So, you're thinking about building a house from the ground up? It's an exciting prospect, but it works a little differently than buying a place that's already built. Instead of a standard mortgage, you'll need a special kind of financing: a home construction loan.

This isn't your typical home loan. It’s a short-term loan with a higher interest rate designed specifically to cover the costs of building a new home. Where a traditional mortgage gives you a big lump sum of cash to buy a house, a construction loan releases money in stages, or draws, as your project hits key building milestones.

Your Financial Blueprint for Building a Home

Think of it less like a mortgage and more like a financial toolkit for your build. It’s the structured funding that turns those blueprints on your table into a real, livable home. A regular mortgage finances a finished product; a construction loan finances a process.

This is a really important distinction. The lender isn’t just cutting you a check and walking away. They’re an active partner in your project, releasing money to your builder only after they've verified that certain phases of the work are actually complete and up to snuff. This draw process is a safeguard for everyone involved.

Key Takeaway: The staged funding of a home construction loan makes sure money is spent as planned. It lowers the risk for the lender and keeps you and your builder accountable, ensuring the project stays on track from the foundation all the way to the final coat of paint.

How the Draw Process Works

The draw schedule is really the engine of a home construction loan. Before anything gets started, you, your builder, and your lender will map out a series of construction milestones. Every time your builder hits one of these targets, they can request a "draw" to get paid for the work they just finished.

Common milestones usually look something like this:

- Land acquisition and site prep: Buying the lot, clearing it, and getting it ready.

- Foundation poured: The concrete slab or basement walls are complete.

- Framing completed: The home’s structural skeleton is up.

- "Dry-in" stage: The house is now weatherproof with windows, doors, and a roof.

- Final finishes: Drywall, flooring, cabinets, fixtures—all the finishing touches.

After a draw request comes in, the lender sends an inspector to the site to make sure the work is actually done. Once they give the green light, the funds are released. This cycle just repeats itself until your home is 100% complete.

A Different Financial Landscape

The global mortgage market, which includes this type of construction financing, is on a steady incline. It was valued at $1.60 billion in 2025 and is projected to hit $2.19 billion by 2032. This growth is fueled by strong demand for new homes, with North America holding a massive 30.2% market share in 2025. You can dig into more insights about the mortgage loan market to see how these trends play out.

Knowing this broader context helps you understand why lenders treat these loans differently. They're financing potential—a house that doesn't exist yet—which is naturally riskier than lending on a move-in-ready property. That risk is exactly why construction loans have their own unique rules and features.

To put it simply, getting a loan for a new build is a different ballgame than buying an existing home. Here's a quick breakdown of how they stack up.

Home Construction Loans vs Traditional Mortgages At a Glance

| Feature | Home Construction Loan | Traditional Mortgage |

|---|---|---|

| Purpose | To finance the construction of a new home | To purchase an existing, completed home |

| Term Length | Short-term, typically 12-18 months | Long-term, usually 15 or 30 years |

| Fund Disbursement | Paid out in stages (draws) as work is completed | Paid out as a single lump sum at closing |

| Interest Payments | Typically interest-only payments on the drawn amount | Principal and interest payments from the start |

As you can see, the core mechanics are built around the reality of the project—one is a work-in-progress, and the other is a finished asset.

Exploring the Main Types of Construction Loans

When you start looking into building a home, you'll quickly realize that not all home construction loans are created equal. Lenders have designed different loan structures to fit different kinds of projects and financial situations. Think of it like picking the right tool from a toolbox—the best one for you depends entirely on what you’re trying to build and your long-term goals.

Figuring out these different paths is your first major step. Each type has a unique way of getting you from a plot of land and a set of blueprints to a finished home with a traditional mortgage.

The three main flavors you'll come across are construction-to-permanent, construction-only, and renovation loans. Let's dig into how each one works.

The Streamlined Path: Construction-to-Permanent Loans

A construction-to-permanent loan is often the crowd favorite, and for good reason. People usually call it a “one-time close” or “single-close” loan because it bundles the construction financing and your final mortgage into one neat package. You go through one application, one approval process, and one closing. That’s it.

Here’s the process: once you’re approved, you get the funds to build your home. During the build, you typically only pay interest on the money that’s been drawn out to pay your builder. After the last nail is hammered and you get the certificate of occupancy, the loan automatically converts into a regular mortgage you’ll pay off for the next 15 or 30 years.

Key Advantage: The biggest win here is simplicity. Locking everything in upfront saves a ton of time, paperwork, and money since you aren't paying for a second round of closing costs. That kind of predictability is a godsend during a project as complex as a home build.

Imagine signing all the final loan documents before the first shovel even hits the dirt. You can proceed with the build knowing your permanent mortgage is already sorted, which takes away the stress of having to requalify for a loan later when interest rates or your own finances might have changed.

The Flexible Option: Construction-Only Loans

On the other side of the coin, you have the construction-only loan, also known as a "two-time close" loan. This is a much more segmented approach. As its name suggests, this loan only covers the building phase. It’s a short-term loan, usually for about a year, that you have to pay off in full once the house is finished.

This means you’ll need to secure a completely separate, traditional mortgage to pay off the construction loan when it’s due. That involves a second underwriting process, a second appraisal, and, you guessed it, a second closing with a second set of fees.

So why would anyone choose this path? It all comes down to one word: flexibility.

- Shopping for Rates: You aren't locked into a mortgage rate from the very beginning. If interest rates happen to drop while your home is being built, you have the freedom to shop around for the best deal on your final mortgage.

- Improved Financials: Maybe your credit score goes up or you get a raise during the 6-12 months of construction. With a two-time close, you can use that improved financial picture to qualify for a better loan than you would have at the start.

Of course, this flexibility comes with risk. Rates could just as easily go up, or your financial situation could take a hit, making it harder to qualify for that final mortgage. It’s a classic trade-off: the certainty of a one-time close versus the potential upside of a two-time close.

Financing for Transformations: Renovation Loans

So far, we’ve focused on building from the ground up. But what if your dream is to buy an existing house and turn it into something special? That’s where renovation loans step in.

These loans are perfect for buyers who want to roll the purchase of a property and the cost of major upgrades into a single loan. Instead of juggling a primary mortgage and a separate personal loan or home equity line for the remodel, you get one loan and one monthly payment. The funds for the renovation are held in an escrow account and paid out to your contractor in stages as the work gets done, much like a new construction loan.

While this guide is focused on new builds, it's helpful to know about related options like home renovation loans if you're planning a major remodel. The core idea of financing a work-in-progress is very similar.

Getting Approved for a Home Construction Loan

Let’s be clear: getting a construction loan is a much heavier lift than qualifying for a standard mortgage. Lenders see these loans as a bigger risk because they’re not funding a finished house—they're funding a blueprint and a promise.

Think about it from their perspective. With a regular mortgage, the house already exists. It’s a physical asset they can use as collateral from day one. With a construction loan, the collateral is built over time, nail by nail. That uncertainty means lenders will put your finances, your plans, and your builder under a microscope.

What Lenders Really Look For

While every lender has slightly different rules, they all zero in on a few key areas to decide if you and your project are a good bet. Nail these four elements, and you’re well on your way to a strong application.

Here's the breakdown of what you'll need to bring to the table:

- A Strong Credit Score: This is non-negotiable. Lenders want to see a history of responsible borrowing. You'll generally need a FICO score of 680 at a minimum, though many lenders feel much more comfortable with scores north of 700.

- A Low Debt-to-Income (DTI) Ratio: Lenders need to know you won't be stretched too thin. Your DTI ratio—your total monthly debts divided by your gross monthly income—should ideally be 43% or less. This shows them you can manage your current obligations and the new loan payments.

- A Serious Down Payment: Forget the 3% down of a conventional loan. For construction loans, you need to have more skin in the game. Expect to put down 20-25% of the total project cost. This commitment lowers the lender's risk and proves you're financially invested in the project's success.

- A Vetted and Reputable Builder: This one is huge. Your builder's track record is almost as critical as your own financial profile. Lenders will do their homework, verifying their license, insurance, and past work. They need assurance that your builder can finish the job on time and on budget.

Getting Your Paperwork in Order

Once your finances are solid, it's time to gather the mountain of documents required for a home construction loan. This isn't just about pay stubs and tax returns; you need to present a complete, professional package that details every single aspect of the build.

A well-organized and thorough loan package is your best friend. It shows the lender you're a serious applicant who has done their homework, which can dramatically boost your odds of getting approved.

To see exactly what paperwork you'll need to start collecting, you can find a comprehensive list right here in our home loan document checklist.

Key Documents You Will Need

Having your documents ready to go before you even apply will make the entire process feel less chaotic. The lender’s goal is to see a rock-solid plan that accounts for every potential cost and contingency.

You’ll absolutely need to provide these essential items:

- Detailed Architectural Plans: The full set of blueprints and specifications (often just called "the specs").

- A Signed Builder Contract: Your official, legally binding agreement with your general contractor.

- A Line-Item Budget: A granular breakdown of every single cost, from pouring the foundation to the last doorknob.

- Proof of Land Ownership: If you already own the lot, you'll need to provide the deed.

- Appraisal Documents: A special appraisal based on the home's future value after it's built.

- Permits and Licenses: Copies of all necessary building permits from your city or county.

Pulling all this together is what transforms your dream from a vague idea into a tangible, financeable project in the eyes of a lender.

Understanding Construction Loan Costs and Interest Rates

If you're used to traditional mortgages, the way a home construction loan is structured can be a bit of a curveball. The key is to understand how the interest and fees work so you can build a realistic budget and sidestep any expensive surprises along the way.

Unlike a typical home loan where you start paying principal and interest right away, construction loans feature interest-only payments during the building phase. This approach keeps your monthly payments manageable while your home is still a construction site—and likely a long way from being move-in ready.

The most critical thing to remember is this: you only pay interest on the money that has actually been paid out to your builder. This means your payments start small and grow as the project hits new milestones and more funds are released.

How Your Payments Grow Over Time

Let's say your total construction loan is for $400,000. You won't be making payments on that full amount from the get-go. Instead, your payments are tied directly to the builder's draw schedule.

Here’s a simple breakdown of how that works in practice:

- Draw 1 – Foundation ($50,000): The foundation is poured, it passes inspection, and the lender releases $50,000 to the builder. Your next monthly payment is calculated only on that $50,000.

- Draw 2 – Framing ($70,000): The framing goes up, and the builder requests the next draw of $70,000. Your total outstanding balance is now $120,000 ($50,000 + $70,000), and your next interest payment is based on this new, higher amount.

- Draw 3 – Dry-In ($80,000): After the roof, windows, and sheathing are installed, another $80,000 is disbursed. Your interest is now calculated on a $200,000 balance, and so on.

This escalating payment system is a fundamental feature of construction financing. It’s designed to keep your costs aligned with the actual, real-time progress of your build.

Key Insight: The draw-based, interest-only system keeps your initial cash outlay low. But it's crucial to budget for those payments to increase month after month as your builder completes more work and draws down more of the loan.

Looking Beyond the Interest Rate

While the interest-only structure is a huge part of the equation, it’s far from the only cost you'll encounter. Lenders have a variety of fees and requirements that you need to factor into your total project budget.

Recent market conditions have also played a big role. Construction loan interest rates in 2025 are up from their historic lows, with typical financing now falling in the 6.25% to 9.75% APR range. Part of this is because lenders have tightened their criteria, often requiring 25-30% in equity and basing approvals on a loan-to-cost ratio of 70-75%. You can dig deeper into the factors driving construction loan interest rates to get a clearer picture.

Make sure you’re prepared for these additional costs:

- Appraisal Fees: This isn't your standard home appraisal. The appraiser has to determine the future value of the home once it’s completed based on plans and specs—a more complex and pricier evaluation.

- Inspection Fees: Every time your builder requests a draw, the lender sends an inspector to verify the work is complete. You’ll be charged a fee for each of these inspections.

- Contingency Reserve: Lenders almost universally require a contingency fund, usually 10-20% of the total construction cost. This isn’t a fee they keep; it's your money set aside in a reserve account. This fund acts as a financial safety net to cover unexpected overruns or change orders, ensuring the project doesn't stall if something goes wrong.

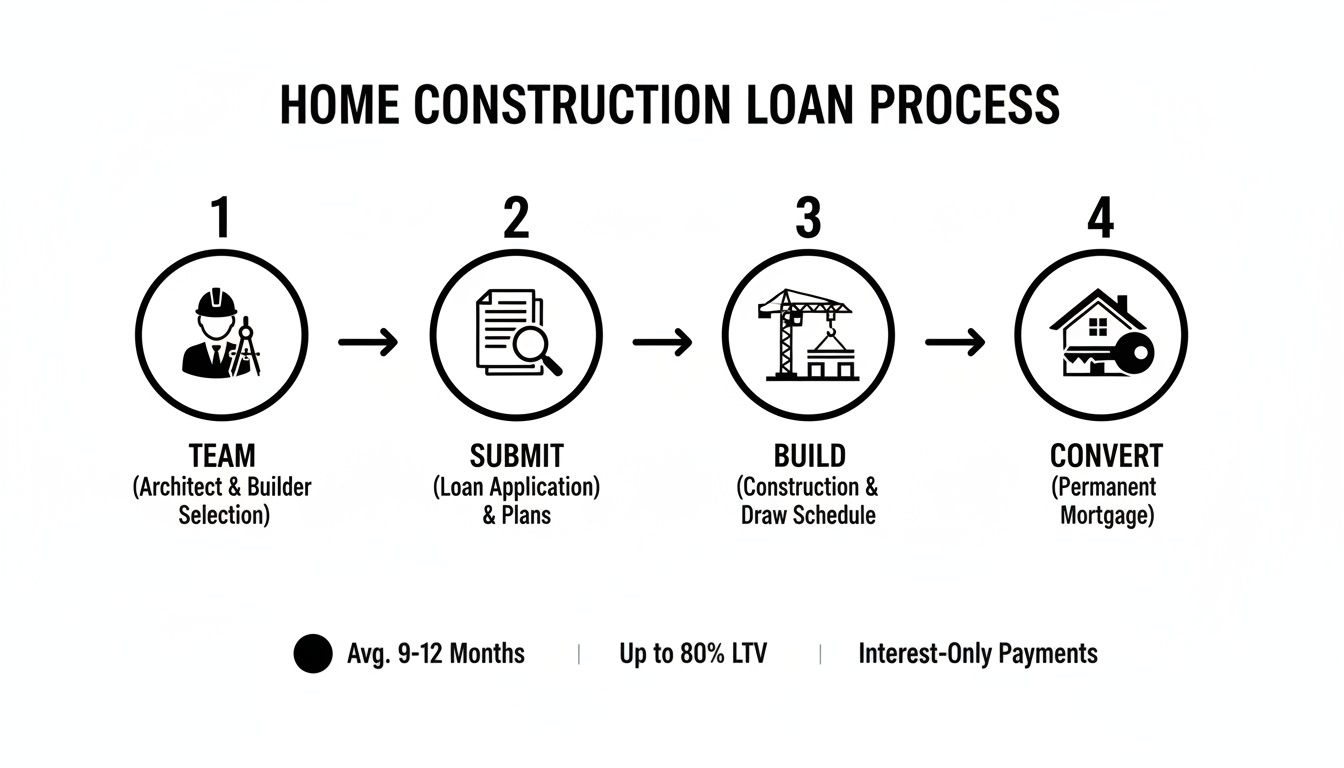

The Construction Loan Process: A Step-by-Step Guide

Building a home is a huge undertaking, but the financing side doesn't have to be a mystery. The whole process follows a logical sequence, and knowing what’s coming next can turn what feels overwhelming into a series of manageable steps.

Think of it like the blueprint for your home's financing. From day one to the final walkthrough, here’s the path you’ll follow.

Step 1: Assemble Your A-Team

Before you even think about talking to a lender, you need to get your key players lined up. This isn’t just a good idea—it’s a requirement. Lenders won't even look at an application until they see you have a credible, professional team ready to bring the project to life.

Your essential team includes:

- A Licensed General Contractor: This is the captain of your ship. Lenders will do a deep dive on your builder, checking their credentials, financial health, and past projects.

- An Architect or Designer: They create the detailed plans and specs that are the very foundation of your loan application.

Having a reputable builder and a full set of architectural plans is non-negotiable. It shows the lender your project is a serious, well-planned venture, not just a dream on a napkin.

Step 2: Get Pre-Approved and Submit Your Full Loan Package

With your team and plans ready, it’s time to talk to a lender about pre-approval. This is a critical early step. It gives you a realistic budget to work with and proves to your builder that you have the financial backing to move forward.

After pre-approval, you’ll gather everything for the formal loan application. Be prepared—this package is way more detailed than what’s needed for a standard mortgage. You’ll need to submit the blueprints, a line-item budget from the builder, the signed construction contract, and proof of permits. Of course, they’ll also take a close look at your personal finances to make sure you qualify.

Pro Tip: Your loan package is your sales pitch. A complete, meticulously organized submission presents your project as a sound investment, which can dramatically speed up the approval process.

Step 3: The Appraisal and Closing

Once your package is submitted, the lender orders a unique kind of appraisal. Instead of valuing an existing house, the appraiser has to determine the "as-completed" value—what your home will be worth once it's finished. They’ll use your blueprints, materials list, and sales of similar new homes in the area to land on a number.

If the appraised value supports the project cost and the loan gets the green light, you head to closing. With a one-time close loan, this is the big day where you sign all the documents for both the construction financing and the permanent mortgage that follows. It's a major milestone that officially unlocks the funds for your build.

Step 4: The Build and Draw Schedule

After you close, the real fun begins: construction. But the loan funds aren’t just handed over in a big check. The lender holds the money and pays it out in stages based on a pre-approved draw schedule.

Here’s how it works: your builder hits a milestone, like pouring the foundation or finishing the framing, and then requests a "draw" from the lender. The lender then sends an inspector to your job site to confirm the work is done and up to snuff. Once the inspection passes, the funds for that phase are released to the builder. This build-inspect-pay cycle repeats until the house is done. For a closer look at these mechanics, check out our guide to the mortgage process.

Step 5: The Final Inspection

When the last nail is hammered and the final coat of paint is dry, the project moves into its last phase. The builder will let the lender know the home is finished, which triggers one last, thorough inspection.

This isn’t just a quick look-around. The inspector’s job is to verify that the finished home matches the original plans and specifications you submitted months ago. Around the same time, your local building department will do their own final inspection to issue a Certificate of Occupancy—the official document that says your home is safe and legal to live in.

Step 6: Converting to a Permanent Mortgage

You’ve passed the final inspection and have the Certificate of Occupancy in hand. The last step is to transition the loan into its permanent form.

If you chose a construction-to-permanent loan, this part is almost automatic. The loan simply rolls over into a standard mortgage, and you start making your regular principal and interest payments. If you went with a construction-only loan, now is the time to secure a separate, traditional mortgage to pay off the balance of the construction loan.

Common Pitfalls in Construction Financing and How to Avoid Them

Building a home is an incredible journey, but let's be honest—it’s also filled with financial landmines. Getting a home construction loan is a different beast than a standard mortgage, and a little foresight can save you from the common mistakes that throw budgets and timelines into chaos. The trick is knowing what to look for before it becomes a real problem.

One of the easiest traps to fall into is underestimating the true cost of the project. Your builder’s quote is just the starting point. It often doesn't include big-ticket items like landscaping, permit fees, or hooking up utilities. This leads directly to the second mistake: not having a big enough safety net. You absolutely need a contingency fund of at least 10-20% of your total budget. This isn't "extra" money; it's what will save your project when the unexpected happens.

Understanding this flow from assembling your team to closing the final loan helps you see where potential delays and financial hurdles might pop up along the way.

Vetting Your Builder Thoroughly

The single most important decision you will make is choosing your builder. A bad partnership with an unreliable or financially shaky contractor isn't just a headache; it can be a complete disaster. You have to do your homework, and it goes way beyond a gut feeling or just picking the lowest bid.

Before you even think about signing a contract, make sure you've taken these steps:

- Verify Licensing and Insurance: Check that their general contractor license is current and they have proper liability and workers' compensation insurance. Don't just take their word for it.

- Check Multiple References: You need to talk to at least three recent clients. Ask them the tough questions about how the builder handled the budget, communication, and the final quality of the work.

- Review Their Portfolio: Go see their finished projects in person. Nothing tells you more about a builder's quality than seeing their work stand the test of time.

A good builder will have a solid grasp of effective construction cash flow management, which is critical to keeping the project on track. You should also take a moment to learn how to spot and avoid common home financing scams to protect your investment.

Managing Delays and Cost Overruns

Even with the best builder in the world, things happen. Supply chain issues can hold up materials for weeks, and those seemingly small "change orders" you make mid-project can add up fast. The key is to manage these things proactively.

Try to lock in prices for materials whenever you can. More importantly, get every single change order in writing, with the cost clearly spelled out and approved by you. This is the only way to prevent your budget from slowly creeping out of control.

It's also worth noting that the financing world itself can be unpredictable. In the first quarter of 2025, for instance, residential construction loans totaled a massive $90.0 billion. That number reflects a market where lending standards can tighten quickly. With nonaccrual loans (loans where the borrower has fallen behind) hovering around 1.2%, it's clear there are risks for anyone who isn't fully prepared.

Your Top Home Construction Loan Questions, Answered

Thinking about building a home from the ground up naturally comes with a lot of questions. Let's tackle some of the most common ones I hear from clients, so you can get a clearer picture of how this all works.

I Already Own the Land. Can I Still Get a Construction Loan?

Yes, and in fact, you’re in a great position! Owning your land free and clear gives you a massive head start. Lenders love to see this, and they'll often let you use your land's equity as your down payment.

Think of it this way: if your land is valued at $100,000 and your total project is $500,000, that $100,000 in land equity could completely satisfy the lender's typical 20% down payment requirement. You’ll just need your deed and a recent appraisal to prove its value.

What if the Build Goes Over Budget?

It happens. That's precisely why lenders require a contingency reserve. This is a safety net, usually 10-20% of the total loan amount, set aside specifically for surprises like a sudden jump in lumber prices or an unexpected change you decide to make.

If your costs go over budget, you'll dip into this reserve first. But if the overages exhaust both the loan and the contingency funds, the responsibility to cover the rest falls on you. This is why a realistic budget and a trustworthy builder are your best friends in this process.

How Does a Lender Know What My Unbuilt Home is Worth?

Great question. They don't guess! The loan is based on the home’s future “as-completed” value. A specialized appraiser reviews every detail—your blueprints, your list of materials (the "spec sheet"), and recent sales of similar new homes in the area.

Based on all that information, they produce a professional opinion of what your home will be worth the day the builder hands you the keys. This future value is the number the bank uses to calculate how much they’re willing to lend.

Can I Save Money by Being My Own General Contractor?

It’s tempting to think about managing the build yourself to cut costs, but most lenders will say no. From their perspective, a licensed, insured, and bonded general contractor isn't a luxury—it's a critical part of ensuring the project stays on track, meets building codes, and gets finished properly.

They see an experienced professional as the best way to protect their investment, and yours.

Building a custom home is one of the most rewarding journeys you can take. Having the right financing partner in your corner is non-negotiable. At Mortgage Seven LLC, we live and breathe construction financing. We know how to navigate the complexities to find the loan that fits your vision.

Ready to take the next step? Schedule your free consultation today!