For entrepreneurs, the path to homeownership often feels like navigating a maze of unique self employed mortgage requirements. If you're a W-2 employee, income verification is pretty straightforward. But when your revenue fluctuates, it presents a different kind of puzzle for lenders. This guide is here to cut through that confusion and help turn your hard-earned business success into the keys to your new home.

Why Getting a Mortgage Is Different for Entrepreneurs

Think of a traditional mortgage application like a simple snapshot. A lender glances at a W-2 employee's pay stubs and sees a clear, predictable monthly income. Simple enough.

For a business owner, though, the picture is more like a feature-length film. Lenders need to understand the whole story—your business's history, its ups and downs, and where it's headed. They aren't just looking at one month's revenue; they're analyzing your financial narrative over the last two years to get a true sense of stability.

This fundamental difference is why the process feels so much more intensive. It’s not that lenders automatically see you as a higher risk. They just need more evidence to piece together your complete financial profile, which means a much deeper dive into your paperwork and a totally different way of calculating your qualifying income.

Debunking the Homeownership Myth

There's a persistent myth that getting a mortgage is nearly impossible if you work for yourself. The truth? It's all about strategic preparation and knowing the rules of the game. This guide reframes the challenge from an obstacle into a clear roadmap. We'll break down exactly what lenders are looking for, so you can present your finances in a language that underwriters understand and appreciate.

Here’s what you can expect to learn:

- Proving Income Stability: We'll cover the essential documents that paint a compelling picture of your consistent success.

- Income Calculation: You'll learn how lenders analyze your tax returns and why those beloved write-offs can be a double-edged sword.

- Loan Program Options: We'll explore mortgages designed specifically for entrepreneurs, like bank statement loans and P&L programs.

- Strengthening Your Application: I'll share actionable tips for improving your credit, debt-to-income (DTI) ratio, and cash reserves to boost your approval odds.

By preparing ahead of time and partnering with an expert, you can confidently navigate the self employed mortgage requirements. It's all about showcasing the true financial strength of your business, not just what a tax form says.

Consider this article your blueprint. We'll walk through the documents, the calculations, and the strategies that make all the difference, empowering you to approach the mortgage process with clarity and confidence.

Proving Your Income for a Mortgage

When you're self-employed, proving your income is the single most important part of getting a mortgage. Lenders need to see a clear, consistent story of your business's financial health, and your paperwork is what tells that story. Think of it less like a standard application and more like building a business case for yourself.

The first concept you'll run into is what we in the industry call the “two-year rule.” Lenders almost always want to see a 24-month history of self-employment. Why? Because one great year is nice, but two solid years show that your business is stable and can weather the normal ups and downs of entrepreneurship. It paints a much more reliable picture of your true earning power.

This isn't just a casual preference; it's a core requirement for most traditional loans. This two-year track record is the foundation lenders use to calculate the average monthly income they’ll use to qualify you for a loan.

What Your Underwriter Needs to See

Getting your documents in order before you apply is a game-changer. It makes the entire process smoother and shows the underwriter you're a serious, organized borrower. An underwriter's job is to poke holes in your story, so giving them clean, complete paperwork from the start is your best first move.

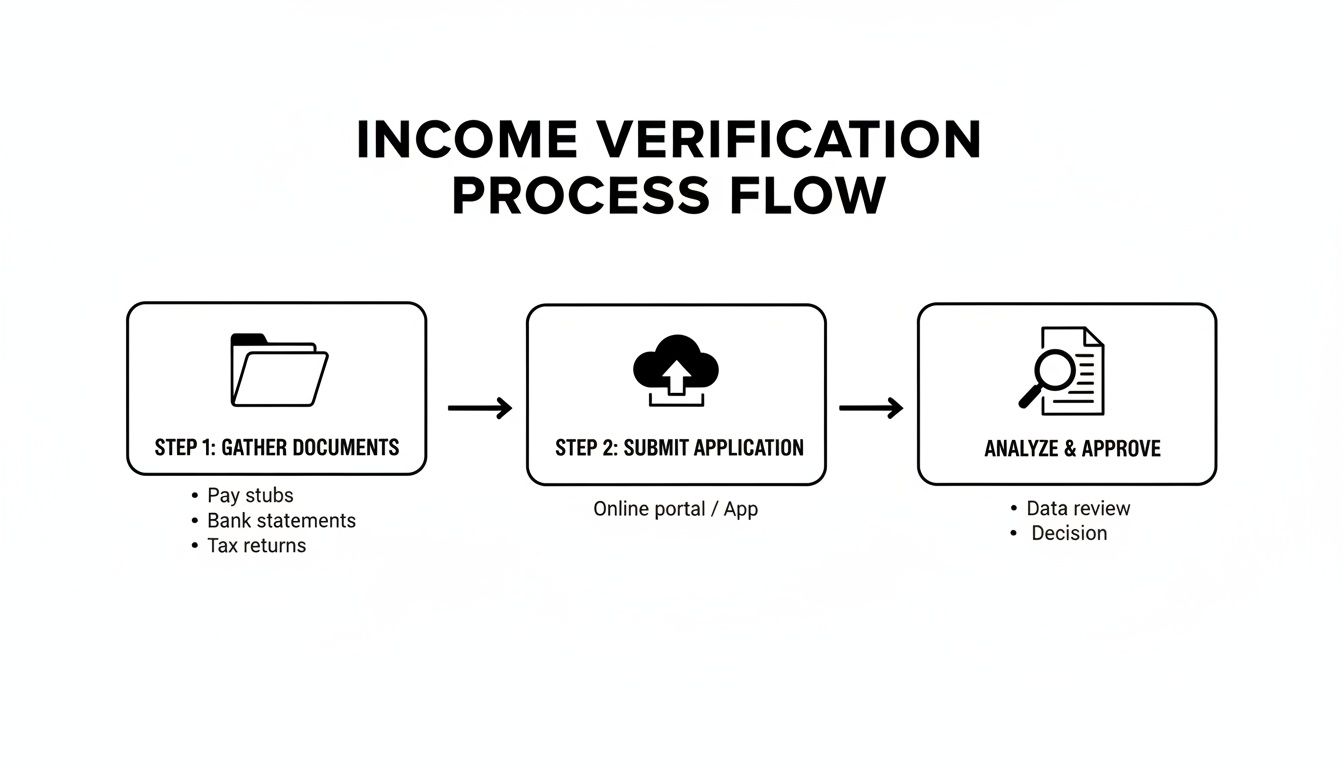

Here's a look at the essential documents you'll need to gather to prove your income and business stability.

Essential Documents for Self Employed Mortgage Applications

| Document Type | What It Shows | Typical Requirement |

|---|---|---|

| Personal Tax Returns | Your adjusted gross income (AGI) after all deductions. | 2 most recent years of signed 1040s with all schedules. |

| Business Tax Returns | The official profit or loss for your LLC, S-Corp, or Partnership. | 2 most recent years of signed returns (1120-S, 1065, etc.). |

| Key Tax Schedules | Details where your income comes from (Schedule C, E, K-1). | Must be included with your personal and business returns. |

| Profit & Loss (P&L) | A snapshot of your business's current year-to-date performance. | A recent, signed P&L statement, usually for the current year. |

| Business Bank Statements | Proof of consistent cash flow and business activity. | 12 to 24 months of recent statements. |

Putting these documents together correctly is crucial. If you need a hand, there are great resources online for preparing your business's financial statements that can walk you through the basics.

How an Underwriter Thinks

An underwriter doesn’t just check boxes; they dig deep into these documents to calculate your average qualifying income. They're looking for trends. Is your revenue steady? Is it growing? Or is it declining? A big drop in income between year one and year two is a major red flag that you'll absolutely need to explain in writing.

Lenders are looking for one thing above all else: predictability. They need to feel confident that the income you've shown for the past two years is a reliable forecast of what you'll earn in the future. That’s how they know you can handle the mortgage payment month after month.

For most conventional, FHA, and VA loans, this two-year history is non-negotiable. But let's be honest—tax write-offs are a huge perk of being self-employed, and they can sometimes make it tough to qualify on paper.

That’s where other loan programs come into play. If your tax returns don't reflect your true cash flow, we can explore other options. For instance, our guide on bank statement loan programs details how we can use 12-24 months of your business deposits to prove income, completely bypassing your tax returns.

By understanding what the lender needs and telling a clear financial story, you put yourself in the driver's seat.

How Lenders Figure Out Your Real Income

If you’re self-employed, this is probably the most frustrating part of getting a mortgage. It’s also the most important. The number you celebrate as your company's gross revenue isn't what the bank sees. They’re looking at what you report to the IRS after all your write-offs.

This is what I call the "entrepreneur's paradox."

When you're doing your taxes, your goal is to maximize deductions and make your taxable income look as small as possible. Smart business, right? But when a mortgage underwriter looks at that very same tax return, they see that smaller number, too. Every dollar you wrote off to save on taxes is a dollar that vanishes from your qualifying income.

This is why lenders anchor their calculations to your Adjusted Gross Income (AGI), and they'll almost always want to see a two-year average to prove that income is stable.

This chart gives you a bird's-eye view of how your financial documents flow through the underwriting process.

As you can see, it's a journey from gathering your documents to a deep-dive analysis where an underwriter puts your qualifying income under a microscope.

Finding "Hidden" Income with Add-Backs

Thankfully, your AGI isn't the final number. Lenders know that certain business expenses are just "paper losses"—deductions that don't actually involve cash leaving your account. We can add these back to your income, and it can make a huge difference.

Think of these "add-backs" as bonus income. They're legitimate tax deductions that an underwriter can add back to your AGI, bumping up the number we can use to get you qualified.

Here are the most common add-backs we look for:

- Depreciation: This is the big one. The value you write off for equipment, vehicles, or property is a non-cash expense.

- Depletion: Similar to depreciation, but for businesses that use natural resources.

- Business Use of Home: The expenses you deduct for your home office can often be added back in.

- One-Time Major Purchases: Did you buy a huge piece of equipment last year that you won't buy again for a decade? With the right paperwork, we can often get that added back.

These adjustments are a game-changer. They help an underwriter see a truer picture of your business's actual cash flow, moving beyond the bottom-line number on your tax return.

Let's Look at a Real-World Example

To see how this works, let's imagine a freelance consultant. Her business brought in a solid $150,000 in gross revenue last year.

Being savvy, she worked with her accountant to claim several deductions:

- Home Office Expenses: $5,000

- Business Miles: $8,000

- Software & Subscriptions: $4,000

- Depreciation on New Computers: $10,000

Her total deductions come out to $27,000. So, on paper, her AGI is $123,000 ($150,000 – $27,000). That's the starting point for a lender.

But here's where the magic happens. That $10,000 for depreciation isn't cash that left her bank account. An experienced underwriter will add that right back on top of her AGI.

How the Qualifying Income Breaks Down:

$123,000 (AGI) + $10,000 (Depreciation Add-Back) = $133,000 in Qualifying Income

Just like that, she has $10,000 more in annual income to qualify with. That small adjustment can be the key that unlocks the door to the home she really wants.

Getting a handle on this calculation is incredibly empowering. It helps you look at your business finances through the same lens as a mortgage underwriter. The trick is to start planning with your accountant at least two years before you apply. By working with a knowledgeable broker here at Mortgage Seven LLC, you can strike the perfect balance between smart tax planning and strong home-buying power.

Beyond the Basics: Creative Mortgage Options for Business Owners

What happens when your tax returns don't quite capture the success of your business? For many entrepreneurs, this is a frustrating reality. A conventional loan often feels like trying to fit a square peg into a round hole because it hinges on a two-year average of your tax return income—a number that rarely tells the whole story for a business that's growing, reinvesting, or taking advantage of legitimate deductions.

Don't worry, you're not out of options. This is exactly why a different class of home loans exists. These are called Non-Qualified Mortgages, or Non-QM for short. Think of them as custom-tailored suits instead of off-the-rack options, designed specifically for borrowers with unique financial pictures like yours. They provide a much-needed lifeline by looking at your income through a different lens, focusing on your business's actual cash flow instead of just the bottom line on your tax forms.

Bank Statement Loans: The Entrepreneur's Go-To

By far the most popular Non-QM route for business owners is the bank statement loan. It's a simple but brilliant concept. Instead of tax returns, we use your business bank statements—usually from the last 12 or 24 months—to see what your income really looks like. We're looking at your consistent monthly deposits as a true measure of your business's health.

This approach is an absolute game-changer. It’s for the entrepreneur whose tax returns show a modest AGI because they have a savvy accountant who maximizes every possible write-off. This loan lets your actual cash flow, the true lifeblood of your company, do the talking.

- Who It's For: Perfect for business owners who have strong, verifiable deposits but show lower taxable income after deductions and reinvestment.

- What to Expect: Lenders are typically looking for credit scores of 660 or higher, with down payments often starting in the 10-20% range.

- The Problem It Solves: It completely sidesteps the AGI calculation from your tax returns. Your home-buying power is finally aligned with your company's real revenue.

This is the loan for the successful business owner who pays a great CPA to minimize their tax bill. It acknowledges that strong cash flow is a far better sign of your ability to pay a mortgage than a low AGI.

Profit and Loss (P&L) Statement Loans: A Streamlined Approach

Another powerful tool in our arsenal is the P&L-only loan. This program lets you qualify using a recent Profit & Loss statement, which must be prepared and signed by a licensed third-party tax professional, like your CPA. This gives the lender a current, real-time snapshot of your business's financial health without sifting through a year's worth of bank statements.

This option is often faster and involves less paperwork than a full bank statement loan, making it a great fit for established business owners who already have clean, professionally prepared financial records on hand.

DSCR Loans: Built for the Real Estate Investor

Are you buying an investment property? Then a Debt Service Coverage Ratio (DSCR) loan is a path you need to know about. This loan is unique because it qualifies you based on the property’s potential rental income, not your personal or business income. The lender just wants to see if the projected rent will cover the mortgage payment (including principal, interest, taxes, and insurance).

- How It Works: Lenders use a simple ratio. A DSCR of 1.0 means the rent exactly covers the mortgage payment. Most lenders want to see a ratio of 1.25 or higher, meaning the property generates 25% more income than its expenses.

- Who It's For: It's designed for real estate investors of all levels, from first-timers to seasoned pros who want to grow their portfolio without their personal W-2 or business income being the main factor.

- The Problem It Solves: It lets you scale your real estate investments based on the performance of the assets themselves, neatly separating your personal finances from your investment ventures.

To help you see how these options stack up, here’s a quick comparison:

Comparing Self Employed Mortgage Programs

This table breaks down the key differences between the most common loan programs available to entrepreneurs, highlighting what they look for and who they're best suited for.

| Loan Program | Income Documentation | Typical Down Payment | Best For |

|---|---|---|---|

| Conventional | 2 Years of Tax Returns | 3-20% | Business owners with consistent, high AGI and minimal write-offs. |

| Bank Statement | 12-24 Months of Business Bank Statements | 10-20% | Entrepreneurs with strong cash flow but significant tax deductions. |

| P&L Only | CPA-Prepared Profit & Loss Statement | 15-25% | Established business owners with clean financials looking for a faster process. |

| DSCR | None (Based on Property's Rental Income) | 20-25% | Real estate investors buying rental properties that cash flow. |

Each of these specialized products shows how the mortgage industry has evolved to meet the needs of modern entrepreneurs. The "one-size-fits-all" approach is a thing of the past.

By exploring these flexible options, you can find a financing solution that actually understands and rewards your business success. To see if one of these programs is the right fit, you can learn more about flexible Non-QM mortgage solutions and see how they are built for the self-employed. Here at Mortgage Seven LLC, we specialize in this—we love digging into a business owner's unique financial profile and finding the perfect match.

Strengthening Your Financial Profile

Getting your income documented is the biggest challenge when you're self-employed, but it's not the whole story. Lenders are really looking at three other key areas to decide if you're a solid borrower. I like to think of a mortgage application as a four-legged stool. Sure, income is one leg, but without the other three—credit, debt, and cash reserves—the whole thing gets pretty unstable.

At the end of the day, an underwriter’s job is all about managing risk. A strong, well-rounded financial profile proves you’re stable and can handle a mortgage, even when business inevitably has its ups and downs.

The Power of Your Credit Score

Your credit score is the first thing a lender sees. It’s a quick snapshot of your financial habits and reliability. For entrepreneurs, a high score is crucial because it helps balance out the perceived risk that comes with an income that isn't always predictable.

While some loan programs might work with a lower score, you should really be aiming for 720 or higher. That’s the magic number that opens the door to the best interest rates and more flexible loan options.

If your score needs a little work, here’s what you can do right now:

- Knock Down Balances: Get your credit card balances below 30% of your total limit. This is a huge factor.

- Set It and Forget It: Automate your payments so you never miss one. A single late payment can do serious damage to your score.

- Play Detective: Pull your credit report and check it for errors. If you find any mistakes, dispute them immediately.

Understanding Your Debt-to-Income Ratio

Your Debt-to-Income (DTI) ratio is another make-or-break number. It simply compares how much you owe each month to how much you make.

The math is straightforward:

(Total Monthly Debt Payments ÷ Gross Monthly Income) x 100 = DTI Ratio

So, if your lender calculates your qualifying income at $8,000 a month and your total debts (like a car payment, student loans, and credit cards) add up to $2,000, your DTI is 25%.

While a conventional loan might technically allow a DTI as high as 43%, self-employed borrowers need to aim lower. A low DTI reassures the lender that you have plenty of breathing room in your budget to handle a new mortgage payment without strain. The fastest way to improve your DTI? Pay down your consumer debt.

Building Your Cash Reserve Safety Net

Finally, lenders want to see you have a solid financial cushion. Cash reserves are the liquid funds you'll have left over after you’ve paid your down payment and all the closing costs. This money is your safety net, proving you can weather a slow quarter or an unexpected expense without missing a mortgage payment.

The bar is set a bit higher for self-employed borrowers. Lenders typically want to see 6 to 12 months' worth of mortgage payments (including principal, interest, taxes, and insurance) sitting in your accounts. For a $3,000 monthly mortgage payment, that means having between $18,000 and $36,000 saved and ready.

Working on these three areas can take your application from just "okay" to "instantly approvable." It's also smart to remember that optimizing self-employed tax benefits can play a big role in the income you're able to show, which helps everything else fall into place. When you walk in with a great credit score, low debt, and healthy reserves, you're exactly the kind of borrower lenders are looking for.

Your Action Plan for Getting Mortgage Ready

Knowing what to do is one thing; actually doing it is what gets you the keys to your new home. I know that preparing for a mortgage application can feel like a massive project, but if you break it down into smaller, more manageable steps, you can turn all that uncertainty into real confidence.

Think of this as your pre-application training. By knocking out these items one by one, you’ll walk into the lender's office looking like a well-prepared, low-risk borrower. That doesn't just improve your odds of approval—it makes the whole process a lot smoother. It's all about building a rock-solid case before an underwriter ever sees your name.

Strategize and Organize Your Finances

Your first move? Get a professional, big-picture view of your financial landscape. This isn't just about shuffling papers; it’s about intentionally shaping your financial story for the next two years.

-

Consult Your Accountant: Before you do anything else, schedule a meeting with your CPA. Talk to them about your homeownership goals and how you should strategically report your income on your next tax return. This is a crucial conversation—it’s about finding the sweet spot between minimizing your tax bill and maximizing the income you need to qualify for the house you want.

-

Create a 'Mortgage-Ready' Folder: Whether it's a physical folder or a digital one on your computer, start it today. Every time a new bank statement comes in, you file your taxes, or you renew a business license, drop a copy in there. Getting everything into one place now will save you from that panicked, last-minute scramble later. For a complete list of exactly what to gather, check out our home loan application checklist.

This kind of proactive organization really shows lenders you're serious and makes the entire process easier on everyone.

Polish Your Personal Financial Picture

Once your business documents are in order, it's time to shift focus to your personal credit and savings. Lenders look at these as direct proof of your financial discipline and how well you handle debt.

Here are the key things to work on:

- Monitor Your Credit: Sign up for a credit monitoring service so you can keep an eye on your score and get alerts if anything changes. You should be aiming for a score of 720 or higher to get your hands on the best interest rates and loan terms.

- Reduce Consumer Debt: Map out a plan to aggressively pay down high-interest debt, like credit cards and personal loans. Every dollar you pay down helps lower your Debt-to-Income (DTI) ratio, which is an absolutely critical number for self-employed borrowers.

- Build Your Cash Reserves: Start saving with a clear goal in mind: have at least 6 to 12 months of your future mortgage payment sitting in an easily accessible account. For most lenders, having this safety net is non-negotiable.

Following this action plan puts you in the driver's seat. Instead of just reacting to a lender's requests, you'll be proactively handing them a complete and compelling financial profile that answers their questions before they even ask.

The final, and most important, step in your preparation is to connect with a mortgage expert who truly understands the ins and outs of self employed mortgage requirements. Here at Mortgage Seven LLC, we live and breathe this stuff. We can review your progress, help you map out a personalized strategy, and get you pre-approved with total confidence.

Common Questions from Self-Employed Homebuyers

Even with a solid plan, you're bound to have questions. Getting a mortgage when you run your own business has its own set of rules. Here are a few of the most common things I hear from entrepreneurs and the straight answers you need.

What if I’ve Been Self-Employed for Less Than Two Years?

This is a big one. While lenders love to see a two-year track record, it’s not always a deal-breaker. You can sometimes get approved with just one year of self-employment history, but it really depends on your story.

Lenders need to see a logical progression. For instance, if you were a salaried graphic designer for five years and then started your own successful design agency 12 months ago, that makes sense. You’re in the same line of work, just for yourself now.

To make it work, you'll need to show you're a very strong borrower in other ways. Think:

- A great credit score, usually 720 or higher.

- More skin in the game with a larger down payment, often 10-20%.

- Plenty of cash reserves left over after closing.

This is where a good broker really shines, as we know exactly which lenders are open to these kinds of exceptions.

How Does My Business Debt Affect My Application?

This is a crucial detail that trips up a lot of people. Lenders will comb through your credit report, and if they see business loans or credit cards, they need to know who’s actually paying them.

The golden rule is to prove the business, not you, makes the payments. If you can show an underwriter 12 straight months of business bank statements with those payments coming directly from the business account, they can often leave that debt out of your personal DTI ratio.

But if you’ve been paying that business Amex from your personal checking account, you can bet it's going to count against you.

What Happens if My Income Dropped Last Year?

Underwriters are trained to look for stability, so a recent dip in your net income can raise a red flag for a conventional loan. You'll definitely need to write a clear letter of explanation for why it happened. Maybe you made a major one-time investment in new equipment or a specific market event impacted your industry.

If the drop was pretty significant, a traditional loan might be off the table. This is the exact situation where a bank statement loan can save the day, since it’s designed to look at your current cash flow, not what your tax returns said a year ago.

Are Interest Rates Higher for Bank Statement Loans?

In most cases, yes, they are a bit higher. Because these programs (often called Non-QM loans) use different ways to verify your income, lenders price in a little extra risk.

The rate you get isn't just a shot in the dark; it's tied directly to your financial strength—your credit score, how much you're putting down, and your overall reserves. For many business owners, paying a slightly higher rate is a smart trade-off to secure a mortgage based on the real money their business is making.

Ready to get answers tailored to your business? The team here at Mortgage Seven LLC lives and breathes this stuff. We know how to position your success to the right lender. Let’s put together a plan that gets you the keys to your new home.