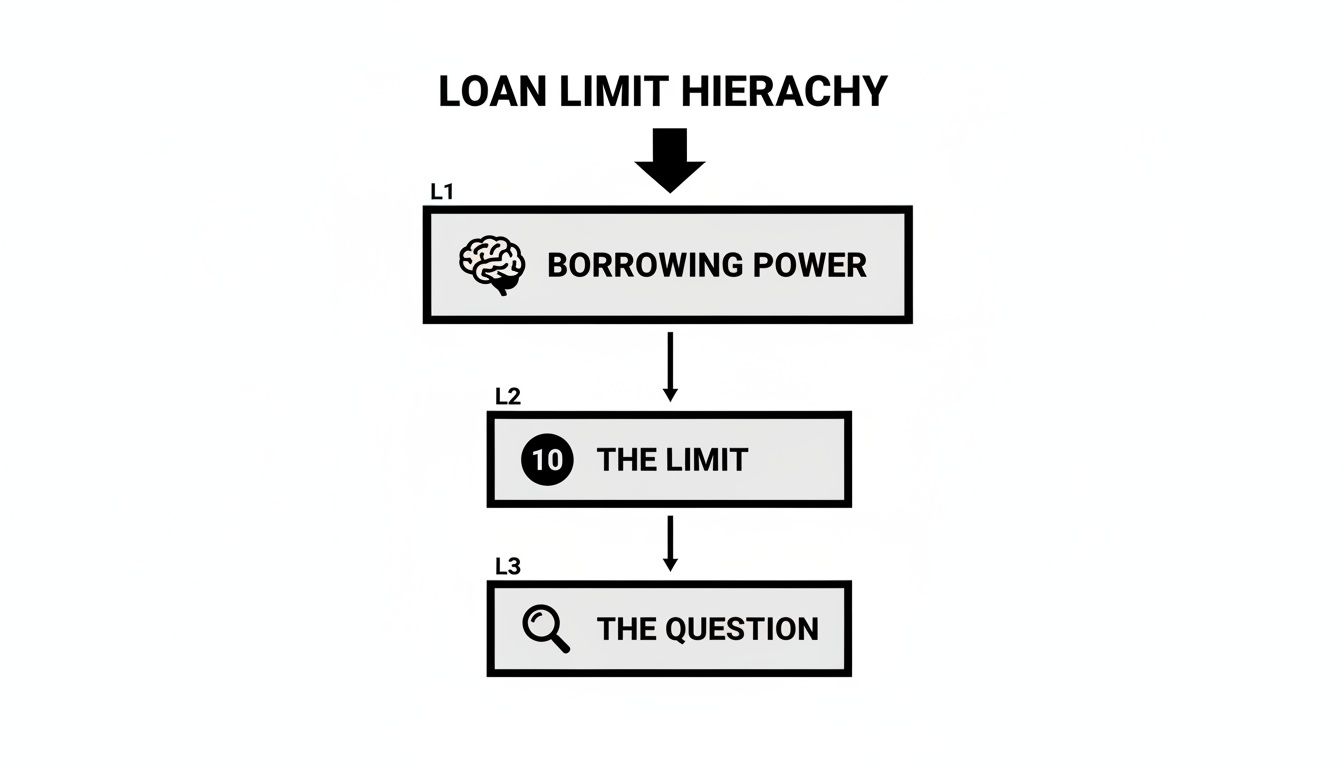

So, how many mortgages can you actually have? For most people using conventional financing, the magic number is ten. That includes your own home plus up to nine other financed properties.

But let's be honest, that's just the simple answer.

The Real Answer is More Than Just a Number

While everyone talks about the ten-property limit, that figure only tells part of the story. The real question isn't about hitting a hard cap. It's about proving to a lender that you can responsibly handle the financial weight of each new property you add to your portfolio.

Think of it like leveling up in a game. Each new mortgage you take on is a new level, and it demands you be stronger, better prepared, and more financially disciplined than the last. This guide is your roadmap for navigating that journey, moving you beyond a simple property count to understand what really drives your borrowing power.

What Lenders Really Care About

At the end of the day, a lender's job is all about managing risk. When you walk in asking for your second, fifth, or even tenth mortgage, they're looking at your application with an increasingly powerful microscope. Your chances of getting that "yes" boil down to three things:

- Your Ability to Repay: Can you prove that another monthly payment won't sink your ship? This means showing strong, consistent income and a rock-solid history of paying your bills on time.

- Your Financial Track Record: Your credit score is your financial report card. As you acquire more properties, a high score isn't just nice to have—it's non-negotiable. It signals to lenders that you're a safe bet.

- Your Cash Safety Net: Do you have enough cash set aside to cover the unexpected? Lenders need to see that you can handle vacancies, surprise repairs, or a slow month across your entire portfolio without breaking a sweat.

The journey from one property to ten isn't just about collecting addresses; it's about proving you're a master of financial management. Your goal is to make each loan application an undeniable 'yes' for the lender.

Once you have these fundamentals down, you can build an airtight case for each new loan. The specific rules change depending on the type of loan you're using, which can make a huge difference in how quickly you can scale.

Mortgage Program Limits at a Glance

Here’s a quick look at how different loan programs view property limits. This sets the stage for the specific strategies we'll dive into next.

| Loan Program | Maximum Financed Properties | Primary Use Case |

|---|---|---|

| Conventional (Fannie Mae) | 10 Properties | Primary Residence & Investment |

| FHA Loan | 1 Property (with exceptions) | Primary Residence |

| VA Loan | 2 Properties (residence focus) | Primary Residence |

| Portfolio & DSCR Loans | No Firm Limit | Investment & Scaling |

As you can see, the path you choose will dictate the rules you play by. While government-backed loans are great for homeowners, investors quickly find themselves needing more flexible options to grow their portfolios.

The Road to 10 Properties With Conventional Loans

If you're looking to build a real estate portfolio, conventional loans are the place most investors start. These are the workhorses of the mortgage world, backed by giants like Fannie Mae and Freddie Mac. This is where you'll run into the well-known 10-property limit—a clear, yet challenging, goal for any serious investor.

But getting from property number one to property number ten isn't a straight shot. The rules of the game change dramatically as your portfolio expands.

Think of it as climbing a mountain in two stages. The first leg of the journey, covering your first four financed properties, is the accessible part of the trail. Lenders are generally pretty accommodating if you have solid credit, a stable income, and a decent down payment. This is where you build your reputation as a reliable borrower and landlord.

The real climb begins when you go for your fifth mortgage. From that point on, lenders are looking at you through a much more powerful microscope. They aren't just financing a house anymore; they're underwriting a small real estate business. And their standards reflect that heightened risk.

The Easy Part: Mortgages One Through Four

Getting your first few investment properties is meant to be achievable. The process feels a lot like buying your own home, and lenders are mostly focused on standard qualifications. The bar isn't set impossibly high.

During this initial phase, lenders just want to see the basics:

- Good Credit: A strong credit score is your ticket to the game.

- Proof of Income: You have to show you can handle your current debts plus the new mortgage.

- A Solid Down Payment: For an investment property, expect to put down 15-25%.

The Big Leap: Mortgages Five Through Ten

Once you're aiming for property number five, everything changes. Lenders now demand a much higher level of financial strength and proven experience. This is the wall many aspiring investors hit because they aren't prepared for just how much the requirements ramp up. The lender's thinking is simple: more properties equal more complexity and more things that could potentially go wrong.

This is the point where lenders shift from evaluating you as an individual borrower to scrutinizing you as a professional operator.

As the visual shows, the limit might be ten, but the real question is whether you can prove you have the financial muscle to handle the risk at each new level.

Fannie Mae, a key player in the conventional market, draws a hard line. To get your seventh loan (and beyond), you'll need a minimum credit score of 720. Down payments also get steeper, often requiring at least 25% for multi-unit properties. But the biggest hurdle for most is the cash reserve requirement.

The Reserve Rule: For properties five through ten, lenders demand you have six months of PITI (principal, interest, taxes, and insurance) reserves in the bank for every single property you finance. Not just the new one—all of them.

Let's break that down. Say you own six properties, and the PITI on each is $1,500 a month. To qualify for your seventh loan, you'd need to show $54,000 in liquid cash reserves ($1,500 x 6 properties x 6 months). This is often the single biggest barrier to scaling, and it catches many investors by surprise. Planning for this cash cushion is absolutely critical if you're serious about hitting the 10-property mark.

Beyond the Basics: Government-Backed and Portfolio Loans

While conventional loans are the workhorse for building a real estate portfolio, they aren't the only tool in the shed. Once you get to ten properties, you’ve hit the conventional limit. So, what’s next?

To really grasp how many mortgages you can truly have, you need to look beyond the standard path. This is where specialized loan types, like government-backed and portfolio loans, come into play. Each one has its own rulebook, and understanding them can either open up new doors or show you where the walls are.

Why Government-Backed Loans Aren't for Empire Building

For a first-time homebuyer, a government-backed loan can feel like a godsend. But for a real estate investor? They're more of a one-and-done deal.

Programs like FHA and VA loans were created to get people into homes they'll actually live in, not to help investors build rental dynasties. That's a crucial distinction. Because of this laser focus on owner-occupancy, they come with some pretty firm guardrails that stop investors in their tracks.

Compared to conventional financing, the limits are tight. The Federal Housing Administration (FHA) typically only allows you to have one FHA loan at a time. The Department of Veterans Affairs (VA) is a bit more flexible, allowing for up to two, but there's a catch: the new property has to be your primary residence, not another rental.

This makes them fantastic for buying your first or even second home, but it's a hard stop for portfolio growth. Once you've used up your FHA loan or your VA loan for your own home, that particular avenue is closed for future investments.

Breaking the 10-Loan Barrier with Portfolio Loans

So, you've hit the ten-property limit with conventional loans. Now what? This is the exact moment when savvy investors turn to portfolio loans.

Unlike conventional loans, which are packaged up and sold to giants like Fannie Mae and Freddie Mac, portfolio loans are kept on the lender's own books—in their "portfolio."

That one simple difference changes the entire game.

Since the lender is keeping the loan in-house, they don't have to follow the rigid, one-size-fits-all rules of the secondary market. They can look at your entire financial story and make a common-sense business decision based on your success as an investor.

This opens up a world of possibilities for serious real estate pros:

- No Hard Property Limit: Forget the 10-property cap. These lenders are far more interested in the cash flow and health of your entire portfolio.

- Creative Underwriting: They look beyond your W-2. A portfolio lender will analyze the income from your rentals, your experience as a landlord, and your overall net worth.

- Relationship-Based Lending: You'll often find these loans at smaller community banks or private lenders who get to know you and want to build a long-term partnership with a successful investor.

With a portfolio lender, you're not just another application—you're a potential business partner. They're sizing you up, looking at how well you manage your properties and generate returns. If they like what they see, they’re often willing to finance deals that a conventional lender wouldn't even touch.

Many of these loans fall into the category of non-qualified mortgages. You can learn more about non-QM loan options here to see just how flexible they can be.

At the end of the day, government loans serve a specific purpose, but they have their limits. Portfolio loans are the key to the next level of growth, unlocking the door for proven investors ready to scale their real estate business beyond the conventional boundaries.

The Four Pillars of Mortgage Qualification

Forget the specific loan program rules for a moment. At its core, a lender's decision boils down to one simple question: Can we trust you with our money? To figure that out, they scrutinize your financial life through the lens of four critical pillars.

Think of it like a table. If one leg is weak, the whole thing gets shaky. As you start stacking more mortgages onto that table, any wobble becomes a serious risk. Getting a handle on these four areas is absolutely essential if you want to get approved for your next loan—and the one after that.

Pillar 1: Debt-to-Income Ratio

The very first metric any underwriter looks at is your Debt-to-Income (DTI) ratio. It's a straightforward comparison of your total monthly debt payments—including the new mortgage you’re applying for—against your gross monthly income. Every time you add a property, that ratio naturally climbs.

Now, there's some good news. You can use the rental income from your properties to help offset the new mortgage payment. But here's the catch: lenders won't count all of it. They typically only consider about 75% of the gross rent to build in a cushion for vacancies and repairs. So, while rental income is a huge help, DTI management becomes a constant balancing act for investors.

Pillar 2: Credit Score

Your credit score is your financial report card, and it's non-negotiable. It's the cleanest, quickest way for a lender to gauge your reliability. As we've covered, the bar gets higher as your portfolio grows. For investors holding several properties, lenders often want to see a FICO score of 720 or higher.

A strong score shows a long, consistent history of paying your bills on time, which tells lenders you're a low-risk borrower. Without it, the other pillars just can't hold up your application. The nitty-gritty of how banks decide on loan qualification always comes back to your credit history being a major factor.

A lender's view is simple: The more mortgages you have, the more opportunities there are for a late payment. A pristine credit history is your best proof that you can handle the complexity.

Pillar 3: Cash Reserves

This is the pillar that trips up most aspiring investors. Cash reserves are the liquid funds you have sitting in the bank after you’ve paid your down payment and closing costs. Lenders need to see this safety net. It gives them confidence that you can cover all your mortgage payments if a tenant moves out or a furnace unexpectedly dies.

The reserve requirements get significantly tougher as you scale:

- For 1-4 Properties: Lenders might just want to see a few months' worth of the new property's PITI (Principal, Interest, Taxes, and Insurance).

- For 5-10 Properties: The requirement typically jumps to six months of PITI for every single financed property you own, not just the new one.

And this has to be real, accessible cash—not money tied up in a 401(k) or other hard-to-reach investments.

Pillar 4: Landlord Experience

Finally, once you've been in the game for a while, your track record becomes a powerful asset. This pillar isn't about a single number, but about proving you know what you're doing. Lenders want to see that you can effectively manage properties, screen tenants, and handle the business side of being a landlord.

A documented history of successful property management, usually found on your tax returns (Schedule E), goes a long way. It proves you're not just a borrower; you're a professional operator who understands the risks and rewards. That makes you a much more compelling applicant in the eyes of an underwriter.

Financing Strategies to Grow Beyond Ten Properties

Hitting the ten-property limit with conventional loans isn't the end of the road. Far from it. Think of it as a graduation. You’ve successfully navigated the world of traditional financing, and now you’re ready to step up to the more powerful, specialized tools designed for serious investors.

This is where your strategy has to evolve. You're not just collecting properties anymore; you're building a scalable business. The loans that will take you to your 11th property and beyond operate on a different wavelength, focusing less on your personal W-2 and more on the performance of your assets. It’s a crucial shift in mindset that opens the door to massive growth.

Embrace the Power of DSCR Loans

For most investors looking to scale, the single most important tool is the Debt Service Coverage Ratio (DSCR) loan. This loan completely flips the script on how you qualify for a mortgage. Instead of obsessing over your personal debt-to-income ratio, lenders ask one simple question: does the property’s rent cover its own mortgage payment?

The DSCR is calculated by dividing the property’s gross rental income by its total housing expense (principal, interest, taxes, and insurance—or PITI). Most lenders want to see a ratio of 1.25 or higher, which simply means the rent collected is 25% more than the total mortgage payment.

This is a total game-changer. Suddenly, your personal salary becomes a minor detail. The property qualifies on its own merits, allowing you to acquire new assets based on their cash flow, not your paycheck.

This approach lets you scale at a pace you never could before. As long as you can find deals that make sense and cash flow properly, there’s no hard limit to how many mortgages you can stack up. You can dig into a variety of these specialized investment property financing options to see what works best for your portfolio.

Consider Blanket and Commercial Mortgages

As your portfolio grows, trying to manage a dozen separate loans can feel like herding cats. This is where a couple of other advanced strategies come into play to help you consolidate and keep expanding.

-

Blanket Mortgages: Imagine one single loan that covers multiple properties at once. Instead of juggling ten different payments, you have one. This not only simplifies your life but can also be used to free up your ten conventional loan "slots." By refinancing existing properties under a new blanket loan, you can effectively reset your count and go back to using conventional financing if you want.

-

Commercial Loans: If your strategy is shifting toward larger multi-family buildings (think five units or more), you’ll naturally move into the world of commercial lending. These loans are underwritten based on the property’s Net Operating Income (NOI) and its value as a commercial asset. The focus is entirely on the business of the building, making your personal finances secondary.

By mixing and matching these strategies, that ten-loan limit stops being a barrier and becomes just another milestone in your rearview mirror. The key at this stage is to partner with a mortgage broker who lives and breathes investor financing. They have the connections to the private lenders and community banks that offer these products, helping you build a financial machine that can support a real estate empire.

Managing the True Cost of a Large Portfolio

Getting the loan is just the first hurdle. While it’s tempting to celebrate adding another property to your name, the real secret to long-term success isn't just buying more doors—it's managing them effectively. The hard work truly begins once the ink on the closing documents is dry.

Suddenly, the question "how many mortgages can you have?" becomes less about finance and more about administration. Each new loan adds another layer of complexity. You're no longer tracking one PITI payment; you're juggling a dozen, each with a different due date, a separate lender portal, and its own escrow account.

This administrative burden can snowball faster than you think. Every loan generates its own 1098 tax statement that you have to chase down and organize. For investors with five or ten properties, this kind of overhead almost always requires hiring professional help, which eats directly into your returns.

The Financial Strain Beyond the Monthly Payment

Beyond the bookkeeping, a bigger portfolio means bigger risks. A single vacancy in one property is an annoyance. But what happens when you have simultaneous vacancies in three of your properties? That’s a potential cash flow crisis.

The same goes for maintenance. One broken water heater is a manageable expense. But imagine getting calls about three major appliance failures in the same month. This is where your cash reserves stop being a lender requirement and become your operational lifeline. Without a serious financial cushion, you'll be forced to make bad decisions under pressure, like renting to a less-than-ideal tenant just to stop the bleeding.

A successful real estate portfolio is run like a business, not a hobby. It demands airtight organization, proactive financial planning, and a clear understanding of your true profitability on every single door.

Measuring Your Portfolio's Health

To stay on top of it all, you have to treat your portfolio like a living, breathing business that needs constant monitoring. This means looking past simple rent collection and tracking key performance indicators (KPIs) to truly understand its financial health.

These are the essential metrics every serious investor should live by:

- Cash Flow per Unit: The actual profit each property puts in your pocket after every single expense is paid.

- Vacancy Rate: The percentage of time your units sit empty, which is a direct drain on your revenue.

- Return on Investment (ROI): The ultimate measure of how hard your invested capital is working for you.

- Capitalization Rate (Cap Rate): This metric gives you a snapshot of a property's potential return based on its income.

Getting a firm grip on calculating cap rate is crucial for accurately assessing profitability and making smart decisions. Mastering these numbers is what separates a passive property owner from a strategic investor—someone who can spot underperforming assets and protect their bottom line. It’s this disciplined, business-minded approach that will allow you to not just sustain your portfolio, but grow it.

Common Questions About Juggling Multiple Mortgages

When you start growing a real estate portfolio, you'll find the same questions pop up again and again. It can feel like you're trying to navigate a maze of rules, but getting straight answers is the only way to plan your next move with any real confidence. Let's tackle some of the most common questions investors have.

Does My Primary Home Count Toward the 10 Mortgage Limit?

Yes, it sure does. Lenders count the total number of properties you have financed, and your primary residence is always first in line. This is a small detail that trips up a lot of new investors.

Think of it this way: when you own your home and then go to buy your first rental, you’re actually applying for your second mortgage. In the lender's system, you aren't starting from scratch. Factoring in your own home from day one is crucial for building a realistic, long-term investment plan.

Can a Married Couple Each Get 10 Mortgages?

This is definitely a pro-level strategy, but it’s possible. If a married couple applies for mortgages together, they're seen as one borrower and share the same 10-loan limit. Any loan they get jointly counts against both of them.

But here’s the workaround: if each spouse can qualify for a mortgage entirely on their own—using their individual income, credit, and assets—then each of them could get up to ten conventional loans. This means a couple could potentially finance up to 20 properties, but it takes serious financial planning and the right guidance to pull off correctly.

The key is individual qualification. If you can stand on your own two feet financially for each application, you can maintain your own separate 10-loan count. It's a powerful way to scale, but it's not simple.

What Happens if I Pay Off a Mortgage?

Good news here. Paying off a mortgage instantly frees up one of your slots. The Fannie Mae rule is about the number of properties you currently have financed, not how many you’ve owned in your lifetime.

So, if you’re at your limit with ten mortgages and you sell one of the properties (or just pay off the loan), you’re immediately back down to nine financed properties. That opens up a spot, letting you apply for another conventional loan to buy a new property and get back up to the ten-loan max.

When Should I Talk to a Mortgage Broker?

It's never too soon to start a conversation, but you absolutely need an experienced mortgage broker in your corner once you're planning to own more than two or three properties. Not just any broker will do—you need someone who lives and breathes investment property financing.

They can help you prepare for the much tougher underwriting you'll face on loans five through ten. More importantly, they'll know which lenders are actually investor-friendly and can introduce you to powerful tools like DSCR loans when you're ready to grow beyond conventional limits. A great broker doesn't just find you a loan; they help you build a financing strategy for your entire portfolio.

Navigating the complexities of investment property financing requires a knowledgeable partner. At Mortgage Seven LLC, we specialize in helping investors find the right loan products to achieve their portfolio goals, from conventional financing to advanced DSCR and portfolio loans. To explore your options and create a clear path forward, schedule a consultation with our expert team today.