When you work for yourself, proving your income to a lender usually boils down to a few key documents. For most, this means showing two years of tax returns, a steady stream of deposits via 12-24 months of bank statements, or a professionally prepared Profit and Loss (P&L) statement.

Deciding which route is best really depends on how your business is set up and, just as importantly, the kind of mortgage you're trying to get.

The Self-Employed Homebuyer's Dilemma

You see that perfect home in Fairfax, and you know you can afford it. But as soon as you look at a standard mortgage application, it feels like the whole system is designed for someone else. As a freelancer, consultant, or small business owner, your income is solid, but proving it without a W-2 can be a nightmare.

It's a common frustration. So many lenders are still stuck in the past, using old-school verification methods that just don't reflect the reality of modern entrepreneurship. This outdated thinking creates unnecessary roadblocks and can slam the door on otherwise fantastic opportunities.

That's why this guide exists—to cut through the noise and give you a clear, actionable plan. Your business success shouldn't be a handicap in the homebuying process. The secret is learning how to translate your financial story into a language that underwriters can finally understand.

Your Primary Tools for Success

Getting a lender to see your true earning power comes down to how you present three core documents. Each one tells a slightly different part of your financial story, and knowing which one to lead with can make or break your application.

- Tax Returns: This is the old standby. Lenders look at your tax returns to see your net income—what's left after all those crucial business write-offs.

- Bank Statements: This is all about cash flow. These statements provide a direct, unfiltered look at the actual money coming into your business accounts every single month.

- P&L Statements: A well-prepared P&L gives a snapshot of your business's health, breaking down revenue and expenses to paint a clear picture of your true profitability.

It's time to ditch the one-size-fits-all mindset that leaves so many entrepreneurs feeling stuck. The first step toward getting that approval is understanding the nuances of self-employed mortgage requirements. We'll walk through specific loan programs—from Conventional and FHA to innovative Bank Statement loans—that are built for borrowers just like you.

When you match the right documents to the right loan product, you can approach the process with confidence, fully prepared to get the financing you need.

Key Takeaway: Being self-employed is not a barrier to homeownership; it just requires a different strategy. The goal is to align your unique income situation with a lender and loan program that understands and values entrepreneurial success, ensuring your application gets the fair look it deserves.

This guide will give you the knowledge to do just that, helping you turn your hard work into the keys to your new home.

Using Tax Returns to Document Your Income

When you're self-employed, your federal tax returns are the gold standard for proving your income to a mortgage lender. They offer a clear, IRS-verified history of your earnings, which is exactly what underwriters are looking for. This is the most traditional and widely accepted path, especially for conventional and government-backed loans.

Lenders will almost always ask for your last two years of complete, filed federal tax returns. I'm not just talking about the main Form 1040 page; they need every single schedule that breaks down your business financials. For most sole proprietors or single-member LLCs, your Schedule C (Profit or Loss from Business) becomes the most important document in the entire file.

Calculating Your Qualifying Income

Underwriters analyze your tax returns with one goal in mind: to find a stable, predictable monthly income they can count on. The standard practice is to average your net income over the past 24 months.

Here’s a quick look at how they do it:

- They find the net profit line on your Schedule C for the most recent two years.

- They add those two numbers together.

- They divide that total by 24.

The result is your average monthly qualifying income.

This is where so many talented entrepreneurs get stuck. The same deductions you cleverly use to lower your tax bill—for your home office, vehicle mileage, equipment, and supplies—directly shrink the net income a lender can use. It's the classic catch-22 of being your own boss.

A savvy business owner might masterfully reduce their taxable income to almost nothing, but to a mortgage underwriter, that financial prudence makes it look like they barely earn a living. The key is to find a strategic balance in the years leading up to your home search.

Think about a freelance graphic designer who grosses $120,000 a year. After deducting software subscriptions, a new computer, and marketing costs, their Schedule C shows a net profit of just $70,000. The lender qualifies them based on the $70,000, not the $120,000 that actually flowed through their business. This single distinction can dramatically lower your borrowing power.

The Double-Edged Sword of Tax Write-Offs

While minimizing what you owe the IRS is just good business, it can actively work against you when applying for a mortgage. Your tax return often doesn't tell the full story of your financial health. In fact, some studies have found that self-employed workers' reported income is about 25% lower on average than what their actual spending habits would suggest, largely due to legitimate deductions.

This gap between your true cash flow and your taxable income is why planning ahead is absolutely critical. If you know you want to buy a home in the next couple of years, you might want to ease up on some of the more aggressive or discretionary write-offs. Paying a bit more in taxes for a year or two could be the trade-off that gets you into the home you really want.

For a full checklist, check out our guide on the documents needed for mortgage pre-approval.

To give you a head start, here’s a quick rundown of the essential paperwork you'll need to pull together when using tax returns.

Essential Documents for Tax-Based Income Verification

Gather these key documents to streamline the income verification process when using your federal tax returns.

| Document Type | What It Shows | Pro Tip |

|---|---|---|

| Federal Tax Returns (2 Years) | Your complete financial picture, including all schedules (C, E, etc.). | Have both years saved as PDFs, ready to upload. Make sure they are signed and dated. |

| Year-to-Date Profit & Loss (P&L) | Your business's current financial performance for the current year. | This shows the lender that your income is stable or growing since your last tax filing. |

| Business Bank Statements | The actual cash flow moving through your business accounts. | Lenders often want the most recent 2-3 months to confirm your P&L statement is accurate. |

| IRS Form 4506-C | Your signed permission for the lender to verify your tax returns with the IRS. | This is a mandatory fraud-prevention step. You'll sign this as part of your application. |

Having these documents organized and ready to go from the start will make the entire process smoother and faster.

Verifying Your Documents The IRS Way

To make sure the tax returns you hand over are the real deal, lenders will have you sign IRS Form 4506-C (IVEST Request for Transcript of Tax Return). This is non-negotiable.

This form gives your lender permission to pull a transcript of your tax records directly from the IRS. They compare that transcript to the documents you provided, and the numbers have to match. Any significant differences can stop your application in its tracks. It's a standard and crucial step to prevent fraud and confirm your financial information is accurate.

Using Bank Statements and P&L to Show Your True Cash Flow

What happens when your tax returns, packed with legitimate business write-offs, show an income that just doesn't match the actual cash hitting your accounts each month? This is the reality for millions of entrepreneurs, and it’s where alternative documentation loans become an absolute game-changer. These specialized mortgages look past your net taxable income to focus on your real financial health.

For self-employed borrowers, proving your income can feel like trying to fit a square peg into a round hole. But with the right approach, you can showcase your true earning power.

How Bank Statement Loans Work

The most powerful tool in this category is the Bank Statement Loan. Instead of digging through your Schedule C, lenders review 12 to 24 months of your business or personal bank statements. Their goal is simple: identify the consistent, recurring deposits that represent your actual gross revenue.

This method completely sidesteps the impact of all those tax deductions. An underwriter is trained to analyze your deposit history, calculate an average monthly income, and use that figure to determine what you can comfortably afford. It’s a commonsense approach that values real-world cash flow over net profit.

Expert Insight: I've seen it time and again—for many freelancers and small business owners, bank statement loans can result in a qualifying income that is 50% higher or more compared to what their tax returns show. That difference can be the key to affording the home you truly want.

Imagine you're a self-employed freelancer dreaming of buying your first home in Fairfax, Virginia, but lenders keep asking for 'proof of income' that feels impossible to provide without a W-2. Bank statements have become one of the most reliable ways to demonstrate your earnings, especially through specialized mortgage programs. As industry data shows, providing 12 to 24 months of bank statements showing consistent deposits can qualify you for a loan. Lenders will typically average your monthly deposits—often excluding the lowest two months—and multiply that by 12 for your annual income figure. You can discover more about these findings on how self-employed individuals prove their earnings.

A Real-World Example: The Freelance Graphic Designer

Let’s put this into perspective.

Meet Sarah, a talented freelance graphic designer who grosses an average of $10,000 per month. Her deposits are consistent, coming from a mix of retainer clients and project-based work.

- The Tax Return Method: After deducting expenses for software, a new computer, marketing, and a home office, her Schedule C shows a net annual profit of $60,000. A traditional lender divides this by 12, giving her a qualifying monthly income of just $5,000.

- The Bank Statement Method: An underwriter reviews 12 months of her business bank statements and sees consistent deposits totaling $120,000 for the year. The lender might apply a standard 50% expense factor (a common practice to account for business costs), which would leave a qualifying annual income of $60,000. So it's the same, right?

Not quite. Here's where it gets interesting. If Sarah keeps clean books and can prove her actual business expenses are lower—let's say 25%—the lender can often use that figure instead. Just like that, her qualifying income jumps to $90,000 annually, or $7,500 per month. That's a 50% increase in borrowing power, all by using a loan program that understands her true cash flow. You can learn more about how lenders make these calculations in our in-depth guide to bank statement loans.

Using a P&L Statement for an Even Stronger Case

Another powerful option is a loan based on your Profit & Loss (P&L) Statement. A P&L, sometimes called an income statement, gives a detailed summary of your business's revenues, costs, and expenses over a specific period.

While a P&L on its own might not be enough, a professionally prepared statement—often created or at least verified by a CPA—can be incredibly persuasive when you pair it with your bank statements. It gives the underwriter a clear, organized narrative of your business's financial health.

A strong P&L accomplishes a few key things for you:

- It itemizes your revenue streams, showing exactly where your money comes from.

- It details your cost of goods sold (COGS) and your operating expenses.

- It calculates your net income, demonstrating clear profitability.

When an underwriter sees a professionally prepared P&L that lines up with the deposits on your bank statements, it builds immense confidence. It validates the story your bank statements are telling and provides a structured financial overview that tax returns, with their focus on deductions, often obscure. This combination is one of the most effective ways for self-employed individuals to prove their income and build a compelling case for mortgage approval.

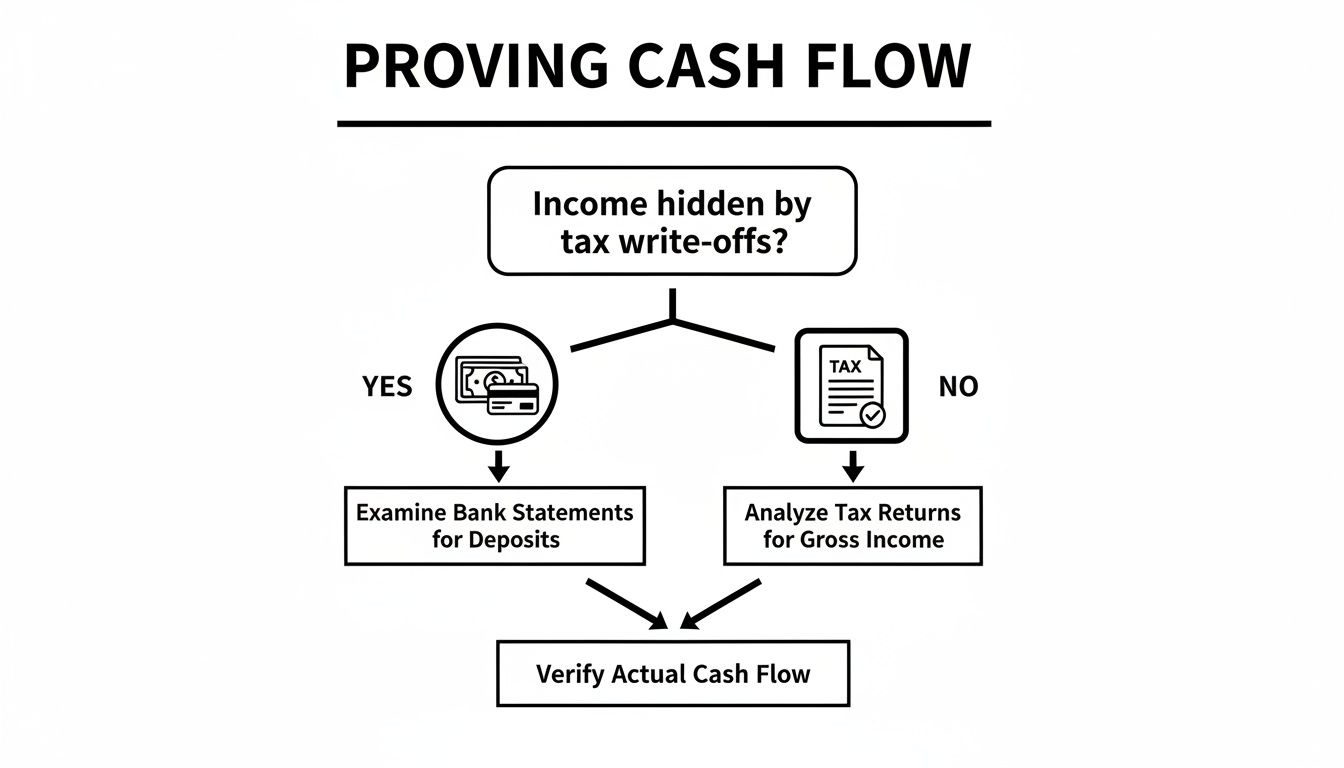

Specialized Loans for Entrepreneurs and Investors

If you’re self-employed, you might think your mortgage options are limited. That’s a common misconception. The truth is, there's a whole suite of specialized loan programs designed specifically for the unique financial profiles of entrepreneurs and real estate investors. It’s all about finding a path to homeownership that reflects your business's reality, not just what’s on page one of your tax return.

Lenders who offer these products get it—a successful business owner's finances rarely look like a W-2 employee's. These loans offer flexible ways to prove your income, focusing on metrics that paint a much clearer picture of your actual ability to handle a mortgage. The trick is knowing which one fits your situation.

This flowchart breaks down the decision-making process based on how you can best prove your cash flow.

As you can see, the core choice is simple. If your business takes full advantage of tax write-offs that dramatically lower your net income, a bank statement loan is probably your best bet. If not, verifying your income the traditional way with tax returns is a perfectly solid route.

DSCR Loans for Real Estate Investors

For investors building a real estate portfolio, the Debt Service Coverage Ratio (DSCR) loan is a game-changer. This isn't your typical mortgage; it shifts the focus entirely away from your personal income.

Instead of combing through your personal tax returns or bank statements, a DSCR loan qualifies the property itself. The lender’s main concern is whether the investment property's projected rental income can cover its own monthly mortgage payment, taxes, insurance, and any HOA fees (PITI).

Here’s a quick look at how it works:

- An appraiser provides a market rent analysis to establish the property's potential monthly income.

- The lender compares that rental income to the property's total monthly housing expense.

- If the income is equal to or greater than the expenses (a DSCR of 1.0 or higher), you’re on your way to qualifying.

This is the perfect solution for investors who have significant tax write-offs or simply want to scale their portfolio without getting bogged down by personal income documentation. The investment stands on its own merits.

Expert Insight: For the best rates and terms, most lenders want to see a DSCR of 1.25 or higher. This means the property is expected to generate 25% more in rent than it costs each month. Properties with strong cash flow are ideal for this type of financing.

ITIN Loans for Non-Citizen Entrepreneurs

Being an entrepreneur and contributing to the economy should open doors to homeownership, regardless of citizenship status. That’s where Individual Taxpayer Identification Number (ITIN) loans come in.

An ITIN is a tax-processing number from the IRS for people who need to file U.S. taxes but aren't eligible for a Social Security Number (SSN).

ITIN mortgage programs are designed for these non-citizen entrepreneurs, allowing them to qualify for a home loan. The underwriting process is often similar to conventional loans, but it’s handled by lenders who specialize in this area. To prove income, you'll typically need:

- Two years of tax returns filed using your ITIN.

- Bank statements to show consistent business deposits.

- A Profit & Loss statement to detail your business's profitability.

These loans create a vital pathway for a hardworking and often overlooked segment of the entrepreneurial community to build wealth through real estate.

Don't Rule Out Conventional and FHA Loans

Even with all these amazing specialized products, don't automatically dismiss traditional financing. Conventional and FHA loans are still very much on the table for self-employed borrowers who have their ducks in a row.

If your tax returns show at least two years of solid, stable, or increasing net income, you could be a great candidate for one of these loans. It all comes down to planning ahead. By strategically managing your business deductions in the years before you apply, you can present a financial profile that sails through traditional underwriting. This is where a skilled broker like one from our team at Mortgage Seven LLC becomes invaluable—we can analyze your entire financial picture and point you toward the program, specialized or traditional, that gives you the highest odds of approval.

Common Pitfalls That Can Derail Your Mortgage Approval

Getting a mortgage when you're self-employed is as much about avoiding common mistakes as it is about providing the right documents. A strong application isn't just about impressive income; it’s about presenting a clean, clear, and organized financial picture that an underwriter can easily understand and approve.

Think of this as your pre-flight checklist. Learning from the missteps others have made is one of the smartest things you can do to ensure a smooth journey to the closing table.

Mixing Business and Personal Finances

This is, without a doubt, the biggest and most frequent mistake we see. When you run your business out of your personal checking account—depositing client payments right next to birthday checks from grandma—you create an absolute nightmare for an underwriter. Their job is to sift through everything to separate your actual business revenue from personal cash, and that’s a time-consuming mess.

Frankly, it forces them to make conservative, and often unfavorable, assumptions about your real income. A commingled account makes it nearly impossible to get a true read on your business's cash flow. It raises red flags about where your money is coming from and makes you look financially disorganized.

- Pro Tip: Do yourself a massive favor and open a dedicated business checking account at least six to twelve months before you even think about applying for a mortgage. All business income goes in, and all business expenses go out. This simple discipline creates the clean, transparent records that underwriters absolutely love to see.

Showing Wildly Inconsistent Deposits

It's the nature of the beast for freelancers and business owners: some months are fantastic, others are lean. While this is normal for any entrepreneur, huge, unexplained swings in your bank deposits can make a lender nervous. Underwriters are trained to look for stability and predictability.

Seeing a $15,000 deposit one month followed by just $2,000 the next will make them question how reliable your income stream really is. While some fluctuation is expected, extreme volatility without context can make it difficult for them to land on a dependable average income. They might even be forced to throw out your best months, which can seriously hamstring your borrowing power.

Expert Insight: If your income is seasonal or project-based, don't just hand over a stack of bank statements and cross your fingers. Be proactive. A brief, professional letter—ideally from your CPA—explaining the nature of your business and the reason for the fluctuations can work wonders. Context is everything.

This is also where a Profit and Loss (P&L) statement becomes your best friend. P&Ls give self-employed borrowers a powerful way to demonstrate their true earning power, especially when their tax returns are written off to the hilt. It’s not uncommon for lenders to qualify 20-30% more income by analyzing a detailed P&L that averages 12-24 months of revenue and expenses. In 2023, a telling 71% of solely self-employed borrowers used P&Ls to secure their loans, which boosted approval odds by 35% for those with volatile earnings. You can learn more about how these methods prove income effectively.

Making Large Purchases Before Closing

I can't stress this enough: the time between your application and closing is a financial quiet zone. Making a large, debt-financed purchase during this period can be catastrophic for your loan approval. Buying a new truck, financing a house full of furniture, or even opening a new business line of credit will change your debt-to-income (DTI) ratio.

Lenders pull your credit and re-verify your finances one last time right before closing. If a new loan or a maxed-out credit card suddenly appears, it could push your DTI over the limit and kill the deal at the eleventh hour. It happens more often than you'd think, and it's heartbreaking every time.

- Pro Tip: Just wait. Put all major spending on hold until the keys are in your hand. If you absolutely have to make a significant purchase, talk to your loan officer first so you understand exactly how it will impact your application.

Submitting Disorganized or Incomplete Paperwork

Finally, remember that presentation matters. Handing over a jumbled mess of unsorted bank statements, incomplete tax forms, or a P&L that looks like it was scribbled on a napkin sends all the wrong signals. It suggests you're disorganized, which can frustrate the underwriting team and lead to endless back-and-forth requests for more information.

Your goal is to make the underwriter's job easy. A clean, complete, and well-organized file allows them to check the boxes, verify your income, and stamp "approved" on your application. Taking the time to get your documents in order shows you're a professional and financially responsible borrower—exactly the kind of person every lender wants to work with.

Your Next Steps to Buying a Home

Knowing this stuff is great, but taking action is what finally gets you the keys to a new home. You've seen the strategies—from using carefully prepared tax returns to proving your actual cash flow with bank statements. You also know there are specialized loans out there designed specifically for entrepreneurs.

The biggest thing to remember is that being your own boss shouldn't stop you from owning a home. It just means you need a different game plan. Your journey starts now, not with a mountain of paperwork, but with a simple conversation.

Chart Your Course with an Expert

Let's figure out your personal roadmap. A quick consultation can give you a clear, step-by-step plan for what documents to gather and how to get pre-approved. It’s your chance to ask all the questions rattling around in your head and get answers that actually apply to your business.

At Mortgage Seven LLC, our job is to connect you with lenders who get it. They don't just see a stack of papers; they see the story behind your business. They know how to look at your income and understand your real earning power, whether we use traditional documents or more flexible loan options.

This is your chance to turn all that hard work into a home. Don't let a little uncertainty get in the way. A strategic chat can clear up the confusion and put you on a direct path to getting approved.

Taking this first step puts a dedicated expert on your team, someone ready to find a mortgage that fits your entrepreneurial life. That dream home is closer than you think. It's time to make it happen.

Common Questions from Self-Employed Borrowers

Navigating the mortgage process when you're self-employed brings up a lot of specific questions. Let's tackle some of the most common ones I hear from clients, clearing up the confusion so you can move forward with confidence.

Can I really get a mortgage with only one year of self-employment?

It’s tougher, but not impossible. Most traditional lenders really want to see a solid two-year track record. However, if you have just one year under your belt, some FHA or conventional loan programs might give you a shot.

The key is proving stability. If you were a W-2 employee in the exact same field before starting your business, that helps your case tremendously. You'll also need a stellar credit score and healthy cash reserves to show the lender you're a reliable borrower.

Insider Tip: This is where alternative loan options really shine. A bank statement loan, for instance, can be much more forgiving. I've seen lenders approve borrowers with just 12 months of business bank statements when the rest of their financial picture is strong.

Do lenders care more about my gross revenue or my net profit?

This is a critical distinction, and the answer completely depends on the type of loan you’re getting.

For any standard loan that requires tax returns (like Conventional or FHA), underwriters are laser-focused on your net income. That’s the bottom-line profit you report on your Schedule C after you’ve written off all your business expenses.

On the other hand, a bank statement loan is built for business owners. Lenders using this method look at your gross deposits—your total business revenue—and then apply a standard expense ratio to figure out your qualifying income. This almost always results in a much higher income figure than what's on your tax returns.

What's the best way to boost my qualifying income before I apply?

If you're planning to buy a home in the next year or two, the single most powerful thing you can do is be strategic about your tax write-offs. It's a classic trade-off: minimizing your tax bill also minimizes the income lenders can use to qualify you.

By consciously reducing your claimed business expenses, you'll show a higher net income on your tax returns. Yes, this means paying more in taxes for a year or two, but that short-term pain can directly translate into a much bigger home loan approval. It's a strategic move that pays off when it matters most.

Ready to turn your entrepreneurial success into homeownership? The expert team at Mortgage Seven LLC can help you navigate your options and find the perfect loan for your unique financial situation. Get started with a personalized consultation today.

Leave a Reply