Choosing a mortgage lender is one of the biggest financial decisions you'll ever make, but it doesn't have to be a shot in the dark. The real secret to comparing lenders comes down to a simple, focused process: get at least three official Loan Estimates and line them up side-by-side.

This turns a confusing decision into a clear, numbers-driven comparison, letting you see exactly where the differences are in rates, APR, lender fees, and third-party costs.

Your Blueprint for Smart Mortgage Shopping

It's easy to feel overwhelmed by the sheer number of lenders out there. The key is to have a plan. Your goal is to look past the slick marketing and dig into the real cost of each loan. This means creating a blueprint for collecting the right documents, asking the tough questions, and finding a lender who will be a true partner on your home-buying journey.

A great first step is simply understanding the different types of lenders and how they operate. From big national banks to your local credit union or a dedicated mortgage broker, each has its own pros and cons.

The Financial Stakes of Comparing Lenders

The time you spend shopping around pays off—big time. In a typical market, just comparing a few lenders can uncover rate differences of up to 0.5%. For someone with a $300,000 loan, that small difference could save you over $50,000 in interest over the life of a 30-year mortgage. It's a huge deal.

A great rate from an unreliable lender can jeopardize your entire home purchase. Your comparison must weigh both the numbers on the page and the quality of the service you'll receive during one of life’s biggest transactions.

Creating Your Comparison Framework

The best way to keep everything straight is to use a consistent method for evaluating each offer. A simple checklist ensures you're comparing apples to apples, looking at every lender through the same lens—from the loan's financial details to their team's responsiveness.

To get started, here's a high-level look at what you should be comparing.

Your Mortgage Lender Comparison Checklist

Use this quick reference to evaluate the key elements of each mortgage offer. We'll explore each of these points in detail throughout the guide.

| Comparison Point | What to Look For | Why It Matters |

|---|---|---|

| Interest Rate & APR | The difference between the two; how points affect the rate | Rate is the cost of borrowing; APR is the total cost including fees. |

| Fees & Closing Costs | Origination fees, underwriting, processing, title, appraisal | These can vary significantly and add thousands to your upfront cost. |

| Loan Program & Terms | Loan type (FHA, VA, Conv.), term length, fixed vs. adjustable | The program must align with your financial situation and long-term goals. |

| Underwriting Overlays | Stricter DTI, credit score, or reserve requirements | Lender-specific rules that can make or break your loan approval. |

| Speed & Service | Communication, responsiveness, estimated closing timeline | Poor service can cause delays, stress, and even a lost deal. |

| Reputation & Reviews | Online reviews, agent recommendations, past client feedback | Tells you what the real customer experience is like. |

This guide will walk you through each point in detail, but you can also download our free mortgage lender comparison checklist at https://mtg7.com/checklist.html to organize your notes as you go. It's a simple tool, but it ensures no critical detail gets missed.

Decoding Your Loan Estimates Side-By-Side

Once you’ve got at least three official Loan Estimate (LE) documents in hand, the real work begins. This standardized, three-page form is your best friend in this process. Why? Because it forces every lender to show you their numbers in the exact same format, making a true apples-to-apples comparison possible. Your job is to look past the shiny advertised interest rate and dig into the real, all-in cost of each loan.

Don't just skim the first page and call it a day. I’ve seen it a hundred times: two loans with the same interest rate can be thousands of dollars apart in actual cost once you uncover the fees buried in the details. By comparing each LE line by line, you take the guesswork out of a massive financial decision.

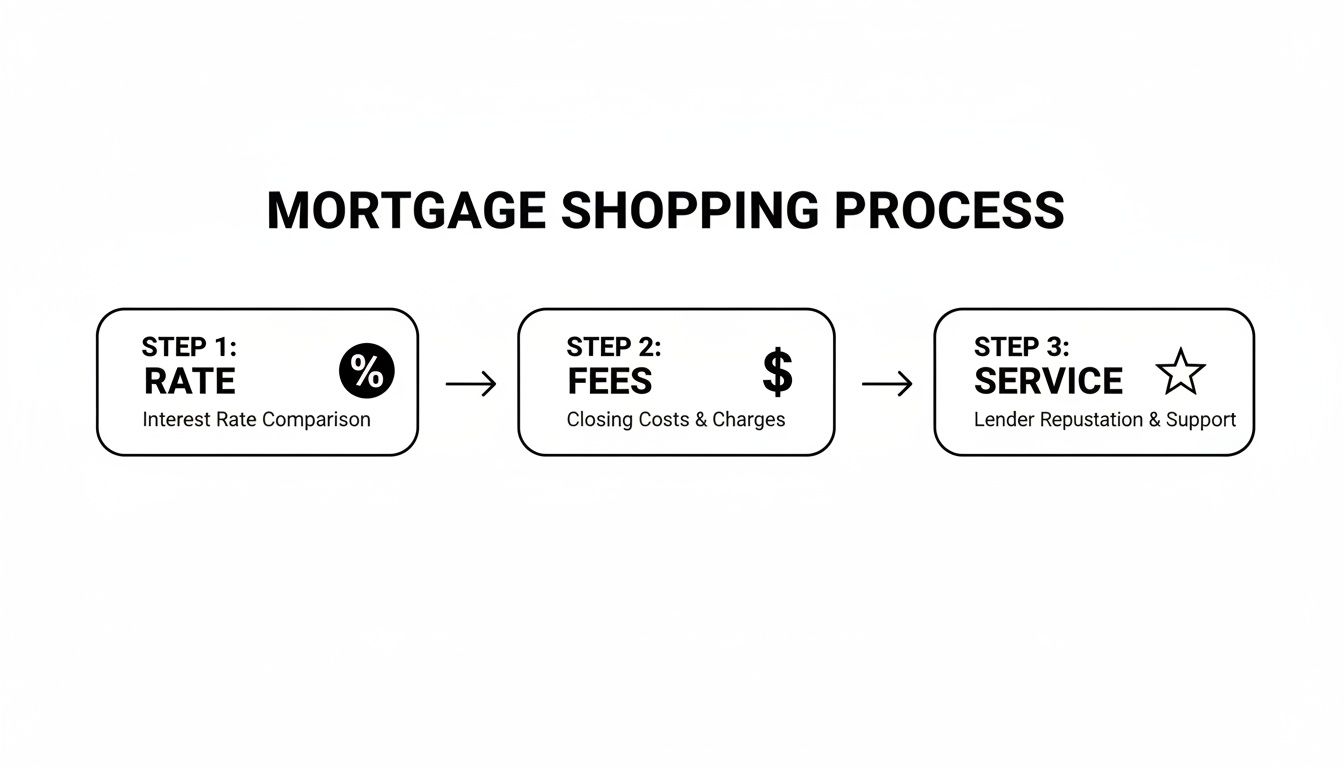

Think of it as a three-part evaluation: you're comparing the rate, the fees, and the service you'll get along the way.

As the graphic shows, a killer rate is just one piece of the puzzle. It means nothing if the fees are sky-high or if the lender can’t get you to the closing table on time.

Page One: The Big Picture—Loan Terms and Projected Payments

Let's start with Page 1 of the Loan Estimate. This is your high-level overview, where you confirm the basics and see a snapshot of your future monthly payment.

First, zero in on the "Loan Terms" section. Does the loan amount, interest rate, and loan term (like 30 years) match what you discussed with the loan officer? And here’s a pro tip: check if the rate is locked. An unlocked rate is just a pretty number on a piece of paper; it can and will change.

Next, shift your eyes to the "Projected Payments" table. This breaks down your monthly nut: principal and interest (P&I), mortgage insurance (if you have it), and an estimate for property taxes and homeowners insurance (escrow). While the escrow part is always an estimate, be wary of any lender whose numbers seem way too low. It can create a false sense of affordability that leads to payment shock down the road.

Page Two: Where the Real Story Unfolds—Closing Cost Details

Alright, this is where you need to put your detective hat on. Page 2 itemizes every single fee, and it’s where a "low-rate" offer can reveal itself as a high-cost trap.

The absolute most important section is Box A: Origination Charges. These are the lender's direct fees—the money they charge for actually doing the loan. Think of it as their profit. This includes things like processing and underwriting fees. Since the lender controls these costs completely, they are your number one target for negotiation.

When you're comparing lenders, treat the Origination Charges in Box A as the lender's price tag. A lender dangling a slightly lower rate might be padding their bottom line with $2,000 more in these fees, making it a much worse deal over the first few years.

Box B, "Services You Cannot Shop For," covers things like the appraisal and credit report. You can’t pick the company, but you can absolutely compare the costs between your Loan Estimates. If one lender’s appraisal fee is $200 higher than another’s, that’s a red flag they might be marking up third-party services.

Finally, you have Box C, "Services You Can Shop For." This includes title insurance, settlement services, and inspections. The lender gives you an estimate, but remember—you have the right to shop around for these providers yourself and potentially save some serious cash.

Page Three: The Bottom Line—Summaries and Key Metrics

Page 3 ties it all together. The "Comparisons" table is incredibly helpful, as it shows you exactly how much you'll have paid in five years, combining principal, interest, mortgage insurance, and all those loan costs.

But the single most critical number on this whole document is the Estimated Cash to Close. This is it. This is the amount of money you need to bring to the closing table, period. It accounts for your down payment, all the closing costs, and subtracts any credits.

Put your Loan Estimates side-by-side and compare this final number. It’s the ultimate reality check and tells you the immediate financial hit of each loan offer.

Don't Just Look at the Interest Rate—Analyze the True Cost

A low interest rate is the oldest trick in the book. Lenders love to flash a low number to get you excited, but that rate rarely tells the whole story of what you'll actually pay. To really compare mortgage lenders like a pro, you have to dig deeper and uncover the loan's true cost. This is how you spot a genuinely great deal versus a cleverly disguised expensive one.

The secret weapon here is the Annual Percentage Rate (APR). Think of the interest rate as the sticker price of a car. The APR, on the other hand, is the "out-the-door" price that rolls in all the extra dealer fees and taxes. It’s a far more honest tool for comparison.

APR: The Truth-Teller of Loan Costs

While your interest rate only covers the cost of borrowing the loan amount itself, the APR bundles in many of the fees the lender controls. We're talking about things like origination charges, underwriting fees, and sometimes even discount points.

This is why a loan with a lower interest rate can, surprisingly, have a higher APR if its fees are sky-high. When you lay your Loan Estimates out side-by-side, the APR is the clearest signal of which loan is genuinely cheaper over its lifetime.

Now, the APR isn't perfect. It's calculated as if you'll keep the mortgage for its full term, and most people don't. Even so, it's still the single best starting point for a quick, apples-to-apples cost comparison.

Zeroing In on Lender-Controlled Fees

Let's get into the nitty-gritty of closing costs—the ones that directly hit your bank account. On your Loan Estimate, pull your focus to Section A (Origination Charges). This is where the lender lists the fees they charge for their own services, and these are the numbers they have complete control over.

You’ll typically see line items like:

- Application Fee: For processing your initial paperwork.

- Underwriting Fee: The cost for their team to vet your finances and approve the loan.

- Processing Fee: An administrative charge for managing all your documents.

- Origination Points: A percentage of the loan paid to the lender or loan officer.

This is where lenders make their money. In fact, industry data showed lenders averaged a profit of $1,201 per loan in Q3 2025. Knowing this gives you leverage. A small reduction in these fees can save you a bundle over the life of the loan.

Here’s a real-world gut check: If Lender X has a slightly lower rate but $2,500 more in Section A fees than Lender Y, you're almost always better off with Lender Y, especially if you don't plan on staying in the home for 30 years.

The Great Debate: To Pay for Points or Not?

Discount points are basically prepaid interest. You pay a fee upfront (one point usually costs 1% of your loan amount) in exchange for a lower interest rate. It can be a brilliant financial move, but only if you stay in the home long enough to make it worthwhile.

You need to calculate your break-even point. This is the moment your monthly savings from that lower rate have officially paid back the upfront cost of the points.

Let's run the numbers on a $400,000 loan:

- Offer A: 7.0% interest rate with zero points. The monthly principal and interest (P&I) is $2,661.

- Offer B: 6.75% interest rate with one point (costing $4,000). The monthly P&I is $2,594.

With Offer B, your monthly savings is $67. To find your break-even point, just divide the cost of the point by your monthly savings:

$4,000 / $67 = 59.7 months (or just under 5 years)

If you see yourself in that home for more than five years, buying the point is a clear win. But if you think you might sell or refinance before then, you'd actually lose money by paying for it upfront. You can play with these numbers yourself using one of the many handy mortgage calculators available online to see exactly how points affect your payment.

Comparing Real Loan Offers: APR vs. Total Costs

To see how this all comes together, let's look at a realistic comparison. Notice how the "best" offer isn't just about the lowest rate.

| Feature | Lender A | Lender B | Lender C |

|---|---|---|---|

| Loan Amount | $350,000 | $350,000 | $350,000 |

| Interest Rate | 6.50% (The Lowest) | 6.625% | 6.75% |

| Points | 1.25 Points ($4,375) | 0.50 Points ($1,750) | 0 Points ($0) |

| Lender Fees (Sec. A) | $1,500 | $995 (The Lowest) | $1,250 |

| Total Upfront Cost | $5,875 | $2,745 | $1,250 |

| Monthly P&I Payment | $2,212 | $2,243 | $2,270 |

| APR | 6.68% | 6.71% | 6.81% |

Lender A looks tempting with that 6.50% rate, but the high points and fees make it the most expensive option upfront. Lender C has the highest rate but the lowest cash-to-close. Lender B sits right in the middle, offering a decent balance. The best choice depends entirely on your personal situation—how long you plan to stay and how much cash you have available.

Ultimately, getting the best deal is about looking beyond the flashy headline rate. By scrutinizing the APR, dissecting the lender fees, and doing the math on discount points, you put yourself in the driver's seat to secure a mortgage that truly works for your financial goals.

Finding the Right Loan for Your Financial Reality

Getting a great interest rate is a huge win, but it's only part of the puzzle. When you're shopping for a mortgage, you're not just comparing rates—you're comparing loan menus. The best lender for you is the one with the right product for your unique financial story, not just the one flashing the lowest number.

Even a small mismatch between your profile and the loan product can get you denied, cause frustrating delays, or cost you thousands more than you need to pay. This is where we go beyond the Loan Estimate and really dig into the bones of the loan itself.

The Big Four: Understanding Your Loan Options

While there's a whole world of niche mortgage products out there, most home loans fall into a few main categories. Getting a handle on these is the first step to figuring out which path is yours.

- Conventional Loans: Think of these as the workhorses of the mortgage industry. They're perfect for borrowers with solid credit (usually a 620 score or higher) and at least 3-5% to put down. Since they aren't government-backed, they often have the best rates for highly qualified buyers.

- FHA Loans: Insured by the Federal Housing Administration, these loans are a game-changer for many first-time buyers. They open the door to homeownership with credit scores as low as 580 and only require a 3.5% down payment.

- VA Loans: This is an incredible benefit for eligible veterans, active-duty military, and surviving spouses. VA loans are tough to beat, often requiring zero down payment and no monthly mortgage insurance, which adds up to huge savings over time.

- USDA Loans: Backed by the U.S. Department of Agriculture, these are designed to help people buy homes in designated rural and suburban areas. They also offer a 0% down payment option, but you'll need to make sure your property and income fit their specific guidelines.

Knowing the basic rules of each is essential. If you're weighing your options, our guide comparing FHA versus Conventional loans breaks down the nitty-gritty details for different financial scenarios.

The Hidden Hurdle: Lender Overlays

Here's an insider secret that trips up a lot of borrowers. Ever wonder why one lender denies you for the exact same loan program another one approves? The answer is often lender overlays.

An overlay is just an extra rule a specific lender tacks onto the official program guidelines. For instance, the FHA might say you can get a loan with a 580 credit score. But Bank XYZ might have an internal rule—an overlay—that says they won't approve any FHA loan with a score below 640. They do this to protect themselves from what they see as extra risk.

This is a hard-and-fast rule at that specific institution. If your credit score is 620, you'll get a denial from them, even though you technically meet the FHA's minimum standard. But the lender down the street, who doesn't have that overlay, would likely give you the green light.

This is exactly why you have to do more than just apply. You have to ask the right questions, especially if your financial situation isn't perfectly straightforward.

Questions to Ask About a Lender's Real-World Rules

Don't be afraid to put a loan officer on the spot. Your goal is to get past the sales pitch and understand their actual underwriting standards.

Be direct and ask things like:

- "What's your bank's minimum credit score for an FHA loan?"

- "Do you have any specific overlays for self-employed borrowers using bank statements?"

- "What is the absolute highest debt-to-income ratio you'll accept for this conventional loan?"

A lender who specializes in helping entrepreneurs will have a totally different set of rules than a giant national bank that primarily works with W-2 employees. And for borrowers in unique situations, like those needing a mortgage loan with an ITIN, finding a lender with true expertise in that niche is non-negotiable. A generalist just won't cut it.

Ultimately, you want a lender with a solid track record. For instance, in Q3 2025, agency mortgage delinquencies were at 4.0%. It’s wise to look for lenders with delinquency rates below the average (under 3.5%), as this often points to better loan servicing and fewer headaches down the road. This is an area where government-sponsored enterprises like Ginnie Mae play a huge role in stabilizing the market, especially for underserved borrowers. You can dig into the data and see the full analysis from Ginnie Mae if you want to understand the bigger picture.

Gauging a Lender's Speed and Responsiveness

Let's be blunt: a fantastic interest rate means absolutely nothing if your lender can't get the loan closed on time. In a competitive housing market, your closing date is a legally binding deadline. A slow or unresponsive loan officer can completely derail the deal, costing you your dream home and maybe even your earnest money deposit.

This is why you have to look beyond the numbers. When you compare mortgage lenders, you aren't just shopping for a product; you're hiring a team to manage one of the biggest financial moves of your life. Their communication style and commitment to your timeline are just as critical as their fees. A rock-bottom rate from a lender who drops the ball is no bargain.

Test the Waters Before You Commit

Before you even think about signing an application, you need to interview your potential loan officer. Treat it like you're the one doing the hiring—because you are. A few direct questions can tell you everything you need to know about the kind of service you'll get.

Here’s what I always recommend asking:

- "What's your average closing time, from application to funding?" A good loan officer knows this number off the top of their head. If they're vague, that's a warning sign. A typical timeframe is 30 to 45 days.

- "Who will be my main contact after I apply?" Find out if you'll be handed off to a processor or an assistant. Knowing the communication chain upfront saves a ton of frustration later.

- "What are your hours? How can I reach you if something urgent comes up after 5 PM or on a weekend?" Real estate doesn't punch a clock from 9-to-5. You need someone who is accessible when it really matters.

- "Looking at my financial picture, do you see any potential underwriting challenges?" This is a great test of their experience. A seasoned pro will spot potential hiccups early on, while a novice might not see trouble until it's almost too late.

Reading Between the Lines of Online Reviews

Online reviews can be a goldmine, but you have to dig past the star rating. Go straight to the one- and two-star reviews and look for patterns. Are multiple people complaining about communication blackouts, missed closing dates, or last-minute fire drills?

Pay attention to keywords in reviews like "delayed closing," "unresponsive," "last-minute request," or "never returned my calls." One bad review could be a fluke, but a clear pattern of these phrases points to a real, systemic service problem.

On the flip side, hunt for detailed five-star reviews that praise specific actions. A review that says, "Jane, our loan officer, got us an updated pre-approval on a Sunday morning so we could make an offer," is infinitely more valuable than a generic "they were great."

Finding the Right Lender Model for Your Style

The kind of company you work with also shapes the service you get. Each lender type has its own vibe and way of doing things, and the best fit really comes down to your personality and how complex your loan is.

- Big National Banks: They often have great rates and a huge menu of loan products. The downside? They can be bureaucratic, with rigid underwriting rules and loan officers who are just a small part of a massive corporate machine.

- Local Credit Unions: These are often praised for outstanding, personal service. They tend to be more flexible and are deeply invested in the local community, though their loan options might be more limited.

- Online Lenders: They usually offer a slick, technology-driven application process. With low overhead, their pricing can be very competitive. The trade-off is often a less personal experience, where you might be dealing with a call center instead of a single, dedicated loan officer.

Think about what matters most to you. If you want a high-touch, personal relationship, a local credit union or a great mortgage broker is probably your best bet. If you're tech-savvy with a straightforward financial file, an efficient online lender could be a perfect match.

How Different Borrowers Should Compare Lenders

Let's get one thing straight: the idea of a single "best" mortgage lender is a total myth.

The right lender for a seasoned real estate investor juggling multiple properties is often the absolute wrong choice for a nervous first-time homebuyer. To really nail this, you have to look at your options through the lens of your own financial story and what you're trying to accomplish.

What works beautifully for one person can lead to a flat-out denial or a much more expensive loan for someone else. It all comes down to finding a lender whose expertise and product lineup click with your specific borrowing profile.

Advice for First-Time Homebuyers

If this is your first time at the rodeo, your priorities are completely different. You need education, hand-holding (and that's okay!), and a clear path to a low down payment. You should be laser-focused on lenders who genuinely shine in these areas.

Hunt for lenders that actively talk about down payment assistance (DPA) programs or government-backed loans like FHA or USDA. You'll often find that local credit unions and community banks are treasure troves of information on state and local DPA grants. A loan officer who patiently answers all your questions is infinitely more valuable than one who just shoves a rate in your face.

Guidance for the Self-Employed and Business Owners

Proving your income when you're self-employed can feel like an uphill battle. Your tax returns, with all their legitimate business write-offs, often don't paint the full picture of your actual cash flow. This means your search has to be for lenders who know how to work with complex income.

When you start making calls, ask specifically if they offer:

- Bank Statement Loans: These programs are a lifesaver. They use your business or personal bank deposit history to qualify your income instead of relying on tax returns.

- Profit and Loss (P&L) Statement Loans: Some lenders will accept a P&L prepared by a CPA, which can completely change the game for your application.

A lot of the big, household-name banks use rigid, automated underwriting systems that just can't handle this kind of nuance. This is one of those times where a specialized non-bank lender or a sharp mortgage broker will give you a much smoother ride to the closing table.

Finding the right lender when you're self-employed isn't just about getting a 'yes'—it's about getting approved for the loan amount that reflects your business's true financial health.

Strategies for Real Estate Investors

Investors are playing a completely different sport. You need speed, aggressive terms on multiple properties, and access to loan products that most homebuyers have never even heard of. You have to find lenders that live and breathe the investment world.

Look for lenders who specialize in DSCR (Debt Service Coverage Ratio) loans. These are incredibly powerful because they qualify the loan based on the property's rental income potential, not your personal debt-to-income ratio. Also, make sure to find lenders with clear, investor-friendly policies on financing multiple properties—some will cap you out sooner than you think.

For investors, comparing a direct lender to a mortgage broker is absolutely critical. A direct lender is limited to their own menu of products. A great mortgage broker, on the other hand, can shop your loan scenario to dozens of wholesale lenders, many of whom have niche investor products you’d never find on your own. For an investor serious about building a portfolio, a good broker isn't just a one-time contact; they're a long-term strategic partner.

Your Top Questions About Comparing Lenders, Answered

When you're diving into the mortgage process, questions are going to pop up. It's totally normal. Getting straight answers is key to feeling confident and steering clear of the common traps that can end up costing you a lot of time and money. Let's tackle the questions I hear most often from borrowers.

How Many Lenders Should I Actually Get Quotes From?

My rule of thumb? Get official Loan Estimates from at least three to five different lenders. Any less, and you might not have a clear picture of what a good deal looks like. Any more, and you can get bogged down in analysis paralysis.

For the best results, don't just shop one type of lender. Cast a wider net.

- Try a big national bank.

- Get a quote from a local credit union or community bank.

- See what a direct online lender can offer.

- Talk to a mortgage broker who can shop dozens of wholesale lenders for you.

This approach gives you a fantastic cross-section of what's available in terms of rates, fees, and the kind of service you can expect.

Is Shopping Around Going to Wreck My Credit Score?

This is a huge fear for so many borrowers, but the short answer is no—as long as you do it the smart way. The credit scoring models know people shop for the best mortgage rate.

All mortgage-related hard inquiries that happen within a 14 to 45-day window get bundled together and count as just one single inquiry on your credit report.

To be safe, just get all your applications in within a two-week span. That way, you can compare offers without stressing about your credit score taking a hit for each one.

Think of your Loan Estimate as an opening bid, not a final contract. You can and should use a better offer from one lender to negotiate with another.

Can I Really Negotiate the Fees on a Loan Estimate?

You bet. A lot of the fees on your Loan Estimate are up for negotiation, particularly the ones the lender controls directly.

When you get your estimate, flip right to Section A: Origination Charges. This is the lender's bread and butter—their fees for underwriting, processing, and originating the loan. If you have a competing offer with lower origination fees, show it to them. Don't be shy about asking for a price match or even a lender credit to help offset your closing costs. The worst they can say is no.

Ready to have an expert in your corner as you compare offers? The team at Mortgage Seven LLC lives and breathes this stuff. We can help you break down the numbers and find the loan that truly fits your goals. Start the conversation at https://mtg7.com today.