Deciding whether to refinance your mortgage can feel like a massive, confusing puzzle. But a good should i refinance calculator is the one tool that makes all the pieces click into place. It gives you a clear, unbiased look at the numbers, helping you figure out if now is really the right time for you to make a move. Let's walk through how to use one to get a straight answer.

Is It The Right Time To Refinance Your Mortgage?

Pinpointing the perfect moment to refinance isn't just about chasing the lowest possible interest rate. It’s a much bigger picture—it's about making sure your mortgage fits your current financial reality and your goals for the future. A solid refinance calculator acts like your personal financial crystal ball, translating your unique situation into hard numbers you can actually work with.

For many homeowners, the biggest trigger is a noticeable drop in market interest rates. From my experience, if you can find rates that are at least 0.75% to 1% lower than what you're paying now, it's almost always worth a closer look. But your personal financial health is just as critical. Has your credit score jumped up since you first got your loan? If so, you could be in line for much better terms than you think.

Key Benefits a Calculator Helps You See

A quality calculator does more than just basic math; it shows you the real, tangible outcomes of refinancing. It's designed to quantify the main reasons people refinance in the first place, giving you a clear picture of what you stand to gain.

- Lowering Your Monthly Payment: This is the big one for most people. The calculator will spit out your new estimated monthly payment, showing you exactly how much cash you could free up every single month.

- Shortening Your Loan Term: Thinking about switching from a 30-year to a 15-year mortgage? The calculator can model that for you. You'll see precisely how much faster you'll build equity and, more importantly, the staggering amount of interest you'll save over the long haul.

- Tapping Into Home Equity: A cash-out refinance lets you borrow against the value you've built in your home. The calculator is perfect for weighing the benefit of that immediate cash against the true cost of taking on a new, larger loan.

Why Timing and Market Conditions Matter

The housing market is always in flux, and these shifts create windows of opportunity for refinancing. Take 2025, for example—as rates dipped, the refinance market exploded. We saw refinance applications surge by 43% from Q2 2024 to Q2 2025. It got even crazier with a massive 54.2% jump in September 2025 alone when rates finally dropped below 6.5%.

By the end of that year, an estimated 4.1 million homeowners were in a perfect spot to save money by refinancing. These numbers highlight why having a calculator on hand is so vital—it lets you monitor your own opportunities as the market changes. You can dive deeper into these mortgage market and housing trends to see how they might affect your decision.

A refinance calculator is your first line of defense against a bad financial decision. It cuts through the sales pitches and marketing noise to answer the one question that truly matters: "Will this move actually save me money after all the fees are paid?"

In the end, the calculator takes abstract financial data and turns it into a clear 'yes' or 'no.' It gives you the confidence you need to make the right call.

Quick Refinance Checklist

Before you spend a lot of time on applications, a quick check of these key indicators can tell you if you're on the right track. This isn't a substitute for running the numbers, but it's a great starting point.

Quick Refinance Checklist Key Indicators

| Indicator | What to Look For | Why It Matters |

|---|---|---|

| Interest Rate Drop | At least 0.75% lower than your current rate | This is the primary driver of monthly savings and the most common reason to refinance. |

| Credit Score | A significant increase since your last loan | A higher score unlocks better rates and terms, increasing your potential savings. |

| Home Equity | At least 20% equity built up | Lenders require this to avoid Private Mortgage Insurance (PMI) and for cash-out options. |

| Time in Home | You plan to stay for at least 3-5 more years | You need enough time to pass the "break-even point" and realize the savings after paying closing costs. |

| Financial Goals | Need cash for renovations, debt, or want to pay off the loan faster | Your "why" determines the type of refinance you should be looking for (e.g., cash-out vs. term reduction). |

If you can check off a few of these boxes, it’s a strong signal that it's time to fire up a calculator and see what a refinance could do for you.

Getting Your Numbers Together for an Accurate Calculation

Any should i refinance calculator is only as good as the numbers you plug into it. Think of it as "garbage in, garbage out." If you feed it vague or incorrect information, you'll get a skewed result that won't help you make a smart decision.

To get a truly useful preview of what refinancing could look like for you, you'll need to pull together a few key details first. Let's go over exactly what you need and where to find it. A few minutes of prep work now will make all the difference.

Your Current Mortgage Details

First things first, you need the specifics of your existing loan. The quickest way to get all this is to pull up your latest mortgage statement, which you can almost always find in your lender's online portal.

Here's what you're looking for:

- Current Principal Balance: This is the exact amount you still owe on the loan itself, not counting any future interest. It's the starting point for your new loan.

- Current Interest Rate: Pinpoint the exact interest rate you're paying today. This is the critical number you'll be comparing new offers against.

- Remaining Loan Term: Your statement should tell you how many years or payments you have left. If it only lists the original term (e.g., 30 years), you'll just have to subtract the time that's already passed since you first got the loan.

If you have an adjustable-rate mortgage (ARM), pay close attention to when your rate is set to change. That date can make refinancing a much more urgent priority.

Estimating Your Home Value and Credit Score

Next, you'll need two numbers that give a snapshot of your current financial situation. These help determine your loan-to-value (LTV) ratio and, most importantly, the new interest rate you're likely to get.

Home Value Estimation

You don't need a formal appraisal just to run the numbers. A quick check on major real estate websites can give you a solid ballpark figure for your home's market value. For an even better estimate, see what similar homes in your neighborhood have sold for recently. A realistic number here is crucial, as it directly impacts your home equity.

Your Credit Score

Your credit score is a huge factor in what rate a lender will offer you. Many credit card companies and banking apps now provide your score for free. A higher score typically means a lower rate, so knowing where you stand helps you enter a realistic target rate into the calculator.

Getting these numbers right is the single most important step. A small mistake in your current balance or an overly optimistic home value can throw off the entire calculation and point you in the wrong direction.

The Numbers You Need to Estimate

Finally, you’ll have to make a couple of educated guesses. The key here is to be realistic, maybe even a little conservative.

- Potential New Interest Rate: Do a quick search for the current average refinance rates. If your credit is excellent (think 740+), you can probably use the lowest rates you see as your target. If your score is a bit lower, it’s smart to add a quarter or even a half-percent to that rate for a more grounded estimate.

- Estimated Closing Costs: These fees usually land somewhere between 2% and 5% of the new loan amount. A good, quick estimate is to use 3%. So, for a $300,000 refinance, you'd be looking at roughly $9,000 in costs.

With all these details in hand, you’re ready to get a meaningful result. If you'd like to see what else you can calculate, you can explore the different types of mortgage calculators available from Mortgage Seven LLC. Taking a few moments to gather this info is what turns a simple calculator into a genuinely personal financial planning tool.

How to Make Sense of Your Calculator Results

Okay, you've plugged in all your numbers, and now the should i refinance calculator has spit out a bunch of new figures. This is where the rubber meets the road. These results hold the key to your decision, but they only make sense if you know how to read the story they're telling. Let's walk through what each number really means for your budget and your future.

The first thing that probably jumped out at you is the new estimated monthly payment. It’s the most immediate and satisfying number to look at, especially if it’s lower. A smaller payment directly boosts your monthly cash flow, freeing up money for other things, whether that’s saving for college, investing, or just having a little more breathing room.

But hold on. Don't let that shiny new payment be the only thing you focus on. It's just one piece of a much bigger puzzle. The real insight comes from looking at the total cost versus the long-term benefit.

The Metrics That Really Matter

Your results will highlight a few key figures that, when looked at together, paint the full picture of your refinance. Each one gives you a different angle on the financial trade-offs you're considering.

- Monthly Savings: This one's simple. It’s the difference between your old mortgage payment and the new one. If you're paying $2,200 now and the new payment is $1,950, you’re pocketing $250 every month.

- Total Closing Costs: This is the upfront cost of the new loan. A good rule of thumb is to expect these fees to be 2-5% of your loan amount. For a $300,000 loan, you could be looking at costs anywhere from $6,000 to $15,000.

- Lifetime Interest Savings: Now this is a powerful number. It shows you the total amount of interest you’ll avoid paying over the entire life of the new loan compared to sticking with your current one. This figure often runs into the tens of thousands of dollars and reveals the true long-term power of refinancing.

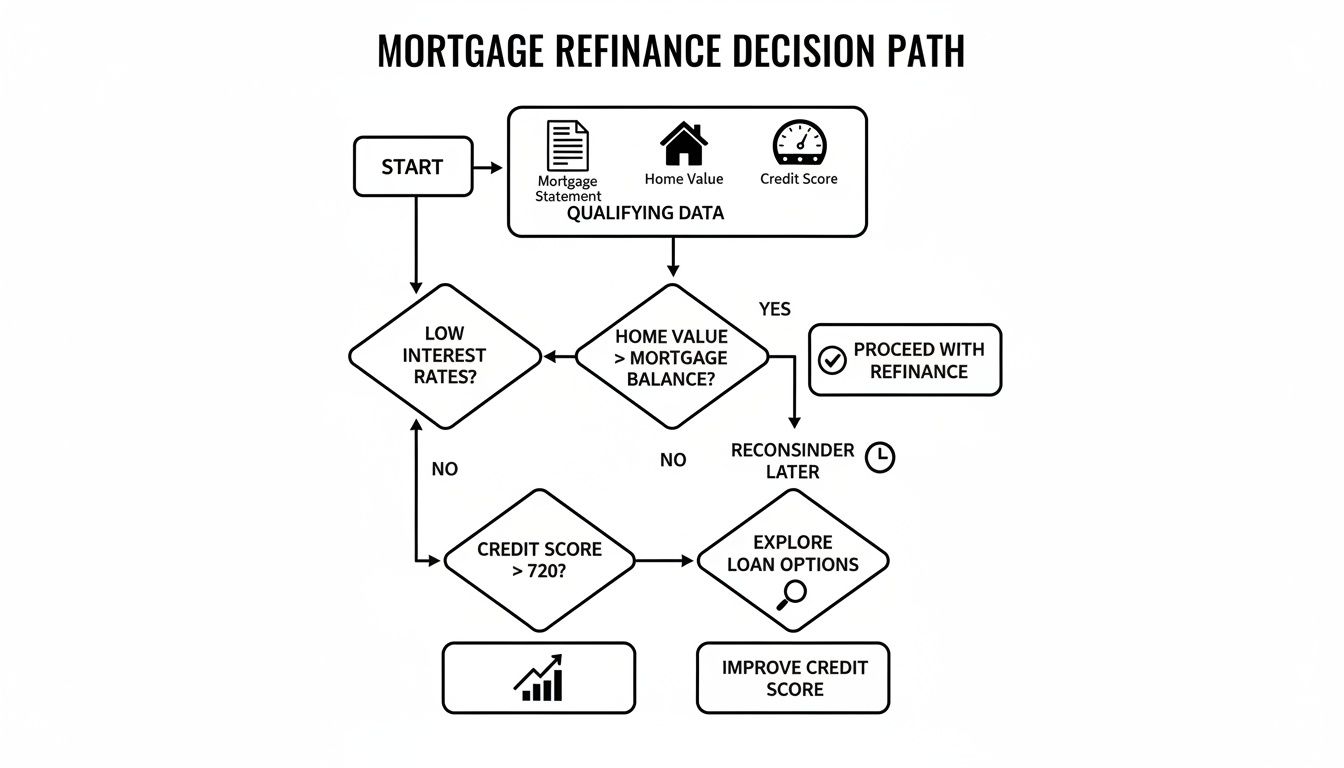

This decision path shows the key information you'll need to pull together for an accurate calculation, from your mortgage statement all the way to your credit score.

Having these details handy makes sure the calculator’s outputs—especially your break-even point—are as accurate as possible.

Your Break-Even Point Is Everything

Of all the numbers your calculator generates, the break-even point is the most important one to wrap your head around. It tells you exactly how many months it will take for your monthly savings to completely pay back your closing costs.

The break-even point is the milestone where your refinance stops costing you money and starts making you money. Every single month you live in your home after that point is pure, unadulterated savings.

The math is straightforward: just divide your total closing costs by your monthly savings.

Let's run a quick example:

- Total Closing Costs: $8,000

- Monthly Savings: $250

- Break-Even Point: $8,000 ÷ $250 = 32 months

In this case, you’d need to stay in your home for 32 months (that’s about 2.7 years) just to recoup the refinance fees. If you think you might sell in two years, this refinance would be a bad financial move. But if you're staying for at least five years, you'd get more than two years of pure savings.

From my experience, a shorter break-even point is always better. It minimizes your risk if life throws you a curveball and you need to move sooner than planned.

What the Numbers Mean for You

Let's bring this all together. Your calculator results are not just abstract figures; they are direct answers to your personal financial questions. I've put together this quick table to help you interpret the key outputs at a glance.

Understanding Your Refinance Results

| Calculator Output | What It Tells You | What to Aim For |

|---|---|---|

| New Monthly Payment | The immediate impact on your monthly budget and cash flow. | A lower number, unless your primary goal is shortening the loan term. |

| Break-Even Point | How long it takes for the refinance to pay for itself and become profitable. | A period significantly shorter than how long you plan to stay in the home. |

| Lifetime Interest Savings | The total long-term financial reward you'll get from the new loan. | The highest savings possible that still fits your monthly payment and term goals. |

By carefully reviewing each of these results, you can move from a vague "should I refinance?" to a confident, data-backed decision. The calculator transforms a complex financial choice into a clear cost-benefit analysis, showing you if the numbers truly work in your favor.

Exploring Different Refinance Scenarios

A good should i refinance calculator isn't just about punching in numbers to see if you can save a few bucks. Its real value comes from its flexibility. It lets you play out different financial futures to see which path actually makes sense for you. Refinancing isn't always about snagging a lower rate—it can be a smart move for boosting your cash flow, building wealth faster, or funding a big project.

To give you a feel for how this works in the real world, let's walk through three completely different situations. Each one starts with a unique goal, and the calculator is the tool that shows us the real-world trade-offs.

Scenario One: Lowering Monthly Payments

This is the one everyone thinks of first: the classic "rate-and-term" refinance. The goal is simple and immediate—cut down that monthly mortgage payment and get some breathing room in your budget.

Let's look at Alex. Five years ago, Alex took out a $400,000 mortgage with a 30-year fixed rate of 7.5%.

Here’s a snapshot of Alex's current loan:

- Original Loan: $400,000

- Current Balance: ~$382,000

- Interest Rate: 7.5%

- Monthly P&I: $2,797

- Time Left: 25 years

Now, rates have dipped, and Alex can get a new 30-year loan at 6.5%. The plan is to stay in the house for at least another 10 years, and the closing costs are estimated at $8,000. Plugging this into the calculator paints a very clear picture.

The new loan on the $382,000 balance at 6.5% brings the monthly payment down to $2,414. That's a $383 savings every single month. To figure out the break-even point, you just divide the closing costs ($8,000) by the monthly savings ($383), which comes out to about 21 months. Since Alex is staying put for years, this is a no-brainer.

Scenario Two: Paying Off The Loan Faster

Next up is Jamie, whose main focus is on building equity and getting out of debt as quickly as possible. Jamie also has 25 years left on a 30-year loan but is thinking about a much shorter 15-year term.

Here's where Jamie stands:

- Current Balance: $320,000

- Interest Rate: 6.8%

- Monthly P&I: $2,185

- Time Left: 25 years

Because shorter loan terms are less risky for lenders, they often come with better interest rates. Jamie qualifies for a 15-year fixed rate of 6.0%, with closing costs around $7,000. The calculator is about to show a very different outcome than Alex's.

The new payment on a $320,000 loan at 6.0% over just 15 years shoots up to $2,702. That's an increase of $517 a month. If you were only looking at the monthly payment, you’d walk away. But that’s not Jamie's goal.

The real win here is in the long game. By switching to a 15-year term, Jamie will own the home free and clear a full decade sooner and save an incredible $174,000 in total interest payments.

This is a perfect example of how the calculator helps you balance a short-term hit to your monthly budget against a massive long-term financial victory.

Scenario Three: Tapping Into Home Equity

Finally, let’s talk about the Martins. Their family is growing, and they desperately need to renovate—a bigger kitchen and another bedroom are no longer optional. A cash-out refinance could be the answer.

Here's their current mortgage situation:

- Current Balance: $250,000

- Home's Value: $500,000

- Interest Rate: 6.2%

- Monthly P&I: $1,612

They need $50,000 for the renovation, and they expect closing costs to be about $9,000. So, their new loan amount will be $309,000 (the $250k balance + $50k in cash + $9k for costs). They can lock in a new 30-year fixed rate at 6.9%.

The calculator shows their new monthly payment will be $2,025, an increase of $413. While that might seem steep, it's almost always a smarter financial move than putting a huge renovation on high-interest credit cards or personal loans, which can easily top 15%. To accurately model and compare these options, professionals rely on sophisticated lending software that can provide a crystal-clear analysis.

For the Martins, the calculator frames the decision perfectly. It's not just about "taking on more debt"; it’s about making a structured investment in their home's value and their family's day-to-day life.

As you can see, exploring different refinancing strategies and options is key. The "right" choice is completely tied to your personal goals, and a good calculator is your best friend for seeing every angle before you make a move.

What The Calculator Doesn't Tell You

A should i refinance calculator is a fantastic starting point. It gives you a clean, black-and-white look at the numbers—potential savings, break-even points, and the rest. It’s brilliant at math. But that's all it is: math. Its vision is narrow, and it can't see the full picture of your life and financial situation.

The numbers are your first step, but they absolutely don't tell the whole story. To make a decision you won't regret later, you have to look beyond the calculator's results and weigh the real-world factors it simply can't compute.

Your Long-Term Plans for the Home

The biggest blind spot for any calculator? Your future. It has to assume you'll stay in your home long enough to make the refinance worthwhile, but life rarely follows a perfect script. So, you have to ask yourself the tough question: how long are we really going to be here?

Let's say the calculator shows a break-even point of 36 months. That sounds great. But if you know a job relocation could be on the horizon in two years, then refinancing becomes a guaranteed money-loser. You'd sell the house before you ever paid back the closing costs, essentially flushing thousands of dollars down the drain.

Think of your break-even point as the minimum time commitment. If you can't confidently see yourself staying in the house for at least that long, walking away from the refinance is probably the smartest play.

No algorithm can guess your career trajectory or shifting family needs. Be brutally honest with yourself about your plans before you sign on for a new loan.

The Hidden Impact on Your Taxes

Here's something else the calculator screen won't show you: the tax implications. When you refinance to a lower interest rate, you're obviously going to pay less in mortgage interest each year. That’s the whole point, right? But this has a knock-on effect on one of the biggest tax perks of homeownership.

A smaller interest payment means a smaller mortgage interest tax deduction. For homeowners in higher tax brackets, this can sometimes eat into the savings from that lower monthly payment.

Now, this is rarely a deal-breaker for an otherwise solid refinance, but it's a detail you need to be aware of. The calculator shows you gross savings, not your net savings after the IRS has had its say.

Short-Term Credit Score and Closing Cost Details

The refinancing process itself causes a few temporary ripples in your financial life that the calculator ignores. Knowing what to expect can help you navigate the process without any surprises.

-

A Temporary Hit to Your Credit: When you apply, lenders will pull your credit report. This hard inquiry can cause a small, temporary dip in your score. On top of that, you're closing a seasoned loan account and opening a brand-new one, which can slightly affect the average age of your credit history. Your score will almost always bounce back within a few months, but it’s something to keep in mind if you plan on applying for other credit, like a car loan, in the near future.

-

Closing Costs Aren't Just One Number: A calculator asks for a single estimate for closing costs, but it's never just one fee. It's a collection of charges like appraisal fees, title insurance, loan origination points, and attorney costs. Getting an itemized breakdown helps you see exactly where every dollar is going.

While a refinance calculator gives you powerful numbers to work with, it's just one piece of the puzzle. It can't tell you about eligibility for specific programs or unique circumstances. For instance, if you're an ITIN holder, learning about options for a Mortgage Loan With Itin requires a conversation, not just a calculation. At the end of the day, the numbers guide you, but your personal context makes the final decision.

Taking Your Next Steps with Mortgage Seven LLC

So, you've crunched the numbers with a should i refinance calculator and have a pretty good idea of what a new mortgage could do for you. That's a fantastic first step. But remember, a calculator gives you an estimate—a snapshot based on general data.

To get the real story, you need to see the actual rates and terms you qualify for. This is where you move from the what-ifs of an online tool to the concrete reality of a professional mortgage quote.

From Calculation to Consultation

Think of your calculator results as your roadmap. Now, it's time to talk to a guide who knows the terrain inside and out. That's where we come in.

A no-obligation chat with our team at Mortgage Seven LLC is the logical next step. We’ll look at the scenarios you’ve run, listen to what you’re hoping to accomplish, and then match you with real-world loan options from our network of lenders.

Whether you're after a lower monthly payment, a shorter loan term, or need to pull cash out for a home improvement project, we're here to help you navigate the options—from conventional loans to FHA and jumbo refinancing.

A calculator shows you what’s possible. A mortgage professional shows you what’s attainable. We help you connect the dots between your goals and the loan products that can make them a reality.

Working with our Fairfax, VA team means you get an advocate in your corner. We cut through the jargon and simplify the entire process, from helping you gather the right documents to laying out lender offers side-by-side so you can make a clear, confident decision.

Seizing the Right Opportunity

The mortgage market doesn't sit still. Rates fluctuate, creating windows of opportunity that you need to be ready for. In fact, market forecasts show that total single-family mortgage originations are projected to grow to $2.2 trillion in 2026.

More specifically, refinance originations are expected to climb 9.2% to $737 billion as homeowners take advantage of rate dips. You can explore the full mortgage industry forecast to see the data for yourself.

This is why timing is everything. When you're ready to make a move, we help you get all your ducks in a row so you can act fast when the perfect rate appears. Want to get a head start? Take a look at our complete refinance application checklist.

Reaching out to Mortgage Seven LLC is how you turn those calculator estimates into a successful refinance. Let's work together to lock in the savings you've been looking for.

Frequently Asked Questions

Even with a great calculator, you're bound to have some questions. It’s a big decision, after all. Here are some of the most common things homeowners ask when they start exploring their refinance options.

How Accurate Is A Refinance Calculator?

A refinance calculator is only as good as the numbers you put into it. If you feed it accurate data, it will give you a very reliable estimate.

But remember, it’s still an estimate. The calculator’s results are based on your best guess for the new interest rate and closing costs. Your actual rate and final fees can only be locked in after you officially apply and a lender reviews your full financial picture. Think of the calculator as an excellent starting point—a way to see if refinancing is even in the ballpark for you, not as a final, binding quote.

Can I Refinance With Less Than 20 Percent Equity?

Yes, absolutely. Refinancing with less than 20% equity is quite common, but it usually has one important catch: Private Mortgage Insurance (PMI).

If your loan-to-value (LTV) ratio is over 80% on a conventional loan, you'll likely have to pay PMI on the new loan. A good refinance calculator will have a field for this so you can add that extra monthly cost. This is crucial because it helps you see if the savings from a lower rate are enough to offset the new PMI payment.

A refinance calculator is your personal "what-if" machine. Use it to play with different scenarios. See what happens if you add PMI or if you can only get a slightly higher interest rate. This is how you get a clear, realistic picture of your potential savings.

Does Using A Refinance Calculator Affect My Credit Score?

Not at all. Using an online should i refinance calculator has zero impact on your credit score.

These tools are for your eyes only. They don't ask for a Social Security number or trigger a "hard" credit inquiry. Feel free to run numbers all day long—it won't show up on your credit report. A hard inquiry only happens much later in the process, when you formally submit a loan application to a lender.

Ready to see if the numbers work for your specific situation? The expert team at Mortgage Seven LLC can give you the concrete figures and personalized advice you need to move forward with confidence. Schedule your no-obligation consultation today!