So, you're thinking about refinancing your mortgage. It's a smart move that can save you a lot of money, but it's not quite as simple as just asking for a new loan. Lenders need to see that you’re a good bet, which means proving you’re financially stable.

Essentially, you're re-applying for your mortgage. This time around, they'll be looking closely at your credit score, your debt-to-income (DTI) ratio, and how much home equity you've built up. It's like a financial check-up to make sure you can comfortably handle the new loan terms.

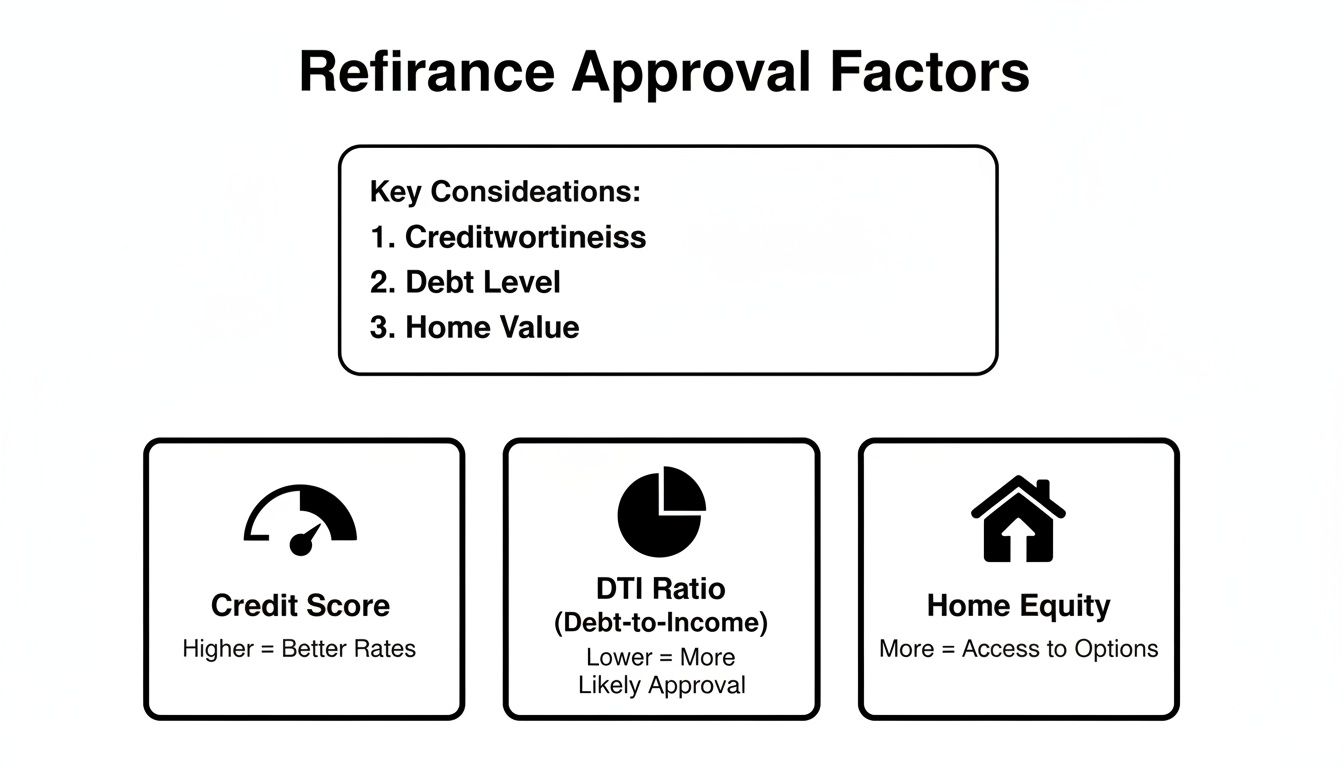

Your Refinance Qualification Roadmap

Before you start filling out any paperwork, it's incredibly helpful to step back and look at your finances through a lender's eyes. When you understand what they care about—and why they care about it—you can put together a much stronger application. Think of this as your inside guide to getting that "approved" stamp.

This infographic breaks down the big three factors that lenders will zero in on.

As you can see, it's not just one thing. Lenders want the full picture, from how you've handled debt in the past to your current monthly budget and the value of the home itself.

The Four Pillars of Approval

When an underwriter reviews your file, they're really focused on four key areas. Getting these four pillars in good shape is your best strategy for locking in a great new rate and terms.

- Credit Score: Your credit score is a snapshot of your borrowing history. A higher score tells lenders you're a low-risk borrower, which is how you get the best interest rates. Generally, you'll need a score of at least 620, but the magic number for top-tier rates is usually 740 or above.

- Debt-to-Income (DTI) Ratio: This one's all about cash flow. DTI is the percentage of your gross monthly income that goes toward paying debts. Lenders want to see you have plenty of breathing room, so for most conventional loans, they're looking for a DTI of 43% or less.

- Home Equity: This is the portion of your home that you actually own, free and clear of your mortgage. It's the lender's security blanket. For most refinance types, you'll need to have at least 20% equity in your home.

- Employment and Income Stability: Lenders need confidence that you can make the new payments, month after month. This means they'll want to see a steady and verifiable income stream, which you'll typically prove with recent pay stubs, W-2s, and tax returns.

Key Takeaway: A winning application isn't about acing just one category. It’s about showing a well-rounded, reliable financial picture across your credit, debt, equity, and income.

To get a better sense of how all these pieces fit together, it helps to understand the complete refinance process from start to finish. Knowing what’s coming next helps you prepare and keep things moving smoothly.

To give you a clearer picture, here’s a quick summary of what lenders are generally looking for.

Key Refinance Qualification Metrics at a Glance

| Qualification Factor | Conventional Loan Target | Government-Backed (FHA/VA) Target | Pro Tip |

|---|---|---|---|

| Credit Score | 620+ (740+ for best rates) | 580+ (lender overlays may require higher) | Check your credit report for errors before applying. Even small fixes can boost your score. |

| Debt-to-Income (DTI) | Below 43% | Can sometimes go up to 50% or more | Pay down small credit card balances or a car loan to quickly lower your DTI. |

| Home Equity | 20% or more | Varies by loan; streamline refis may not require an appraisal. | Cash-out refinances will require more equity (typically 20%) than rate-and-term refis. |

| Income/Employment | 2-year stable history | 2-year stable history | Organize your pay stubs, W-2s, and tax returns ahead of time to speed up the process. |

Remember, these are just general guidelines. Every lender has slightly different criteria, and certain loan programs offer more flexibility.

Building a Credit Score That Opens Doors

When it comes to refinancing your mortgage, your credit score is the first thing a lender looks at. Think of it as your financial report card—it tells them, at a glance, how reliable you are with debt. It's not just about getting approved; a strong score is your ticket to the best interest rates available, which can save you a fortune over the life of the loan.

While you might get your foot in the door with a score around 620 for a conventional loan, the real magic happens once you climb higher. To unlock the most competitive rates, you’ll want to aim for 740 or above. This isn't just about bragging rights; a score in this elite tier signals to lenders that you're a low-risk borrower, and they'll reward you for it.

In fact, pushing your score above 760 could potentially slice as much as 0.5% off your interest rate compared to someone with a lower score. On a sizable loan, that adds up to serious savings month after month. As highlighted in recent refinance trends on Fortune.com, the most qualified borrowers are the ones who benefit most from favorable market conditions.

How to Give Your Score a Boost

The good news is that improving your credit score isn't some mystical process. You don’t need to wait years to see a change. With a few smart, focused actions, you can see a real difference in just a few months, putting you in a much stronger position when you're ready to apply.

Here are a few high-impact strategies I always recommend to clients:

- Go on an Error Hunt: You might be surprised to learn that one in five people have an error on their credit report. Pull your free reports from all three bureaus—Equifax, Experian, and TransUnion—and look for anything that seems off. An incorrect late payment or an account you never opened could be dragging your score down. Dispute any inaccuracies immediately.

- Tackle Your Credit Utilization: This is a big one. Lenders look at how much of your available credit you're using, and they get nervous if it's too high. A good rule of thumb is to keep your balance below 30% of the limit on every single card. For example, on a card with a $10,000 limit, a balance under $3,000 is ideal.

- Put a Freeze on New Credit: In the months before you apply for a refinance, resist the temptation to open new credit cards or take out other loans. Every application triggers a "hard inquiry" on your report, which can temporarily ding your score by a few points.

Here's a Real-World Example: I recently worked with a homeowner who had a 690 credit score and wanted to refinance their $400,000 mortgage. We identified a few quick wins: they paid down $2,000 in credit card debt and successfully disputed an old collection error on their report. Their score jumped to 725 in under two months. That 35-point increase qualified them for a rate that was 0.375% lower, saving them about $85 every single month.

These aren't just hypotheticals; these are the practical steps that make a difference. For a more detailed breakdown, our guide to understanding and improving your credit score offers even more tips to get you ready. A little effort now can lead to a huge financial payoff down the road.

Getting Your Debt-to-Income Ratio in Shape

Think of your debt-to-income (DTI) ratio as a financial stress test that lenders use. It’s a simple but critical calculation: your total monthly debt payments divided by your gross monthly income. That one percentage tells a lender exactly how much of your paycheck is already spoken for, which shows them how comfortably you can afford a new mortgage payment.

A high DTI is a red flag for lenders. It suggests your budget is stretched thin, making a refinanced loan a bigger risk. On the other hand, a low DTI shows you have plenty of breathing room in your budget, making you a much stronger candidate for approval.

Understanding the DTI Thresholds

When it comes to qualifying for a refinance, hitting the right DTI number is non-negotiable. For most conventional loans, lenders draw the line at 43%. This means no more than 43 cents of every dollar you earn (before taxes) can go toward debt.

Some government-backed programs are a bit more flexible. FHA or VA loans might allow a DTI as high as 50% in certain situations. As we see interest rates change, refinance trends shift, often favoring borrowers with solid financial footing. You can actually dig into some fascinating data on this over at ICE Mortgage Technology.

What Counts as Debt? Lenders look at everything. They'll add up all your recurring monthly payments, including your current mortgage (or rent), car loans, student loans, minimum credit card payments, and any personal loans. Don't forget alimony and child support—those count, too.

Actionable Strategies to Lower Your DTI

Is your DTI a little too high for comfort? Don't panic. You have a couple of levers to pull: either reduce your monthly debt or increase your documented income. With a little strategy, you can get that number down.

Here are a few tactics I’ve seen work time and again for my clients:

-

Pay Down Small Balances: The quickest win is to completely wipe out a small monthly payment. Got a credit card with a low balance or a small personal loan? Focus on paying it off. Once that payment is gone for good, your DTI instantly improves.

-

Consolidate High-Interest Debt: Juggling multiple high-interest credit card payments can really inflate your DTI. Rolling them all into a single personal loan with a lower, fixed monthly payment can shrink your total debt outlay each month.

-

Boost and Document Your Income: Every dollar counts, so make sure it's on paper. This includes side hustles, freelance income, or consistent bonuses. If you're self-employed, having two years of tax returns and a current profit-and-loss statement is essential to prove your income is stable.

If old tax debt is weighing down your financial profile, looking into the top tax debt relief options can be a game-changer. Getting that cleared up can dramatically improve how a lender sees your application. By taking these proactive steps, you’re not just lowering a number—you’re setting yourself up for a much smoother path to approval.

Putting Your Home Equity to Work

When it comes to refinancing, your home equity is your most powerful tool—even more so than your credit score or income in many cases. Think of it as the skin you have in the game. It’s simply the gap between what your home is worth today and the remaining balance on your mortgage.

For a lender, that equity is their safety net. It shows you have a real financial stake in the property, which makes you a much safer bet.

This stake is calculated using your loan-to-value (LTV) ratio. Let's say your home is currently valued at $500,000 and you still owe $400,000. Your LTV is 80%, which means you have 20% equity. That 20% figure is the magic number for most conventional refinances.

The Appraisal: Where Your Value Is Proven

You might feel confident about what your home is worth, but lenders need an official, unbiased number to work with. That's where the home appraisal comes in.

A licensed appraiser will come out and do a deep dive into your property. They’ll look at its condition, size, and unique features, then compare it to recent sales of similar homes nearby to land on its fair market value. A strong appraisal can literally change everything, boosting your equity and unlocking better rates. It’s why we always advise clients to finish any value-adding renovations before starting the refi process.

Key Insight: Lenders usually look for at least 20% equity for a standard rate-and-term refinance. If you're pulling cash out, they often want an even bigger cushion—typically requiring you to leave 20-25% equity in the home. As rates have started to come down, a lot of homeowners are discovering they finally have enough equity to make a move. You can see the data on this in a recent ICE Mortgage Monitor report on refinance candidates.

What If You Have Less Than 20% Equity?

Don't panic if you're not quite at the 20% mark. It’s a hurdle, but not necessarily a dead end.

Some government-backed programs are built for this exact situation. FHA and VA streamline refinances, for example, are specifically designed for homeowners with lower equity—and often, they don't even require a new appraisal.

Refinancing can also be the perfect strategy to ditch Private Mortgage Insurance (PMI). If you bought your home with a smaller down payment, you've been paying that extra fee every month. But if your home's value has climbed enough to push you over the 20% equity line, a refinance can get rid of PMI for good, potentially saving you hundreds each month.

Organizing Your Paperwork for a Smooth Approval

I can't stress this enough: a well-organized application is a fast-tracked application. The entire underwriting process really just boils down to one thing: verification. When you hand over a complete and orderly package right from the start, it tells the lender you're a serious, prepared borrower. Trust me, that goes a long way in speeding up your approval timeline.

Think of your paperwork as the evidence that proves everything you've claimed about your income, assets, and creditworthiness. Making an underwriter's job easier is always a good thing.

Your Core Document Checklist

While every lender’s specific list might have slight variations, there’s a standard set of documents you'll almost certainly need. Getting these together before you even apply will save you from that frantic, last-minute scramble that can cause unnecessary delays.

The best approach is to create a dedicated folder, whether it's a physical one or a digital one on your computer, and start gathering the essentials. This isn't just about having the documents; it's about having them ready to go when your loan officer asks.

Here's a breakdown of what lenders need to see and, more importantly, why they need it.

| Refinance Document Checklist |

| :— | :— | :— |

| Document Category | Specific Documents Needed | Why It's Required |

| Proof of Income | – Recent pay stubs (covering the last 30 days)

– W-2 forms (for the past two years) | To confirm you have a stable and sufficient income to repay the new loan. |

| Tax History | – Full federal tax returns (for the past two years)

– All schedules (e.g., Schedule C for self-employed) | To verify your income over a longer period and understand any additional income sources or deductions. |

| Asset Verification | – Bank statements (all pages, for the past two months)

– Investment/retirement account statements | To prove you have the funds (reserves) to cover closing costs and handle mortgage payments. |

| Existing Loan Details | – Most recent mortgage statement

– Home Equity Line of Credit (HELOC) statement, if applicable | To get the exact payoff amount for your current loan and understand your payment history. |

| Property Information | – Homeowners insurance declaration page

– Property tax bill | To ensure the property is properly insured and to calculate your total monthly housing expense (PITI). |

This table covers the basics for most borrowers. Being proactive here will make the whole process feel much less stressful.

For a comprehensive, printable version you can use to check things off as you go, download our free refinance document checklist. It’s designed to make sure you don't miss a single detail.

What If My Situation Is More Complex?

Of course, not everyone is a W-2 employee with a straightforward financial life. If you have a more unique situation, you’ll need to provide a bit more paperwork to paint a clear picture for the underwriter.

Pro Tip: If you're self-employed, don't just rely on tax returns. A current Profit & Loss (P&L) statement and a balance sheet for your business are incredibly important. Having an accountant prepare these adds a significant layer of credibility to your file.

Here are a few other common scenarios:

- Rental Properties: You'll need to provide copies of current lease agreements to document your rental income.

- Gift Funds: If a relative is giving you money to help with closing costs, you’ll need a signed gift letter from them stating the funds are a gift, not a loan.

- Recent Divorce: A copy of your divorce decree may be required to clarify any alimony, child support, or division of assets.

The key is to anticipate what a lender will need to see to understand your full financial story. The more you can provide upfront, the fewer questions and conditions you'll have to deal with later.

Finding the Right Partner for Your Refinance

Figuring out how to qualify for a refinance can feel overwhelming, but you absolutely don't have to go it alone. Your first instinct might be to call your current bank, and while that’s a logical starting point, it’s also a limited one. A bank can only ever offer you its own products, which might not be the best fit or the best deal out there.

This is precisely where a good mortgage broker becomes your secret weapon.

Unlike a bank employee who works for the bank, a broker works for you. Their job is to shop your application around to a whole network of lenders—dozens, in fact—giving you access to a much wider world of loan programs and competitive rates you’d never find on your own.

When a Broker Makes All the Difference

For a straightforward, cookie-cutter loan, a bank might be fine. But if your financial picture has any unique angles, a broker’s expertise can be a game-changer. They thrive on complexity and know exactly which lenders are best for specific situations.

Think about these common scenarios:

- You're Self-Employed: If you're a freelancer or own your own business, proving your income with traditional tax returns can be a nightmare. A seasoned broker knows which lenders offer bank statement or P&L loans and how to package your file for approval.

- You're a Real Estate Investor: Looking for a DSCR (Debt Service Coverage Ratio) loan to finance your next rental property? You need someone who lives and breathes investment financing, not a generalist at a retail bank.

- You Have a Unique ID: An experienced broker can quickly connect borrowers using an ITIN with lenders who have specific programs designed for them, saving you countless hours of searching.

A great mortgage broker is more than just a matchmaker; they're your advocate. They use their industry relationships to push your file through underwriting, solve problems before they start, and translate all the confusing lender jargon into plain English.

To find the best path forward, you'll want to explore various providers offering general mortgage solutions that align with your goals. Here at Mortgage Seven LLC, our entire focus is on understanding your unique situation and finding the lender who will give you the best terms, ensuring your refinance journey is smooth from start to finish.

Got Questions About Refinancing? We've Got Answers.

It's totally normal to have questions pop up, even with the best-laid plans. Getting a handle on the timeline, the real costs involved, and how it all affects your credit score can make the whole refinance process feel a lot less intimidating. Let's dig into a few of the questions we hear all the time from homeowners.

How Long is This Going to Take?

You can generally expect the refinance process to take anywhere from 30 to 45 days, from the moment you hit "submit" on your application to signing the final loan documents.

But that's just a ballpark figure. The actual timeline can shift depending on a few things. If the lender is swamped with applications, things might slow down. The same goes if your financial picture is a bit more complex. And, of course, how fast you get your documents back to them plays a big role. If an appraisal is needed, that alone can add a week or more just for scheduling and getting the report back.

What's the Real Cost of a Refinance?

When it comes to closing costs, a good rule of thumb is to budget for about 2% to 5% of the new loan amount. These fees aren't just random charges; they pay for all the essential services needed to get your new loan across the finish line.

So, what are you actually paying for?

- Appraisal Fee: This covers the cost of a professional appraiser determining your home's current market value.

- Title Insurance: A crucial policy that protects your new lender from any surprise ownership disputes.

- Lender Origination Fees: This is what the lender charges for the work of processing, underwriting, and funding your loan.

- Attorney Fees: Covers the legal oversight and services required to finalize the transaction.

You've probably seen ads for "no-closing-cost" refinances. Just know that those costs don't magically vanish. Lenders typically recoup that money by either adding it to your loan balance or giving you a slightly higher interest rate.

I Just Bought My House. Is It Too Soon to Refinance?

This is a common one. While it's not impossible, most lenders have a "seasoning" requirement, which is just their term for how long you need to have owned the home. For most conventional loans, you'll need to have been in the house for at least six months.

Government-backed loans like FHA and VA have their own set of rules, so there isn't a single answer. If rates have taken a nosedive since you closed on your home, it’s definitely worth talking to a loan officer to see if you qualify.

Expert Tip: Don't be alarmed by the hard credit inquiry. Refinancing will cause a small, temporary dip in your credit score, usually just a few points. As you start making consistent, on-time payments on the new loan, your score will recover and often even improve over the long haul.

Trying to sort through all these details alone can be a headache. Having an expert in your corner makes a world of difference. The team at Mortgage Seven LLC can give you straight answers and help you find the refinance option that truly aligns with your goals. Start a conversation with our team today.