Yes, you can absolutely get a HELOC on an investment property, but you need to know it's a completely different ballgame than tapping into the equity on your primary home. Lenders do offer them, but they're a lot more careful and the requirements are tougher.

I'll walk you through exactly what you need to know to successfully unlock the equity tied up in your rental property.

Unlocking Equity In Your Rental Property

For a savvy real estate investor, equity isn't just a number on a spreadsheet—it's dormant capital, just sitting there waiting for a job. A Home Equity Line of Credit (HELOC) is the tool that puts that capital to work. Think of it like a credit card secured by your property: you can draw funds when you need them, pay it back, and draw again. It’s perfect for the fast-moving world of real estate investing.

This kind of flexibility means you can jump on opportunities without having to sell off other assets. For example, imagine the house next door to one of your rentals suddenly hits the market at a great price. A HELOC gives you the power to make a strong, quick offer, potentially securing the deal before another buyer can even get their traditional financing in order.

Why It's A Different Process For Investors

When a lender looks at a HELOC application for an investment property, they see it through a business-risk lens. It’s not your home, it's an income-producing asset. From their perspective—and the data backs this up—borrowers in a financial pinch are far more likely to default on a rental property loan than on the mortgage for the roof over their own head.

Because of this increased risk, lenders raise the bar for qualification. Expect to face tougher credit score requirements, a lower loan-to-value (LTV) limit, and almost certainly higher interest rates.

This is a critical distinction to grasp right from the start. While you might be able to borrow up to 85% of the equity in your personal home, an investment property HELOC is often capped much lower, typically around 70-75%. Lenders need that extra equity cushion as a safety net. Understanding how to finance investment property means getting your head around these fundamental differences before you even apply.

Investment Property HELOC vs Primary Residence HELOC at a Glance

To set clear expectations, it’s helpful to see the differences side-by-side. The requirements for a rental property HELOC are designed to make sure the property's cash flow—and your own personal finances—can comfortably handle the new debt.

Here’s a quick comparison of what to expect.

| Requirement | Investment Property HELOC | Primary Residence HELOC |

|---|---|---|

| Max Loan-to-Value (LTV) | Typically 70-75% | Often up to 85% or higher |

| Credit Score | Usually 700+ is the starting point | More lenient (can start around 660+) |

| Interest Rates | Generally higher | Typically lower |

| Documentation | Needs rental agreements, P&L statements | Standard income verification (W-2s, pay stubs) |

| Cash Reserves | Often requires 6-12 months of reserves | Less common requirement |

As you can see, lenders are looking for a much stronger financial profile from an investor. They want to see a history of successful property management and the cash on hand to weather any potential vacancies or unexpected repairs.

Why Lenders See Investment Properties Through a Different Lens

To get a HELOC on an investment property, you have to start thinking like a lender. In their world, your family home and your rental property are two completely different animals, each with a unique risk profile. This simple distinction is why investors face a much higher bar for approval.

Let's put it this way: a lender is looking at two loan applications. One is for your primary residence, and the other is for a duplex you own across town. If you suddenly lost your job, which mortgage payment are you going to make first? It's human nature. People will fight tooth and nail to keep the roof over their own heads, which makes an investment property loan statistically more likely to default.

This isn't a knock on your reliability; it's a cold, hard risk calculation based on decades of data. Lenders see your rental as a business venture, subject to all the ups and downs of the market—tenant vacancies, unexpected repairs, and rent fluctuations. This heightened sense of risk dictates every single requirement, from the credit score they ask for to the amount of equity they'll let you tap into.

The Metrics That Matter to Lenders

Lenders don't just go with their gut; they use specific financial tools to measure risk. When underwriting a HELOC on an investment property, they zero in on a few key numbers that tell them how stable the loan is likely to be. If you want to build a bulletproof application, you need to understand these metrics.

Two of the big ones are the Combined Loan-to-Value (CLTV) and the Debt Service Coverage Ratio (DSCR).

- Combined Loan-to-Value (CLTV): This is just a fancy way of comparing your total debt on the property (your first mortgage plus the new HELOC) to its current market value. For an investment property, lenders want you to have a much bigger equity cushion.

- Debt Service Coverage Ratio (DSCR): This ratio is all about cash flow. It compares the property’s income to its expenses, including the mortgage. A DSCR above 1.0 means the property is breaking even. Lenders, however, want to see a safety net, so they typically look for a DSCR of 1.25 or higher.

Notice the focus here is on the property's ability to pay its own bills. Your personal income is still part of the equation, but for an investment property HELOC, the asset itself has to pull its own weight.

Higher Hurdles and Less Leverage

So, what does all this mean for you? It means tougher rules and less wiggle room. Lenders are essentially insuring themselves against the business risks of your rental portfolio, and their policies reflect that.

At its core, a lender's job is to manage risk. For an investment property, they'll demand more "skin in the game" from you—more equity, a stronger credit history, and deeper cash reserves—to balance out their own exposure.

The most noticeable difference is in the amount of leverage you can get. The latest data shows that while investment property HELOCs are available, lenders are playing it safe. They typically cap the CLTV for investment properties somewhere between 50% and 60%. That’s a massive drop from the 80% or more you can often get on a primary home. To see how these trends are shifting, you can find more home equity insights from the Mortgage Bankers Association.

This lower CLTV isn't just a suggestion; it's a core part of a bank’s risk-management playbook. On top of that, you should be ready to meet several other strict requirements:

- Minimum Credit Score: Don't be surprised if they require a FICO score of 700 or higher.

- Cash Reserves: Lenders will want to see that you have enough liquid cash to cover 6 to 12 months of PITI (principal, interest, taxes, and insurance) for the rental property.

- Heavy Documentation: Get your paperwork in order. You'll need current lease agreements, rent rolls, and a profit and loss statement for the property.

Weighing the Pros and Cons for Your Portfolio

Tapping into your property's equity with a HELOC on an investment property is a major financial decision. It’s not something to jump into lightly. While it can be an incredibly effective tool for growing a real estate portfolio, it's definitely not the right move for every investor or every situation.

Think of it like a financial multi-tool. It’s versatile and powerful, but you have to know what you’re doing. In the right hands, it can help you build something amazing. In the wrong hands, you can do some serious damage. Let’s break down exactly what you’re getting into by looking at the good and the bad.

The Upside: Flexible Capital and Growth Opportunities

The single biggest draw of a HELOC is its flexibility. Unlike a traditional loan that gives you a pile of cash all at once, a HELOC is a revolving line of credit. You get approved for a certain amount, and it just sits there, ready for you to use when you need it.

This on-demand access to cash is a massive advantage in the fast-paced world of real estate. When a great deal pops up—say, an underpriced property that just hit the market—you can make a strong offer immediately without having to scramble for financing.

Here’s where it really shines for investors:

- Financial Agility: Need cash for a down payment on a new rental? Pull it from the HELOC. Facing an unexpected five-figure roof repair? The funds are there. You only pay interest on what you actually borrow.

- Asset Preservation: You can access the equity you've built without having to sell a solid, cash-flowing property. This means you keep your rental income stream and your long-term asset.

- Potential Tax Benefits: The interest you pay might be tax-deductible if you use the funds to buy or make significant improvements to an investment property. Of course, you’ll want to run this by your tax advisor to see how it applies to you.

For an investor focused on scaling, a HELOC is like having a strategic war chest. It turns the dormant equity in your current properties into active capital you can deploy to seize opportunities and expand your portfolio.

The Downside: Volatility and Financial Risks

Now for the flip side. That flexibility comes with some real risks you need to manage carefully. The biggest one is the variable interest rate. Most HELOCs are tied to a benchmark rate, which means your payments can fluctuate.

If rates climb, your monthly payment will climb right along with them. This is often called "payment shock," and it can seriously mess with your property's cash flow. A profitable rental can quickly turn into a money pit if your costs skyrocket but your rent stays flat.

Investors absolutely must keep these drawbacks in mind:

- Over-Leveraging Danger: A HELOC piles more debt onto your property. If the market dips and your property value falls, you could find yourself underwater, owing more than the asset is worth.

- Frozen Credit Lines: This is a big one. In a shaky economy, lenders can (and do) reduce credit limits or freeze HELOCs altogether. The cash you were counting on could vanish overnight, right when you need it most.

- Your Property is the Collateral: Never forget this. A HELOC is a secured loan. If you can't make the payments, the lender can foreclose on your investment property, just like with a primary mortgage.

Pros and Cons of Using a HELOC on Your Investment Property

A balanced look at the key benefits and potential drawbacks for real estate investors considering this financing option.

| Advantages | Disadvantages |

|---|---|

| Flexible Access to Funds: Draw cash as needed, pay interest only on the amount used. | Variable Interest Rates: Payments can increase unexpectedly, squeezing cash flow. |

| Competitive Edge: Make faster, stronger offers on new properties without new loan applications. | Risk of Over-Leveraging: Easy to pile on too much debt, leaving you vulnerable in a downturn. |

| Keeps Assets Intact: Unlock equity without selling a valuable, income-producing property. | Credit Line Can Be Frozen: Lenders can reduce or freeze your credit line during economic uncertainty. |

| Potential Tax Deductions: Interest may be deductible when used for investment purposes. | Foreclosure Risk: Your investment property is the collateral and can be lost if you default. |

Ultimately, a HELOC is a powerful but demanding financial product. Success depends on having a clear strategy, a solid understanding of your numbers, and a healthy respect for the risks involved.

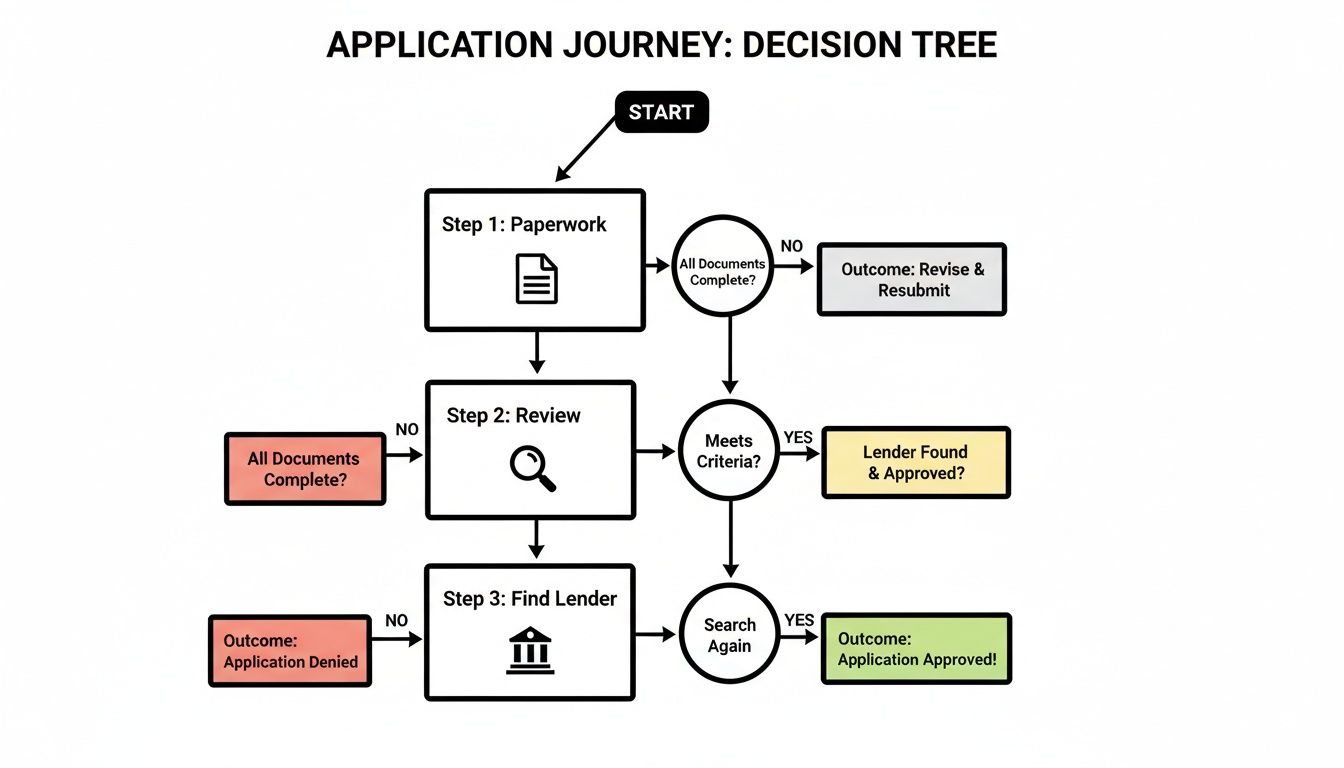

Your Step-by-Step Application Checklist

Getting a HELOC on an investment property isn't like applying for your typical home loan. It’s a different beast altogether. Lenders will be looking at your application with a much sharper, business-focused eye, weighing the property's performance just as heavily as your personal finances.

Think of it like pitching a business plan. You need to present a solid case backed by hard data. This five-step checklist will walk you through the entire journey, from gathering your initial paperwork to finally accessing your funds, helping you build an application that gets a "yes."

Step 1: Assemble Your Documentation

Before you even think about calling a lender, get your paperwork in order. This is non-negotiable. Lenders need a crystal-clear financial snapshot of you and the property, and showing up prepared signals that you’re a serious, organized investor.

It helps to split your documents into two piles: personal and property.

- Your Personal File: This is all about you. Dig out your last two years of tax returns (personal and business), your most recent pay stubs or other proof of income, and statements from all your bank, retirement, and brokerage accounts. Lenders want to see your cash reserves.

- The Property's File: This is the property’s resume. You’ll need the deed (proof of ownership), your latest mortgage statement, the property insurance declarations page, and recent property tax bills. Critically, you must have copies of all current lease agreements to prove your rental income stream.

Having a clean, complete file makes an underwriter’s job a hundred times easier, and trust me, you want them on your side.

Step 2: Perform a Financial Health Check

With your documents in hand, it’s time to play lender and look at your own finances with a critical eye. This is your chance to spot and fix any potential red flags before they can derail your application. It’s a self-audit, plain and simple.

First, pull your credit reports from all three bureaus. For an investment property HELOC, lenders are almost always looking for a credit score of 700 or higher. If you find any errors or nagging issues, deal with them now.

At its core, a lender's decision is a risk calculation. Your mission is to present yourself as a low-risk borrower by showcasing strong credit, reliable cash flow, and a solid equity position.

Next, run the numbers on your property. Calculate its current loan-to-value (LTV) ratio by dividing your mortgage balance by the property's estimated market value. If you're not familiar with this key metric, it’s worth taking a moment to understand what a loan-to-value ratio is and how it affects your borrowing power. Finally, put together a simple profit and loss (P&L) statement for the property that clearly lays out its income and expenses.

Step 3: Find the Right Lender

Here’s a piece of advice many investors learn the hard way: not all lenders are created equal. This is especially true when it comes to financing for investment properties. Many of the big national banks have rigid, one-size-fits-all rules and may not offer investment HELOCs at all.

You need to look for a financial partner who actually gets real estate investing. Cast a wider net and explore these options:

- Community Banks and Credit Unions: These smaller, local institutions are often your best bet. They tend to have more flexibility in their underwriting and are more likely to build relationships with local investors.

- Mortgage Brokers: A good broker is worth their weight in gold. They have relationships with dozens of lenders, including niche players who specialize in investor products, and can shop your application to find the best fit.

- Specialty Lenders: Some lenders live and breathe investor finance. They focus exclusively on products like DSCR loans and other creative solutions, so they know exactly how to evaluate rental income and property performance.

Step 4: Navigate the Underwriting Process

Once your application is submitted, it heads to underwriting. This is where a team of specialists puts everything under a microscope to verify your information and make the final call. The process usually involves a full property appraisal to confirm its value, deep income verification, and a title search to make sure there are no surprise liens or claims.

Stay on your toes during this phase. Be ready to answer questions and provide extra documents at a moment's notice. An underwriter might ask for clarification on a large deposit in your bank account or want a more detailed breakdown of your property’s maintenance costs. Responding quickly and thoroughly is the key to keeping things moving.

Step 5: Close and Access Your Funds

You've made it to the finish line: closing. You’ll sign the final loan documents, and the HELOC will be officially recorded against your property's title. After a brief waiting period (known as a rescission period, if one applies), the line of credit is yours to use.

Typically, you’ll get a dedicated checkbook or a debit card linked to the HELOC, giving you the flexibility to draw funds as you need them for that next renovation project or down payment.

What If a HELOC Isn't the Right Fit? Exploring Your Other Options

A HELOC is a fantastic tool, but it's just one of many proven strategies to finance rental property. It’s smart to look at the whole toolkit before picking your instrument. The flexibility of a HELOC is its main draw, but it’s not always the best or only way to tap into your property's equity.

Depending on where you're at with your investment goals, your comfort with risk, and how your property is performing, a different financing product might actually serve you better. Let’s walk through the main contenders.

Cash-Out Refinance

The most common alternative is the cash-out refinance. It’s pretty straightforward: you replace your existing mortgage with a new, bigger one. The difference between the two loans comes straight to you as a tax-free lump sum of cash.

Think of it as hitting the reset button. You're wrapping your old loan and the equity you're pulling out into one new, predictable package. The big win here is that cash-out refinances usually have a fixed interest rate, so your monthly payment is set in stone. For investors who live and die by their cash flow projections, that stability is golden.

But there's a catch. You're refinancing the entire mortgage. If you locked in a fantastic, low interest rate a few years back, you'll have to give that up. It's a classic trade-off: is getting a big pile of cash now worth sacrificing that great rate on your primary loan?

Traditional Second Mortgage

A traditional second mortgage—often called a home equity loan—is another solid choice. This works just like a car loan or personal loan. You get a lump sum of cash upfront and pay it back in fixed monthly installments over a set period. Simple.

This is the perfect move when you have a specific, one-time project with a clear price tag. Maybe it's the down payment on your next property or a major renovation where you already have a contractor's quote. You know exactly what you'll owe each month, making it super easy to budget for.

The downside? It's not flexible. Unlike a HELOC, you can't draw money as you need it. You get the funds once, and that's it. If you need more later, you have to go through the whole application process again.

No matter which path you're considering, the journey to getting approved looks pretty similar.

This flowchart shows that whether it's a HELOC or one of these alternatives, the core steps of gathering your docs, finding the right lender, and getting through underwriting are fundamentally the same.

The Investor’s Secret Weapon: The DSCR Loan

Now, for the serious real estate investors out there—especially if you're self-employed or have a more complex financial picture—the DSCR loan is an absolute game-changer. DSCR stands for Debt Service Coverage Ratio, and it qualifies you based on one simple question.

Does the property’s rental income cover its mortgage payment and other expenses? If the answer is yes, you’re probably getting the loan.

That's the magic right there. Lenders offering DSCR loans don't get bogged down in your personal W-2s, tax returns, or employment history. They care about one thing: does the asset itself generate enough cash to pay its own bills? Most lenders will want to see a DSCR of 1.25 or higher, meaning the property pulls in 25% more income than it costs to run.

This makes it the perfect financing tool for investors who:

- Are self-employed and find it a headache to document personal income the traditional way.

- Want to scale their portfolio fast without letting their personal debt-to-income ratio get in the way.

- Already own several properties and need a straightforward path to financing the next deal based purely on its own merits.

Sure, the interest rates might be a touch higher than a conventional loan, but the ease of access and the focus on the property’s performance make DSCR loans an indispensable tool for growth. If you want to get into the nitty-gritty, you can learn more about what a DSCR loan is and see how it could help you expand your portfolio.

Navigating the Investor-Specific Hurdles

Applying for a **HELOC on an investment property** isn’t quite like getting a loan for your own home. The whole process is different because, as an investor, your financial picture often looks a lot more complex than a typical W-2 employee’s.For starters, many real estate investors are self-employed or run their portfolio like a business. This means standard income verification, like pay stubs and tax returns, doesn't tell the whole story. This is a common snag that can stop an application dead in its tracks with a big, conventional bank.

If You're Self-Employed, You Have Options

When your income flows from your real estate business, you need to find lenders who know how to look past the usual paperwork. Thankfully, investor-focused lenders get it and have programs built specifically for people like you.

Here’s what they often offer:

- Bank-Statement Loans: Instead of tax returns, these lenders will look at 12 to 24 months of your bank statements (either personal or business) to see your actual cash flow. They use this real-world data to figure out what you can afford.

- Profit & Loss (P&L) Loans: You can also have a CPA prepare a Profit & Loss statement that shows your business is healthy and generating enough income to handle the new debt.

These alternative documentation programs are a game-changer for entrepreneurs. They let the true performance of your business speak for itself, helping you secure the financing you need to keep growing.

What If Your Property Is in an LLC?

Smart investors often hold their properties in a Limited Liability Company (LLC) to protect their personal assets. It's a great strategy, but it can throw a wrench in the works when you apply for a HELOC, as many traditional banks won't lend to an LLC.

This is another area where specialized lenders shine. They understand why you use an LLC and are comfortable with it. They will almost always require you to sign a personal guarantee, which is your promise to personally repay the loan if the LLC can't. This gives the lender the security they need while letting you maintain your smart asset protection strategy.

The secret is finding the right lender. Partnering with a mortgage broker who specializes in investment properties can be a huge advantage. They have a roster of investor-savvy lenders and know exactly who to call, saving you the time and frustration of applying at the wrong places.

Avoiding Common Investor Traps

A HELOC can be a powerful tool, but it demands respect and careful management. More and more investors are tapping into their equity for everything from renovations to down payments on new properties. And while delinquency rates are low, you still need to be careful. You can read more on home equity trends and their reliability to get a broader perspective.

Keep these two potential pitfalls in mind:

- Forgetting About Variable Rates: Your HELOC's interest rate will likely fluctuate. A sudden rate hike can shrink your profit margins or even put you in the red. Always stress-test your numbers. See if the property still cash-flows if your rate jumps a few percentage points.

- Miscalculating Your Real Costs: Profit isn't just rent minus the mortgage payment. You have to factor in all the expenses a lender will look at: property taxes, insurance, routine maintenance, property management fees, and a fund for when the property sits vacant.

By thinking ahead about these investor-specific issues and working with pros who live and breathe this stuff, you can make the HELOC process much smoother and get the capital you need to scale your portfolio.

Your Top Questions About Investment Property HELOCs, Answered

Getting into the weeds of investment property financing can feel a bit overwhelming. Let's clear up some of the most common questions real estate investors ask when considering a HELOC.

Can I Get a HELOC if I Already Have a Mortgage on the Property?

You bet. This is actually the most common way it’s done. Think of a HELOC as a second lien that simply sits behind your primary mortgage in the pecking order.

Lenders look at something called the Combined Loan-to-Value (CLTV) ratio. They'll take your current mortgage balance, add the HELOC amount you're asking for, and divide that total by your property's appraised value. As long as the CLTV is within their acceptable range, you’re good to go.

How Is My Interest Rate Determined?

Almost every HELOC on an investment property comes with a variable interest rate. The rate isn't just a random number; it's typically tied to a benchmark index, like the Prime Rate, plus a "margin."

This margin is the lender's slice of the pie, and it's based on their assessment of risk. The main things they look at are:

- Your personal credit score

- The property's CLTV

- Your overall financial picture and the property's risk profile

What’s the Minimum Credit Score I Need?

The bar is definitely higher for investment properties than for your personal home. While specific requirements vary by lender, you should really aim for a credit score of 700 or higher to be a strong candidate.

Lenders view loans on investment properties as a bigger risk. When you can show them a strong credit history, it proves you're a reliable and financially stable borrower, which makes them much more comfortable lending to you.

Remember to factor in all the financial details. A great resource is this guide on the mortgage interest deduction for rental property, which can affect your bottom line. At the end of the day, a higher score doesn't just get your foot in the door—it helps you lock in a better interest rate and a lower margin.

Ready to see how an investment property HELOC can fuel your real estate ambitions? The team at Mortgage Seven LLC lives and breathes investor financing. We'll help you cut through the complexity and tap into your property's equity. Schedule your consultation with us today!

Leave a Reply