A home pre-approval is your golden ticket in the homebuying process. It's a conditional commitment from a lender, confirming they're willing to loan you a specific amount of money to buy a house. Think of it less like a suggestion and more like a VIP pass—it tells sellers and real estate agents you're a serious, qualified buyer who's ready to make a real offer.

What a Home Pre Approval Really Means for You

Imagine walking into an open house, not just browsing, but knowing exactly what you can afford. That's the power a home pre-approval gives you. It shifts you from being a casual looker to a genuine contender in the real estate game. Honestly, it's probably the single most important step you can take before you even start looking at listings.

This isn't just some ballpark estimate. A pre-approval letter is a lender's formal declaration, issued only after they've done a deep dive into your finances, that you're good for a certain loan amount. With this letter in hand, you gain some serious advantages.

The Power of a Pre-Approval Letter

Having a pre-approval letter completely changes how you're viewed as a homebuyer. It proves to everyone involved—from your agent to the person selling their home—that you have the financial backing to see the deal through.

- Sets a Realistic Budget: It clearly spells out your maximum loan amount, so you can stop wasting time on homes outside your price range. This saves you from the heartache of falling in love with a property you simply can't afford.

- Strengthens Your Offer: In a competitive market, sellers love seeing a pre-approval. It tells them your financing is unlikely to fall through, making your offer much more secure than someone else's. This can be the very thing that gets your offer accepted in a bidding war.

- Speeds Up the Closing Process: Because the lender has already done most of the heavy lifting on your financial verification, the final steps to closing the deal can happen much more quickly.

A home pre-approval isn't just a box to check—it's a strategic move that puts you miles ahead of the competition. In fact, pre-approved buyers have been shown to close up to 91% faster than those without one, which can shave weeks off your timeline.

From Financial Clarity to Closing Confidence

Getting pre-approved is also about understanding the long-term commitment you're making. It forces you to get real about the numbers, and a key part of that is doing a mortgage payment calculation to see what your monthly expenses will actually look like. This clarity ensures you're not just getting a loan, but one you can comfortably live with.

Ultimately, getting pre-approved is about arming yourself with the confidence and negotiating power you need to win. It’s the official green light that says you're no longer just dreaming about a new home—you're making it happen.

Pre Approval vs Prequalification: Understanding the Critical Difference

When you start your homebuying journey, you’ll hear the terms “prequalification” and “pre-approval” thrown around a lot. It’s easy to think they mean the same thing, but in the eyes of a seller, they’re worlds apart. Getting this distinction right from the start gives you a massive advantage and the confidence to shop for a home you can truly afford.

Think of it this way: a prequalification is like window shopping. You're just getting a feel for what might be in your price range. A home pre-approval, on the other hand, is like walking into the store with cash in hand. It proves you're ready and able to make a serious purchase.

What Is a Prequalification?

A prequalification is essentially a quick, informal conversation about your finances. It's the first step where a lender gives you a rough estimate of what you might be able to borrow based on information you provide off the top of your head.

You’ll answer a few basic questions, such as:

- What’s your approximate annual income?

- What are your monthly debt payments (like car loans or credit cards)?

- How much do you have saved up for a down payment?

- Do you have a general idea of your credit score?

Based on your answers, the lender gives you a ballpark number. No documents are checked, and your credit isn't usually pulled. It's a helpful starting point to gauge your budget, but it carries very little weight when you're ready to make an offer.

What Makes a Home Pre-Approval Different?

A home pre-approval is the real deal. This is where a lender digs in and thoroughly vets your financial situation to give you a firm, conditional commitment for a loan. They aren’t just taking your word for it anymore; they’re asking for proof.

A pre-approval transforms you from a casual house hunter into a serious, qualified buyer. It’s a lender’s conditional promise to loan you a specific amount, backed by a deep dive into your actual financial documents.

During the pre-approval process, the lender will pull your credit report (a hard inquiry) and ask for documentation to verify everything—your income, your assets, your employment history, and your debts. Because it’s based on verified facts, a pre-approval letter gives you serious negotiating power. It tells sellers that you’re a low-risk buyer whose financing is already lined up, making your offer far more attractive and competitive.

To put it simply, the two serve very different purposes. Here's a quick breakdown of how they stack up against each other.

Pre-Approval vs Prequalification at a Glance

| Feature | Prequalification | Pre-Approval |

|---|---|---|

| Verification Level | Based on self-reported financial data. | Based on verified documents (pay stubs, bank statements, tax returns). |

| Credit Check | Typically a soft credit pull, or sometimes none at all. | Requires a hard credit inquiry, which is more thorough. |

| Lender Commitment | An informal estimate of borrowing power; not a commitment. | A conditional commitment to lend a specific amount. |

| Impact on Offer | Offers little to no advantage when making an offer. | Significantly strengthens your offer, showing you are a serious buyer. |

As you can see, while a prequalification is a good first conversation, a pre-approval is what you need to be taken seriously in a competitive market. It’s the key to unlocking your true buying power.

What Lenders Actually Look At: Your Documents and Financial Story

Getting a mortgage pre-approval isn't some mysterious process. It’s really about telling a clear, verifiable story of your financial life. Lenders need to see on paper that you can confidently handle a mortgage, so they'll dig into your income, assets, debts, and credit history.

Think of it like putting together a puzzle. Every document you provide is a piece that helps the lender see the full, stable picture of your finances.

The review is meant to be thorough. Lenders are looking at your entire financial health, including any existing debts or liens. This is why understanding potential hurdles, like navigating an IRS lien on a home, is so important before you even start. The more you prepare upfront, the smoother this whole thing will be.

The Core Four: What Lenders Need to See

For most traditional borrowers, the required documents fall into four main categories. Getting these organized ahead of time is the single best thing you can do to speed up your pre-approval.

- Proof of Income: Lenders need to see that you have consistent, reliable money coming in. This is their proof you can make the monthly mortgage payments.

- Proof of Assets: This is how you show you have the cash for the down payment, closing costs, and some reserves left over. It’s all about demonstrating financial stability.

- Credit History: Your credit report and score give lenders a quick snapshot of how you’ve handled debt in the past. It helps them gauge how reliable you are.

- Employment Verification: A stable job is the source of your income, so lenders will call to confirm you’re still employed.

Nailing these four areas is your first step toward a rock-solid application. Let's break down exactly what you’ll need.

Your Go-To Checklist for a Standard Loan

If you’re a W-2 employee, your list is pretty straightforward. The goal is to paint a clear picture of your finances over the last two years.

Here’s what you’ll need to verify your income:

- Recent Pay Stubs: Usually from the last 30 days.

- W-2 Forms: From the past two years to show a consistent work history.

- Federal Tax Returns: Lenders will want your complete personal tax returns for the last two years.

And here's what you'll need to verify your assets:

- Bank Statements: Typically the last two months for all your checking and savings accounts. Be ready to explain any large, out-of-the-ordinary deposits.

- Investment Account Statements: This includes statements from your 401(k), IRA, or any brokerage accounts.

This list covers the basics for most folks. For a super detailed breakdown, you can check out our full guide on all the documents needed for mortgage pre approval.

What If I'm Not a Traditional W-2 Earner?

Life isn’t one-size-fits-all, and neither are mortgages. That’s where specialized loan programs come into play. Lenders like Mortgage Seven LLC are pros at working with people who have unique financial situations, from business owners to real estate investors. These programs use different kinds of documentation to prove you can handle the loan.

The modern mortgage world finally understands that a W-2 isn't the only sign of financial strength. Lenders now offer flexible programs that look at the bigger picture, from business cash flow to investment property income.

These alternative loans are a game-changer, opening doors for so many people who would have been turned down by a conventional lender in the past.

Documents for the Self-Employed and Business Owners

If you run your own business, your paperwork will look a bit different. Instead of W-2s, you’ll be providing documents that prove your business is profitable and that you draw a steady income from it.

- Profit and Loss (P&L) Statements: A lender will usually ask for a year-to-date P&L, often one put together by your accountant, along with P&Ls from the previous one to two years.

- Bank-Statement Loans: This is a fantastic option. Lenders analyze 12 to 24 months of your business or personal bank statements to calculate an average monthly income. It's a way to qualify without using tax returns, which often show a lot of write-offs.

These programs are built for entrepreneurs whose tax returns don't tell the full story of their cash flow.

Programs for Real Estate Investors and Non-Residents

Real estate investors and non-U.S. citizens also have their own pathways to getting pre-approved.

- Debt Service Coverage Ratio (DSCR) Loans: This program is made specifically for real estate investors. The lender qualifies you based on the investment property's rental income, not your personal salary. They just need to see that the expected rent will cover the new mortgage payment. No personal income verification needed.

- ITIN Loans: These are designed for non-U.S. citizens who work and pay taxes here but don't have a Social Security number. Borrowers can use their Individual Taxpayer Identification Number (ITIN) to apply, along with other ways to prove their credit history and income.

Knowing which box you fit into is the key. It helps you gather the right documents from the start and find a lender who knows how to work with your specific financial profile.

A Step-by-Step Guide to the Pre-Approval Process

Getting a home pre-approval might feel like a huge, complicated ordeal, but it’s really just a series of clear, logical steps. Think of it less like a test and more like putting a puzzle together with your mortgage expert. When you know what’s coming next, the whole experience feels much more manageable and, dare I say, even empowering.

This is a team effort. Your mortgage expert is your guide, and your role is to provide the necessary info so they can map out the best path for you. Let's walk through the four key stages you'll encounter on your way to getting that powerful pre-approval letter.

Stage 1: The Initial Consultation

Everything starts with a simple conversation. Before any applications are filled out, you’ll have a chat with a mortgage professional, like one of our experts here at Mortgage Seven LLC. This isn't the application itself; it's more of a strategy session to get on the same page about your goals and your financial situation.

We'll talk about your income, how much you have saved, and the kind of home you're dreaming of. This initial discussion helps us figure out which loan programs are the best fit for you. Are you a traditional W-2 employee? Or maybe a business owner who would benefit from a bank-statement program? An investor looking for a DSCR loan? The goal here is to set a clear direction from the very beginning.

Stage 2: Application and Document Submission

With a game plan in place, it's time to make it official. You'll fill out the formal mortgage application, officially known as the Uniform Residential Loan Application (URLA), which captures all the necessary financial details.

This is also when you'll hand over all the documents we talked about earlier—your pay stubs, W-2s, bank statements, and tax returns. A little organization goes a long way here. Having all your documents ready to go can shave significant time off the process.

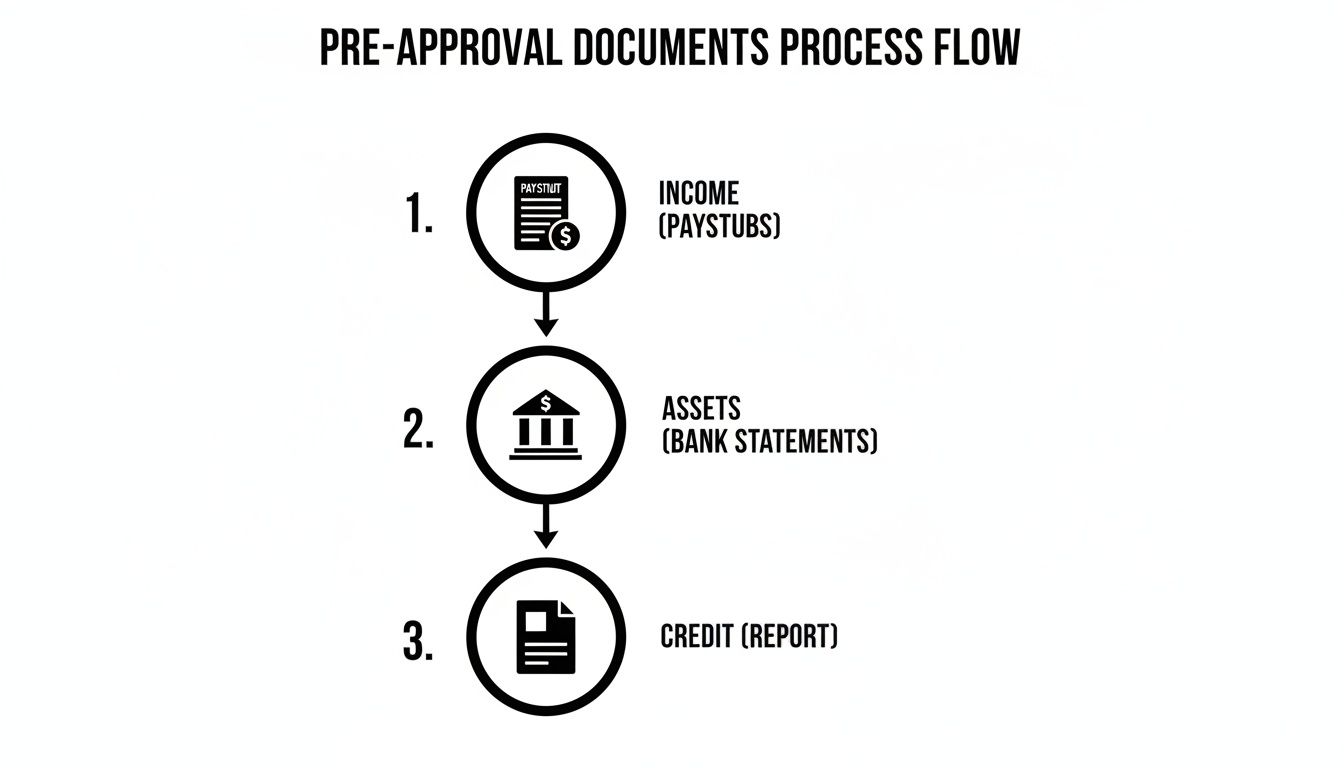

This flow chart breaks down the three core areas lenders examine with your documents.

Each piece of paper tells a part of your financial story, giving the lender a complete, verifiable picture of your ability to manage a mortgage.

Stage 3: The Underwriting Review

Once your application and documents are in, your file heads to an underwriter. Think of the underwriter as a financial detective. Their job is to verify every single detail, confirm your employment, pull your credit report, and review your bank statements to make sure everything lines up.

The underwriter’s role is to ensure your financial story adds up and meets the specific guidelines for the loan program you've chosen. Their approval is the green light that confirms you are a qualified borrower.

If they have questions—say, about a large, recent deposit in your checking account—they'll reach out to your loan officer for clarification. Responding to these requests quickly is the secret to keeping things moving forward without a hitch. For a deeper dive into this stage, our home buying process checklist is an excellent resource.

Stage 4: Conditional Approval and the Pre-Approval Letter

After the underwriter has crossed all the t's and dotted all the i's, you’ll receive a conditional approval. This is fantastic news! It means you're approved, pending a few final items (the "conditions") that usually relate to the specific house you choose, like a satisfactory appraisal and clear title report.

This is the moment you get the prize: the official pre-approval letter. This document clearly states the loan amount you qualify for, the type of loan, and the interest rate. It's typically valid for 60 to 90 days, giving you plenty of time to house hunt.

So, how long does all this take? For a borrower with a straightforward W-2 job and all their ducks in a row, it can be as fast as a few business days. For more complex situations, like for a self-employed buyer, it might take a week or so. No matter the timeline, finishing this process means you're ready to shop with the confidence and power to make a winning offer.

How to Strengthen Your Application and Boost Your Approval Odds

Getting a home pre-approval isn't about luck—it’s about smart preparation. Think of it like training for a marathon; the work you put in before the race starts is what really determines how well you'll do. By taking a few key steps before you even talk to a lender, you can present a much stronger financial picture and seriously increase your chances of getting that green light.

Ultimately, you want to show a lender two things: financial stability and that you manage your credit responsibly. This means getting ahead of the game and focusing on the very same metrics they’ll be scrutinizing in your file.

Polish Your Financial Profile

Before you send over a single document, take some time to tidy up your finances. Lenders love seeing a clean, stable, and organized financial history. It makes their job easier and makes you look like a great candidate.

- Boost Your Credit Score: This is single-handedly one of the most powerful moves you can make. Pay every single bill on time. If you have any old collections or late payments lingering, now's the time to handle them. A higher score doesn't just help you get approved; it often gets you a better interest rate.

- Lower Your Debt-to-Income (DTI) Ratio: Lenders look at how much of your monthly income goes toward debt payments. You can lower this DTI ratio by paying down high-interest credit cards or other loans. A lower DTI sends a clear signal that you aren't financially overstretched.

- Organize Your Down Payment: Make sure your down payment money is sitting in one single account for at least two months. Lenders have to "source" and "season" these funds, and having everything in one place avoids a lot of questions about large, last-minute deposits.

A lender's primary goal is to confirm you are a reliable borrower. Presenting a clean credit report and a low debt-to-income ratio is the clearest signal you can send that you are financially prepared for homeownership.

Avoid These Common Pre-Approval Pitfalls

What you don't do is just as important as what you do. Once you start the pre-approval process, your finances are officially under a microscope. Any sudden financial moves can raise red flags and put your entire approval at risk.

And in today's market, this matters more than ever. With so much competition, a squeaky-clean application helps you stand out and secure the best possible rates. As Redfin's housing market predictions show, being a prepared buyer is a huge advantage.

Critical Don'ts During the Approval Process

To keep your application moving smoothly, you absolutely must steer clear of these common mistakes. They can derail even the strongest file.

- Don't Apply for New Credit: This is a big one. Avoid opening new credit cards, financing a car, or even buying furniture on a payment plan. Every new inquiry dings your credit score and can mess with your DTI ratio.

- Don't Change Jobs: Lenders crave stability. Suddenly switching jobs, especially if you move from a salaried W-2 role to one that's commission-based or self-employed, can create a massive headache for underwriters.

- Don't Make Large, Undocumented Deposits: Avoid depositing large sums of cash into your bank account. Lenders have to verify where every dollar comes from, and they can't use "mattress money" that has no paper trail.

- Don't Miss Any Payments: Keep paying every bill on time, without exception. A single late payment reported while your loan is in process can be catastrophic and might even lead to a denial.

Following these simple do's and don'ts will position you as an ideal borrower. To dive deeper into the specific numbers and benchmarks lenders look for, check out our guide on how to qualify for a mortgage.

Frequently Asked Questions About Home Pre-Approval

Even after you've got the basics down, a few questions always pop up when you're getting serious about buying a home. Getting pre-approved is a huge step, and it’s completely normal to wonder about the finer points. Let’s tackle the most common questions we hear from buyers just like you.

Think of this as your go-to resource for those nagging little details. We've talked about the big picture; now it's time to zoom in on the practical stuff that really matters when you start looking at houses.

How Long Is a Home Pre-Approval Good For?

Your pre-approval letter does have an expiration date. Typically, a home pre-approval is valid for 60 to 90 days. Why the time limit? Because your financial situation isn't static—credit scores change, income can fluctuate, and debt levels go up and down. Lenders need a recent snapshot of your finances to confidently back their offer.

If your house hunt takes longer than that, don't sweat it. It’s a common scenario and not a major hurdle. You'll just need to touch base with your mortgage advisor and provide some updated documents, like your latest pay stubs and bank statements. They can get your pre-approval renewed quickly, so you can stay in the market as a strong, prepared buyer.

Can I Get Pre-Approved by Multiple Lenders?

Yes, you absolutely can—and honestly, it's a savvy move. Shopping your mortgage with a few different lenders lets you compare interest rates, closing costs, and loan terms side-by-side. It’s the best way to make sure you’re getting a great deal and not leaving thousands of dollars on the table over the life of your loan.

A lot of people worry this will tank their credit score. While it’s true that each application results in a hard inquiry, the credit bureaus are smart about this. They recognize that you’re rate shopping for a single major purchase. As a result, all mortgage-related inquiries made within a short window (usually 14-45 days) are bundled together and treated as just one inquiry. This allows you to find the best possible loan without penalizing your credit score.

A denial is not the end of your homeownership journey. Instead, view it as a detailed, personalized roadmap showing you exactly what financial areas need attention to achieve a successful approval in the future.

What Happens if My Pre-Approval Is Denied?

Getting a denial can sting, there's no doubt about it. But it's so important to see it not as a final "no," but as a "not yet." Better yet, a denial gives you a clear, actionable game plan. Lenders are legally required to tell you why they denied your application, giving you a roadmap for what to fix.

Some of the usual suspects for a denial include:

- A high debt-to-income (DTI) ratio, which means too much of your monthly income is already spoken for by other debts.

- A low credit score that falls below the lender's minimum threshold for a particular loan program.

- Insufficient or unverified income, making it tough for the lender to confirm you can handle the new mortgage payment.

Your first move should be to call your mortgage professional and go over the denial letter together. They can help you map out a strategy, whether it's paying down a specific credit card, disputing errors on your credit report, or just giving it a little more time to build a longer work history. A denial today can easily pave the way for a solid approval tomorrow.

Ready to turn your homeownership dreams into reality? The expert team at Mortgage Seven LLC is here to guide you through every step of the pre-approval process with personalized advice and access to a wide network of loan programs. Start your journey with confidence by visiting https://mtg7.com to schedule your consultation today.