Choosing how to finance a home is one of the biggest decisions you'll make, and it starts with a fundamental question: Should you work with a mortgage broker or go directly to a bank? The answer boils down to one key distinction.

A mortgage broker is like a personal shopper for home loans. They have access to a whole network of lenders and their job is to find the best loan for your specific situation. A bank, on the other hand, is a direct lender. They only sell their own products. Your choice really depends on what you value more—a wide selection and expert guidance, or the familiarity of working with a single financial institution.

Understanding The Core Difference Between A Broker And A Bank

When you're ready to get a mortgage, you're faced with two very different paths. The whole "broker versus bank" conversation is about understanding these distinct models, because each one offers a unique experience. Getting this right from the start helps you align your financing strategy with your personal financial goals.

Going straight to a bank or credit union means you're dealing with a direct lender. Their loan officers are employees who can only offer you the mortgage products their specific institution has created. This can feel straightforward and simple, especially if it’s a bank you already use for checking or savings.

A mortgage broker, however, is an independent professional who acts as a middleman. They aren't tied to any single lender. Instead, they work for you, connecting you with a wide array of lenders—from major banks to smaller, niche lenders you might never find on your own.

This difference is everything. It impacts the variety of loans you can access, the interest rates you're offered, and the kind of personalized service you'll get along the way. You can see how these differences play out by looking at the specific mortgage application processes for each.

The market itself shows a clear trend. Independent mortgage banks and brokers are gaining significant traction, with their market share growing from 50% in 2022 to an estimated 53% by 2024. During that same period, the big national banks saw their share drop from 20% to 15%. This shift tells us that more and more borrowers are seeing the real advantages of the choice and flexibility that brokers offer.

For a simple side-by-side, this table breaks down the essentials.

Quick Look: Mortgage Broker vs Direct Bank Lender

Let’s quickly distill this down. The table below gives you a snapshot of the fundamental roles and loyalties of each.

| Attribute | Mortgage Broker | Bank (Direct Lender) |

|---|---|---|

| Primary Function | Acts as an intermediary, shopping for loans across multiple lenders. | Lends money directly to the borrower using its own funds and products. |

| Product Access | Offers a wide variety of loan programs from a diverse network of lenders. | Limited to its own suite of in-house mortgage products. |

| Service Model | Provides personalized guidance to find the best-fit lender and loan for you. | Loan officer serves as a representative of the single banking institution. |

| Allegiance | Works for you, the borrower, to navigate the lending market. | Works for the bank, aiming to sell the bank's mortgage products. |

Essentially, a broker's loyalty is to you, the borrower. A bank's loan officer, as an employee, works for the bank. This single fact is often the most important differentiator for many homebuyers.

Comparing Brokers And Banks Across Key Financial Factors

When it's time to get a home loan, your main goal is simple: get the best deal possible. But "best" isn't just about the advertised interest rate. You have to look at the whole picture—from fees to the type of loan you actually get. Both mortgage brokers and banks have their own financial pros and cons, and figuring them out is the key to making the right choice.

The biggest difference boils down to their business models. A bank is like a retail store selling its own brand of products. A broker, on the other hand, is like a massive marketplace, giving you access to products from dozens of different lenders. This single distinction impacts everything from the rates you're offered to how flexible the approval process is.

In-Depth Comparison: Broker vs. Bank Performance

To really understand the practical differences, it helps to see how brokers and banks stack up in the areas that matter most to you as a borrower. This table breaks down their performance across key functions, from the variety of loans they offer to how fast they can get your loan approved.

| Feature | Mortgage Broker | Bank | Key Takeaway for Borrowers |

|---|---|---|---|

| Product Variety | Extensive. Access to dozens of lenders, including niche products for unique situations (self-employed, investors). | Limited. Offers only its own set of standard loan products (Conventional, FHA, VA, Jumbo). | A broker is your best bet if you don't fit the perfect "W-2 employee, great credit" box. |

| Rate Competitiveness | Highly Competitive. Shops your loan with multiple wholesale lenders to create a bidding environment. | Hit or Miss. Offers its own retail rate. It might be good, but you won't know without shopping around yourself. | Brokers almost always have a structural advantage in finding the most competitive rate on any given day. |

| Approval Speed | Often Faster. Knows which lenders are quickest and how to package a file for a smooth underwriting process. | Variable. Can be slow due to internal bureaucracy and multiple departments. | If speed is critical, a good broker can act as a project manager to push your loan through efficiently. |

| Fees & Compensation | Typically paid by the lender (commission). Borrower-paid options exist. Clear disclosure on the Loan Estimate. | Fees (application, origination) are charged directly to the borrower. Loan officers are salaried/commissioned. | Don't assume a broker costs more. Their wholesale rate access often leads to a lower overall cost, even with their compensation. |

| Flexibility & Underwriting | Highly Flexible. Can find lenders with more lenient guidelines for credit, income, or property type. | Rigid. Must adhere to its own strict, internal underwriting guidelines. Less room for exceptions. | A broker can find a "yes" when a bank says "no" by finding a lender whose rules fit your situation. |

Ultimately, a broker’s main advantage is choice. They provide a strategic, market-wide approach, while a bank offers a more direct but limited path. Your personal financial situation will determine which of these models serves you best.

Interest Rates And Access To The Market

One of the first things people ask is, "Can a broker really get me a lower interest rate?" The answer is often yes, but it's not because they have some secret magic. It’s all about market access. A good broker can pull wholesale rates from dozens of lenders at once, making them compete for your business.

A bank can only offer you its own retail rates. If they happen to have the best deal on the market that day, great! But if they don't, you'd have to call ten other banks to find that out yourself. A broker does all that legwork in a single step.

Key Insight: A broker’s value isn’t just finding a lower rate; it's the comprehensive market scan they perform. This ensures the rate you get is genuinely competitive across a broad spectrum of lenders, not just the best a single institution can offer.

This access is more important than ever. In many places, banks have become incredibly reliant on brokers. Take Australia, for example, where a massive 70-80% of all home loans come through the broker channel. Some banks, like Macquarie Bank, source 97% of their mortgage business from brokers. They need brokers to bring them customers.

Fees And Total Borrowing Costs

The conversation about cost needs to go way beyond the interest rate. Both brokers and banks have fees, but they work differently. Getting a handle on this is crucial for figuring out your true borrowing cost.

Banks usually charge you directly for things like application fees, origination fees, or processing fees, which all get bundled into your closing costs. The loan officer you're working with gets a salary and maybe a commission, but that's all part of the bank's cost of doing business, which is baked into the rates and fees they quote you.

Mortgage brokers get paid in a couple of ways:

- Lender-Paid Compensation: This is how it works most of the time. The lender who funds your loan pays the broker a commission. This payment happens behind the scenes and doesn't come directly out of your pocket.

- Borrower-Paid Compensation: Less common for standard loans, but sometimes you might pay the broker a flat fee, which will be clearly spelled out on your loan estimate. This can happen in more complex borrowing situations.

It's a common myth that using a broker is automatically more expensive. Because they work on thinner margins and bring lenders a high volume of business, the wholesale rates they unlock can easily save you more than what they're compensated. To see the real impact, you need to compare apples to apples. A good mortgage calculator can help you lay out different loan offers side-by-side to see the true lifetime cost.

Variety And Flexibility Of Loan Products

This is where the difference between a broker and a bank becomes night and day. A bank has its set menu of loans—conventional, FHA, VA, and maybe a jumbo option. If your financial situation doesn't fit neatly into one of their boxes, you're likely out of luck.

A broker, on the other hand, has a catalog of loan programs from a huge range of lenders. This is a total game-changer for anyone with a less-than-perfect or unique financial profile.

Think about these real-world scenarios:

- Self-Employed Borrowers: Banks often stumble when it comes to non-traditional income. A broker knows which lenders specialize in loans based on bank statements or a P&L, no W-2s required.

- Real Estate Investors: Brokers work with lenders that offer specialized investor loans, like DSCR (Debt Service Coverage Ratio) loans that qualify you on the property’s cash flow, not your personal income.

- Credit Challenges: If your credit score is a few points shy of what a big bank requires, a broker will know a lender with more forgiving credit standards.

This flexibility is why a broker can often salvage a deal after a bank has already said no. They aren't stuck with one set of rules. Before you get too far, it’s a smart move to play with the numbers yourself using our collection of mortgage calculators to see how different loan types could impact your monthly budget.

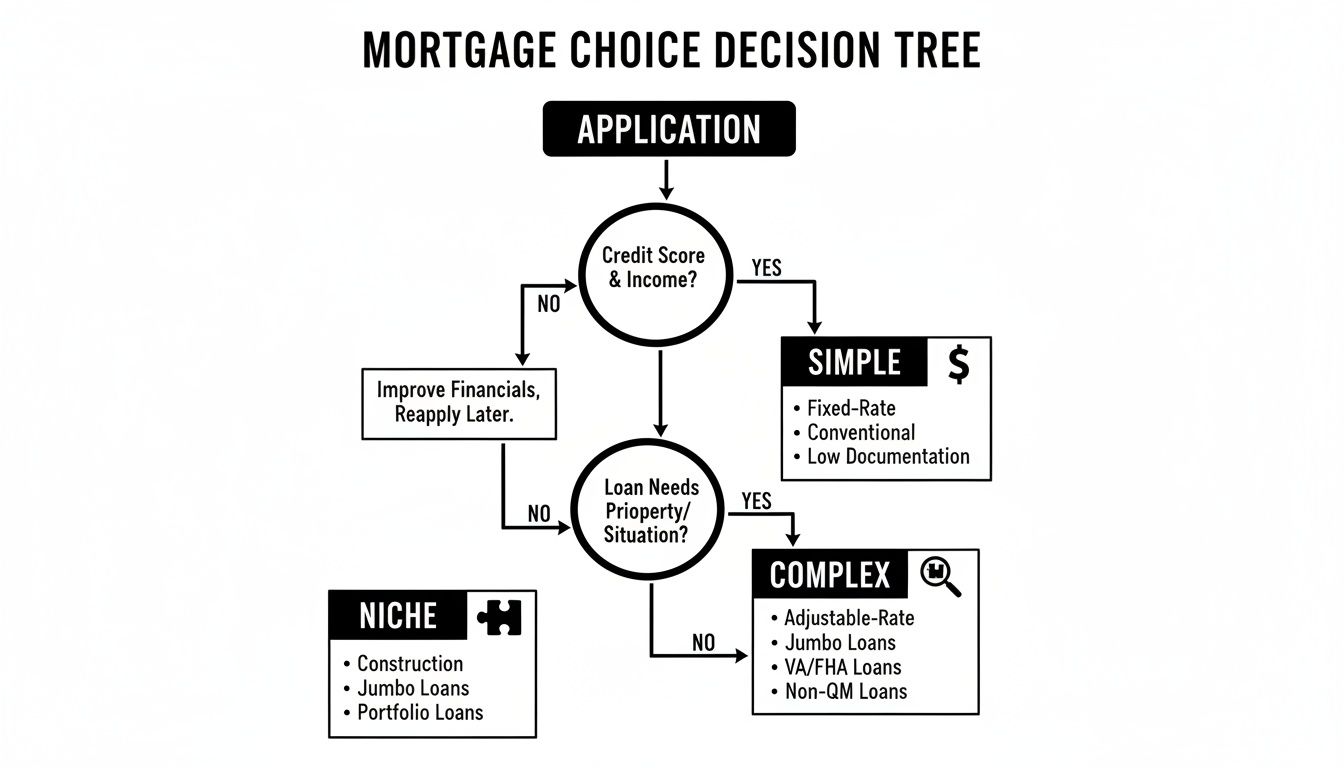

Which Lender Is Right For Your Specific Situation

The whole "mortgage broker vs. bank" debate isn't about finding one right answer for everyone. It's about finding the right partner for your unique financial story. A borrower with a straightforward W-2 job and stellar credit has completely different needs than a self-employed entrepreneur or a seasoned real estate investor. Your specific circumstances are what will ultimately point you toward the smoother, more affordable path to getting a loan.

Think of it this way: choosing a lender is like picking the right tool for a job. For some, a simple hammer from the local hardware store (the bank) is all they need. But for others, a specialized toolkit with multiple attachments (the broker) is the only way to get the project done right.

This decision tree gives you a good visual of how the complexity of your finances can help you decide between a bank and a broker.

As you can see, the more complex or niche your borrowing needs are, the more sense it makes to explore the multi-lender approach a broker offers.

For First-Time Home Buyers

Jumping into the mortgage process for the first time can feel like learning a new language. You're suddenly hit with terms like LTV, DTI, and PMI, and it’s easy to feel overwhelmed. This is where getting personalized guidance is an absolute game-changer.

A bank can be a perfectly good choice if you have a simple financial profile and already have a good relationship with them. The loan officer can walk you through their specific products, and that sense of familiarity can be really comforting.

However, this is where a mortgage broker really shines. Their job is to educate and guide you through the entire market, not just the products from a single institution. They can lay out the pros and cons of an FHA loan versus a conventional one from multiple lenders, helping you find a program with a lower down payment or more forgiving credit requirements.

Key Takeaway: For first-timers who need a bit more hand-holding and want to be sure they’re seeing all the low-down-payment options out there, a broker’s advisory role and wide market access give them a clear edge.

For The Self-Employed Borrower

If you run your own business or work as a freelancer, you know that documenting your income is rarely a simple affair. Traditional banks often hit a wall here because their underwriting systems are built for predictable W-2 income and neat pay stubs. Your tax returns, which probably show significant write-offs, could lead to a quick denial even if your business is thriving.

This is one scenario where a mortgage broker isn't just a good idea—it's often essential. Brokers build relationships with lenders who specialize in non-traditional income and know exactly how to handle your situation.

A broker can connect you with lenders offering:

- Bank Statement Loans: These programs use your business or personal bank deposit history to calculate your income, completely bypassing the need for tax returns.

- Profit & Loss (P&L) Loans: Some lenders will accept a P&L statement prepared by a CPA to verify your income instead.

- Asset-Based Loans: For borrowers with significant liquid assets, these loans qualify you based on your wealth, not a documented income stream.

A bank simply doesn't have these specialized tools in its toolbox. For a self-employed person, a broker moves from being a convenience to a necessity.

For The Real Estate Investor

Real estate investors need three things: speed, flexibility, and access to loan products that help them grow their portfolios. A typical bank, with its one-size-fits-all approach and rigid underwriting, is rarely set up to meet these demands.

Investors often need to jump on a property fast or use creative financing strategies, and that’s where brokers are perfectly positioned to help. They work with a whole network of lenders that cater specifically to investors, including those offering DSCR (Debt Service Coverage Ratio) loans. These are fantastic because they qualify you based on the property’s rental income, not your personal income.

This allows an investor to buy multiple properties without their personal debt-to-income ratio getting in the way. Brokers can also find lenders offering more favorable terms for investment properties, like interest-only options or portfolio loans that cover multiple properties under one mortgage. When you start exploring, platforms that help you find reputable mortgage brokers can be a great place to start your search.

For The Homeowner Looking To Refinance

When you're refinancing, your goal is usually to lower your interest rate, shorten your loan term, or pull cash out of your home's equity. While going back to your current bank might seem like the easiest route, it’s rarely the most competitive. They already have your business, so they may not be motivated to offer you their absolute best deal.

Shopping your refinance with a mortgage broker forces lenders to compete for your business. Even a small 0.25% reduction in your interest rate can save you tens of thousands of dollars over the life of the loan. A broker can quickly pull quotes and compare closing costs from dozens of lenders, making sure you get the most financially sound deal.

The market is always in flux, so what was true last year might not be true today. A good broker helps you navigate these trends to find the best current offers, whether they come from a big, stable bank or a more nimble nonbank lender.

Essential Questions To Ask Before You Commit

Deciding between a mortgage broker and a bank is a huge financial step. The best way to feel confident in your choice is to know exactly what to ask. Before you sign anything, you need to interview them—whether it's a broker or a bank's loan officer—to make sure they're the right fit for your goals. This is about more than just getting the lowest rate; it's about finding a transparent, skilled partner for one of the biggest purchases of your life.

The answers you get back will tell you everything you need to know about their process, how they get paid, and what they do when things get complicated. Think of it like you're hiring for a critical job. You need someone who knows their stuff, communicates clearly, and truly has your back.

Questions About Fees and Compensation

You absolutely have to understand how your loan professional gets paid. It tells you a lot about their incentives. If you get vague answers about costs, consider it a giant red flag. Push for total clarity on every single dollar.

- How do you get paid for this loan? A broker should tell you upfront if the lender pays them (which is most common) or if you'll be paying their fee directly. A bank loan officer should be able to explain their commission or salary structure.

- Can you give me a detailed breakdown of all the fees? Ask for a Loan Estimate or a fee worksheet. This document should spell out every single cost—from origination fees and points to appraisal and title charges.

- Could any of these fees change before we close? A true professional will be honest about what might cause costs to shift, like a drop in your credit score or a last-minute change to the loan program.

Questions About The Loan Process and Timeline

Getting from application to closing day has a lot of moving parts. You need a clear roadmap of what's ahead to avoid surprises. These questions help you set realistic expectations and spot potential bumps in the road early.

Pro Tip: Ask them to estimate a timeline from application to closing for someone with a financial profile like yours. A seasoned pro can usually give you a solid estimate, typically somewhere between 30 to 45 days, and can also explain what might make things move faster or slower.

It’s also smart to find out who you'll be dealing with day-to-day. Will you have one dedicated point of contact, or will you be passed along to a team? Also, ask them what documents they need from you right away to get the ball rolling and make underwriting as smooth as possible.

Finally, one of the best questions you can ask is this: "What are the biggest potential hurdles for my loan, and how do you plan to handle them?" This single question shows you how experienced and proactive they are, which is exactly what you need if things don't go perfectly. Getting your documents ready ahead of time is a huge help, and our home loan application checklist is a great resource to get you organized.

Questions For A Mortgage Broker

- How many lenders do you work with, and who do you think is the best match for me? This gives you a feel for how many options they can actually bring to the table.

- What's our plan B if the first lender denies the loan? A great broker won't just have one option in mind; they'll be ready to pivot to another lender without missing a beat.

Questions For A Bank Loan Officer

- What makes your bank's loan programs better than what else is out there? This pushes them to explain the real value they offer, beyond just the convenience of working with your current bank.

- If I don't fit into your standard loan boxes, do you offer any portfolio loans or other solutions? This is a key question to gauge their flexibility, especially if your financial situation isn't cookie-cutter.

How to Make Your Final Decision

Alright, we've covered a lot of ground. Now it's time to land the plane and decide which path—broker or bank—is the right one for you. There’s no magic formula here. The best choice simply comes down to your financial picture, your personality, and what you value most in this process.

Think of this as the final gut check. Let's walk through a few key questions to help you synthesize everything and move forward with confidence.

Your Personal Decision Checklist

- How complex is your financial life? If you have a straightforward W-2 job and a great credit score, a bank can be an easy, direct route. But if you're self-employed, have some credit hiccups, or your income streams are unconventional, a broker is built for that kind of complexity.

- Do you want a curated menu or the whole buffet? A bank will show you their specific loan products—which can be great—but a broker opens the door to dozens of lenders and a much wider array of options.

- How much hands-on guidance do you need? A broker’s job is to be your market guide, navigating you through multiple lenders to find the perfect fit. A bank's loan officer is an expert, but only on their institution's products.

- Is your banking relationship a big deal? If you've banked with the same institution for years and have a great relationship, don't discount that. Sometimes loyalty perks and the comfort of familiarity can tip the scales.

- How much time do you want to spend shopping? A broker does all the rate shopping and comparison work for you. If you go directly to a bank, you're the one responsible for calling other lenders to see if you're truly getting a good deal.

Running through these points should give you a pretty clear idea of which direction to lean. Your gut feeling after answering these is probably the right one.

When a Mortgage Broker Is Likely Your Best Bet

For some people, a mortgage broker isn't just an option; they're a game-changer. Their real power comes into play when your situation requires more than a one-size-fits-all solution.

You're a prime candidate for a mortgage broker if you are self-employed, a real estate investor, have a credit score that needs a bit of flexibility, or simply want an expert to shop the entire market to ensure you get the absolute best deal available.

Think of it this way: if your financial story has a unique chapter or two, a broker's network and problem-solving skills are exactly what you need. They specialize in finding the lender who will say "yes" when a big bank's rigid rulebook might lead to a "no."

When Going Directly to a Bank Makes More Sense

Brokers bring a ton to the table, but that doesn't mean going straight to your bank is a bad move. In fact, for some borrowers, it’s the most logical and efficient choice. This is especially true when simplicity is your top priority.

A bank is often the right call if you have a strong, long-term relationship with them and your finances are clean and simple (think excellent credit and steady W-2 income). They might offer relationship discounts or preferred pricing to keep your business, and the convenience of having everything under one roof is hard to beat. If you trust your bank and value that streamlined experience, it can be the path of least resistance.

Got Questions? We’ve Got Answers

Even after laying it all out, you might still be wrestling with a few specific questions. Let's tackle some of the most common ones that pop up when people are deciding between a mortgage broker and a bank.

How Do Mortgage Brokers Get Paid?

This is a big one, and it's important to understand. In almost every case, the mortgage broker is paid a commission by the wholesale lender who funds your loan. This is called lender-paid compensation.

You'll see this fee on your official Loan Estimate, but it's not a separate check you write at closing. Think of it this way: brokers bring a steady flow of business to lenders, so they get access to wholesale interest rates—the kind of rates that aren't available to the general public. That built-in margin is usually enough to cover the broker's fee while still leaving you with a fantastic deal, often better than what a bank could offer directly. On rare occasions for very complex loans, a borrower might pay the broker directly, but that’s something discussed and agreed upon upfront.

Is a Mortgage Broker Always Cheaper?

More often than not, yes. A broker’s entire business model is built on making lenders compete for your loan. On any given day, it’s a safe bet that at least one of their dozens of lending partners will have a better rate and fee structure than the single option your local bank has on its menu.

That said, there are exceptions. If you have a long, deep relationship with your bank—think significant deposits, investments, and multiple accounts—they might roll out the red carpet with special discounts to keep your business. The only way to know for sure is to get an official Loan Estimate from both a broker and a bank and compare them, apple to apples.

The Bottom Line: The "cheapest" loan isn't just about the lowest interest rate. It's the total cost over time, including all the fees. A broker's ability to shop your loan across the entire market gives them a massive advantage in finding the lowest true cost.

Can a Broker Guarantee a Better Interest Rate?

No one can guarantee an interest rate until it's locked in. Rates fluctuate with the market every single day, sometimes even every hour. A broker can't promise you a specific rate before you're approved and ready to pull the trigger.

What a great broker can guarantee is that they'll scour the market to find the most competitive rate available for your exact financial situation at that exact moment. Their real value is their access and their power to create a bidding war among lenders—which is your best shot at landing a great rate.

What Happens After My Broker Gets the Loan Approved?

Once the lender gives the green light, your broker switches hats from shopper to project manager. Their job is to quarterback the entire process. They'll work hand-in-hand with the lender's underwriting and closing teams, the title company, and your real estate agent to make sure every box is checked and all the paperwork is flawless.

Your broker becomes the central hub for communication, coordinating all the moving pieces to get you to the closing table on time and without any drama. They'll schedule the final signing, walk you through the closing statement line by line, and make sure you're comfortable with everything before you sign on the dotted line.

At Mortgage Seven LLC, our goal is to give you clear answers and expert guidance every step of the way. If you're ready to see what a dedicated broker can do for you and simplify your home financing journey, schedule a consultation with our team today.