Getting a lower mortgage rate isn't about luck. It's about knowing which levers to pull. You have a surprising amount of control over the rate you're offered, and it all comes down to improving your financial picture, shopping smart, choosing the right loan structure, and picking your moment. Nail these four things, and you could save yourself tens of thousands of dollars over the life of your loan.

Your Blueprint for a Lower Mortgage Rate

Forget the idea of a secret lender or waiting for rates to magically drop. The real path to a lower mortgage rate is understanding how lenders think. They don't pull rates out of a hat; they follow a specific playbook to measure risk. Once you know the rules they play by, you can start winning the game.

This guide goes beyond the usual generic advice. We’re digging into the actionable steps you can take to present yourself as the kind of low-risk, responsible borrower every lender wants to work with.

The Four Pillars of Rate Reduction

Think of this as a four-part strategy. Each part gives you a different way to chip away at your interest rate and, ultimately, your monthly payment.

First up is polishing your financial profile. This goes way deeper than just paying your bills on time. We're talking about a close look at your credit score, how much of your available credit you're using (your credit utilization), and your debt-to-income (DTI) ratio. These are the core numbers lenders fixate on, and even small, deliberate tweaks can make a real difference in the rate they offer.

Next is simply mastering the art of shopping around. Grabbing the first offer you see is one of the most expensive mistakes a homebuyer can make. By getting quotes from different banks, credit unions, and mortgage brokers, you create competition. That competition puts you in a powerful negotiating position.

The third pillar is structuring your loan intelligently. This is where you get into the details—understanding tools like mortgage discount points, deciding between a 15-year and a 30-year fixed loan, or even weighing the pros and cons of an Adjustable-Rate Mortgage (ARM) if it fits your financial goals.

The most important thing to realize is that you're in the driver's seat. The effort you put into preparing your finances and exploring your options is directly tied to how much you'll save.

Finally, timing is everything, especially if you're looking to refinance. Broader economic shifts can open up golden opportunities to lock in a rate that's significantly lower than what you're paying now.

This blueprint shows you have way more power over your interest rate than you might believe. By focusing on these four key areas, you can systematically build a case for a lower rate and keep more of your hard-earned money. Let's walk through each step and turn what seems complex into a clear, manageable plan.

Building a Strong Financial Foundation

Before a lender even glances at a property appraisal, they’re looking at you. Your financial health is the absolute bedrock of their decision, and two numbers matter more than anything else: your credit score and your debt-to-income (DTI) ratio.

Getting a handle on these two factors is the single most powerful thing you can do to prove you're a low-risk borrower. This isn't just about paying bills on time; it’s about strategically polishing your financial profile in the months before you apply. A little focused effort here can translate into massive savings over the life of your loan.

The Power of Your Credit Score

Think of your credit score as your financial report card. It tells lenders how reliable you've been with borrowed money, and they use it to predict how likely you are to pay them back. The reward for a high score? A lower interest rate.

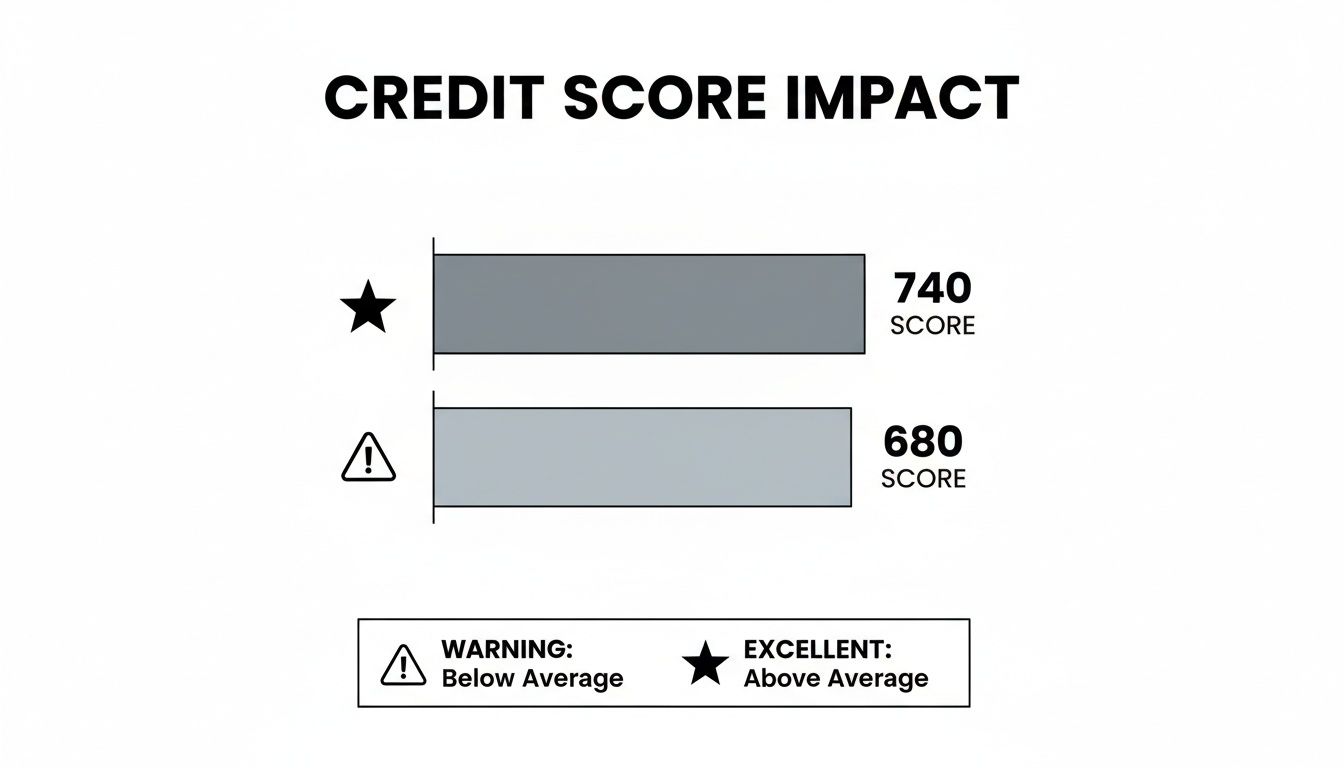

The difference a few points can make is staggering. Let's say you have a 680 credit score. You might get approved, sure, but the lender will bake in a higher rate to offset their perceived risk.

Now, imagine you spend a few months boosting that score to 740. You've just moved into a top tier. That jump could easily knock 0.50% or more off your interest rate, saving you tens of thousands of dollars over 30 years. You can learn more about how lenders view your credit history and its direct impact on mortgage rates in our detailed guide on the subject: https://mtg7.com/Credit.html

Key Takeaway: A great credit score isn't just a "nice-to-have"—it's a powerful negotiation tool. Lenders reserve their absolute best rates for borrowers who have proven their financial discipline.

Your first move is to see exactly what lenders see. By law, you can pull your credit reports for free every single week from the three main bureaus.

Use the official government-authorized site above to get your reports. Once you have them in hand, you can hunt for errors and start making targeted improvements.

Actionable Steps to Boost Your Score

Improving your score is all about strategy. Focus on these high-impact areas for the quickest results:

- Slash Your Credit Utilization: This is the ratio of your card balances to your credit limits. Lenders get really nervous when they see maxed-out cards. Your goal should be to keep your utilization below 30% on every single card, but if you can get it under 10%, you’ll see the biggest score jump.

- Dispute Every Error: Go through your reports from Equifax, Experian, and TransUnion with a fine-tooth comb. A late payment that wasn't late? An account you don't recognize? Get it fixed. Removing just one negative mistake can give your score a serious lift.

- Keep Old Accounts Open: Don't be tempted to close that old credit card you never use. The average age of your credit accounts is a key scoring factor. Closing an old account can shorten your credit history and actually hurt your score.

Understanding Your Debt-to-Income (DTI) Ratio

DTI is the other side of the coin. It’s a simple but critical formula: your total monthly debt payments divided by your gross (pre-tax) monthly income. Lenders use this to see if you can truly afford to add a mortgage payment to your budget.

For instance, if you earn $8,000 a month before taxes and your total monthly debts (car payment, student loans, credit card minimums) add up to $1,600, your DTI is 20% ($1,600 / $8,000).

A huge part of preparing for a mortgage involves finding proven steps to pay off debt fast. Tackling your existing debt is the most direct way to improve this ratio.

Most lenders draw the line at a DTI of 43%, though some programs are more flexible. A lower DTI shows you have financial breathing room, which makes you a much more attractive borrower.

How to Lower Your DTI

You can lower your DTI by either decreasing your debts or increasing your income. Since getting a huge raise overnight isn't always realistic, attacking your debt is the most practical approach.

- Knock Out Small Loans: Got a small personal loan or a store financing plan with just a few payments left? Pay it off entirely before you apply. Wiping that monthly payment off your slate can make a bigger difference than you’d think.

- Pay Down Credit Cards: This is a fantastic two-for-one. Reducing your credit card balances lowers your DTI and improves your credit utilization score at the same time. To make the biggest impact on DTI, focus on the card with the highest minimum monthly payment first.

- Hit Pause on New Debt: This is non-negotiable. In the year leading up to your home purchase, do not finance a car, open a new credit card, or take on any new monthly debt. A new payment can throw your DTI out of whack right when it matters most, potentially costing you a loan approval or saddling you with a higher rate.

Mastering the Art of Lender Shopping

If there's one mistake I see homebuyers make over and over, it's accepting the first mortgage offer they get. It might seem easier, but you're leaving a massive amount of money on the table. The single most powerful tool you have for securing a lower rate is simple: make lenders compete for your business.

This isn't about some secret handshake or insider trick. It’s a straightforward process of getting multiple quotes to see who can give you the best deal. The differences between lenders can be shocking, and a little bit of shopping puts you in the driver's seat for a decision that will impact your finances for decades to come.

Know Who You Are Shopping For

Before you start, it helps to understand who you'll be talking to. The mortgage world is made up of a few key players, and each has its own pros and cons.

- Retail Banks and Credit Unions: Think of the big national bank on the corner or your local credit union. These are direct lenders—they use their own money to fund your loan and typically have a set menu of products. Credit unions are member-owned, so they can sometimes offer fantastic rates and lower fees, which is a definite plus.

- Mortgage Brokers: A broker is your personal mortgage shopper. They don’t lend money themselves. Instead, they have access to a huge network of wholesale lenders and can shop your loan application to dozens of them at once. This effectively creates a bidding war for your loan, often resulting in better terms than you could ever find on your own.

For a lot of people, especially those with unique situations like being self-employed or an investor, a good mortgage broker can be a complete game-changer. They do all the legwork and have access to niche programs you might not even know exist.

The Financial Impact of Comparison Shopping

Getting multiple quotes isn't just a good idea—it's a massive money-saver. We're not talking about a few bucks here and there. We're talking about tens of thousands of dollars over the life of your loan.

A Freddie Mac research on mortgage rates study from 2020 found that borrowers who got five rate quotes saved an average of 0.17 percentage points. That might not sound like a lot, but in some cases, the savings jumped to over 0.50 percentage points.

What does that look like in real dollars? On a $400,000 loan, a 0.50% rate reduction can cut your monthly payment by $120–$130. Over 30 years, that adds up to more than $40,000 in savings.

This is where having a strong financial profile really pays off. A higher credit score makes you a more attractive borrower, which means lenders will roll out the red carpet with their best offers.

As you can see, jumping from a 680 to a 740 score puts you in a completely different league. You become a prime candidate for the most competitive rates available.

The bottom line is simple: getting just one quote is a financial mistake. Every additional offer you get gives you more negotiating power and puts more money back in your pocket.

To see just how powerful this is, let's look at a quick comparison on a typical home loan.

Impact of Shopping Lenders on a $400,000 Mortgage

This table shows how a slightly better interest rate, found by comparing just a few lenders, translates into huge long-term savings.

| Interest Rate | Monthly Payment (P&I) | Total Interest Paid (30 Years) | Lifetime Savings |

|---|---|---|---|

| 6.50% | $2,528.23 | $510,163 | Baseline |

| 6.25% | $2,462.86 | $486,630 | $23,533 |

| 6.00% | $2,398.20 | $463,352 | $46,811 |

As you can see, finding that 6.00% rate instead of settling for the first 6.50% offer saves you nearly $47,000. That's a new car, a college fund, or a serious boost to your retirement savings—all from making a few extra phone calls.

How to Compare Offers Like a Pro

Once you start getting quotes, you'll receive an official document called a Loan Estimate (LE). This standardized three-page form is your best friend for making a true apples-to-apples comparison. But please, don't just glance at the interest rate and call it a day.

You have to look deeper to understand what you’re really paying.

Your Loan Estimate Checklist

- Page 1 – The Big Numbers: Start here. Compare the Interest Rate and the Annual Percentage Rate (APR). The APR gives you a better picture of the loan’s true cost because it bakes in some of the lender fees. Also, keep an eye on the "Total Loan Costs" and "Cash to Close" figures.

- Page 2 – The Details: This is where you need to get forensic. Look closely at Box A: Origination Charges. These are the fees the lender charges for creating the loan, like processing and underwriting. This section is highly negotiable. If one lender's fees are way higher than another's for the same rate, you have a powerful piece of leverage.

- Page 3 – Long-Term Costs: This page is a reality check. It shows how much interest you'll pay in the first five years and over the entire life of the loan. Seeing those big numbers makes it crystal clear why even a tiny rate difference matters so much.

Once you have a few Loan Estimates in hand, you're ready to negotiate. Pick the lender you like best, show them the competing offer, and simply ask: "Can you match or beat these terms?" More often than not, they’ll sharpen their pencil to keep your business. This is how you take control and walk away with the best deal possible.

Using Loan Structure and Points to Your Advantage

Beyond your financials, the loan itself offers powerful levers you can pull to get a better rate. This is where you get to actively shape your mortgage by making smart choices about loan products and tools like discount points. It's about tailoring the loan to your life, not just accepting the first offer you see.

One of the most direct methods for an immediate rate reduction is buying mortgage discount points. It's a straightforward concept: you pay an upfront fee to the lender to "buy down" your interest rate. This isn't just a temporary fix; it lowers your rate for the entire life of the loan.

Typically, one point will cost you 1% of your total loan amount. In return, you might see your rate drop by about 0.25%. While the exact discount can shift with the market and the lender, the basic trade-off is the same: pay more now to save a lot more later.

Calculating Your Break-Even Point

So, when does paying for points actually make sense? The answer lies in finding your break-even point. This is the moment in time when the money you've saved each month from the lower rate officially covers the initial cost of the points.

Let's break it down with a real-world example on a $400,000 mortgage.

- Option A (No Points): The lender offers you a 6.50% rate. Your monthly principal and interest payment is $2,528.

- Option B (1 Point): You pay $4,000 (1% of the loan amount) upfront. The lender drops your rate to 6.25%, making your new monthly payment $2,463.

In this scenario, you're saving $65 every single month.

To find your break-even point, just divide the cost of the point by those monthly savings:

$4,000 ÷ $65 = 61.5 months

This means it will take you just over five years to recoup the cost of the point.

If you're confident you'll stay in the home for longer than 62 months, buying the point is a great move that will save you money in the long run. But if you think you might sell or refinance before that time, you'd be better off skipping the points.

You can run these numbers for your own situation. Our site has a suite of helpful mortgage calculators that let you model different scenarios and see exactly how points would impact your bottom line.

Choosing the Right Loan Term

The length of your loan is another key factor that directly impacts your interest rate. Lenders generally see shorter-term loans as less risky, and they pass that confidence on to you in the form of a lower rate—often 0.75% to 1.0% lower for a 15-year loan compared to a 30-year.

A 15-year fixed mortgage means a higher monthly payment, no doubt about it. But the trade-off is huge: you build equity at a lightning pace and pay dramatically less in total interest. It's a fantastic option for disciplined homeowners with a stable income who prioritize being debt-free.

The classic 30-year mortgage, on the other hand, gives you a lower, more comfortable monthly payment. This frees up cash flow and provides more financial breathing room month to month.

When to Consider an Adjustable-Rate Mortgage (ARM)

Adjustable-rate mortgages have a tricky reputation, but for the right person, they are a brilliant strategic move. An ARM starts with a very low introductory interest rate for a set period (usually 5, 7, or 10 years) before it starts to adjust with the market.

This can be a perfect fit if you don't see yourself in the home for the long haul. For instance, if you know a job relocation is likely in the next five years, a 5/1 ARM could be a savvy choice. You'd get to enjoy that low initial rate for the entire time you own the home and then sell before the rate ever has a chance to change. It's a way to lock in a lower payment without taking on the risk of future rate hikes.

Timing Your Refinance for Maximum Savings

If you're already a homeowner, refinancing is your most direct path to a lower mortgage rate. It's an incredibly powerful tool, but getting it right is a mix of smart timing and simple math. The whole point is to swap your current loan for a new one with better terms, but it only makes sense if the long-term savings actually beat the upfront costs.

Timing is everything. Economic cycles create these windows of opportunity for homeowners. When the broader economy cools down, central banks often lower interest rates to get people borrowing and spending again. This pushes mortgage rates down, creating a perfect chance to lock in a new, lower payment for years to come.

We saw this play out dramatically between 2018 and 2021 when the average 30-year fixed rate in the U.S. plunged from 4.54% to 2.96%. Millions of homeowners refinanced out of rates above 4.5% and into the low-3s or even high-2s. That simple move often slashed monthly payments on a $400,000 loan by $400–$600.

Even a smaller drop makes a huge difference. Shaving just 1.0% off your rate—say, going from 7.25% to 6.25% on a $450,000 loan—can still save you around $280–$320 every single month.

Calculating Your Break-Even Point

A lower rate always looks good on paper, but refinancing isn't free. You'll have to cover closing costs, which typically run between 2% to 5% of your new loan amount. So, the real question is: how long will it take for your monthly savings to cover those fees? This is your break-even point.

Let’s walk through a quick example.

- Current Loan: You have a $400,000 balance at 6.75%.

- Refinance Offer: A new loan at 5.75%.

- Closing Costs: The lender estimates $8,000.

Dropping your rate by 1.0% saves you roughly $250 a month. To figure out your break-even point, you just divide the costs by the savings:

$8,000 (Closing Costs) ÷ $250 (Monthly Savings) = 32 months

In this scenario, it would take you 32 months—a little under three years—to recoup the $8,000 you spent on closing costs. If you know you'll be in the house for five, ten, or fifteen more years, this is a financial slam dunk.

Pro Tip: Never refinance based on the rate alone. Always run the numbers on your break-even point. If there's a chance you'll sell the home before you hit that mark, the refinance will actually cost you money.

It also pays to keep an eye on what's happening in the global economy. For example, understanding the logic behind the Bank of England's rate decisions can give you clues about where interest rates might be headed worldwide, which often influences the U.S. mortgage market.

What's Your Refinance Goal?

Not everyone refinances just to get the lowest possible rate. People use it to achieve all sorts of financial goals, and knowing your primary objective is key to picking the right loan. For a full rundown of the process, our guide on what to expect when refinancing your mortgage is a great resource.

Here are the most common reasons people refinance:

-

Rate-and-Term Refinance: This is the classic move. The goal is simple: replace your loan with one that has a lower interest rate, a shorter term (like going from a 30-year to a 15-year mortgage), or both. It's all about either cutting your monthly payment or building equity faster.

-

Cash-Out Refinance: This is how you tap into your home's equity. You take out a new, bigger mortgage that pays off your old one, and you get the difference in cash. It's a popular way to fund home renovations, consolidate high-interest debt, or pay for a college education. The interest rate might be a touch higher than a standard refi, but it's usually far cheaper than a personal loan or credit card.

-

Eliminating Private Mortgage Insurance (PMI): If your original down payment was less than 20%, you're probably paying for PMI every month. Once your home's value rises and your loan balance drops below 80% of its current worth, you can refinance to a new loan and ditch that PMI payment for good. This can save you hundreds of dollars a month, even if your interest rate stays about the same.

Common Questions About Lowering Your Mortgage Rate

Navigating the world of mortgages can feel like learning a new language. Even with a solid strategy in place, you’re bound to have questions. Let's tackle some of the most common ones that come up when people are trying to land a lower rate.

How Quickly Can I Improve My Credit Score for a Better Rate?

You'd be surprised how fast you can make a difference. While major credit repair takes time, you can see real improvement in as little as 30-60 days. The fastest way to give your score a boost is to hammer down your credit card balances. Lenders pay close attention to your credit utilization ratio.

Getting all your balances below 30% of the credit limit is a solid goal. But if you really want to impress lenders and see a significant jump, push that number below 10%. It’s a powerful signal that you’re not overextended and can manage debt responsibly.

Another quick win? Scour your credit reports for errors. Seriously, get copies from all three bureaus—Equifax, Experian, and TransUnion.

- Dispute Inaccuracies: A single mistake, like a payment that was on time but reported as late, can be an anchor on your score. Find it, dispute it, and get it removed.

- Pause New Activity: For a few months before you apply for a mortgage, just stop. Don't open new credit cards, don't close old ones, and don't take on new loans. Any of these moves can cause a temporary dip in your score right when you need it to be at its peak.

A common myth is that closing old credit cards helps. Don't do it! The length of your credit history is a major factor in your score, and closing an old account can actually shorten that history and hurt you.

Is Refinancing for a 0.5% Rate Drop Worth It?

It absolutely can be, but it all comes down to the numbers. You have to figure out your break-even point to see if the upfront closing costs are worth the long-term savings.

Let's run a quick scenario. Say your closing costs to refinance will be around $5,000. On a $400,000 mortgage, dropping your rate by 0.5% (from 6.5% to 6.0%) would save you roughly $125 a month.

The math is simple:

$5,000 (costs) / $125 (monthly savings) = 40 months

In this case, it would take you 40 months, or just over three years, to recoup the cost of refinancing. If you're planning to stay in the home for longer than that, it's a smart financial move. And remember, the bigger your loan, the more impactful even a tiny rate reduction becomes.

Does My Property Type Affect My Mortgage Rate?

Yes, absolutely. Lenders look at different property types with different levels of risk, and they price your loan accordingly.

- Single-Family Primary Residence: This is the gold standard. It’s your home, and lenders know you’ll fight to keep it, making it the lowest-risk loan for them. You’ll get the best possible rates here.

- Investment Property: Lenders see rental properties as a business venture, which means they’re higher risk. If you hit a financial rough patch, you’re more likely to let the investment property go before your own home. As a result, expect rates to be 0.50% to 1.0% higher.

- Condominiums: Condos can sometimes land you a slightly higher rate, too. The lender isn't just underwriting you; they're also underwriting the entire condo association. They’ll dig into the HOA’s budget and financial reserves. A poorly managed HOA introduces more risk, which can mean a less favorable rate for you.

Can I Lock a Rate Before I Find a House?

In most cases, no. A rate lock is tied to a specific property address because the home itself is part of the lender's risk equation. You generally can't lock a rate until you have a signed purchase contract.

What you can and should do is get a full pre-approval. This isn't just a quick online form; it's a deep dive where a lender verifies your income, assets, and credit. A solid pre-approval gives you a clear picture of what you can afford and the rate you'll likely qualify for based on today's market.

The standard path is: get pre-approved, find your home, get it under contract, and then lock your rate. Some lenders do offer "lock and shop" programs that let you lock a rate while you're house hunting, but they usually come with upfront fees and a lot of fine print. For most buyers, sticking to the traditional process works best.

At Mortgage Seven LLC, we specialize in helping you find the ideal loan structure and the most competitive rate for your unique financial situation. Whether you're a first-time buyer or an experienced investor, our team is here to guide you through every step of the process. Schedule your free consultation today at https://mtg7.com to start your journey toward a better mortgage.