Refinancing to ditch PMI is one of the smartest ways to lower your monthly mortgage payment once you've built up a decent chunk of home equity. The idea is simple: you replace your current mortgage with a brand-new one that doesn't have the Private Mortgage Insurance (PMI) requirement. For many homeowners, this move can free up hundreds of dollars every single month. It works best when your home's value has climbed, pushing your equity stake past that magic 20% threshold.

Is Now the Right Time to Refinance and Drop PMI?

It's a common story. You bought your home a few years ago, and since then, you've been diligently making payments while property values in your area have been on the rise. You're sitting on a growing pile of home equity, yet you're still stuck paying for PMI—an insurance policy that only protects your lender.

That monthly PMI fee does absolutely nothing for you, and it’s one of the first things savvy homeowners look to eliminate. Your home equity isn't just a number on a statement; it's a financial tool waiting to be used. By refinancing, you can turn that paper equity into real, immediate cash savings month after month.

How Market Appreciation Unlocks Savings

Let's walk through a real-world example to see this in action.

Say you bought a home back in 2022 for $320,000 with 10% down ($32,000). You financed $288,000. Now, fast forward to 2025. Thanks to a strong market, your home is appraised at $380,000, and you've paid your loan down to about $276,000.

Suddenly, you have over 27% equity, but you're still paying $240 a month in PMI on top of your $1,750 principal and interest payment. Your total monthly outflow is $1,990.

This is the perfect moment to refinance. You could get a new conventional loan, and that $240 PMI charge vanishes completely. Even if your new principal and interest payment ticks up to $1,780 after rolling in $5,000 of closing costs, you're still saving $210 every month. That's $2,520 in your pocket each year. Your break-even point on the closing costs? A mere 23.8 months.

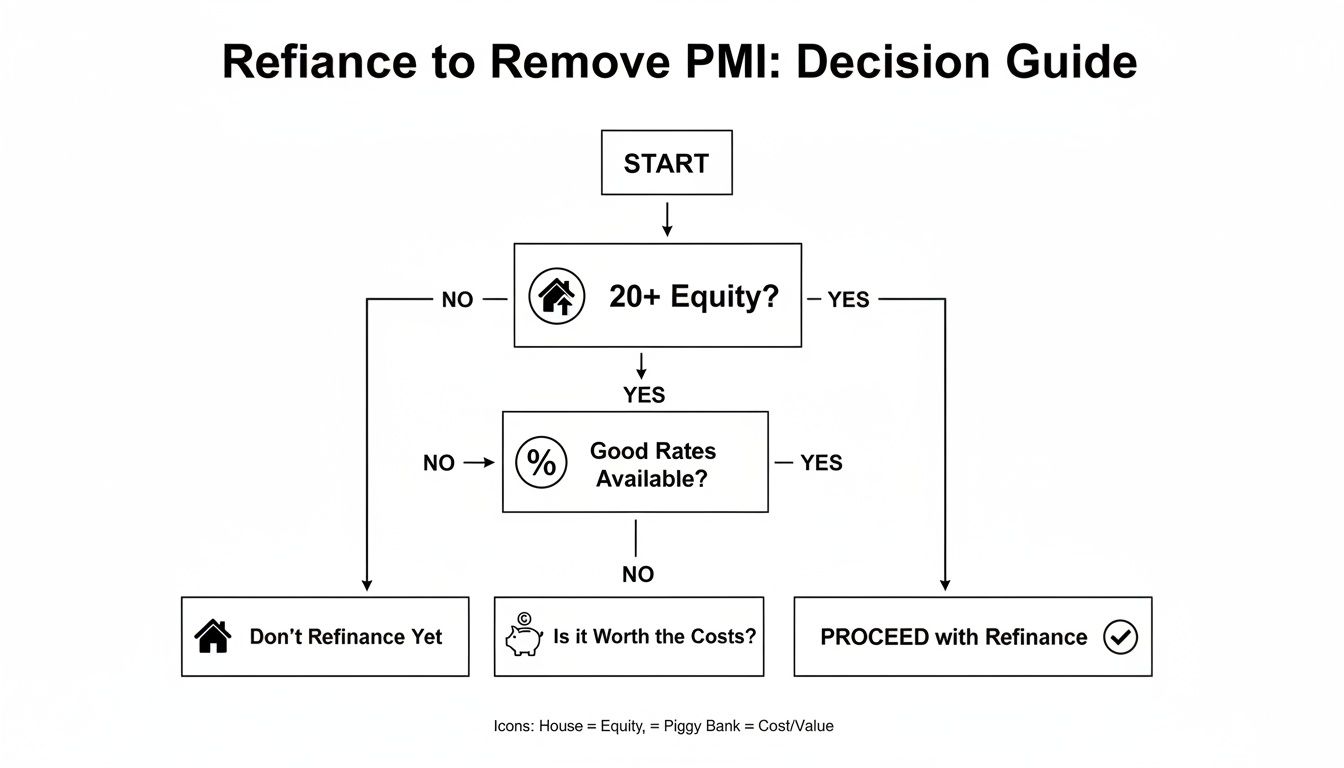

This decision flowchart can help you visualize whether this path makes sense for you.

As you can see, it really boils down to three core checkpoints: having enough equity, checking the current interest rate environment, and making sure the long-term savings are worth the upfront closing costs.

Key Signals That It’s Time to Act

Knowing when to pull the trigger is everything. A successful refinance depends on a combination of favorable market conditions and your own financial situation lining up just right.

So, what are the green flags?

- You've Hit 20% Equity: This is the big one. Once your loan-to-value (LTV) ratio hits 80% or less, you can qualify for a new conventional loan without PMI.

- Interest Rates Look Good: If current mortgage rates are lower than or even just comparable to what you have now, you can drop PMI without taking a big hit on your monthly principal and interest payment.

- Your Credit Score Has Improved: A better credit score than when you first bought your home can unlock much better interest rates, making the savings from refinancing even bigger.

Timing your refinance can be the difference between a good financial move and a great one. The goal isn't just to drop PMI but to secure a better overall mortgage for your future. For a deeper look at the nuts and bolts, you can review this comprehensive guide on refinancing.

To make things even clearer, here is a quick checklist of the key factors to consider. This table breaks down what to look for and why each element is so important in making your decision.

Quick Checklist When To Refinance For PMI Removal

| Indicator | What to Look For | Why It Matters |

|---|---|---|

| Home Equity | At least 20% equity in your home. Your loan balance should be 80% or less of the home's current market value. | This is the primary requirement for qualifying for a new conventional loan without needing to pay for PMI. |

| Current Interest Rates | Rates are lower than or similar to your existing mortgage rate. | A lower rate amplifies your savings. A similar rate still lets you drop PMI for a net monthly saving. |

| Break-Even Point | Your monthly savings will cover the closing costs within a reasonable timeframe (e.g., 2-3 years). | This calculation confirms the refinance is financially sound and you'll stay in the home long enough to benefit. |

| Credit Score | Your credit score has improved since you originally took out the loan. | A higher score can qualify you for the best available interest rates, maximizing your total savings. |

| Future Plans | You plan to stay in the home for at least the next 3-5 years. | Refinancing has upfront costs. You need to remain in the home long enough to recoup those costs and realize the savings. |

Looking at these factors together gives you a solid, 360-degree view of your situation. If you check off most of these boxes, it's very likely a great time to start talking to a lender and get the ball rolling.

Do You Have Enough Equity? Crunching the Numbers on Your LTV

Before you even think about calling a lender, there’s a crucial question you need to answer: do you actually have enough equity to ditch your PMI? Lenders aren't just going to take your word for it. They need proof that your ownership stake has crossed the magic 20% threshold.

This is where your Loan-to-Value (LTV) ratio becomes the star of the show. It's the single most important number in this process, and getting it right is your first real step toward saying goodbye to that extra monthly payment.

How to Figure Out Your Home's Current Value

Your home’s value isn't what you paid for it; it's what it’s worth today. Market shifts, neighborhood improvements, and your own upgrades can all have a big impact. To get an accurate number, you'll need to accurately determine your home's current market value using real estate comps.

Here are a few common ways people pin down that number:

- Online Estimators: Sites like Zillow and Redfin offer a quick, free estimate. These are great for a ballpark figure, but don't hang your hat on them—they can be off by a wide margin.

- Ask a Real Estate Agent: A local agent can pull a Comparative Market Analysis (CMA) for you, often for free. This is far more reliable than an online tool because a professional is comparing your home to truly similar, recently sold properties.

- Pay for an Appraisal: This is the gold standard. A formal appraisal is what the lender will require anyway, so getting one upfront can give you a definitive answer before you spend money on application fees.

The LTV Calculation Made Simple

Once you have your home's current value and your latest mortgage balance (just check your most recent statement), the math is surprisingly simple.

Here’s the formula: Current Loan Balance ÷ Current Home Value = LTV Ratio

Let’s walk through a quick example. Say you still owe $276,000 on your mortgage, and after talking to an agent, you're confident your home is now worth about $380,000.

Here's How It Breaks Down:

- Current Loan Balance: $276,000

- Estimated Home Value: $380,000

- The Math: $276,000 ÷ $380,000 = 0.726

Your LTV ratio is 72.6%.

Since that 72.6% is comfortably below the 80% LTV mark, you're in a great position to refinance and finally get rid of PMI. Now you can approach lenders with confidence, knowing you’ve already cleared their biggest hurdle.

Running the Numbers: Your Refinance Break-Even Point

The idea of dropping your PMI payment is definitely appealing, but refinancing isn't a free move. Before you jump in, you have to run the numbers to see if it truly makes financial sense for you.

This all boils down to one simple question: How long will it take for the money you save each month to cover the upfront costs of the new loan? This is what we call the break-even point.

Refinancing involves closing costs, just like your original home purchase. You can generally expect these to be somewhere between 2% and 5% of your new loan amount. It’s crucial to understand these fees before you commit.

Some of the usual suspects you'll see on your cost estimate include:

- Lender Origination Fee: This is what the lender charges to process and underwrite your loan.

- Appraisal Fee: Pays for a professional appraiser to confirm your home's current market value.

- Title Insurance: Protects the lender (and you, with an owner's policy) from any issues with the property's title.

- Credit Report Fee: The cost for the lender to pull your credit scores and history.

- Recording Fees: What your local government charges to officially record your new mortgage.

Pinpointing Your Break-Even Point

This is the most critical calculation you'll do. It's the moment the refinance stops costing you money and starts saving you money. To really see if this move is worthwhile, you have to calculate your break-even point and get a clear picture of when the savings finally overtake the initial costs.

The formula itself is pretty simple:

Total Closing Costs ÷ Monthly PMI Savings = Months to Recoup Costs

Let's walk through a quick example. Say you're currently paying $150 a month for PMI. After shopping around, you get a quote showing your total closing costs for the refinance will be $4,500.

Plugging that into our formula:

$4,500 (Total Closing Costs) ÷ $150 (Monthly Savings) = 30 months

In this scenario, it would take you 30 months—or two and a half years—to "break even." If you know for sure you'll be in your home longer than that, then every month after the 30-month mark is pure, tangible savings in your pocket. But if you think you might sell in the next year or two, the math just doesn't work out.

To help you visualize this, here’s a sample breakdown:

Refinance Cost vs. PMI Savings A Sample Break-Even Calculation

| Calculation Step | Example Figure | Description |

|---|---|---|

| Total Closing Costs | $4,500 | This includes all lender, title, and appraisal fees. |

| Current Monthly PMI | $150 | The amount you're saving each month. |

| Break-Even Calculation | $4,500 / $150 | Divide the total costs by your monthly savings. |

| Months to Recoup | 30 Months | The number of months until you're "in the green." |

This table clearly shows the timeline. If your plans align with staying in the home past the 30-month mark, the refinance is a solid financial strategy.

Don't feel like you have to do all this with a pen and paper. You can explore different scenarios with our suite of powerful mortgage calculators at https://mtg7.com/Calculators.html. Playing with the numbers a bit will give you the confidence that your decision is based on a solid financial foundation, not just the dream of a lower payment.

Choosing Your New Loan and Getting Your Paperwork in Order

Alright, you've crunched the numbers and refinancing looks like a smart play. Now it's time to get down to business: picking the right loan and building an application that will sail through underwriting. This is where your homework pays off.

For most people in this situation, the goal is pretty straightforward—they want to jump from an FHA loan, with its seemingly endless mortgage insurance, to a conventional loan where PMI has a clear expiration date.

It's the only real escape hatch from the FHA's Mortgage Insurance Premium (MIP), which, for most borrowers, sticks around for the life of the loan. Even if you already have a conventional loan, refinancing into a new one is the fastest way to use your newfound equity to kick that monthly PMI payment to the curb.

The decision you make at this stage can impact your monthly budget for years to come.

The Classic Move: FHA to Conventional Refinance

This is a path I've seen hundreds of homeowners take. You used an FHA loan to get your foot in the door with a small down payment, built up some equity, and now you’re ready to shed that MIP for good. The biggest win here is obvious: no more FHA mortgage insurance payment eating into your budget every single month.

This strategy is a huge deal for many families. In fact, nearly 35% of households paying for private mortgage insurance have an annual income under $75,000.

Let's look at a real-world scenario. Imagine a family bought a home for $320,000 in the Virginia suburbs back in 2022. By 2025, thanks to appreciation, their home could easily be worth $380,000. That jump in value pushes their equity well past the 20% threshold, allowing them to refinance into a conventional loan. By doing so, they could ditch a $240/month PMI payment, saving over $2,500 a year. You can find more data on market trends like this from resources like HSH.com.

Your Document Checklist

Lenders aren't just going to take your word for it; they need to verify everything about your financial situation. Gathering your documents upfront is the single best thing you can do to make the process smoother and faster.

Here’s what you should have ready to go:

- Proof of Income: Grab your most recent pay stubs covering a 30-day period, plus your W-2s from the last two years.

- Tax Returns: Lenders will want to see your full federal tax returns for the past two years, including all schedules.

- Bank and Asset Statements: Be prepared to provide the last two months of statements for every account—checking, savings, and any investments—to show you have cash reserves.

- Current Mortgage Statement: Your latest statement has all the key details: your current loan balance, interest rate, and escrow information for taxes and insurance.

- Homeowners Insurance Policy: You'll need the declarations page from your current policy to help the lender set up your new escrow account correctly.

Pro Tip: I always tell my clients to create a "Refi Docs" folder on their computer. Scan everything and save it as a PDF. When the lender asks for something, you can upload it in minutes instead of digging through file cabinets. It can honestly shave days off the timeline.

A spotless application is built on a solid financial history, which is why your credit score plays such a central role. For a deeper dive into how your credit can affect your mortgage options, you can get more information at https://mtg7.com/Credit.html. A better score often means a better interest rate, which just adds to the savings when you refinance to remove PMI.

Exploring Alternatives to a Full Refinance

While refinancing is a fantastic way to ditch PMI, it's not always the right move for everyone. If interest rates have shot up since you got your mortgage, trading your great low rate for a new, higher one might wipe out any savings you’d get from dropping that PMI payment. It can be a real "one step forward, two steps back" situation.

Luckily, you've got other plays you can make that don't involve swapping out your entire home loan.

The most straightforward path is to simply ask your current lender to cancel your PMI. Federal law is on your side here. Once your loan balance is scheduled to hit 80% of your home's original value, you can send a written request to your servicer. As long as you've been making your payments on time, they are generally required to grant it.

Using Market Appreciation to Your Advantage

But what if your neighborhood has been booming and your home's value has soared? You don’t have to just sit around waiting for your loan balance to slowly tick down to that 80% mark. You can be proactive.

This is where a fresh appraisal can be your best friend. If a big jump in home values has pushed your loan-to-value (LTV) ratio below 80% based on the current market value, you might be able to get rid of PMI much sooner.

Here’s what that looks like in practice:

- Order a New Appraisal: This will be on your dime and typically runs between $450 and $650. Think of it as an investment—it’s the official proof your lender needs to see.

- Submit a Written Request: Don't just call. Put it in writing and formally ask your loan servicer to remove the PMI, citing the new valuation as the reason.

- Meet Lender Requirements: This strategy only works if you have a solid payment history and don't have other loans against your house, like a home equity line of credit.

Going this route lets you keep the great interest rate you already have while still accomplishing the main goal: getting that monthly PMI payment off your back.

Understanding Your Rights and Lender Timelines

The government has put some real consumer protections in place. Thanks to the Homeowners Protection Act of 1998, lenders are required to automatically terminate your PMI once your loan balance is scheduled to reach 78% of the home's original value. Waiting for that to happen can take a long, long time, which is why so many homeowners look for ways to speed things up.

For conventional loans, servicers often have "seasoning" requirements. These are waiting periods before they'll let you use a new appraisal to request PMI cancellation. It might be two years after your loan closed if your new LTV is 75% or better, or five years if you've hit 80% LTV. You can dig into the specifics by reading up on how Freddie Mac handles PMI cancellation.

A full refinance is the ultimate shortcut. It completely bypasses those lender-imposed waiting periods. If a new appraisal confirms you have more than 20% equity, you can refinance immediately and get a new loan without PMI—no two- or five-year anniversary required. That speed and certainty are exactly why it remains such a powerful and popular option.

Common Questions About Ditching PMI With a Refinance

Even when the numbers seem to line up perfectly, it's completely normal to have a few lingering questions. Refinancing is a big financial step, and you want to feel sure about your decision before diving in.

Let's walk through some of the most common questions homeowners ask when they're thinking about refinancing to get rid of PMI for good.

Will I Have to Pay for a New Appraisal?

Yes, almost always. A new appraisal is typically a non-negotiable part of the deal. Your new lender needs a fresh, professional opinion on what your home is worth today. This isn't just a formality—it's how they officially calculate your new loan-to-value (LTV) ratio.

Think of the appraisal as the proof in the pudding. While it's an upfront cost you'll need to budget for (usually somewhere between $450 and $650), it’s the key that unlocks the door to dropping PMI by confirming you have that magic 20% equity. While some lenders might grant an appraisal waiver in rare cases, it's smart to plan on having this expense.

What if My Credit Score Isn't What It Used to Be?

A drop in your credit score can definitely throw a wrench in the works. It’s one of the biggest factors lenders look at when setting your new interest rate. A lower score could mean a higher rate, which might eat up all the savings you were hoping to get from dropping PMI.

Before you even fill out an application, I always recommend pulling your credit report. Check for errors and see if there are any quick wins, like paying down a high-balance credit card. A good mortgage pro can also take a look at your complete financial picture and give you an honest opinion on whether your current score makes refinancing a smart move right now.

Can I Refinance Out of an FHA Loan to Remove PMI?

You bet. In fact, this is one of the most common and powerful reasons to refinance. If you have an FHA loan with a small down payment, you’re likely stuck with a Mortgage Insurance Premium (MIP) that lasts for the entire life of the loan.

For many FHA borrowers, refinancing into a conventional loan isn't just an option—it's the only way to eliminate that monthly MIP payment once they've built up at least 20% equity. This single move can save you thousands upon thousands of dollars over time.

How Long Will This Whole Refinance Process Take?

From start to finish, you should plan on the refinance taking about 30 to 60 days. That's from the day you submit your application to the day you're signing the final paperwork. The exact timeline can shift depending on how busy the lender is, how straightforward your financial situation is, and how quickly the appraisal gets done.

The journey usually looks something like this:

- Application & Docs: You gather and send in all your financial paperwork.

- Appraisal & Underwriting: The lender orders the appraisal while an underwriter reviews your file.

- Conditional Approval: You might get a request for a few more documents or a quick explanation.

- Clear to Close: This is the green light! Your loan is approved, and a closing date is scheduled.

- Closing Day: You sign the new loan documents, and you're done.

The best way to keep things on track? Be organized. Have your documents ready to go and respond to your lender’s requests as quickly as you can. A little preparation on your end can prevent a lot of delays.

At Mortgage Seven LLC, we specialize in guiding homeowners through this exact process, ensuring you have the clarity and support needed to make the best decision for your financial future. If you're ready to see how much you could save, start your application with us today.