Before you even start asking "how can I refinance," the real first question should be, "should I refinance?" A successful refinance is all about timing. It’s when your personal financial goals, the current market, and your own situation all click into place. This isn't about chasing news headlines; it's a strategic move that has to fit your life.

Is Now the Right Time to Refinance?

Figuring out if you should refinance your mortgage is a major financial decision, and it goes way beyond just spotting a lower interest rate advertised online. Think of it as a calculated move that needs to line up perfectly with your long-term plans. Are you looking to slash your monthly bills, fund a big life event, or just get a better handle on your overall debt? The right time to pull the trigger is when the numbers make sense for you.

The market can turn on a dime, creating golden opportunities for homeowners. We saw this back in September 2025 when 30-year fixed rates hit a one-year low. What happened? Refinancing activity skyrocketed by a massive 54.2% as homeowners rushed to lock in those savings. As the National Association of Home Builders reported, it just goes to show how quickly people will act when the rates are right.

Key Triggers for a Refinance

So, what are the common signs that it might be time to look into refinancing? From my experience, homeowners usually start exploring their options when they find themselves in one of these situations:

- You want a lower monthly payment. This is the number one reason, hands down. If rates today are noticeably lower than what you're currently paying, a simple rate-and-term refinance can drop your monthly payment and put more cash back in your pocket.

- You need to fund a major expense. Life happens. Whether it's a dream kitchen remodel, college tuition bills, or startup capital for a new business, a cash-out refinance lets you tap into the equity you've built up in your home to get the funds you need.

- You're drowning in high-interest debt. Juggling multiple credit card bills or personal loans can be stressful and expensive. A cash-out refi can be a smart way to pay off that high-interest debt and roll it all into one, manageable mortgage payment—often at a much lower rate.

- You want to switch loan types. If you have an Adjustable-Rate Mortgage (ARM) and are worried about future rate hikes, refinancing into a stable fixed-rate loan can give you peace of mind. On the flip side, if you know you'll be moving in a few years, switching to an ARM could save you money in the short term.

Personal Financial Considerations

Market rates are important, but what matters most is your own financial picture. Before you even fill out an application, you need to be brutally honest about your finances and where you're headed.

A refinance only makes sense if it genuinely improves your financial health. You have to look past the shiny new monthly payment and really dig into the total cost, figure out your break-even point, and make sure the new loan fits your five- or ten-year plan.

Ask yourself the tough questions. How long are you really planning to stay in this house? If you think you might sell in a couple of years, the closing costs on the refi could completely wipe out any savings you’d make. Also, get clear on your goals. Is the main objective to become debt-free as fast as possible, or do you just need more breathing room in your budget each month? Your answer will point you toward the right type of refinance.

Exploring Your Refinance Options: More Than One Way to Save

When homeowners ask me how to refinance, the first thing I tell them is that it’s not a one-size-fits-all product. Think of it like a toolbox—you’ve got different tools for different jobs. Your job is to pick the right one for your specific financial goal, whether that’s cutting your monthly payment, pulling out cash for a big project, or just simplifying your loan.

Picking the wrong tool can be a costly mistake. You might leave money on the table or, worse, put yourself in a tougher financial spot. Let's walk through the three most common paths so you can see which one makes the most sense for you.

Rate-and-Term Refinance: The Classic Money-Saver

This is what most people think of when they hear "refinance." It’s straightforward: you’re swapping your current mortgage for a new one with better terms. That usually means a lower interest rate, a shorter loan term, or both. You’re not borrowing extra cash; you’re simply restructuring the debt you already have to make it work better for you.

For example, I recently worked with a client, Sarah, who bought her house a few years back with a 6.5% interest rate on a $400,000 loan. With rates dropping into the low fives, we ran the numbers on a rate-and-term refi. By securing a 5.25% rate, she was able to slash her monthly principal and interest payment by hundreds of dollars. It was a no-brainer.

This is probably your best bet if:

- Interest rates are lower now than when you first got your loan.

- Your credit score has jumped up, making you eligible for better rates.

- You want to get out of an Adjustable-Rate Mortgage (ARM) and lock in a predictable fixed rate.

- You’re ready to pay your home off faster and can handle the higher payment of a 15-year term instead of a 30-year.

Cash-Out Refinance: Turning Home Equity into Opportunity

If you’ve been paying down your mortgage for a while and your home's value has gone up, you've built equity. A cash-out refinance lets you tap into that value. You take out a new, larger mortgage that pays off your old one, and you get the difference in a lump-sum check. It's a powerful way to turn your home's value into liquid cash.

Take the Miller family, who I helped last year. Their home was worth $450,000, and they owed $250,000. They needed $60,000 to cover their daughter’s college tuition and wipe out some high-interest credit card debt. We set them up with a new $310,000 loan. It paid off the original mortgage, and they walked away with $60,000 in cash. Their new loan balance was higher, but they consolidated everything into a single, manageable mortgage payment at a much lower interest rate than their credit cards.

A cash-out refinance can be a game-changer for big financial goals, but remember, you are increasing your mortgage debt. You have to go into it with a clear, disciplined plan for how you'll use the funds.

Streamline Refinance: The Fast-Track for Government-Backed Loans

Have an FHA, VA, or USDA loan? You might qualify for a "streamline" refinance. These are designed to be much faster and require a lot less paperwork than a traditional refi. The big plus? They often don’t require a new appraisal, which saves you a good chunk of time and money.

A perfect example is the VA Interest Rate Reduction Refinance Loan (IRRRL), which I do for veterans all the time. As long as we can show that the new loan provides a "tangible benefit"—like a lower monthly payment—the process is incredibly simple.

This kind of accessibility is a big reason why refinancing has become so common. The global refinance market hit USD 22.82 billion in 2025 and is expected to grow at 8.8% a year through 2034. As technology makes it easier for homeowners to see their options, more people are taking advantage of these opportunities. You can dig deeper into these global refinance market trends and projections to see just how much the industry is evolving.

Which Refinance Type Is Right for You?

Choosing between these options comes down to what you're trying to achieve. Each one serves a different purpose, so matching your goal to the right product is the most important step in the process.

This table breaks it down to help you see which path aligns with your financial goals.

| Refinance Type | Primary Goal | Best For… | Key Consideration |

|---|---|---|---|

| Rate-and-Term | Lower monthly payments and/or total interest paid. | Homeowners whose primary focus is saving money on their existing mortgage debt. | The savings from the lower rate should outweigh the closing costs. |

| Cash-Out | Accessing home equity as a lump-sum of cash. | Funding large expenses like home renovations, debt consolidation, or education. | You are increasing your total mortgage balance and paying interest on the cash you take out. |

| Streamline | A faster, lower-cost refinance process. | Borrowers with existing FHA, VA, or USDA loans looking for a simple rate reduction. | Limited to government-backed loans and typically doesn't allow for cash out. |

Ultimately, the best choice depends entirely on your personal circumstances—your current loan, your financial health, and what you hope to accomplish. Let’s figure it out together.

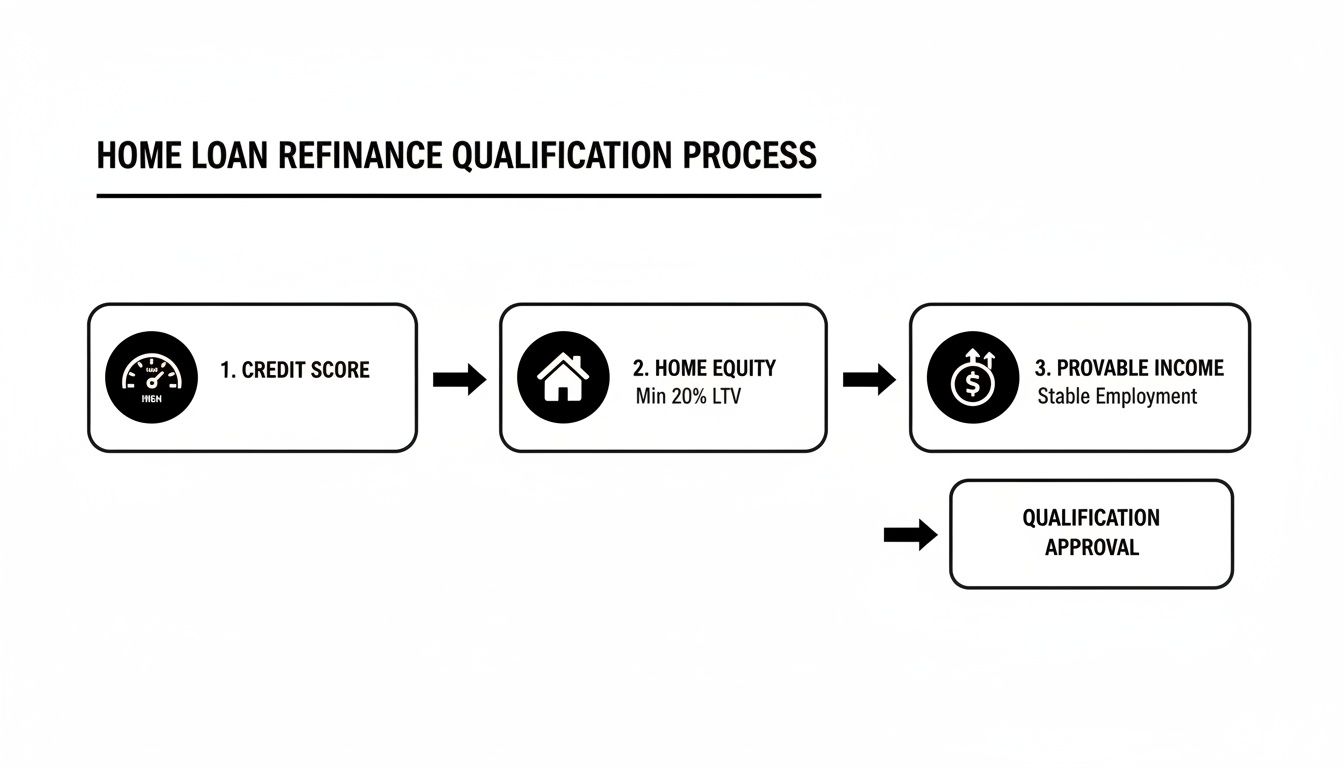

Qualifying for a Refinance: What Lenders Look For

When you're thinking about refinancing, the real question is, "What do I need to get approved?" Lenders aren't looking for a perfect financial picture, but they do need to see a stable and reliable borrower. If you can understand what they're looking for, you can put together a strong application that sails right through.

Think of it like telling a financial story. A lender is reading that story to see if you're a good risk. The main chapters they focus on are your credit score, your home equity, your income, and your overall debt. Let's break down how to get each part of your story in great shape.

The Power of Your Credit Score

Your credit score is the first thing a lender checks, and honestly, it carries a lot of weight. It’s their quickest snapshot of how you’ve managed debt in the past, which they see as the best predictor of how you’ll handle your new mortgage.

You might be able to get a refinance with a score in the low 600s, but the best deals—the lowest interest rates and most favorable terms—are always reserved for those with higher scores. We've seen firsthand that improving your credit score can save you thousands over the life of the loan.

- Good (670-739): You're in a solid position to qualify and should see some competitive rates.

- Excellent (740+): This is the magic number. A score this high opens the door to the absolute best rates and terms a lender can offer.

If your score isn't quite there yet, don't sweat it. Simple things like consistently paying bills on time, chipping away at credit card balances, and holding off on any new credit applications can make a real difference. For a deeper look, our guide on how to improve your credit for a mortgage has some great, actionable tips.

Understanding Your Home Equity and LTV

Before a lender signs off, they need to know exactly how much of your home you actually own. That's your home equity—the difference between your home's current market value and what you still owe on your mortgage. Lenders measure this using a metric called Loan-to-Value (LTV).

For a standard rate-and-term refinance, most lenders want your LTV to be 80% or lower. In plain English, that means you need at least 20% equity. If you're looking to pull cash out, the bar is often set a bit higher, since the lender is taking on more risk by handing you cash.

Calculating Your LTV Is Simple:

(Current Mortgage Balance / Current Appraised Value) x 100 = LTV

For example, if you owe $300,000 on a home now worth $400,000, your LTV is a healthy 75%.

Your Debt-to-Income Ratio Matters

Don't let the name intimidate you. Your Debt-to-Income (DTI) ratio is just a simple percentage that tells lenders how much of your monthly income is already spoken for by other debts. It’s a crucial number because it shows them if you can comfortably afford another payment.

To figure out your DTI, just add up all your monthly debt payments—things like your mortgage, car loans, student loans, and minimum credit card payments. Then, divide that total by your gross monthly income (your income before taxes). Ideally, lenders want to see a DTI of 43% or less. Some programs might be a bit more flexible, especially if you have a high credit score or a lot of cash in savings.

Proving Stable and Sufficient Income

Finally, a lender needs proof that you have a steady income to cover the new mortgage payment. It’s not just about the amount you make, but also the consistency. You'll typically need to document your employment for the last two years.

Here’s a quick rundown of the documents you’ll probably need to gather:

- W-2 Employees: Your last 30 days of pay stubs, W-2 forms from the past two years, and your most recent bank statements.

- Self-Employed Borrowers: Two years of both personal and business tax returns, a year-to-date profit and loss (P&L) statement, and a few months of business bank statements.

Being prepared is everything, especially when interest rates start to move. For instance, when rates dipped in the second quarter of 2025, refinance applications shot up by a staggering 43% year-over-year. That activity was a huge driver in the market, with refinance securitizations jumping 63%. Having your paperwork ready to go means you can jump on opportunities like that the moment they appear.

Your Refinance Journey: From Application to Closing

So, you've decided to move forward with a refinance. That's a big step, but what actually happens next? For many homeowners, the process from application to signing the final papers can feel like a bit of a black box. My goal here is to pull back the curtain and show you exactly what to expect at every stage.

This flowchart gives you a great high-level view of what lenders are really looking at.

As you can see, it all boils down to a few key pillars: your credit, your home's equity, and your income. These pieces fit together to give the lender a clear picture of your financial health, which is what they use to approve your new loan.

The Initial Application

First things first, we gather your information. You'll fill out the official loan application, which asks for all the standard details—personal info, job history, what you own, and what you owe. It’s thorough, but a little prep work makes it a breeze.

My advice? Get your financial documents together before you even start. Having everything organized in one folder saves a ton of time and back-and-forth later.

To make it easy, you can download our complete refinance document checklist to see exactly what you’ll need. Walking in with all your paperwork ready to go shows the lender you're serious and organized.

Loan Processing and Underwriting

Once you submit your application, it lands with a loan processor. Their job is to review the file, make sure all the necessary documents are there, and check for accuracy. They might reach out for a more recent bank statement or ask for a quick letter explaining a large deposit. It's all part of dotting the i's and crossing the t's.

From there, your file goes to the underwriter. This is the make-or-break stage. Think of the underwriter as the lender's detective; they verify every single detail to make the final call on your loan. They’ll comb through your credit report, confirm your income, analyze your DTI ratio, and ensure everything lines up with their guidelines.

Expert Tip: Once you're in underwriting, try to keep your financial life as quiet as possible. Don't open a new credit card, finance a car, or change jobs. Any of these moves can alter your financial profile at the last minute and put your approval at risk.

The Home Appraisal

Unless you're doing a specific type of loan like a streamline refinance that might not require one, the lender will order an appraisal. A licensed, third-party appraiser will come out to your property to determine its current market value.

What are they looking for? It comes down to a few key things:

- Recent Comparable Sales: What have similar homes in your neighborhood sold for recently?

- Home Condition: They'll assess the overall shape of your home, noting any updates or repairs.

- Location and Features: Desirable neighborhoods, square footage, and unique features all play a part in the final value.

This appraisal number is crucial. It has to be high enough to support the new loan amount and meet the lender's loan-to-value (LTV) rules. A low appraisal can be a hurdle, but it doesn't always mean the deal is dead.

Final Approval and Closing Day

When the underwriter has given the final stamp of approval and signed off on the appraisal, you'll get the green light: a "clear to close." This means all conditions are met, and the lender is ready to fund your new loan.

You’ll then receive your Closing Disclosure (CD) at least three business days before closing. This document is incredibly important. It breaks down all the final numbers—your loan amount, interest rate, monthly payment, and total closing costs. You need to review it carefully and compare it to the Loan Estimate you got at the beginning to make sure everything looks right.

Closing day is the finish line. You'll sit down with a closing agent or attorney to sign the final loan documents. Once the ink is dry and the funds have been sent to pay off your old loan, your refinance is officially complete. You’ve successfully navigated the process and secured a better mortgage.

Crunching the Numbers: What Does Refinancing Really Cost?

Figuring out if a refinance makes sense goes way beyond just snagging a lower interest rate. You have to ask a tougher question: will the long-term savings actually cover the upfront costs of getting the new loan? If not, you could end up losing money.

This is where we get into the nitty-gritty of the numbers.

Before you start picturing all the money you’ll save, you have to face the costs. Refinancing isn't free. You'll have closing costs, which are the fees you pay to finalize the new loan, typically running between 2% to 5% of the total loan amount. Getting a handle on these expenses is the first real step.

What’s Included in Refinance Closing Costs?

Closing costs can seem like a confusing jumble of fees, but they all pay for essential services required to set up your new mortgage. While the specific charges can differ depending on your lender and state, some common ones pop up on nearly every loan estimate.

To give you a clearer idea, we've broken down some of the most common fees you'll likely encounter during a refinance. These are the third-party and lender charges that make up your total closing cost figure.

Sample Refinance Closing Costs

| Fee Type | Description | Estimated Cost Range |

|---|---|---|

| Lender Origination Fee | The lender's fee for processing, underwriting, and funding your loan. | 0.5% – 1% of the loan amount |

| Appraisal Fee | Pays a licensed appraiser to confirm your home's current market value. | $400 – $700+ |

| Title Insurance & Search | Protects you and the lender from past claims or liens on the property. | $1,000 – $2,500+ |

| Credit Report Fee | A small fee for the lender to pull your credit history and scores. | $30 – $60 |

| Recording Fees | Paid to your county government to officially record the new mortgage lien. | $125 – $250+ |

Getting a detailed Loan Estimate from any potential lender is absolutely essential. It’s the only way to compare apples to apples and see who is truly offering you the best deal.

Your break-even point is the single most important calculation in a refinance. It tells you, in simple terms, the exact month when your savings officially start. If you plan to sell before you hit that point, the refinance might not be worth it.

How to Calculate Your Refinance Break-Even Point

Once you have a solid estimate of your total closing costs and you know your new, lower monthly payment, finding your break-even point is surprisingly easy. This calculation tells you precisely how many months it will take for your monthly savings to completely pay off the upfront costs.

The formula is as simple as it gets:

Total Closing Costs / Monthly Savings = Your Break-Even Point (in months)

Let's walk through a quick example. Say your total closing costs come out to $5,000. Your new refinanced mortgage saves you $250 every month compared to your old one.

Here’s the math:

$5,000 (costs) ÷ $250 (savings) = 20 months

In this scenario, it will take you 20 months to recoup the money you spent on closing costs. From month 21 onward, that $250 is pure savings in your pocket. This is critical if you're not sure how long you'll stay in the home. If your break-even is three years out but you might sell in two, refinancing would be a financial mistake.

Feel free to play around with your own numbers using our free mortgage calculators. It’s a great way to get a personalized look at your potential savings and break-even timeline.

Common Questions About Refinancing a Home

Even when you feel you've got a good handle on the process, a few nagging questions tend to surface right as you're about to pull the trigger. Getting these last-minute uncertainties cleared up can give you the confidence to move forward.

Let's tackle some of the most common concerns I hear from homeowners just like you.

One of the biggest worries is always about credit. Yes, applying for a refinance does trigger a "hard" credit inquiry, which might temporarily knock your score down by a few points. But think of it this way: that small, temporary dip is often a tiny price to pay for the long-term win of a lower monthly payment and improved cash flow.

What Is the Typical Refinance Timeline?

From the moment you apply to the day you sign the final papers, you can generally expect the refinance process to take 30 to 45 days.

Of course, that’s just a ballpark. A few things can speed things up or slow them down:

- The Appraisal: Getting an appraiser out to your property can take time, especially in a hot market. Scheduling alone can sometimes add a week or two.

- Your Financial Picture: If you're self-employed or have a more complex income situation, the underwriter will need more time to review your file. It’s totally normal.

- Title Search Surprises: Every now and then, a title search digs up an old, forgotten lien or a clerical error that needs to be sorted out before closing.

Being organized with your documents is the best way to keep things moving on your end.

Can I Refinance With Less-Than-Perfect Credit?

Absolutely. While a higher credit score will always get you the most competitive rates, having less-than-perfect credit doesn't automatically disqualify you. Your options might just look a little different.

Lenders see a lower score as higher risk, which usually translates to a higher interest rate.

The key is to show strength in other areas of your financial life. If you can demonstrate a stable income, a healthy debt-to-income ratio, and a good amount of equity in your home, lenders are often more willing to work with you.

If your score is on the bubble, it might be smart to spend a few months improving it before you apply. A small bump in your score could unlock a much better rate, saving you a significant amount of money over the years. For more perspectives, you can find additional financial insights that might help.

Ultimately, every borrower's situation is unique. The best first step is always to have a straightforward conversation with a mortgage professional who can look at your specific numbers and lay out your real-world options.

Ready to explore your options and see if a refinance is the right move for you? The team at Mortgage Seven LLC is here to provide clear, personalized guidance without the pressure. Schedule your no-obligation consultation today. https://mtg7.com