Feeling the pinch from your monthly mortgage payment? You're not alone. The good news is that you have options to bring that number down, whether it's by refinancing for a better rate, recasting your loan after making a lump-sum payment, or tackling your escrow costs. These are proven strategies that can provide immediate and long-term relief for homeowners.

Your Guide to a Smaller Mortgage Payment

It's easy to feel stuck with your mortgage payment, especially when it feels like housing costs are sprinting while wages are just jogging. Since January 2020, the typical payment on a new home has shot up by a staggering 74%, easily outpacing most people's income growth. That kind of financial pressure makes finding ways to trim that monthly bill more critical than ever.

The good news? You have more control than you might think. This guide is designed to cut through the jargon and lay out the most effective strategies to lower your payment, each one suited for different financial situations.

Understanding Your Options

The best way to lower your mortgage payment really comes down to your specific goals, how much equity you've built, and your current credit standing. Generally, the strategies fall into three main buckets: changing the loan itself, using a chunk of cash to pay down the principal, or trimming the other costs tied to your home.

Here’s a quick breakdown:

- Loan-Focused Strategies: This is where refinancing to snag a lower interest rate or extending your loan term comes in. These can be incredibly powerful but usually mean going through a new application and paying closing costs.

- Equity-Based Strategies: Have some extra cash on hand? You could do a loan recast or, if you've hit 20% equity, finally get rid of that pesky PMI. These methods lower your payment without touching your interest rate.

- Escrow-Focused Strategies: Sometimes the easiest wins are outside the loan itself. Successfully appealing your property tax assessment or shopping around for a better deal on homeowners insurance can lower your total monthly outlay.

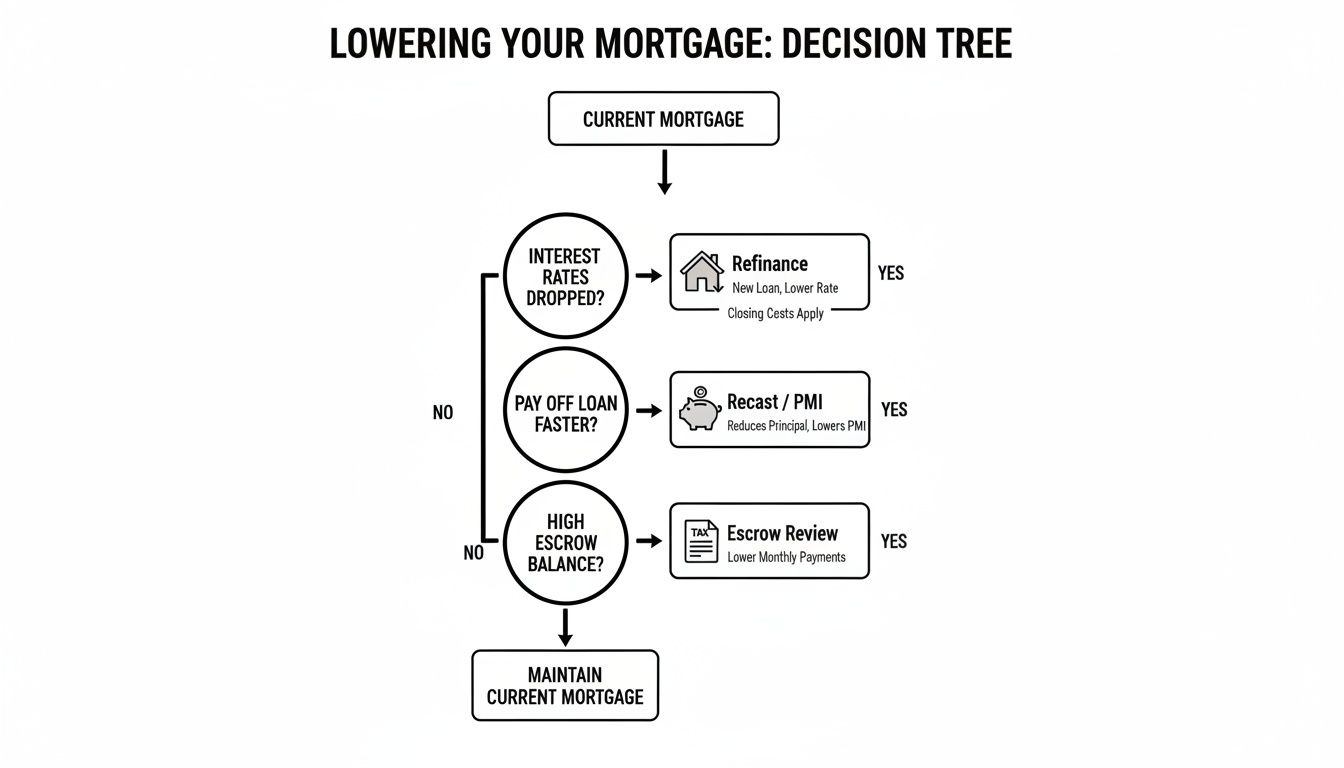

This decision tree gives you a great visual of the main paths you can take—refinancing, recasting, or reviewing your escrow—to help you figure out where to start.

Ultimately, your best move depends on whether you can qualify for a better interest rate, have extra funds to put toward your principal, or can find savings in those non-loan costs.

Your mortgage payment isn't set in stone. By strategically evaluating your loan, equity, and escrow, you can uncover significant monthly savings and improve your overall cash flow.

To get a real sense of what’s possible, it helps to run the numbers. A good online mortgage calculator is a great place to start. For more detailed scenarios, you can also use our mortgage payment calculators at https://mtg7.com/Calculators.html to see how different adjustments might fit your budget. The goal is to quickly see which path makes the most sense for you.

Mortgage Payment Reduction Strategies at a Glance

To simplify things, here's a quick comparison of the most common methods for lowering your monthly mortgage payment. This table breaks down what each strategy involves, who it's best for, and the key things to keep in mind before you jump in.

| Strategy | How It Lowers Your Payment | Best For… | Key Consideration |

|---|---|---|---|

| Refinancing | Replaces your old loan with a new one at a lower interest rate or with a longer term. | Homeowners with good credit when interest rates are lower than their current rate. | Involves closing costs, which can be 2-5% of the loan amount. You need to calculate the break-even point. |

| Loan Recasting | Reduces the principal balance after a lump-sum payment, then re-amortizes the new, lower balance. | Those with a sudden influx of cash (e.g., inheritance, bonus) who want to keep their current interest rate. | Not all lenders offer it, and there's usually a small administrative fee ($250-$500). |

| PMI Removal | Eliminates the Private Mortgage Insurance premium once you reach 20% equity. | Conventional loan borrowers who have paid down their loan or whose property value has increased. | You may need to formally request it and possibly pay for a new appraisal to prove your equity. |

| Escrow Review | Lowers your total payment by reducing property taxes or homeowners insurance premiums. | Anyone, but especially those in areas with high property taxes or who haven't shopped for insurance in a while. | Appealing taxes can be time-consuming, and insurance savings vary widely by provider and location. |

| Loan Modification | Works with your lender to permanently change the loan terms due to financial hardship. | Homeowners facing long-term financial difficulty and who are at risk of foreclosure. | This can negatively impact your credit and is typically a last-resort option. |

Each of these paths has its own set of pros and cons, but understanding them is the first step toward taking control of your monthly housing costs and freeing up more of your money.

Is It Time to Refinance? How a New Loan Can Unlock Serious Savings

Out of all the ways to lower your mortgage payment, refinancing is usually the heavy hitter. Think of it as trading in your current home loan for a brand-new one that comes with a much better deal. You’re essentially wiping the slate clean and starting over with terms that are a better fit for your wallet today.

For most homeowners, the big prize is snagging a lower interest rate. You'd be amazed at how much even a small drop in your rate can save you every single month—and we're talking tens of thousands of dollars over the life of the loan. This is especially true if you bought your home back when rates were higher than they are now.

How a Lower Rate Actually Changes Your Payment

The power of refinancing really comes down to simple math. When your interest rate goes down, less of your monthly payment gets eaten up by interest. This frees up cash and gives your budget some much-needed breathing room.

Let's look at a real-world scenario to see what this looks like in practice:

- The Original Loan: A homeowner has a $400,000 mortgage with a 30-year fixed rate of 7.0%. Their principal and interest payment works out to about $2,661 each month.

- The Refinance Opportunity: Market rates have dropped, and they now qualify for a new 30-year fixed-rate loan at 5.5%.

- The New Payment: After refinancing, their new monthly payment for principal and interest is just $2,271.

That’s an extra $390 in their pocket every single month, adding up to $4,680 a year. This is cash you can now put toward other important goals, like bulking up your retirement savings, tackling other debts, or finally starting that investment portfolio.

If you're curious about what a new rate could do for you, you can dive deeper into the refinancing process and its benefits on our dedicated page.

Why Timing Your Refinance Is Everything

A good refinance is all about timing. The mortgage market is always shifting, and these fluctuations create golden opportunities for homeowners. We all saw a perfect example of this during the pandemic when interest rates hit historic lows.

When rates drop dramatically, that's your cue to act. For instance, mortgage rates hit an unbelievable low of 2.65% in January 2021. But by October 2023, they had climbed to 7.79%, causing the monthly payment on the same median-priced home to soar by 78%. As of January 15, 2026, the average 30-year fixed rate sits around 6.06%, which means there are still plenty of homeowners with older, higher-rate loans who could stand to save a lot.

A key takeaway here: Don't just assume the rate you have is the best you'll ever get. What was a great deal a few years ago might look expensive today. Getting into the habit of checking current mortgage rates every so often is just smart money management.

The All-Important Break-Even Point

While the savings look fantastic, refinancing isn't a free lunch. You'll have closing costs to cover, which typically run between 2% and 5% of your new loan amount. These fees cover things like the appraisal, title search, and lender origination fees. Because you have to spend money to save money, it's absolutely critical to figure out your break-even point.

The break-even point is simply the amount of time it will take for your monthly savings to pay back your closing costs.

Here's the quick formula:

Total Closing Costs / Monthly Savings = Months to Break-Even

Let's go back to our homeowner. If their closing costs on the new $400,000 loan were $8,000 and they were saving $390 a month:

$8,000 / $390 = 20.5 months

It would take them just over 20 months to recoup what they spent on closing costs. If they plan on staying in their home for at least two or three years, this move makes perfect financial sense. But if they think they might sell before that 20-month mark, the upfront cost probably isn't worth it.

While you're looking at refinancing, it can also be a great time to learn how to consolidate your debt effectively, as you might be able to roll other high-interest debts into your new, lower-rate mortgage.

Extend Your Loan Term for Immediate Relief

Sometimes, the name of the game isn't saving every last penny in interest over 30 years. It’s about freeing up cash right now. If your monthly budget feels like it's stretched to the breaking point, extending your loan term can be the pressure release valve you need.

This strategy, most often done by refinancing from a 15-year loan to a 30-year one, is a direct assault on a high monthly payment. By spreading your remaining balance over a much longer timeline, each payment shrinks, giving you immediate breathing room. It's a smart play for anyone dealing with a temporary income dip, a sudden spike in expenses, or simply wanting to redirect cash toward higher-interest debt like credit cards.

The Big Trade-Off: Payment Relief vs. Total Cost

That lower monthly payment feels incredible, but it doesn't come for free. There’s a critical trade-off you absolutely have to understand before you pull the trigger.

While you're enjoying the smaller payment each month, you're almost guaranteed to pay significantly more in total interest over the life of the loan. Why? Because a longer schedule simply gives interest more time to pile up. This is the central dilemma: you're swapping long-term cost for short-term flexibility. It's not a bad choice, but it’s a choice that demands a clear-eyed look at your finances today and where you see them going tomorrow.

A Tale of Two Mortgages: A 15-Year vs. 30-Year Loan

Let's put some real numbers to this. Imagine you have a $350,000 mortgage. Here’s how the math could break down with realistic interest rates for a 15-year versus a 30-year term.

| Loan Term | Interest Rate | Monthly P&I Payment | Total Interest Paid |

|---|---|---|---|

| 15-Year Fixed | 5.50% | $2,872 | $166,935 |

| 30-Year Fixed | 6.25% | $2,154 | $425,562 |

Right away, you can see the appeal. Making this switch would instantly put $718 back into your pocket every single month. For most families, that's a massive win.

But look at the long-term picture. The 30-year loan costs you over $258,000 more in interest. It’s a stark difference that proves this isn't a one-size-fits-all solution.

Think of it like this: A 15-year mortgage is a sprint. It’s tough, it demands more from you each month, but you get to the finish line faster and with less overall effort (interest). A 30-year mortgage is a marathon. The pace is more sustainable, but the journey is much, much longer.

Who Benefits Most from a Longer Loan Term?

So, who is this for? Extending your loan can be a financial lifesaver in the right circumstances.

- First-Time Homebuyers: It can be the key to affording a home in the first place by keeping those initial payments manageable.

- Those with Fluctuating Income: If you're a freelancer, work on commission, or just hit a temporary rough patch, the lower, stable payment is a godsend.

- Strategic Investors: Some homeowners intentionally take the lower payment to free up cash for investments they believe will outperform their mortgage interest rate.

- Growing Families: Life changes, like a new baby or a family member needing care, can strain a budget. A lower payment can make all the difference.

The key is to make a conscious decision to prioritize your monthly cash flow. And remember, nothing stops you from making extra payments down the road if your financial picture brightens up, effectively shortening the term on your own schedule.

Extending your loan term is a proven method for lowering your monthly mortgage payment, even if it means paying more interest over time. Historical data from the Freddie Mac PMMS report consistently shows that 15-year loans have lower rates. For instance, on January 15, 2026, the 15-year fixed-rate mortgage averaged 5.38% while the 30-year was 6.06%. Yet, even with a slightly higher rate, that 30-year loan can slash your monthly payment by 40-50%, providing critical budget relief when you need it most.

Look Beyond a Refi: Loan Recasting and PMI Removal

When homeowners think about lowering their monthly mortgage payment, refinancing is usually the first thing that comes to mind. But there are a couple of powerful, and often overlooked, strategies that can deliver serious savings without the complexity of a brand-new loan: loan recasting and getting rid of Private Mortgage Insurance (PMI).

These two options work by adjusting your existing loan, which is a whole lot simpler than starting from scratch. Let's break down how each one works.

The Smart Way to Use a Lump Sum: Loan Recasting

Loan recasting is a fantastic option if you’ve come into a sum of money and want to lower your monthly bills. Maybe it’s a work bonus, an inheritance, or proceeds from selling another asset.

Instead of just making an extra payment, recasting is a formal process where your lender re-amortizes your loan based on a new, lower principal balance. Your interest rate and loan term don't change at all. But because you owe less, your monthly payment drops.

Let’s run the numbers. Say you have a $400,000 mortgage with 25 years left and a great 6% interest rate. Your current principal and interest payment is $2,577. If you put a $50,000 lump sum toward the principal and then recast the loan, your new balance is $350,000.

Your lender recalculates the payment over the remaining 25 years, and voilà—your new monthly payment drops to $2,255. That’s an extra $322 in your pocket every single month, totaling $3,864 a year. The best part? You keep your low interest rate, and the process usually only costs a small administrative fee, typically $250 to $500.

Loan recasting is an excellent strategy for homeowners who want to improve their monthly cash flow but are happy with their current interest rate. It offers immediate payment relief without the complexity of a full refinance.

A quick heads-up: not all loans are eligible. Government-backed loans like FHA and VA typically don't allow recasting. You'll need to talk to your lender to see if it's an option for you and ask about their minimum lump-sum requirement, which often falls between $5,000 and $10,000.

Ditching That Pesky PMI Payment for Good

Private Mortgage Insurance (PMI) can feel like a major drain on your budget. If you bought your home with a conventional loan and put down less than 20%, you’re probably paying it. This insurance protects your lender, not you, and can easily add $100 to $300 (or more) to your monthly payment.

But here’s the good news: PMI is not a life sentence. You have the right to request its cancellation once you have 20% equity in your home, which means your loan-to-value (LTV) ratio is 80%.

You can build that equity in a few key ways:

- Regular Payments: Every month, a portion of your payment goes toward the principal, slowly but surely building your equity.

- Home Appreciation: If your local market is hot, your home's value may have shot up since you bought it. That rising value counts as equity.

- Smart Renovations: Upgrades like a new kitchen or bathroom can increase your home's market value, giving your equity a nice boost.

The impact of that initial down payment is huge. Amid the market shifts of 2022-2023, the monthly cost of owning a home climbed to 33.79% of the median income. As an example from the history of monthly mortgage payments, a home bought with 5% down in 2023 carried a $2,891 monthly payment—a staggering 113% jump from 2021. Simply avoiding PMI from the start makes a massive difference.

How to Proactively Cancel PMI

By law, lenders have to automatically drop PMI when your loan balance is scheduled to hit 78% of the original home value. But why wait? You can take action yourself once you think you’ve reached the 80% equity mark.

Here’s the game plan:

- Reach Out to Your Lender: Send a formal, written request to cancel your PMI.

- Prove Your Equity: They’ll first check your LTV based on the original purchase price. If your equity comes from rising property values, you'll likely need to pay for a new appraisal, which usually runs a few hundred dollars but can be well worth it.

- Check Your Payment History: To qualify, you’ll need a solid record of on-time payments, especially within the last year.

Shedding your PMI payment feels like an instant pay raise. To get a full breakdown of the entire process, check out our guide on the steps to remove PMI from your mortgage. By being proactive with either recasting or PMI removal, you can free up a surprising amount of cash in your monthly budget.

Lower Your Escrow Costs On Taxes And Insurance

When you open your mortgage statement, you’ll notice a chunk of your payment isn’t going toward principal or interest. It’s sitting in an escrow account to cover property taxes and homeowners insurance. Tackle these two areas head-on, and you’ll shave dollars off your monthly bill without touching your loan terms.

Consider this a behind-the-scenes savings play. Small tweaks to taxes and insurance can add up to significant relief over the life of your mortgage.

Challenge Your Property Tax Assessment

Your local assessor assigns a value to your home each year—and that figure drives your tax bill. While you can’t alter the tax rate, you can appeal an inflated assessment.

Start by pulling your property tax card from the assessor’s office or website. It outlines square footage, bedroom count, and listed improvements. Even a misplaced decimal on square footage can push your taxes higher.

Build your appeal package with:

- Comparable Sales: Gather data on three to five nearby homes of similar age and size. If they sold for 10% to 15% less than your assessed value, that’s solid proof.

- Condition Notes: Document any issues—a leaky roof, aging HVAC, or dated interior—that lower your home’s market value.

- Independent Appraisal: A professional appraisal reporting a lower value can tip the scales in your favor.

Then follow your municipality’s formal appeal process. It usually involves a short form and a hearing. Many homeowners see hundreds knocked off their annual tax bill—and their monthly escrow contributions follow suit.

Shop Around For Better Homeowners Insurance

Insurance rates shift constantly. Sticking with the same provider by default often means missing out on lower premiums elsewhere.

Many homeowners overpay for insurance simply out of habit. Taking an hour once a year to compare quotes can uncover hundreds of dollars in annual savings, directly reducing your monthly escrow deposit.

When you gather quotes, keep coverage levels consistent, then explore these cost-saving tactics:

- Bundle Policies: Insurers typically offer 10% to 25% off when you combine home and auto coverage.

- Raise Your Deductible: Moving from $500 to $1,000 can cut premiums by roughly 20%—just be sure you have the extra cash on hand.

- Ask About Credits: Security systems, smoke detectors, or a clean claims history often qualify you for additional discounts.

- Adjust Coverage Limits: Reducing protection on accessory structures or personal property levels can yield extra savings without compromising core coverage.

By actively managing both taxes and insurance, you’ll keep more money in your pocket each month—and transform your escrow account from a hidden expense into a source of real relief.

Common Questions About Lowering Your Mortgage Payment

When you start looking into ways to lower your mortgage payment, it’s natural for a bunch of questions to pop up. This is a huge financial decision, so getting clear on the details before you make a move is the smartest thing you can do.

Let's walk through some of the most common questions homeowners ask. My goal here is to give you straightforward answers so you can feel confident about choosing the right path for your situation.

How Much Equity Do I Need to Refinance My Mortgage?

This is one of the first hurdles. How much of your home you actually own is a huge factor for lenders when you want to refinance.

For a standard conventional loan, that magic number is usually 20% equity. Hitting that mark means you can refinance without having to pay for Private Mortgage Insurance (PMI), which is key to getting the lowest possible new payment.

But don't panic if you're not quite there. You still have options.

- Government-Backed Loans: Programs like the FHA Streamline Refinance or the VA Interest Rate Reduction Refinance Loan (IRRRL) are famously flexible when it comes to equity.

- Low-Equity Conventional Loans: Some lenders will work with as little as 5% equity, but be prepared—you will almost definitely have to pay PMI with this route.

This is where a good mortgage broker becomes invaluable. They know the landscape and can match your specific equity level with the right lenders and loan programs.

Is It Better to Recast My Loan or Make Extra Payments?

This one comes down to your primary goal. Both recasting and making extra payments involve throwing a lump sum at your mortgage, but they solve different problems.

If you need to improve your monthly cash flow right now, recasting is the clear winner. Your lender re-amortizes the new, lower balance, which directly reduces your required monthly payment. It's instant relief for your budget without touching your interest rate or term.

On the other hand, if your main mission is to kill the mortgage faster and save a ton on interest over the long haul, making extra principal payments is the way to go. This strategy relentlessly chips away at your principal, shortening the loan's life and cutting down the total interest you’ll pay. The catch? Your required monthly payment doesn't change.

A simple way to think about it: Recasting lowers your monthly bill today. Extra payments shorten your financial finish line tomorrow. Both are great for your net worth, but they serve different immediate needs.

Can I Lower My Mortgage Payment If I Have Bad Credit?

A lower credit score definitely makes things trickier, but it doesn't slam the door shut on every option. A traditional rate-and-term refinance might be off the table for now, but other effective strategies are still in play.

Focus on what you can actually control. You can work on appealing your property tax assessment or shop around for a better deal on homeowners insurance. Neither of these actions cares about your credit score, and they both directly lower the escrow portion of your payment.

Some loan programs are also more forgiving. If you have an FHA loan, you might still be able to get an FHA Streamline Refinance, which is known for its less-stringent credit requirements. For homeowners facing genuine financial hardship, a loan modification is another possibility, though it's critical to understand that this can have a negative impact on your credit.

Ultimately, your best long-term play is to work on improving your credit score. A higher score unlocks a world of better options down the road.

When Should I Contact a Mortgage Broker?

The short answer? As soon as you start seriously thinking about it. Getting an expert in your corner right from the start can save you a world of time, money, and headaches.

A broker's true value is their insider knowledge and their network. They essentially act as your personal mortgage shopper, doing all the legwork for you.

Here’s what a good broker brings to the table:

- A Deep Dive Into Your Finances: They'll look at everything—your current loan, credit, income, and equity—to figure out which strategies are actually realistic for you.

- Lender Matchmaking: Instead of you filling out application after application, a broker sends your profile to their network to find the best rates and programs you qualify for.

- Clear, Expert Advice: They can break down the pros and cons of each option, helping you confidently decide between something like a refinance and a recast.

This is a game-changer, especially if you have a unique situation like being self-employed or having a credit history that’s a little bruised. A broker knows which lenders specialize in scenarios like yours, which can make all the difference.

Navigating the mortgage world can feel like a maze, but you don't have to go it alone. The experts at Mortgage Seven LLC are here to help you find the best path forward, whether that's refinancing, recasting, or exploring other creative solutions. Schedule your free consultation today to get personalized advice for your financial situation.