Building a home from the ground up is an exciting journey, but the financing can feel complicated. That’s where a one-time close construction loan comes in, simplifying the entire process into a single, streamlined transaction.

Think of it as an all-in-one loan that covers both building your home and your final mortgage. This means you go through the application, approval, and closing process just once, which can save you a significant amount of time, money, and headaches.

The All-in-One Pass for Building Your Dream Home

Imagine your home-building adventure in two parts. First, you have the construction phase—the busy period with contractors, materials, and a whole lot of progress. The second part is when you finally move in and start making memories. A one-time close loan is like a single ticket that gets you through both parts of this journey without any extra stops.

Instead of juggling two separate loans—a short-term one for the build and a permanent mortgage later—this loan bundles them together. The beauty of this single-closing model is the predictability and security it offers right from the start.

One Loan, Two Distinct Phases

Even though it’s a single loan, it works in two clear stages. Getting a handle on this is key to seeing its real value.

- The Construction Period: During this initial phase, the loan’s job is to pay your builder. Funds are released in a series of payments called "draws" as specific construction milestones are hit. A great feature here is that you typically only pay interest on the money that's been paid out so far, not the full loan amount.

- The Permanent Mortgage: Once the last nail is hammered in and you have the keys, the loan automatically converts into a standard mortgage. This is when you’ll start making your regular principal and interest payments, just like with any other home loan.

This seamless transition is the core benefit of the one-time close loan. It eliminates the need to requalify for a mortgage when the home is finished, protecting you from potential changes in your financial situation or rising interest rates during the construction period.

Why Is This Approach So Popular?

For anyone who's ever built a house, the simplicity and security here are a huge deal. It takes a massive amount of financial uncertainty off the table. You break ground knowing your long-term financing is already locked in and ready to go.

This isn’t just a niche product; it’s incredibly common. In fact, a National Association of Home Builders survey found that builders reported an average of 63% of the single-family homes they built were financed this way for the home buyer. It’s clear this has become the preferred path for many.

By locking everything in upfront, you dodge a mountain of redundant paperwork, avoid paying for a second set of closing costs, and sidestep the stress of having to secure financing at the last minute. To learn more about how this financing works in practice, explore the details of the construction loan process with Mortgage Seven. It’s easy to see why so many people choose this simpler, more predictable route to build their dream home.

One Time Close vs. Two Time Close: What’s the Difference?

To really see why the one time close construction loan is so appealing, it helps to look at the alternative. The traditional approach, known as a two time close loan, splits the process into two completely separate loans, which introduces a few hurdles the single-close loan was specifically designed to avoid.

Think of the two-close process like this: first, you apply for and get a short-term loan just to cover the build. Once the house is finally finished, you have to start all over again, applying for a completely new, permanent mortgage. A lot can happen in the 9 to 12 months it takes to build a home, and that’s where the risk comes in.

The Double Qualification Gauntlet

With a two time close loan, you’re basically jumping through the same hoop twice. You have to qualify for the initial construction loan to get started. Then, after the last nail is hammered in, you have to requalify all over again for your permanent mortgage.

This second qualification is the biggest gamble of the whole process. If anything about your financial picture changes during the build—a new job, a dip in your credit score, an unexpected car loan—you could be denied that final mortgage. You'd be left with a brand-new house you can't get long-term financing for. This is the exact nightmare scenario a one time close loan eliminates by getting you approved for everything from day one.

The single close loan offers what every home builder craves most: certainty. By locking in your permanent financing before a single shovel breaks ground, you're protected from the risk of not qualifying for a mortgage on your own finished home.

Dodging Interest Rate Volatility

The financial markets are always moving, and they won't pause just because your home is under construction. With a two time close loan, the interest rate for your permanent mortgage isn't locked in until after the build is complete. If market rates climb while your house is being framed—which is not uncommon—you could be stuck with a much higher monthly payment than you ever budgeted for.

A one time close construction loan, on the other hand, lets you lock in your permanent mortgage interest rate right at the start. This is a huge advantage. It shields you from market swings and gives you a predictable, stable long-term housing payment. You can plan your future budget with confidence, knowing exactly what you'll owe when you move in.

One Closing Table or Two?

Closing on any loan comes with a pile of fees for appraisals, title searches, attorney reviews, and more. A two-time close process means you pay for all of that twice—once for the construction loan, and then again for the permanent mortgage.

That duplication can easily add thousands of dollars to your project's bottom line. The single-close structure consolidates everything into one event, which means one set of closing costs. It's a simpler process that offers significant savings. And remember, beyond these two main types, there are various construction financing options available that might fit different needs.

To make the comparison crystal clear, here’s a simple breakdown of how the two loan types stack up against each other.

One Time Close vs. Two Time Close Construction Loans

The table below lays out the key differences, showing why so many people building a home prefer the security and simplicity of a single transaction.

| Feature | One Time Close Loan | Two Time Close Loan |

|---|---|---|

| Closings | A single closing event for both construction and permanent loans. | Two separate closings are required, one for each loan. |

| Closing Costs | One set of closing costs, saving you money. | You pay closing costs twice, increasing overall expenses. |

| Qualification | You qualify once at the beginning of the entire process. | You must qualify twice, once for each loan. |

| Interest Rate | Permanent mortgage rate is locked in before construction starts. | Permanent rate is subject to market changes during construction. |

| Risk Factor | Low risk; your permanent financing is secured upfront. | High risk; changes in finances or rates can jeopardize final loan. |

As you can see, the one time close loan is built for peace of mind, removing the major financial uncertainties that can pop up during a long construction project.

Your Step-by-Step Guide to the Loan Process

The journey of a one-time close construction loan might look complicated from the outside, but it's really just a series of logical stages. Think of it as the financial blueprint for your build, with each step getting you closer to unlocking the door of your new home. Let's walk through the entire process, from initial planning to final move-in day.

It's a common misconception that the process starts when the ground is broken. In reality, the most critical work happens long before a single shovel hits the dirt.

Stage 1: Pre-Construction and Approval

This first phase is all about building a solid foundation—not for your house, but for your loan and project plans. You’re essentially getting all your ducks in a row to present a complete, compelling picture to the lender.

-

Financial Pre-Approval and Budgeting: Your very first move should be getting pre-approved. This crucial step tells you exactly how much you can borrow, which in turn sets your total project budget. A realistic budget is the most powerful tool in your toolbox; it will guide every single decision from here on out.

-

Assembling Your Build Team: Next, it’s time to find a licensed and insured builder you trust. Lenders will want to vet your contractor to make sure they have a proven history of finishing projects on time and on budget. You'll also team up with an architect to draw up the final blueprints and specifications for your home.

-

Gathering Documentation: This is the paperwork phase. Your lender will need to see your personal financial documents (think pay stubs, tax returns, and bank statements). Your builder will also contribute key project documents, including a detailed line-item budget, the signed construction contract, and the finalized architectural plans.

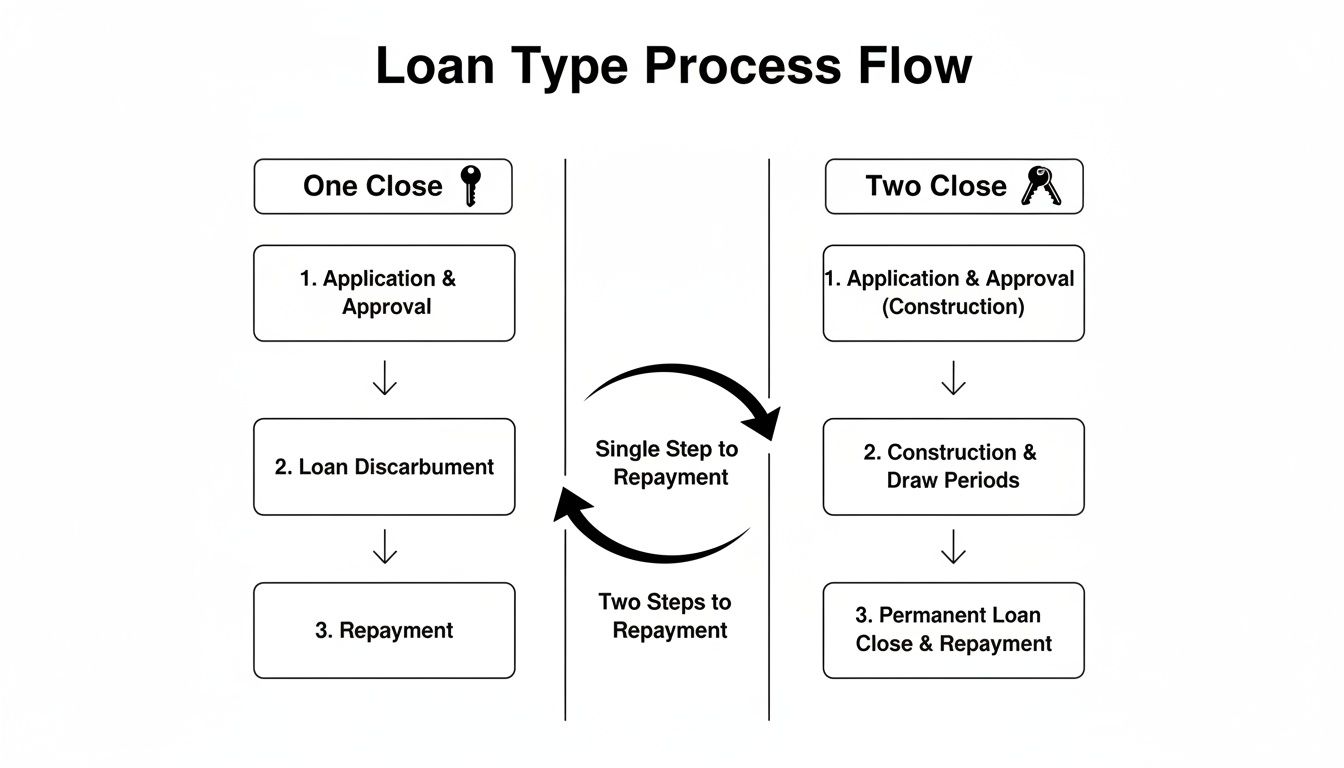

This flowchart gives you a great visual for how the single-close journey stacks up against the more traditional two-close route.

As you can see, the one-time close loan consolidates what could be two separate, stressful closings into one streamlined event. That simplicity saves you time, money, and a whole lot of uncertainty.

Stage 2: Underwriting and Closing

Once your complete application package is submitted, it goes to the lender’s underwriters. This is the official review process where the team scrutinizes every detail before giving the final green light.

The appraisal is a huge piece of this puzzle. Unlike an appraisal for an existing home, this one is based on the home's future value—what it will be worth once it's built to spec. The appraiser analyzes your blueprints, materials list, and lot to project the property's finished market value.

The success of your appraisal hinges on having detailed and realistic plans and a comprehensive budget. An appraised value that supports the loan amount is essential for final approval.

After the appraisal comes back clean and all your financial and project documents check out, you'll get the final loan approval. This takes you to the single closing day where you'll sign all the loan documents. At this table, your permanent mortgage rate is locked in for good, and the construction funds are officially set aside for your project.

Stage 3: The Construction Phase and Draw Schedule

With the loan closed, it's finally time to build! The construction funds aren't just handed over to your builder in a lump sum. Instead, they’re paid out in phases based on a pre-approved draw schedule.

This schedule connects payments to specific construction milestones. It's all agreed upon before construction starts. For example, a "draw" might be released after:

- The foundation is poured and has cured.

- The house is fully framed with the roof on.

- Plumbing, electrical, and HVAC systems are installed.

- Drywall is up and interior finishing work has started.

Before each payment is sent, an inspector usually visits the site to confirm the work for that stage is complete and up to code. This protects everyone involved—you, the lender, and the builder—by ensuring money is only paid for work that's actually been done. During construction, you'll typically make interest-only payments on the funds that have been drawn so far. You can dive deeper into the nuts and bolts by reviewing the detailed loan processes at Mortgage Seven, which really clarifies what to expect during this busy phase.

Stage 4: Finalizing Your New Home

When the last coat of paint is dry and the final punch list item is checked off, a final inspection is scheduled. This inspection verifies that the home was built according to the original plans and is ready for you to move in.

Once you pass that final inspection, the loan automatically converts from a construction loan into your permanent mortgage. There's no second closing or new round of paperwork. You just start making your regular principal and interest payments.

And that's it. Congratulations—you're now the proud owner of a brand-new custom home

How to Qualify for Your Construction Loan

Getting the green light for a one-time close construction loan isn't quite like qualifying for a standard mortgage. It's a much deeper dive. Lenders aren't just looking at you; they're also scrutinizing the entire project—from your builder's track record to the fine print on your blueprints.

This means you essentially have to make a strong case on two fronts: your personal financial health and the soundness of your construction project. Knowing what lenders are looking for ahead of time is the best way to assemble a convincing application that gives them confidence in both you and your vision.

What Lenders Look for in a Borrower

First things first, the lender needs to see that you're a reliable borrower with your financial house in order. Because a one-time close construction loan is a major undertaking, the standards are typically a bit tougher than for a regular home loan.

Here’s a look at the personal finance metrics that will be under the microscope:

- Credit Score: You’ll generally need a good to excellent credit score. While the exact number can vary, a score of 680 or higher is a common starting point. Lenders feel much more comfortable when they see scores above 720.

- Debt-to-Income (DTI) Ratio: This number shows how much of your monthly income goes toward debt. To make sure you can manage the new mortgage payment, lenders usually want to see a DTI of 43% or lower.

- Down Payment: A solid down payment lowers the lender’s risk. For a conventional construction loan, you should plan for a down payment of at least 10% to 20%. Good news, though: if you already own the land, you can often use its equity as part of your down payment.

Passing these financial checks is just the first hurdle. The lender also needs to be absolutely sure that the team and the plan you have in place can get the job done right.

Preparing Your Project and Builder for Approval

Beyond your own finances, the project itself has to get a stamp of approval. This means your builder will be thoroughly vetted and your construction plans will be examined with a fine-tooth comb. At the end of the day, the lender needs to be confident the home will be built on time, on budget, and to a professional standard.

You'll need to pull together a complete package of documents related to the build itself. This paperwork is your proof that the project is well-thought-out and in very capable hands.

Key Builder and Project Documents:

- Builder's Credentials: Proof of your builder’s license and insurance (both liability and workers' compensation), plus a portfolio showcasing their previous work.

- Detailed Building Plans: The complete set of architectural blueprints and specs that map out every last detail of your new home.

- Line-Item Budget: A comprehensive cost breakdown for every single phase of construction, from laying the foundation to installing the final light fixtures.

- Signed Construction Contract: The formal agreement between you and your builder that outlines the project’s scope, timeline, and payment schedule (the draw schedule).

Your builder's reputation and experience are just as important as your credit score. A lender will be hesitant to finance a project with a contractor who has a poor track record or lacks the necessary credentials.

It's a great time to be thinking about building. After a bit of a slowdown, construction financing is seeing a resurgence. In the first quarter of 2025, 1-to-4 family residential construction loan volume saw its first increase in two years, with outstanding loans hitting $90.0 billion. This tells us that lenders are feeling more confident in the market, which is fantastic news for well-prepared applicants. You can read more about these recent trends in construction financing to get a better sense of the current climate.

Weighing the Financial Risks and Rewards

Like any big financial move, a one-time close construction loan has its own unique mix of powerful benefits and potential hurdles. To feel truly confident in your decision, you need a clear-eyed, 360-degree view of what you’re signing up for. It’s about understanding the incredible upside and the responsibilities that come with it.

The biggest win, without a doubt, is locking in your permanent interest rate before the first shovel ever hits the dirt. In a market where rates can feel like a rollercoaster, this is a massive advantage. It completely insulates you from the risk of rates climbing during the months your home is being built, giving you priceless peace of mind and a predictable budget. You get to start your project knowing exactly what your mortgage payment will be for the long haul.

You'll also see some serious savings from a more streamlined process. Because you're combining the construction loan and the permanent mortgage into a single transaction, you only have to go through closing once. That means you pay just one set of closing costs, potentially saving you thousands of dollars on duplicate fees for things like appraisals, title searches, and attorney reviews that are simply unavoidable with a two-time close loan.

Understanding the Potential Trade-Offs

Now, for the other side of the coin. That upfront security and rate-lock protection can sometimes come with a slight trade-off. To account for the risk they're taking by locking your rate for such a long period, lenders might offer a slightly higher initial interest rate on a one-time close loan compared to what you'd see on a standalone, short-term construction loan.

It’s always smart to see how these rates stack up. For example, recent government-backed options have been quite competitive. FHA one-time close loans often carry fixed 30-year rates between 6.250% and 6.875%, while VA loans can be a touch lower, ranging from 6.000% to 6.750%. Conventional loans tend to be a bit higher, typically landing somewhere between 6.500% and 7.250%. Digging into the current one-time close interest rates can give you a real sense of how valuable that rate lock truly is.

This isn't necessarily a deal-breaker—it's just the cost of locking in predictability. The real question is whether paying a slightly higher rate upfront is worth it to avoid the risk of facing a much higher rate down the road if the market turns.

The Importance of a Contingency Fund

Let's be honest: building a home is an exercise in managing the unexpected. Lumber prices can spike, a key subcontractor could get delayed, or you might fall in love with a last-minute upgrade you just have to have. Because a one-time close loan is based on a fixed, pre-approved budget, figuring out how to handle these overages is absolutely critical.

This is where a contingency fund is non-negotiable. In fact, most lenders will require it.

A contingency fund is an amount of money, usually 5% to 10% of the total construction cost, that you set aside specifically for unforeseen expenses. Think of it as your financial safety net, making sure that surprise costs don't derail your project or wreck your budget.

Without that buffer, a big cost overrun could put you in a serious bind. Your lender is only going to release funds based on the original contract, meaning you’re on the hook for any expenses that go above and beyond the approved loan amount. Having a healthy contingency fund is the mark of a well-planned project. You can even use our mortgage calculators to play with different budget scenarios and see how a contingency fits into your bigger financial picture.

At the end of the day, the one-time close loan brings huge financial rewards to the table: significant cost savings, simplicity, and, most importantly, security. By understanding the trade-offs and preparing for the unexpected with a solid plan, you can confidently manage the risks and truly enjoy the benefits of this powerful way to finance your dream home.

Your Expert Partner for the Build

Getting your head around how a one-time close construction loan works is a great first step. But turning that knowledge into a successful build? That’s where having an experienced guide in your corner makes all the difference.

Building a home has a lot of moving parts, and let's be honest, navigating the world of construction lending isn't something you should have to do alone. This is exactly where a dedicated mortgage expert becomes your most valuable player.

At Mortgage Seven, we do more than just push paper. Think of us as your advocate and strategist. We connect you with our network of lenders who truly specialize in construction financing—people we know and trust. Our team has been down this road countless times and knows precisely what lenders look for in borrowers, builders, and the project plans themselves.

Building Your A-Team and Securing the Loan

A smooth construction project that ends with your dream home starts with the right people. That's why it's so important to invest time in finding the right contractor. We’ll work hand-in-hand with you and your chosen builder to put together a loan application package that is clear, complete, and compelling.

Our job is to walk you through every decision and make sure you land the best possible terms. We'll help you figure out if a Conventional, FHA, or VA construction loan is the right fit for you. Each one has its own set of advantages, and we’ll break down which one lines up perfectly with your financial picture.

Your dream home is a huge investment—of your money, your time, and your vision. Partnering with an expert ensures the financial foundation of that dream is just as solid as the one your builder will pour.

Ready to see those blueprints come to life? The team at Mortgage Seven is here to give you the expert guidance and one-on-one support you need. Let’s talk about your project and lay out a clear plan to get your one-time close construction loan approved.

Common Questions About Single-Close Loans

Even after getting the big picture, you're bound to have some specific questions about how a one-time close construction loan plays out in the real world. That's completely normal. Let's dig into a few of the most common questions we hear from borrowers to make sure you have the clarity you need to move forward confidently.

A lot of people who are ready to build worry that they're in a tricky spot if they've already purchased their lot. The good news? It's actually the opposite.

Can I Get This Loan If I Already Own My Land?

Yes, you absolutely can—and it’s a huge plus! Owning your land outright before you even apply for a one-time close construction loan gives you a significant leg up. Lenders love to see that you already have skin in the game, and they view the equity in your land very favorably.

In fact, you can often use your land equity to cover your down payment. Say your land is valued at $75,000, but your required down payment is only $50,000. You've already satisfied that requirement without bringing extra cash to the table.

Using your land as equity is one of the smartest ways to finance a new build. It simplifies your financial contribution and leverages an asset you already possess to secure the loan for your dream home.

Another frequent concern is the budget. We all know that construction projects have a lot of moving parts, and unexpected costs can pop up.

What Happens If My Project Goes Over Budget?

This is exactly what a contingency reserve is for. Lenders build this safety net right into the loan from the very beginning. It’s typically a fund equal to 5-10% of the total construction cost, set aside specifically for those "just in case" moments.

If you hit a snag and the project goes over the initial budget, you can tap into these reserve funds to cover the difference. This keeps the build moving forward without forcing you to pay for surprises entirely out-of-pocket. And if you don't end up using the contingency money? It simply gets applied to your principal loan balance after the house is finished.

How Long Does Construction Usually Take?

Every custom home is different, of course, but you can generally expect the construction phase for a standard single-family home to last between 9 and 12 months. During this time, you'll only be responsible for making interest-only payments on the money that has been paid out to your builder.

Knowing this timeline helps you plan for that interest-only period. As soon as the last nail is hammered in and the final inspection is complete, your loan automatically rolls over into its permanent phase. That's when you'll start making your regular principal and interest payments, just like a standard mortgage.

Navigating these questions is much easier with an expert by your side. At Mortgage Seven LLC, we specialize in guiding clients through every detail of the construction loan process, ensuring you have the clarity and support you need.

Schedule your free consultation with a Mortgage Seven expert today!