Let's be honest, the biggest myth in real estate is that you absolutely have to put 20% down to get a conventional loan. It's a persistent piece of advice, but the reality is much more flexible and, for many people, much more encouraging.

The truth is, for a lot of qualified buyers—especially first-time homebuyers—the door to homeownership can open with as little as 3% down. This single fact makes buying a home a real possibility for millions of people who thought it was years away.

The Real Answer to Your Down Payment Question

So, let's cut right to it. The idea that a 20% down payment is mandatory is simply outdated. While a larger down payment certainly comes with perks (like a lower monthly payment and no mortgage insurance), it is absolutely not a dealbreaker for getting a conventional loan.

The actual amount you'll need is tied to your financial picture, the kind of property you're buying, and the specific loan program that fits you best. This flexibility is a complete game-changer. Instead of watching home prices rise while you spend years saving, you might be able to get into the market much sooner than you think. It's all about knowing the rules of the game.

Minimums Vary by Scenario

Your down payment isn't some fixed, one-size-fits-all number. Lenders look at the whole picture to figure out the minimum they’re comfortable with. For instance, buying a home you plan to live in as your primary residence is viewed very differently than buying an investment property, and the down payment reflects that.

On top of that, there are fantastic loan programs from Fannie Mae and Freddie Mac designed specifically to make homeownership more accessible. These often cater to first-time buyers or those with moderate incomes, featuring down payments as low as 3-5%.

This means your path to buying a home is unique to you. A solid credit score and a handle on your debt can unlock these low-down-payment options, giving you way more financial breathing room.

Minimum Conventional Loan Down Payments at a Glance

To make this crystal clear, let's break down the typical minimums you can expect for different conventional loan situations. This table gives you a quick snapshot of what to anticipate.

| Borrower / Property Type | Minimum Down Payment | Key Considerations |

|---|---|---|

| First-Time Homebuyer | 3% | Often requires homebuyer education and may have income limits. |

| Repeat Homebuyer (Primary) | 5% | This is the standard for a single-family home you'll live in. |

| Second Home / Vacation Home | 10% | Lenders see this as a slightly higher risk, so more is needed upfront. |

| Multi-Unit Investment Property | 15-25% | Because it's a business venture, it requires a larger investment. |

As you can see, what you plan to do with the property really drives the down payment requirement. And don't just take our word for it—the data backs this up. A report from the National Association of Realtors found that nearly 70% of conventional loan borrowers put down less than 25%, with 29% putting down 10% or less. You can dig into more of these fascinating home buying trends on nar.realtor.

The question isn’t just "how much do I need?" but "what's the smartest down payment for my financial goals?" A smaller down payment gets you into a home faster, allowing you to start building equity, while a larger one lowers your monthly payment.

Navigating all these options can feel a bit overwhelming, but you don't have to figure it out on your own. Here at Mortgage Seven LLC, our entire job is to match your financial situation with the perfect loan program. We're here to guide you through every requirement and find a path that makes sense for you, so you can feel confident from the moment you apply to the day you get the keys.

Why the 20 Percent Down Payment Myth Exists

So, where did this idea that you must have a 20% down payment come from? You’ve probably heard it from well-meaning family, read it online, or seen it on TV. It’s one of the most persistent myths in real estate, and it all boils down to one thing: Private Mortgage Insurance (PMI).

Let's be clear: the 20% figure isn't a law or a hard-and-fast rule. It's simply the magic number that lets you avoid paying for this extra insurance. When you put down less than 20%, lenders see the loan as having a bit more risk. If something goes wrong and you can't make your payments, they have less of a financial cushion to fall back on.

To offset that risk, they require you to have an insurance policy that protects them. That’s PMI. Think of it as the lender's peace of mind, paid for by you. It’s a temporary cost, but it's what gives lenders the confidence to say "yes" to buyers who are ready to own a home but haven't saved up a massive nest egg.

So What Exactly Is Private Mortgage Insurance?

PMI is a monthly fee that gets rolled right into your total mortgage payment. The cost isn't one-size-fits-all; it’s calculated based on a few key things about your loan profile.

- Your Down Payment: The less you put down, the higher the risk, and the more your PMI will cost. Someone putting 5% down will pay a higher PMI premium than someone putting 15% down.

- Your Credit Score: A strong credit history shows you're a reliable borrower. Lenders reward this with a lower PMI rate.

- Your Loan Amount: The premium is a percentage of the total amount you borrow.

On average, you can expect PMI to run anywhere from 0.5% to 2% of your loan amount per year. Let’s say you’re buying a $400,000 house with a 5% down payment ($20,000). Your loan would be $380,000, and your annual PMI could be anywhere from $1,900 to $7,600. That breaks down to an extra $158 to $633 per month. It's an added expense, for sure, but it's often the key that unlocks the door to homeownership years sooner.

How to Get Rid of PMI

Here's the good news: PMI doesn't stick around forever. You are definitely not stuck with it for the next 30 years. There are two main ways to say goodbye to that extra monthly payment.

- It Drops Off Automatically: Thanks to the Homeowners Protection Act, your lender is legally required to automatically terminate your PMI once your loan balance hits 78% of the home's original purchase price. This happens on its own as you chip away at your mortgage each month.

- You Can Request It: You can be more proactive. Once your loan balance gets down to 80% of the original value, you have the right to request in writing that your lender remove the PMI. You just need to be current on your payments.

A hot real estate market can be your best friend here. If home values in your neighborhood have shot up, you might have enough equity to cancel PMI much earlier. You can order a new appraisal, and if it shows your loan is less than 80% of the new, higher value, you can ask your lender to drop the PMI.

The Benefits of a Larger Down Payment

While it’s great that you don’t need 20% down, there are some undeniable perks to putting down more if you can. Figuring out how much down payment on a conventional loan makes sense for you means weighing these advantages.

- No PMI: This is the big one. With 20% down, you skip the PMI conversation entirely.

- Lower Monthly Payment: A smaller loan means a smaller monthly payment, freeing up your budget for other things.

- Instant Equity: You start out with a solid ownership stake in your home, which acts as a nice financial buffer.

- Potentially Better Interest Rates: Lenders love to see borrowers with more "skin in the game" and often reward them with slightly better interest rates.

Ultimately, deciding whether to buy sooner with less down or wait to save up a larger sum is a personal call. To see how these loans compare to other popular options, check out our guide on FHA vs. Conventional loans for a side-by-side breakdown.

Exploring Your Low Down Payment Loan Options

So, we've established that the old 20% down rule isn't the only game in town. Now for the fun part: what are your actual options for getting into a home with less cash upfront?

Thankfully, conventional lending isn't a one-size-fits-all product. There are some fantastic loan programs specifically designed to open the door for qualified buyers, even if they haven't saved a huge nest egg. These aren't obscure, hard-to-find loans, either. They’re mainstream options backed by Fannie Mae and Freddie Mac—the two major players that set the rules for most conventional mortgages in the U.S. Their goal is to make homeownership more accessible, especially for first-time buyers and folks with low-to-moderate incomes.

The Standard 97 LTV Conventional Loan

One of the most popular and straightforward choices is the Conventional 97 loan. The name gives it away: it lets you finance up to 97% of the home's price, which means you only need a 3% down payment. This is a huge deal for people who have a solid income and good credit but just haven't had the time to save up a massive down payment.

The main requirement is that at least one person on the loan must be a first-time homebuyer. For lending purposes, that just means you haven't owned a home in the past three years. It’s a widely available, no-fuss option that has become a go-to for many new buyers.

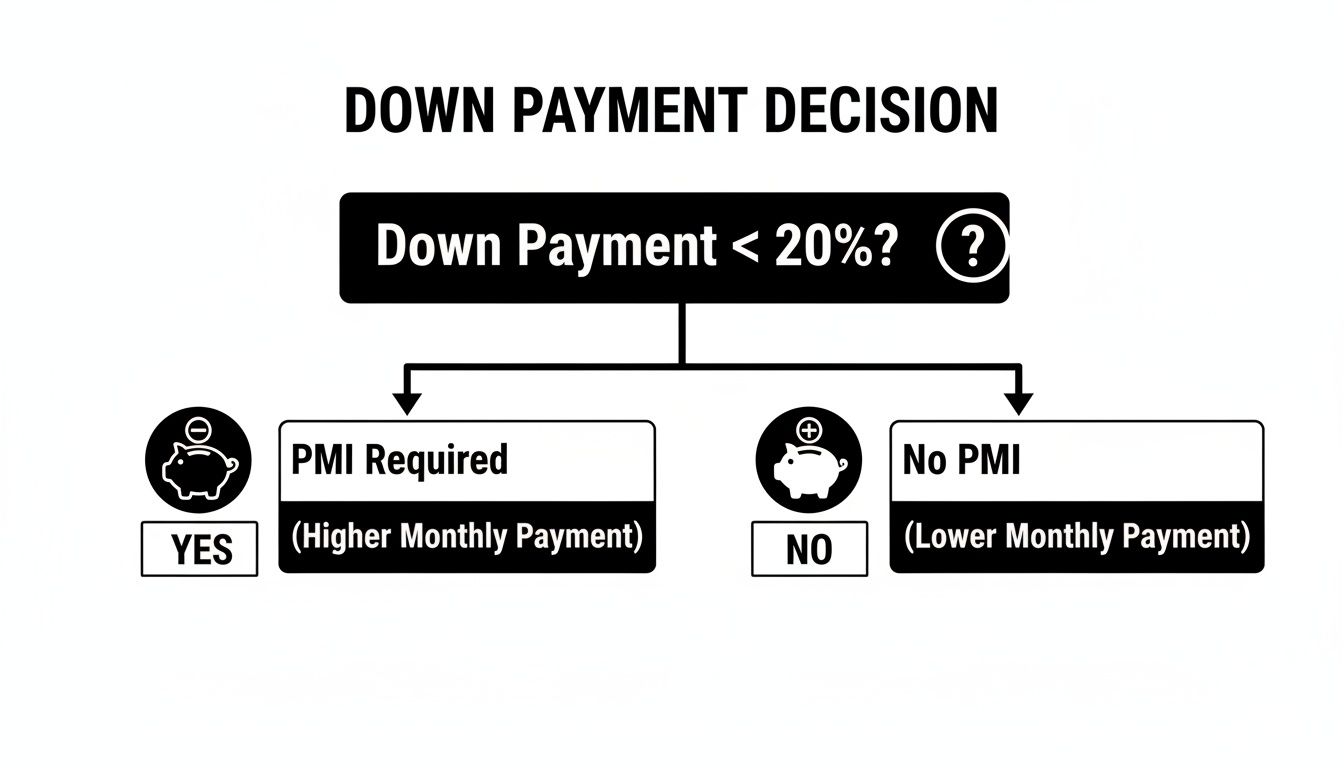

The key thing to remember is that a smaller down payment usually means paying for Private Mortgage Insurance (PMI). This flowchart really simplifies how that decision plays out in your monthly budget.

As you can see, it's a clear fork in the road. Putting down less than 20% brings PMI into the picture and increases your monthly payment, while hitting that 20% mark lets you sidestep it completely.

Fannie Mae HomeReady Program

The Fannie Mae HomeReady program is another powerful tool for buying a home with just 3% down. What makes this one special is its flexibility around income. It’s built specifically for creditworthy borrowers who fall into the low-to-moderate income bracket.

Here’s what makes HomeReady stand out:

- Income Limits: Your eligibility is tied to where you're buying. Typically, your household income can’t exceed 80% of the Area Median Income (AMI).

- Flexible Income Sources: HomeReady gets creative. Lenders can consider income from a roommate or even rent from an accessory dwelling unit (ADU) to help you qualify.

- Homebuyer Education: You'll usually need to complete a homebuyer education course. Honestly, this is a great perk—it prepares you for the realities of owning a home.

Best of all, this program isn't just for first-timers. Repeat buyers who meet the income guidelines can use it, too.

Freddie Mac Home Possible Program

On the other side of the coin is the Freddie Mac Home Possible loan, which is very similar to HomeReady. It’s another path to securing a mortgage with as little as a 3% down payment and is also geared toward helping low-to-moderate-income families.

The ground rules are almost identical to HomeReady:

- Minimum Down Payment: Just 3% of the home’s purchase price.

- Income Caps: Your income generally needs to be at or below 80% of the Area Median Income (AMI).

- Property Types: It’s flexible, covering single-family homes, condos, and even 2- to 4-unit properties, as long as you live in one of the units.

Both HomeReady and Home Possible are incredible programs that make homeownership a reality for people who might otherwise be stuck renting. They’re built on the understanding that having a giant pile of cash isn't the only measure of a responsible homeowner.

Figuring out which of these fits your unique financial picture is a critical next step. To get into the nitty-gritty of these programs, you can learn more about our conventional loan offerings and see how we can structure a loan to meet your goals. The team at Mortgage Seven LLC is here to run the numbers, give you a clear comparison, and help you make a confident, informed choice on your path to owning a home.

How Your Financial Profile Shapes Your Down Payment

Think of getting a conventional loan like assembling a team for a big project. Your down payment is a huge part of your contribution, but it’s not the only thing a lender—your new teammate—is looking at. They want to see your entire playbook: your financial habits, your strengths, and your overall reliability.

Your complete financial picture is what really determines how much you’ll need to put down. Lenders zero in on three core pillars of your finances to figure out how much risk they’re taking on. A strong profile doesn't just get you approved; it can unlock the best terms, including those coveted low down payment options.

Your Credit Score: The Trust Metric

At its heart, your credit score is a measure of your financial reputation. It’s a simple number that tells a story about how you've handled debt in the past. For a lender, a high score signals you’re a low-risk borrower who pays their bills on time. It’s their main gauge of trust.

When it comes to conventional loans, a great credit score is your golden ticket. While the bare minimum is usually around a 620, borrowers with scores of 740 or higher are the ones who get the best interest rates and lowest PMI costs. That financial strength makes it much easier to qualify for a 3% down payment, as the lender feels confident in your ability to pay.

On the flip side, a score in the lower 600s might still get you in the door, but the lender will likely ask for a larger down payment—maybe 5% or even 10%—to offset their perceived risk. It's their way of building a bigger safety net for the loan.

Your Debt-to-Income Ratio: The Budgeting Test

Your Debt-to-Income (DTI) ratio is a straightforward but powerful calculation. It simply compares your total monthly debt payments (car loans, student loans, credit card bills) to your gross monthly income. This number tells a lender how much of your paycheck is already spoken for before you even add a mortgage.

A low DTI shows you have plenty of breathing room in your budget to comfortably handle a new mortgage payment. A high DTI, on the other hand, can be a red flag that you might be stretched too thin.

For conventional loans, lenders typically want to see a DTI of 43% or lower. Some programs might go as high as 50%, but only if you have other strengths, like a high credit score or a lot of cash in the bank. If your DTI is on the high side, a lender might approve your loan on the condition that you make a larger down payment. Doing so reduces the loan amount, lowers your future monthly payment, and brings your DTI back into an acceptable range.

Your Cash Reserves: The Emergency Fund

Finally, lenders need to see that you have cash reserves—money left in the bank after you’ve paid your down payment and all the closing costs. This isn't about being wealthy; it's about having a solid financial cushion for life's surprises.

These reserves, often measured in how many months of mortgage payments you could cover, prove you can handle an unexpected car repair or job loss without missing a house payment.

- For a primary home, having two to six months of reserves is pretty standard.

- For an investment property, that requirement can easily jump to six months or more.

If your profile is a little borderline in other areas, showing that you have strong cash reserves can be the very thing that gets your loan approved with a lower down payment. It gives the lender peace of mind that you're financially stable and truly ready for homeownership.

With home prices on the rise, having a solid financial profile is more critical than ever. A recent Realtor.com Down Payment Report revealed that the median down payment shot up to $30,400—a staggering 117.9% increase from just a few years ago—averaging 14.4% of the home's price. You can dive into the details in the full Realtor.com research report.

Ultimately, these three elements—credit, DTI, and reserves—all work together. A stellar credit score might make up for a slightly higher DTI. A huge down payment could make a lender more comfortable with lower cash reserves. It’s a balancing act, and every borrower’s situation is different. To see how these numbers play out for you, feel free to experiment with our user-friendly mortgage calculators to model different scenarios. At Mortgage Seven LLC, we look at your complete financial picture to find the loan that’s the right fit for you.

Creative Ways to Fund Your Down Payment

Coming up with a big pile of cash for a down payment can feel like the toughest part of buying a home. But the money in your savings account isn't the only option. Lenders are actually quite open to different funding sources, provided you can show them where the money came from with a clear paper trail.

Getting creative here can genuinely speed up your homeownership journey. You might have access to funds you haven't even thought of, from a helping hand from family to programs specifically designed to get you over the finish line. It's all about knowing the rules.

Using Gift Funds From Family

One of the most popular ways to bulk up a down payment is with a gift from a close relative. Lenders are completely on board with this, but they have one non-negotiable rule: it must be a real gift, not a sneaky loan that adds to your monthly debt.

To prove this to the underwriting team, you'll need a formal gift letter. This is a straightforward, signed document stating a few key facts:

- The donor's name and their relationship to you.

- The exact amount of money being gifted.

- A crystal-clear sentence confirming the money is a gift with no expectation of repayment.

The person giving the gift will also need to show a bank statement proving they have the funds. This simple step protects everyone involved and shows the lender your down payment isn't secretly borrowed money.

Leveraging the Sale of an Existing Property

Already a homeowner? The equity you've built is your secret weapon. When you sell your current home, the profit can go directly toward the down payment on your next one.

It’s a pretty standard process, but the timing is crucial. You’ll need to work with your real estate agent and lender to line up the sale of your old house with the purchase of your new one so the money is ready to go at closing.

Down payment assistance isn't just for first-time homebuyers. Many programs are available to repeat buyers who meet the income and location requirements, making them a valuable resource for anyone needing help with upfront costs.

Exploring Down Payment Assistance Programs

Don't sleep on one of the best-kept secrets in real estate: Down Payment Assistance (DPA) programs. These are usually run by state and local housing agencies to help make buying a home more affordable for more people.

DPA programs generally fall into a few categories:

- Grants: This is the best kind of help—free money that never has to be repaid.

- Forgivable Loans: Think of this as a second, interest-free loan that disappears over time (usually a few years), as long as you stay in the home.

- Low-Interest Loans: A second mortgage with a very low rate that you pay back over time, sometimes with payments that don't start for several years.

These programs can make a huge difference, often covering most or even all of your down payment and closing costs. Eligibility usually depends on your income and where you're buying. As you look into different funding options, you might also be surprised at the flexibility of your existing accounts; for example, you can utilize your RRSP for your first-time home buyer down payment.

Comparing Down Payment Funding Sources

Choosing the right source for your down payment depends on your personal situation. Some methods are quick and simple, while others involve more paperwork but offer significant financial benefits. The table below breaks down the most common options to help you see what might work best for you.

| Funding Source | How It Works | Lender Requirements | Best For |

|---|---|---|---|

| Personal Savings | Using money from your checking, savings, or investment accounts. | 2-3 months of bank statements to show the funds are "seasoned" and not from an undisclosed loan. | Borrowers who have had time to save and want the most straightforward documentation process. |

| Gift Funds | A relative provides money for the down payment with no expectation of repayment. | A signed gift letter and proof of the donor's ability to give the funds (e.g., a bank statement). | Buyers who have family support and need a boost to reach their down payment goal quickly. |

| Sale of Property | Using the net proceeds (equity) from selling your current home. | A copy of the signed Closing Disclosure from the sale of your previous home. | Existing homeowners who are "moving up" or downsizing and want to roll their equity into a new property. |

| DPA Programs | Grants or forgivable/low-interest loans from state or local housing agencies. | Varies by program, but typically includes income limits, credit score minimums, and homebuyer education courses. | First-time or repeat buyers who meet income criteria and need help covering upfront costs. |

Ultimately, the best approach is often a combination of sources. You might use some savings, a gift from your parents, and a DPA grant to pull together the funds you need. The key is to be transparent with your loan officer so they can guide you through the documentation for each source.

Let's Find the Right Loan for You at Mortgage Seven LLC

Figuring out conventional loans can feel like a maze, but the truth is, the path to owning a home is much more straightforward than most people believe. If there's one thing you should take away from all this, it's that the old 20% down payment rule is a myth. Fantastic low-down-payment options are out there, and what truly matters is your complete financial picture.

Instead of fixating on one magic number, the goal is to find the loan that fits your life right now. That's exactly where working with an experienced mortgage brokerage like Mortgage Seven LLC comes in. We don't just push paperwork; we work with you to build a strategy that lines up with your personal and financial goals.

Our whole process is built around giving you clarity and confidence. We want you to understand exactly how much down payment on a conventional loan makes sense for your specific situation.

Your Path to Pre-Approval

Getting the ball rolling is simple. We use a clear, step-by-step approach to take you from just curious to confidently pre-approved.

- Schedule a Consultation: It all starts with a simple conversation. We’ll talk about what you're hoping to achieve, answer your questions, and map out a clear plan.

- Get a Personalized Assessment: We'll dive into the details of your financial profile—credit, income, and assets—to see where you stand and find the best opportunities.

- Explore Your Loan Options: As a brokerage, we have access to a huge network of lenders. We’ll bring you the best conventional loan programs you qualify for, whether you're buying your first home or are self-employed.

- Move Toward Closing: Once we’ve locked in the right loan, we'll help you pull together your documents and guide you through the pre-approval and underwriting process with no surprises.

At Mortgage Seven LLC, our commitment is to clear communication and personalized guidance. We find the perfect mortgage that aligns with your financial reality, ensuring you feel supported from our first call to the day you get your keys.

Ready to see what’s possible? Let our expert team at Mortgage Seven LLC give you the clarity and support you deserve. Contact us today to schedule your no-obligation consultation and start your journey home.

Common Questions, Answered

Even after getting the basics down, you probably still have a few specific questions about how much down payment you'll need for a conventional loan. That’s completely normal. Let's tackle some of the most frequent ones we hear from homebuyers just like you.

Can I Really Get a Conventional Loan with Zero Down?

In a word, no. A true zero-down conventional loan isn't really a thing. Lenders almost always need you to have some of your own money in the deal, with 3% being the typical starting point for the most popular programs.

You'll usually find zero-down options with government-backed mortgages, like VA loans for military members and veterans or USDA loans for homes in certain rural areas. If you stumble across an ad for a "no down payment" conventional loan, it’s wise to be a little skeptical. A more realistic route to a low-cash-to-close purchase is through down payment assistance (DPA). These programs offer grants or small, secondary loans that can cover your upfront costs, giving you that zero-out-of-pocket feeling while still using a standard conventional mortgage.

Does My Down Payment Actually Change My Interest Rate?

It absolutely can. From a lender’s perspective, a bigger down payment means less risk. When you have more of your own money invested in the property—what we call "skin in the game"—you're statistically far less likely to default on the loan.

Lenders often reward a down payment of 20% or more with a better interest rate. It shows you're financially solid and, just as importantly, it gets rid of the need for Private Mortgage Insurance altogether. A smaller down payment might nudge your rate slightly higher to offset the lender's increased risk.

A good loan officer can easily run the numbers for you. They can show you a side-by-side comparison of what your loan looks like with 5%, 10%, or 20% down, so you can see exactly how it affects your interest rate and total loan cost over the years. Seeing the actual math makes the decision much clearer.

If I Put Less Than 20% Down, Am I Stuck with PMI Forever?

Not at all. Think of Private Mortgage Insurance (PMI) as a temporary cost, not a life sentence for your mortgage. Thanks to a federal law called the Homeowners Protection Act, there are clear rules for getting rid of it.

Your lender is legally required to automatically terminate your PMI once your loan balance is scheduled to hit 78% of your home's original value. This happens on its own, so you don't have to lift a finger.

But you can be proactive and speed things up. Once your loan balance drops to 80% of the original value, you can formally request in writing that your lender cancel the PMI. You can get to that 80% mark a few different ways:

- Paying as Scheduled: Just making your regular mortgage payments will eventually get you there.

- Making Extra Payments: Chipping in a little extra toward your principal balance each month can significantly shorten the timeline.

- Rising Home Value: If your home's value has jumped since you bought it, you can order a new appraisal. If the new value shows your loan balance is now less than 80% of what the home is worth, you can request to have the PMI removed based on the new appreciation.

PMI is simply the trade-off for getting into a home sooner with less cash. It’s a tool that helps you start building your own equity now instead of waiting years to save up a massive down payment.

Ready to figure out the right down payment for your situation and map out a clear path to owning your next home? The expert team at Mortgage Seven LLC is here with the answers and guidance you need.