbers on both the upfront and annual MIP. A refinance only makes sense if the savings you get are real and meaningful, even after accounting for these insurance costs.

There's a small silver lining for some: if you're doing an FHA Streamline on a loan that originated before June 1, 2009, you might get a grandfathered-in, lower MIP rate. Digging into these costs is key to making a smart financial move.

What Are the "Seasoning" Requirements for FHA Refinancing?

"Seasoning" is just the industry term for the mandatory waiting period before you can refinance your mortgage. The FHA puts these rules in place to promote stability, and they vary based on which refinance program you’re using.

These timelines are firm and are a fundamental part of the FHA guidelines.

- For an FHA Streamline Refinance: You need to wait at least 210 days from your original FHA loan's closing date. You also must have made at least six monthly payments on time.

- For an FHA Cash-Out Refinance: The rules are much stricter here. You must have owned and lived in the home as your main residence for at least 12 months before you can even submit an application.

Do FHA Loan Limits Apply to a Refinance?

They sure do. The final amount of your new, refinanced loan has to stay within the FHA loan limits for the county where your property is located. The FHA updates these limits every year to keep up with local home prices, which is why a limit in a rural area might be drastically different from one in a major city.

Your total new loan amount—including any cash you pull out or closing costs you roll in—cannot go over that county limit. A quick chat with an experienced lender is the fastest way to find out the exact FHA loan limit for your specific area.

Wading through FHA refinance guidelines can feel overwhelming, but you don't have to figure it all out on your own. The experts at Mortgage Seven LLC are here to give you clear, personalized advice. We’ll help you make sense of your options and find the right path for your financial goals. Schedule your free consultation today at https://mtg7.com.

Leave a Reply