When a loved one offers you money for a down payment, it can feel like a dream come true. But for a mortgage lender, a large, unexplained deposit in your bank account is a major red flag. This is where a gift letter for mortgage comes in—it’s a straightforward document that clarifies those funds are a true gift, not an under-the-table loan.

Think of it as a formal note from your donor to the lender, making it crystal clear that you don’t have to pay the money back. This is non-negotiable for lenders, as it proves your down payment source won't saddle you with extra debt.

What Is a Mortgage Gift Letter and Why Lenders Require It

When you're buying a home, lenders need to know where every single dollar for the purchase is coming from. That big check from your parents? Without documentation, the lender has no way of knowing if it’s a gift or a loan you'll be struggling to repay alongside your mortgage.

The gift letter solves this problem. It’s a signed statement from the person giving you the money (the donor) that confirms two crucial things:

- The funds are a legitimate gift, and there's absolutely no expectation of repayment.

- The donor holds no financial stake or ownership interest in the home you're buying.

This simple piece of paper directly protects one of the most critical calculations in your loan application: your debt-to-income (DTI) ratio. By officially classifying the money as a gift, it isn't counted as a new debt. This gives the underwriter confidence that you aren't taking on a "secret" loan that could jeopardize your ability to afford your mortgage payments down the road.

To help you get a clearer picture, this table breaks down the essentials of a mortgage gift letter.

Quick Overview of a Mortgage Gift Letter

| Component | Purpose and Importance |

|---|---|

| Clear Statement of Gift | Explicitly states the funds are a gift with no repayment required, satisfying lender requirements. |

| Donor Information | Identifies the donor and their relationship to the borrower, establishing a legitimate connection. |

| Gift Amount and Date | Specifies the exact dollar amount and when the funds were transferred for clear tracking. |

| No Financial Interest Clause | Confirms the donor has no claim to the property, a key underwriting requirement. |

This letter is the official proof that turns a potential underwriting headache into a verified asset.

The Underwriter's Perspective on Gifted Funds

Mortgage underwriters are financial detectives. Their job is to assess risk by scrutinizing every aspect of your financial life. From their point of view, an undocumented chunk of cash looks exactly like an undisclosed loan—a serious issue that misrepresents your true financial obligations. You can get a deeper look at what they examine in our guide to the mortgage underwriting process.

Without a proper gift letter, your application could be denied on the spot. In a worst-case scenario, it could even raise concerns about mortgage fraud. In 2024, an incredible 95.8% of all mortgages in the U.S. were for primary residences, showing just how vital tools like gift letters are for helping families get into homes.

A mortgage gift letter isn't just a formality; it's a key piece of evidence that protects both you and the lender. It provides the clean, transparent paper trail needed to verify your down payment funds and keep your loan approval on track.

Ultimately, getting the gift letter right is a big part of your overall Mortgage Auto Approval Readiness. It's how you ensure a generous gift from a loved one helps, rather than hinders, your path to closing.

Who Can Give a Down Payment Gift and How Much

When it comes to getting help with your down payment, lenders have a vested interest in where that money comes from. They aren't just going to accept a check from anyone. These rules are in place to ensure the money is a true gift—not a secret, undocumented loan that you'll have to pay back.

For most mortgage programs, the funds must come from a close relative. Think parents, siblings, grandparents, your spouse, or even your kids. Lenders see these relationships as genuine, which eases their concern that the money might have strings attached.

Who Is an Acceptable Donor

The exact definition of an "acceptable donor" can shift a bit depending on your loan type. While immediate family is almost always a safe bet, some loan programs open the door to a wider circle of relationships.

Conventional Loans, the kind backed by Fannie Mae and Freddie Mac, stick to a pretty specific list:

- Family Members: Anyone related to you by blood, marriage, adoption, or even legal guardianship.

- Fiancé or Domestic Partner: Your soon-to-be spouse or a long-term partner typically gets the green light.

- Godparents or Future Relatives: In some situations, a lender might even approve a gift from a godparent or a future in-law.

FHA Loans are a little more flexible and sometimes allow gifts from:

- Employers or Labor Unions: This is definitely less common, but it's permitted under FHA guidelines.

- Close Friends: The key here is proving a clear, documented interest in your well-being. It's a higher bar to clear.

- Charitable Organizations: Non-profits focused on homeownership assistance can also be an approved source.

The Bottom Line: The lender needs to be completely confident that the person giving you the money has a personal interest in helping you succeed, not a financial one in the property itself. Always check with your lender upfront to confirm their specific list of approved donors.

Understanding Gift Limits and Tax Rules

One of the first questions people ask is, "How much can someone give me?" From your mortgage lender's point of view, there really isn't a cap. If your family wants to gift you the entire down payment for a conventional loan, that’s usually fine as long as the paperwork is solid. If you're trying to figure out how much you'll need, our guide on calculating your down payment can help you pin down a target number.

The real consideration here isn't the lender—it's the IRS. While you, the recipient, typically don't have to worry about taxes on the gift, the person giving it needs to be aware of the federal annual gift tax exclusion.

For 2024, any individual can give another person up to $18,000 without needing to file a gift tax return.

Here’s how that plays out in the real world: a married couple (like your parents) could give another married couple (you and your spouse) a combined $72,000 in one year, completely tax-free. That’s $18,000 from each parent to each of you. If a gift exceeds that annual limit, the donor simply has to file a gift tax return. They probably won't owe any tax unless they've used up their massive lifetime gift tax exemption—a whopping $13.61 million per person in 2024.

As home prices have climbed, more and more buyers are leaning on this kind of help. In fact, reliance on family for down payment funds has skyrocketed, with 31% of first-time homebuyers receiving assistance in recent years. That’s a huge jump from just 20% in 2015. This trend isn't just local; it’s a global phenomenon, as recent reports on the rise of gifted down payments have shown. All of this just goes to show how critical a well-written, properly structured gift letter has become in today's housing market.

Getting Your Mortgage Gift Letter Right

A mortgage gift letter isn't just a nice little note—it's a critical legal document an underwriter will scrutinize. Think of it this way: any ambiguity or missing detail can throw a major wrench in your loan approval, causing delays you definitely don’t want. Nailing it on the first try is one of the easiest ways to keep your closing on track.

This letter is essentially a sworn statement. Its whole purpose is to tell the lender, loud and clear, "This money is a gift, not a loan." That distinction is huge because a loan would count against your debt-to-income ratio, while a gift doesn't. You're building an undeniable case for why this cash infusion is a genuine act of generosity.

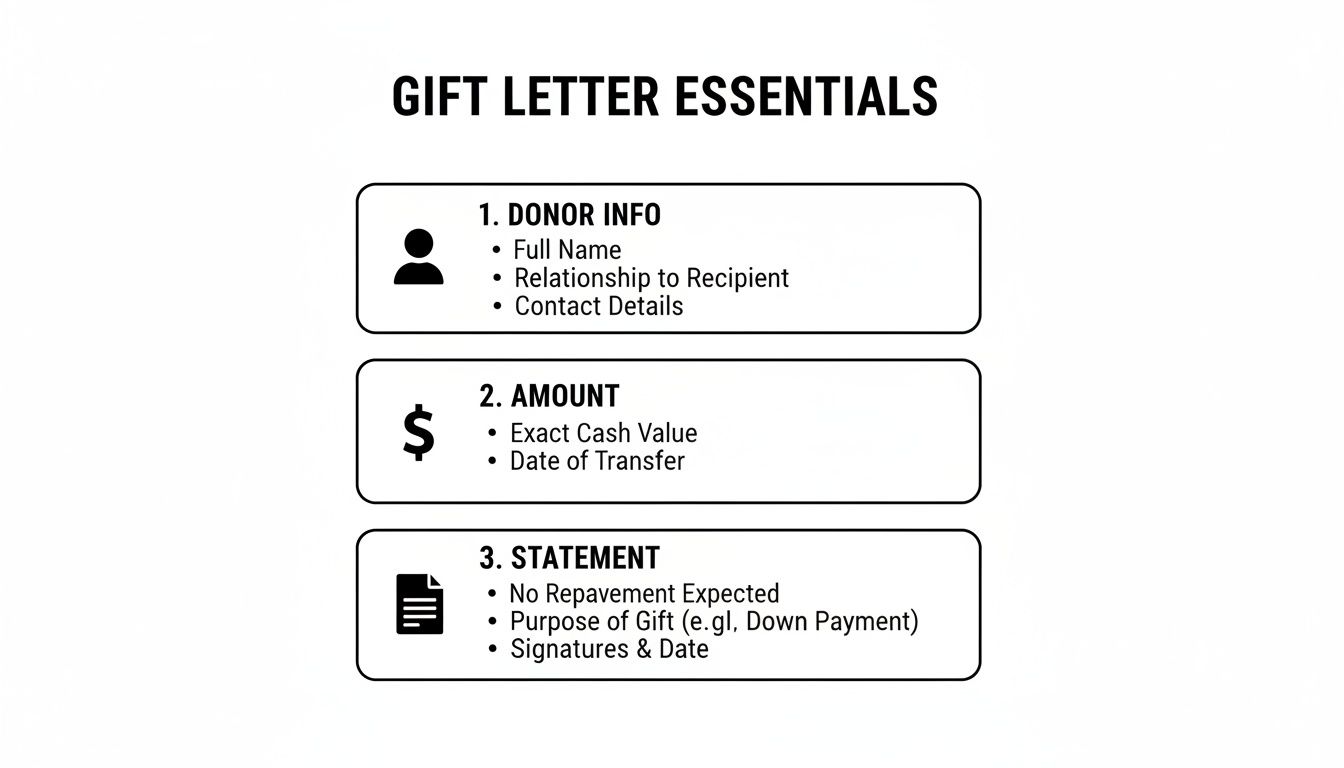

What Goes into an Airtight Gift Letter?

While every lender might have their own preferred template, the essential ingredients are always the same. Each piece of information is there for a reason—to leave no doubt in the underwriter's mind about where the money came from and what it's for.

Let's break down exactly what you'll need.

First, you need to clearly identify everyone involved. The letter must have the complete and accurate details for both the person giving the gift and the person receiving it.

- Donor’s Full Legal Name: This needs to be an exact match to what’s on their driver's license and bank statements.

- Donor’s Full Address: Their complete home address.

- Donor’s Phone Number: A real contact number is a must-have in case the lender needs to call and verify anything.

- Your Full Legal Name (the Borrower): Make sure this is identical to how your name appears on the loan application.

- The Property Address: List the address of the home you're buying.

This basic contact info creates a solid, verifiable link between you, the donor, and the property.

Be Crystal Clear About the Gift

When it comes to the money itself, vagueness is your worst enemy. The letter has to be incredibly specific about the financial gift to avoid any misinterpretation.

Don't just say something like, "a gift for their down payment." You need to be precise with the numbers and dates.

For example: "I, [Donor's Name], am gifting the amount of $20,000 to [Borrower's Name] on [Date of Transfer]."

This isn't optional. That level of detail lets the underwriter perfectly match the amount in the letter to the bank statements showing the money leaving the donor's account and landing in yours. It connects all the dots.

The Single Most Important Sentence

If you only remember one thing from this guide, make it this: the letter absolutely must declare that the money is a true gift. This single statement is the entire point of the document.

The letter needs an unmistakable sentence confirming that no repayment is expected.

Here's the magic phrase:

"This is a bona fide gift, and there is no expectation of repayment, either in cash or services, now or in the future."

Without that exact wording, an underwriter might have to treat the funds as a loan. That could completely wreck your debt-to-income ratio and potentially get your entire mortgage application denied. It's the legal heart of the letter.

Explain Where the Money Came From

Want to make your underwriter’s job easier and speed up your approval? Add a little extra context about the source of the gift funds. This simple step can answer their questions before they even have to ask.

It just adds another layer of transparency, showing the lender where the money originated. For instance, the donor can add a quick line like:

- "The source of these gift funds is my personal savings account at ABC Bank."

- "These funds are from the sale of stocks held in my brokerage account."

Adding this little detail helps the underwriter follow the paper trail when they review the donor's financial documents. It proves the money didn't just appear out of thin air, which is a major red flag for lenders. By putting all these key elements together, you’ll craft a perfect mortgage gift letter that sails through underwriting and keeps you on the fast track to closing day.

How Different Loan Programs Treat Gift Funds

When you’re lucky enough to get a financial gift to help buy a home, you can't just deposit the check and move on. The type of mortgage you're getting—whether it's Conventional, FHA, VA, or USDA—has its own specific set of rules about where that money can come from and how you can use it.

Getting a handle on these differences from the get-go is a game-changer. It helps you and your loan officer pinpoint the right mortgage for your situation and avoids those gut-wrenching, last-minute underwriting problems that can stall or even kill a deal. A gift letter for a mortgage that sails through for one loan might be a non-starter for another.

Conventional Loan Gift Rules

Conventional loans are the workhorses of the mortgage world. Since they aren't backed by the government, they follow guidelines set by giants like Fannie Mae and Freddie Mac. The good news is that if you’re putting down 20% or more, you can usually use gift money for the entire down payment without any issues.

Things get a little tighter if your down payment is less than 20%. In that scenario, some lenders will want to see you put some of your own skin in the game. They might require a certain percentage to come from your own "seasoned" funds—that’s money that has been sitting in your bank account for at least a couple of months.

So, who can give you the gift? For conventional loans, the circle is pretty tight:

- Immediate family (think spouse, parents, siblings, children)

- A fiancé, fiancée, or domestic partner

- Other relatives (by blood, marriage, adoption, or even legal guardianship)

No matter the loan type, every gift letter needs these core components. Think of them as the non-negotiables: who the donor is, how much they’re giving, and a crystal-clear statement that it's a gift, not a loan.

FHA Loan Gift Guidelines

If you need a bit more flexibility, FHA loans are fantastic. Backed by the Federal Housing Administration, they are practically designed to help people with less cash on hand get into a home.

One of their biggest perks is that 100% of your down payment can be a gift. You can even use gifted funds to cover your closing costs. This feature alone makes FHA a go-to option for many first-time buyers.

The list of who can give you money is also a bit wider than with conventional loans. For an FHA loan, a gift can come from:

- A family member

- Your employer or a labor union

- A close friend (but you’ll need to prove a genuine, long-standing relationship)

- A charitable organization or an approved government assistance program

The Bottom Line: FHA’s generous rules on gift funds can be the key that unlocks the door to homeownership. Just make sure the donor is on their approved list and that your paperwork, especially the gift letter, is absolutely perfect.

VA and USDA Loan Specifics

VA loans (for veterans and service members) and USDA loans (for rural areas) also welcome gift funds, but each has its own unique spin.

With VA Loans, the rules are pretty accommodating. Since most VA loans don't require a down payment, gift money is typically used for other out-of-pocket expenses like closing costs or the VA funding fee. The one major rule is that the gift can't come from anyone who stands to gain from the sale, like the seller, builder, or your real estate agent.

USDA Loans are similar in that they also offer 100% financing, meaning no down payment is needed. Here, too, gifted money can be a huge help for covering closing costs. As with other loans, the funds have to come from an acceptable source (usually family) and be documented meticulously with a gift letter and a clear paper trail.

Gift Fund Rules Comparison by Loan Type

The specifics can feel like a lot to track, so I've put together this table to give you a quick side-by-side look at how the major loan programs handle gift funds. It really highlights the key differences you’ll want to discuss with your lender.

| Loan Program | Minimum Borrower Contribution | Acceptable Donors | Key Considerations |

|---|---|---|---|

| Conventional | May be required if down payment is < 20% | Family members, fiancé/fiancée, domestic partner | Stricter donor list; lender overlays can add requirements. |

| FHA | 0% | Family, close friends, employers, charities, government agencies | Allows 100% of down payment and closing costs to be gifted. |

| VA | 0% | Anyone not an interested party to the transaction (e.g., seller, agent) | No down payment required, so gifts typically cover closing costs. |

| USDA | 0% | Typically family members, but can be flexible | No down payment needed; gift must be from a non-interested party. |

As you can see, government-backed loans like FHA, VA, and USDA are generally more lenient, often allowing your entire cash-to-close to come from a gift. Conventional loans are a bit more traditional, sometimes requiring you to contribute some of your own savings. Knowing this ahead of time helps you set clear expectations with your generous donor and your loan officer.

Creating the Paper Trail Lenders Need to See

Think of the signed gift letter for mortgage as your opening argument. The paper trail is the evidence that proves your case. Lenders need to follow the money from the donor’s account directly into yours—no gaps, no questions. This isn't because they don't trust you; it's a non-negotiable part of complying with federal anti-money laundering laws and verifying every dollar used to buy a home.

An underwriter’s entire job is to connect the dots. A single missing piece in this financial puzzle can bring your loan application to a screeching halt, leaving you scrambling for old bank statements under a tight deadline. By building a rock-solid paper trail from day one, you’ll answer the lender’s questions before they even have a chance to ask.

What the Donor Needs to Provide

First things first: the lender needs proof that the person giving you the money actually had it and that it came from a legitimate source. This all comes down to their bank statements.

Your donor needs to supply a copy of the bank statement from the month the funds were sent. This statement must clearly show:

- The donor's full name and account number.

- Enough money in the account before the gift was transferred out.

- The exact withdrawal that matches the gift amount, down to the penny.

This step is critical. It shows the money didn't just magically appear in their account right before they sent it to you—a huge red flag for underwriters looking for undisclosed loans.

Tracking the Money in Transit

How the money gets from them to you is just as important as where it came from. You need a transfer method that’s clean, official, and easy to trace.

Your best options are:

- Wire Transfer: This is the gold standard. It creates an immediate, undeniable electronic record showing the funds moving from one specific bank account to another.

- Cashier's or Certified Check: These are also great choices. Since the bank issues the check and guarantees the funds, it provides a solid paper trail.

Crucial Tip: Never, ever use cash. A large, unexplainable cash deposit into your account is nearly impossible to source. It’s the fastest way to get your file flagged and potentially rejected by an underwriter. Just don't do it.

What You Need to Provide

Once the gift funds land in your account, you have to document their arrival. This is the final step that closes the loop, showing the underwriter the money is officially yours and ready for the down payment.

You'll need to provide your bank statement showing the incoming deposit. Make sure it includes your name, account number, and the transaction details matching the gift amount. If a check was used, include a copy of the cleared check (both front and back).

Getting all this paperwork together can feel overwhelming, but a good checklist of all the documents needed for mortgage pre-approval can really help streamline things.

Lenders today often rely on sophisticated mortgage banking document automation to manage the sheer volume of paperwork. By meticulously documenting every step—from the donor’s withdrawal to your deposit—you’re essentially handing them a clean, easy-to-approve file that will keep your home purchase on track.

Common Gift Letter Mistakes That Can Derail Your Loan

Even with the best of intentions, a simple mistake on a gift letter for mortgage—or in how the money is transferred—can create a massive headache for underwriting. The problem usually comes down to not seeing things from the lender's point of view. Their one and only job here is to verify, without a shadow of a doubt, where every penny of your down payment came from.

Steering clear of these common pitfalls is one of the simplest things you can do to keep your loan approval on the fast track. A tiny oversight can lead to frustrating delays, a barrage of questions from underwriters, and a ton of last-minute stress for you and your generous family member.

The Problem with Vague Language

By far, the single most damaging mistake is submitting a gift letter that’s vague or missing crucial details. An underwriter isn't going to guess or fill in the blanks. If the letter doesn't explicitly state that the money is a gift and not a loan, they have to assume it's debt. That can throw your entire application into chaos.

We once saw a client’s loan get held up for two weeks because their letter was missing one simple phrase: "no repayment is expected." It seems small, but that omission forced the underwriter to slam the brakes on the entire process until they received a corrected letter. It almost cost them their closing date.

Your gift letter has to be crystal clear. Leave zero room for interpretation. It must explicitly state the donor’s information, the exact dollar amount, and the ironclad promise that it is not a loan in disguise.

Mishandling the Money Transfer

How the gift money gets from the donor to you is just as important as the letter itself. Lenders need to see a clean, easy-to-follow paper trail that they can verify with bank statements.

Here are the blunders we see most often when it comes to the transfer:

- Depositing Cash: Never, ever deposit a large sum of cash. For an underwriter, a big cash deposit is a giant red flag. There’s no paper trail, which makes the source impossible to prove.

- The Donor Paying Someone Else: The person gifting you the money should never pay the seller, the title company, or anyone else directly. The money must travel from the donor’s bank account directly into your bank account. This creates the clean chain of custody the lender needs to see.

- "Unseasoned" Funds: Lenders look very closely at any large, recent deposits. If the donor’s bank account shows a sudden, unexplained influx of cash right before they give it to you, it raises questions about where that money came from in the first place.

Misunderstanding Why Lenders Are So Picky

It might feel like your lender is just being difficult, but they are legally required to prevent fraud and money laundering. Historically, down payment funds have been a hotbed for shady activity. Think back to the housing boom of 2003-2004—Suspicious Activity Reports related to mortgage fraud skyrocketed by over 92%.

That history is exactly why lenders are so meticulous today, especially now that about 23% of all down payments involve a gift from family. You can dig into these trends in mortgage loan fraud yourself to get a better sense of why these rules are in place. They’re not just trying to make your life harder; they're protecting everyone involved.

Answering Your Lingering Gift Letter Questions

Even after you've dotted all the i's and crossed all the t's on your gift letter, a few questions might still be nagging at you. It happens all the time. Let's walk through some of the most common scenarios that pop up, so you can move forward with confidence.

Can We Use the Gift Money for Closing Costs, Too?

Yes, absolutely. Lenders are generally pretty flexible here. The gifted funds aren't just for the down payment; you can typically apply them toward your closing costs and prepaid items like your first year of homeowners insurance or property tax reserves.

This is a huge help, especially with programs like FHA and VA loans, which have generous rules about gift funds. The key is simply to make sure the total gift amount is spelled out in the letter and that the money has been in your account long enough to be considered "seasoned" by the lender.

What if the Gift Is Coming From Overseas?

Getting a gift from a family member living abroad is definitely doable, but you'll need to be extra buttoned-up with your paperwork. This situation adds a few extra hoops to jump through because lenders need to follow international banking rules and meticulously track the money's origin.

Be prepared to show:

- A clear paper trail of the funds leaving the donor's foreign bank account.

- Documentation of the currency exchange rate when the transfer happened.

- If the original gift letter was in another language, you'll need a certified translation.

The more detailed your documentation, the smoother this process will be. Lenders just need to be 100% sure where the money came from.

Can My Mom or Dad Give a Gift for My Sibling’s House, Too?

Of course. There are no rules stopping a generous donor from giving gifts for more than one home purchase. As long as they have the funds and are willing to help, they can provide a gift to you, your sibling, or anyone else they choose.

Each mortgage is its own separate transaction. The lender for your sibling's loan will require a completely new gift letter and a fresh paper trail, just like yours did.

Sorting out the details of a down payment gift can feel like a lot, but you don't have to figure it all out on your own. The experts at Mortgage Seven LLC are here to make sure your financing is smooth and stress-free. Schedule a consultation with our team today!

Leave a Reply