Let’s be honest—buying your first home in this market can feel like an uphill battle. With sky-high prices and a dizzying number of loan options, it's easy to get overwhelmed. This is exactly where a great mortgage broker becomes your most valuable player.

Think of a broker as your personal guide through the mortgage maze. Instead of you having to go from bank to bank, filling out application after application, they do the heavy lifting for you. A good broker takes your unique financial story and shops it around to dozens of different lenders to pinpoint the best rates and loan programs out there. You’re not limited to one bank's menu; you get access to the entire market.

This access dramatically boosts your chances of not only getting approved but also saving a significant amount of money over the life of your loan.

Finding an Edge When the Market is Tough

The numbers don't lie. Recent data revealed that in 2025, the share of first-time homebuyers dropped to a historic low of just 21% of all home sales—the lowest point since the National Association of Realtors started tracking this stuff back in 1981. You can dig into the full report on first-time home buyer trends to see for yourself.

This statistic really drives home why having an expert in your corner is so critical. Savvy first-timers are turning to local mortgage brokers, like our team at Mortgage Seven LLC here in Fairfax, Virginia (NMLS #2124799), because we know how to navigate this landscape. We have deep connections with lenders who offer specialized programs—like FHA loans, ITIN loans, or bank-statement loans—designed for borrowers who don't fit into a perfect little box.

The Broker Advantage for Real-Life Scenarios

Here’s a common situation we see all the time: a self-employed individual with a great, but fluctuating, income. They walk into a big bank, and the automated underwriting system takes one look at their tax returns and spits out an instant "no." It's incredibly disheartening.

A skilled broker, on the other hand, sees that same file and immediately knows which lenders specialize in working with entrepreneurs and non-traditional income. We know how to package your application to highlight your strengths, turning that initial rejection into a confident "yes."

A mortgage broker works for you, not for a single bank. Our goal is to find the loan that fits your life, not to shoehorn you into a product that benefits the lender. That personalized strategy is something you just can't replicate on your own.

To make it even clearer, let's break down the practical differences between working with a broker versus going straight to your bank.

Mortgage Broker vs Direct Lender: A First-Time Buyer's Comparison

This table shows you at-a-glance why having a broker in your corner can be such a game-changer, especially when you're just starting out.

| Feature | Mortgage Broker (e.g., Mortgage Seven LLC) | Direct Lender (e.g., A Bank) |

|---|---|---|

| Loan Options | Access to dozens of lenders and a huge variety of loan products. | Limited to whatever products that one institution offers. |

| Flexibility | Much higher chance of finding loans for unique situations (self-employed, lower credit). | Stricter, more rigid approval criteria are the norm. |

| Guidance | Personalized advice focused on finding the best deal for your specific financial profile. | Advice is centered around selling their own loan products. |

| Rate Shopping | We shop multiple lenders with just one credit pull, protecting your credit score. | Every application at a new bank requires a separate credit pull, which can lower your score. |

Ultimately, by tapping into a broker's expertise and network, you gain a powerful advantage right from the very beginning of your homebuying journey.

Getting Your Financial Ducks in a Row for Pre-Approval

Think of meeting with a mortgage broker less like an application and more like telling your financial story. You're not just handing over papers; you're painting a picture that shows you're a serious, reliable home buyer. Getting everything organized ahead of time doesn't just speed things up—it makes a fantastic first impression.

The whole point is to demonstrate stability. Lenders are looking for a clear, consistent history of you managing your money well. Having all your documents ready before you even pick up the phone shows you mean business.

Why All This Paperwork?

Every single document a mortgage broker requests adds a new chapter to your story. It’s not about being nosy or judging how you spend your money; it’s about verifying that your financial situation fits within established lending guidelines.

-

Pay Stubs & W-2s: These are the basics. They prove your current income and show a consistent work history. Lenders will typically want to see your pay stubs from the last 30 days and your W-2s from the past two years to confirm your earnings are stable.

-

Bank Statements: This is where things get a bit more detailed. A lender will review your last two to three months of bank statements to make sure you have the cash for your down payment and closing costs. They're also on the lookout for a clean, traceable source for that money. A big, unexplained cash deposit can be a huge red flag.

-

Tax Returns: For most people with a regular salary, your last two years of tax returns simply back up what your W-2s show. But if you’re self-employed or have other income sources like a rental property, these documents become the main event, proving your average income over time.

Having all these files scanned and saved in a secure digital folder makes sending them to your broker a breeze. For a complete rundown of everything you'll need, you can grab our first-time home buyer document checklist. It’s a great way to make sure nothing gets missed.

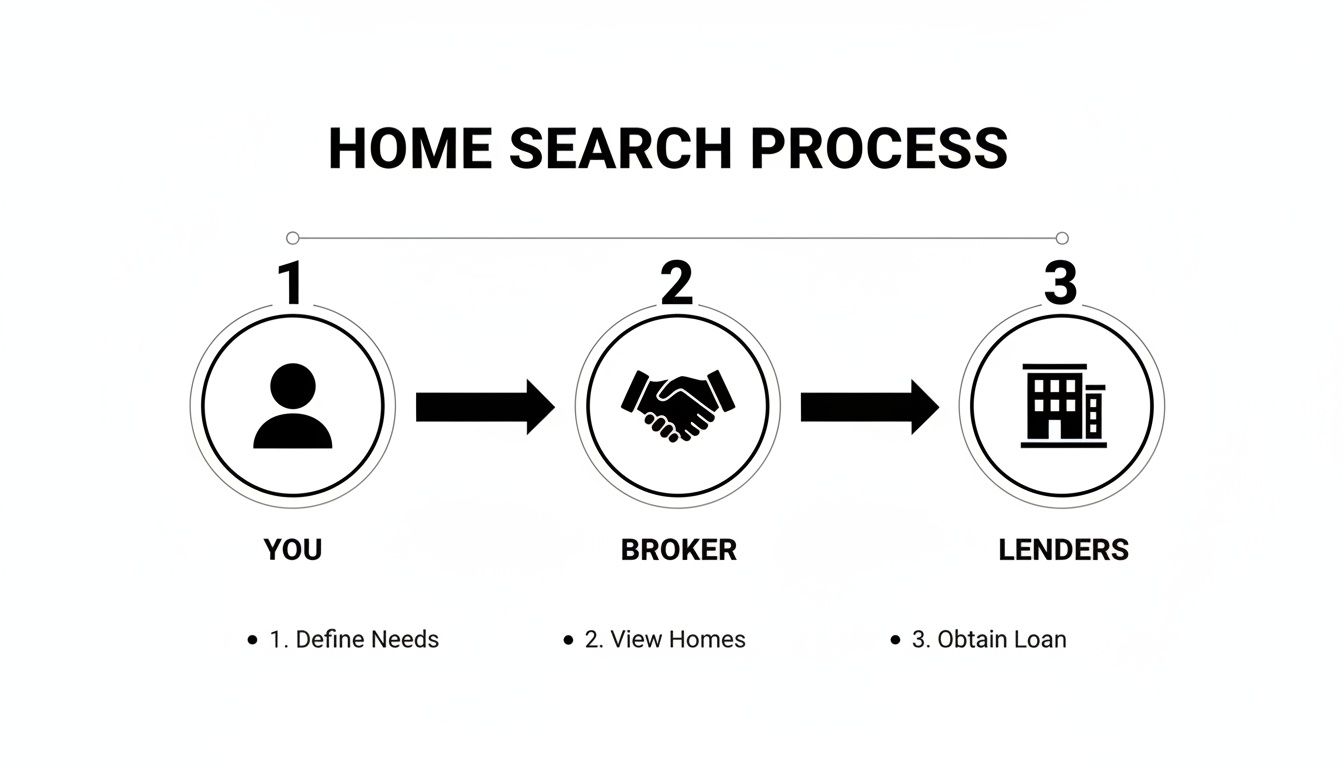

This flowchart shows how a broker is the essential connection between you and the lenders who will ultimately finance your home.

When you pull together your financial documents, you're essentially handing your broker the tools they need to find the right lender for your specific situation, which really boosts your odds of getting approved.

The Story Behind Your Down Payment

Your down payment is a critical part of the equation. As you get your finances ready for pre-approval, it's crucial to understand these upfront costs, especially how to calculate your down payment correctly. The money for it needs to be "seasoned," which is industry-speak meaning it's been sitting in your account for at least 60 days.

Pro Tip: If a family member is giving you money for your down payment, don't just deposit the check! Call your mortgage broker first. They'll walk you through the proper way to document it with a formal "gift letter" so that it meets the lender's strict requirements.

Being proactive like this helps avoid frustrating delays during the underwriting phase and shows the lender you know what you're doing. A clean financial history, without any last-minute surprises or undocumented cash, is your fastest ticket to getting that pre-approval letter. It proves you're an organized, low-risk borrower—exactly the kind of person lenders love to work with.

What to Ask Your Potential Mortgage Broker

Your first sit-down with a mortgage broker is more than just a chat—it’s an interview. You’re essentially hiring a financial partner for one of the biggest investments you'll ever make. This is your chance to see if their expertise, personality, and work ethic are the right fit for you.

Walking in with a solid list of questions is what separates a smooth homebuying journey from a stressful one. You need to dig deeper than the surface-level stuff to find a broker who will genuinely go to bat for you.

Questions About Their Process And Experience

Let's start with the basics. You want to understand how they operate and if they have a track record of helping people in your exact situation. A great broker who frequently works with first-time buyers will have clear, reassuring answers.

- How many lenders do you work with? This is a huge one. A broker connected to dozens of lenders has a much bigger toolbox to pull from. They can shop around for the best rates and find a loan that works, even if your financial picture isn't perfect.

- What percentage of your clients are first-time home buyers? Experience with newcomers is invaluable. A broker like the team at Mortgage Seven LLC, who specializes in guiding first-timers, knows the common fears and roadblocks and can navigate them with ease.

- How do you get paid? Don't be shy about asking this. Most brokers earn a commission from the lender (lender-paid compensation), so it doesn't come directly out of your pocket. Knowing their fee structure upfront avoids any awkward surprises later.

It's also helpful to recognize the operational side of their business, like how mortgage broker services are supported behind the scenes, which allows them to dedicate more time to you.

Questions About Your Specific Scenario

Now, turn the conversation to your situation. A sharp broker should be able to offer some initial strategies right on the spot based on the numbers you share. This gives you a glimpse into how they think.

Here's a powerful question: "Looking at my income, credit, and what I've saved, what are the top three loan programs you'd recommend, and why?" A vague response is a major red flag. A pro will break down the pros and cons of options like an FHA loan versus a 3% down conventional loan and explain which one makes the most sense for you.

Questions About Communication And Problem-Solving

The path to closing day can have a few twists and turns. Underwriting can be tricky, and you need to know how your broker handles the pressure when things get complicated.

- What's the best way to reach you?

- Who will be my main point of contact throughout this process?

- How often can I expect updates on my loan's progress?

- Can you walk me through a recent challenge you faced with a client's loan and how you got it resolved?

That last question is pure gold. It reveals their real-world problem-solving skills and their dedication to seeing a loan through to the finish line. You're looking for an answer that shows they're proactive, a clear communicator, and, most importantly, a reliable guide you can count on.

Decoding Loan Programs for Virginia Home Buyers

Trying to understand the mortgage world for the first time can feel like you're learning a whole new language. You're suddenly hit with a barrage of acronyms—FHA, VA, USDA—and it's completely normal to feel a bit lost in the jargon.

This is where a good mortgage broker becomes your guide. Think of us as your personal translator, breaking down these complex options into clear, simple choices that actually make sense for your life and your goals, especially right here in Fairfax, VA.

We look at the whole picture, not just a credit score on a screen. Our job is to match your unique financial situation with the right loan program so you can confidently step into homeownership.

The Go-To Loans for First-Time Buyers

Most first-time buyers land on one of a few popular loan types, and each one has its own set of strengths. Getting a handle on these basics is the first real step toward making a smart decision.

-

FHA Loans: Backed by the Federal Housing Administration, these are a huge favorite among first-time buyers for a reason. They're designed to be accessible, allowing for down payments as low as 3.5% and offering more flexibility on credit scores.

-

Conventional Loans: These are the loans you get from private lenders, not the government. While they often require a slightly higher credit score, a common myth is that you need 20% down. The reality? Many conventional loan programs are available with as little as 3% down. The big win here is that once you build up 20% equity in your home, you can typically ditch the private mortgage insurance (PMI). To dig deeper, check out this side-by-side comparison of FHA vs. Conventional loans.

-

VA Loans: This is an incredible benefit for our veterans, active-duty service members, and eligible surviving spouses. VA loans usually require zero down payment—that’s right, 0% down—and they don’t have monthly PMI, which frees up a lot of cash in your monthly budget.

The market out there is tough, no question. With the median age of first-time buyers now at a record 40 years in 2025 and repeat buyers making 30% of their offers in all-cash, the competition is fierce. We see people taking on side gigs or getting help from family just to pull together a down payment. This is precisely where a broker can give you an edge, by pinpointing the exact loan that fits your circumstances. NerdWallet.com has some great insights on these trends if you want to learn more.

Popular Loan Options for First Time Home Buyers

To make things a little clearer, I've put together a quick comparison table. This should help you see how the most common loan types stack up and start thinking about which path might be the best fit for your financial profile here in Virginia.

| Loan Type | Typical Down Payment | Best For… | Key Consideration |

|---|---|---|---|

| FHA Loan | 3.5% or more | Buyers with lower credit scores or smaller savings. | Requires mortgage insurance for the life of the loan. |

| Conventional Loan | 3% – 5% | Buyers with solid credit looking to avoid long-term PMI. | Stricter credit and debt-to-income requirements. |

| VA Loan | 0% | Eligible veterans and active-duty military members. | Requires a VA funding fee, but no monthly PMI. |

| Bank Statement Loan | 10% – 20% | Self-employed borrowers and entrepreneurs. | Rates may be slightly higher than traditional loans. |

This table is just a starting point, of course. Your broker will help you weigh the pros and cons of each based on your specific numbers and long-term financial picture.

Looking Beyond the Standard Options

Here’s one of the biggest reasons to work with a mortgage broker: we have access to loan products that most big banks simply don't offer. Our network of lenders is our secret weapon.

Let’s say you’re a small business owner in Virginia. Your tax returns are full of write-offs that lower your taxable income—which is smart—but it doesn't show your real cash flow. A traditional bank’s automated underwriting system will likely take one look and stamp "denied."

A broker, on the other hand, can connect you with lenders who offer Bank Statement Loans. These programs are a game-changer for entrepreneurs because they use your business bank statements to prove your income, not your tax returns.

Finding the right loan isn't just about qualifying. It's about finding the one that makes financial sense for your future. A broker's job is to present all viable paths, not just the most obvious ones.

Common Mistakes First-Time Home Buyers Make (and How to Avoid Them)

Knowing the right steps to take on your home buying journey is only half the battle. What’s just as important is knowing what not to do, especially during that critical window between getting your pre-approval and sitting down at the closing table.

Think of your loan approval as a snapshot of your finances at a specific moment. Any major financial move after that picture is taken can throw the whole thing into question.

This is where a good mortgage broker becomes your financial co-pilot. We're here to steer you clear of the common mistakes that can sink a loan application. And believe me, these aren't just hypotheticals—we see them happen all the time, and they can be heartbreakingly easy to make.

Here's the golden rule: Once you are pre-approved, don't change a single thing about your finances without talking to your broker first. That means your job, your credit, your savings… everything.

The Big Financial "Don'ts" After Pre-Approval

Consider the time after you're pre-approved a "financial quiet period." The lender's underwriter will double-check everything right before you close, and any new, unexpected activity is an instant red flag.

Here are the most frequent blunders we help our clients in Fairfax, VA, steer clear of:

- Making Large, Undocumented Cash Deposits. Lenders need a crystal-clear paper trail for every dollar. A sudden, unexplained cash deposit of $5,000 looks incredibly suspicious and can bring your application to a screeching halt until you prove exactly where it came from.

- Applying for New Credit or Co-signing. This is a huge one. Whether you're opening a new credit card to get a discount, financing a living room set, or co-signing on a car for your cousin, it creates a new inquiry on your credit report and can mess up your debt-to-income ratio.

- Changing Jobs. You'd think a promotion with a pay raise would be a good thing, right? Well, not always. Lenders prize stability above all else, and a new job—even a better one—often comes with a probationary period, which can be a deal-breaker for an underwriter.

These actions might seem innocent enough, but to a lender, they signal new risk.

A Real-World Example: The Pre-Closing Couch Purchase. I once worked with a first-time buyer who had a perfect pre-approval. About a week before closing, they found their dream sofa during a "no payments for 12 months" sale. They applied for the store credit, and that small inquiry and new debt was just enough to tip their debt-to-income ratio over the lender's strict limit. We had to scramble to restructure the entire loan, and it nearly delayed their closing.

How to Keep Your Loan on Track

The solution is straightforward, but it takes a little discipline. Once that pre-approval letter is in your hands, your new mission is to keep your financial life as boring as possible.

Keep paying every bill on time, continue saving money, and fight the urge to start shopping for furniture and appliances. You'll have plenty of time for that once you have the keys.

When in doubt, just call your broker. Seriously. A quick, two-minute phone call can save you from a massive headache and ensure your path to the closing table stays smooth and stress-free.

Your Top Home Buyer Questions Answered

Even with the most detailed plan, you're going to have questions as you start seriously looking at homes. That's completely normal. Buying your first home is a huge step, and there’s a lot to wrap your head around.

Think of this as your quick-reference guide for the questions that pop up most often. Getting straight answers is the best way to feel confident and ready to make a move. Let's tackle some of the big ones.

How Do Mortgage Brokers Get Paid?

This is easily the most common question we get, and for good reason—you need to know where the money is going. For most loans, especially when working with a mortgage broker for first time home buyer clients, our compensation comes directly from the wholesale lender who ultimately funds your mortgage.

This is known as lender-paid compensation. The fee is a small percentage of the final loan amount and is already factored into the interest rate you're offered. The beauty of this setup is that you don’t have to cut us a separate check. It aligns our goals perfectly: we succeed when we find you the right loan that closes successfully.

How Long Does a Pre-Approval Last?

Your pre-approval letter is a powerful tool, but it does have an expiration date. Typically, you can count on it being valid for 60 to 90 days.

Why does it expire? Simple: life happens. Your financial picture—credit score, income, debt—can change over time. Lenders need to work with current information to ensure you still qualify for the loan. If your house hunt takes a bit longer than expected, don't sweat it. Renewing a pre-approval is usually just a matter of providing a few updated documents.

A strong pre-approval letter isn't just a piece of paper; it's your golden ticket in a competitive market. It proves to sellers you’re a serious buyer who can back up their offer.

What Happens if the Appraisal Comes in Low?

This scenario can definitely cause some anxiety, but a low appraisal doesn't have to be a deal-breaker. It just means the appraiser's professional opinion of the home's value is less than what you offered. Since the lender will only finance up to the appraised value, you have a few potential paths forward.

Here are the most common options:

- Negotiate: Your agent can go back to the seller and ask them to lower the price to match the new value.

- Bridge the Gap: You can choose to pay the difference between the offer and the appraisal out of your own pocket.

- Challenge It: You can submit an appraisal rebuttal with new data, but success here isn't guaranteed.

- Walk Away: If your contract includes an appraisal contingency, you can cancel the deal and get your earnest money back.

This is where having an experienced mortgage broker and real estate agent in your corner is invaluable. We can help you weigh the pros and cons and figure out the smartest move. For even more answers, check out our complete First-Time Home Buyer FAQ page.

You don't have to figure all this out on your own. The team at Mortgage Seven LLC is here to give you clear answers and guide you from start to finish. Schedule your free consultation today!