If you've ever wondered what affects mortgage interest rates, you're not alone. The short answer is it’s a combination of three big things: the wider economic conditions (which you can't control), the lender's internal business pricing, and your own personal financial health. All three of these pieces come together to create the final rate you see on a loan offer.

Cracking the Code of Mortgage Rates

The best way to think about your final mortgage rate is to picture it as a three-layer cake. Each layer represents a different set of factors, and stacking them up explains why rates can feel so unpredictable—varying from person to person and even from one day to the next.

We're going to slice into each of those layers. This will give you the inside knowledge you need to find the best financing for your home.

It doesn’t matter if you’re a first-time buyer in Fairfax looking at conventional loans, an investor using a DSCR loan for a rental property, or a small business owner who needs a bank-statement loan. The core principles behind mortgage rates are the same for everyone. Getting a handle on them is your first step toward a smarter, more confident home-buying journey.

The Three Layers of a Mortgage Rate

This "rate cake" model makes it easy to visualize how it all works. Each layer builds on the one below it, leading to the specific rate a lender ultimately offers you.

The Base Layer: The Economy. This is the foundation. It’s made up of huge, market-wide forces like Federal Reserve policy, the inflation rate, and how the bond market is behaving. These elements establish the basic "cost of money" for every lender out there, and they're completely out of your hands. When you hear on the news that rates are going up or down, it’s this layer they're talking about.

The Middle Layer: Lender Pricing. On top of that economic base, each lender adds its own layer. This accounts for their business costs, their appetite for risk, and the profit margin they need to stay in business. This is precisely why you can get slightly different rate quotes from two different lenders on the exact same day.

The Top Layer: Your Financial Profile. This final, crucial layer is all about you. It's built from the factors you have direct control over, like your credit score, the size of your down payment (which determines your Loan-to-Value), and your debt-to-income (DTI) ratio. The stronger your financial profile, the less risky you appear to a lender—and the better rate they'll offer you as a result.

Understanding this structure is key. You can't change the U.S. economy, but you can strengthen your personal financial profile and shop around for lenders with the most competitive pricing. That gives you a surprising amount of power over your final rate.

Let’s take a closer look at each of these layers, starting with the big-picture economic drivers and then drilling down into the specific, actionable steps you can take to land the best rate possible.

Key Factors Influencing Your Mortgage Rate at a Glance

To quickly recap, the interest rate you're offered isn't just one number; it's the result of several components working together. This table breaks down the three main categories of influence.

| Factor Category | What It Is | How It Impacts Your Rate |

|---|---|---|

| Broad Economic Conditions | Macroeconomic factors like inflation, the 10-Year Treasury yield, and Federal Reserve policy. | These set the baseline for all mortgage rates. When they rise, all rates tend to rise. This is the "wholesale" cost of money. |

| Lender-Specific Pricing | Each lender's operational costs, profit margins, and risk assessment for different loan types. | This is the lender's "markup." It's why rates vary between banks, credit unions, and mortgage brokers, even for the same borrower. |

| Your Borrower Profile | Your personal financial details, including your credit score, DTI ratio, LTV ratio (down payment), and loan type. | This is the personalized risk adjustment. The stronger your profile, the lower the lender's risk, resulting in a lower rate for you. |

Think of it this way: the economy sets the floor, the lender adds their margin, and your personal profile determines your final position on their pricing sheet. By focusing on what you can control—your own finances and your choice of lender—you can significantly improve your outcome.

How the Economy Shapes Your Mortgage Rate

Long before a lender looks at your credit score, the stage for your mortgage rate has already been set by massive economic forces. Think of these as the deep ocean currents that steer every ship in the water, from giant tankers to small sailboats.

While you can't control these currents, understanding them is like having a reliable weather forecast. It helps you make sense of why rates are moving up or down and gives you the context to make smarter decisions about your own mortgage.

The Federal Reserve and Inflation

The biggest player in this economic ocean is the U.S. central bank, better known as the Federal Reserve or "the Fed." One of its most critical jobs is to keep inflation in check. Inflation is just a fancy word for the rate at which prices for everyday goods and services go up, which means your dollar buys less tomorrow than it does today.

When inflation gets too hot, the Fed typically steps in and raises its benchmark interest rate. While this rate isn't your mortgage rate, it triggers a chain reaction. Suddenly, it costs banks more to borrow money from each other, and they inevitably pass that extra cost on to you through higher rates on all loans, including mortgages.

Inflation is a powerful driver of mortgage rates because lenders have to protect the value of their money. History shows a dramatic link: in the early 1980s, U.S. inflation soared past 10%, and 30-year mortgage rates followed, hitting a staggering 16.64% average in 1981. Fast forward to 2021, when inflation was a tame 2%, and rates dropped to a rock-bottom 2.96%, kicking off a home-buying and refinancing frenzy.

At its core, it's simple. Lenders need to make sure the payments you make over 30 years won't be worthless due to rising prices. High inflation means they have to charge a higher interest rate to protect their investment.

The Bond Market and Treasury Yields

While the Fed sets the general direction, the most immediate signal for mortgage rates comes from the bond market—specifically, the yield on the 10-year Treasury note.

It's a surprisingly direct relationship. Imagine the 10-year Treasury yield is a huge cargo ship, and mortgage rates are a smaller boat tied to it. When the big ship turns, the little boat gets pulled right along with it.

So, why are they tied together? Mortgages are often packaged together and sold to investors as mortgage-backed securities (MBS). These investors need a safe place to put their money, and U.S. Treasury bonds are considered the safest investment on the planet.

To convince an investor to buy a slightly riskier MBS instead of a super-safe Treasury bond, the MBS has to offer a better return (a higher yield). This means that whenever Treasury yields climb, MBS yields have to climb, too, to stay attractive. Those higher costs are then passed directly to homebuyers as higher mortgage rates.

Overall Economic Health

Finally, the general vibe of the economy has a big say in where rates go. It might feel a bit backward at first.

- A Strong Economy: When jobs are plentiful and wages are going up, more people are confident enough to buy homes. This high demand, often coupled with fears of inflation, tends to push mortgage rates higher.

- A Weak Economy: During a recession, the opposite happens. The Fed often cuts rates to encourage spending, housing demand cools off, and investors run to the safety of bonds. This flood of money into bonds pushes their yields—and mortgage rates—down.

Getting a handle on these forces can feel like learning a new language, but even a basic understanding goes a long way. Exploring the leading economic indicators that analysts watch can give you a peek into where things might be headed.

This big-picture view is exactly why timing matters so much. Knowing when the economic tides are in your favor is crucial for locking in the best possible rate, and it’s why understanding the best time to refinance your mortgage can save you a fortune over the life of your loan.

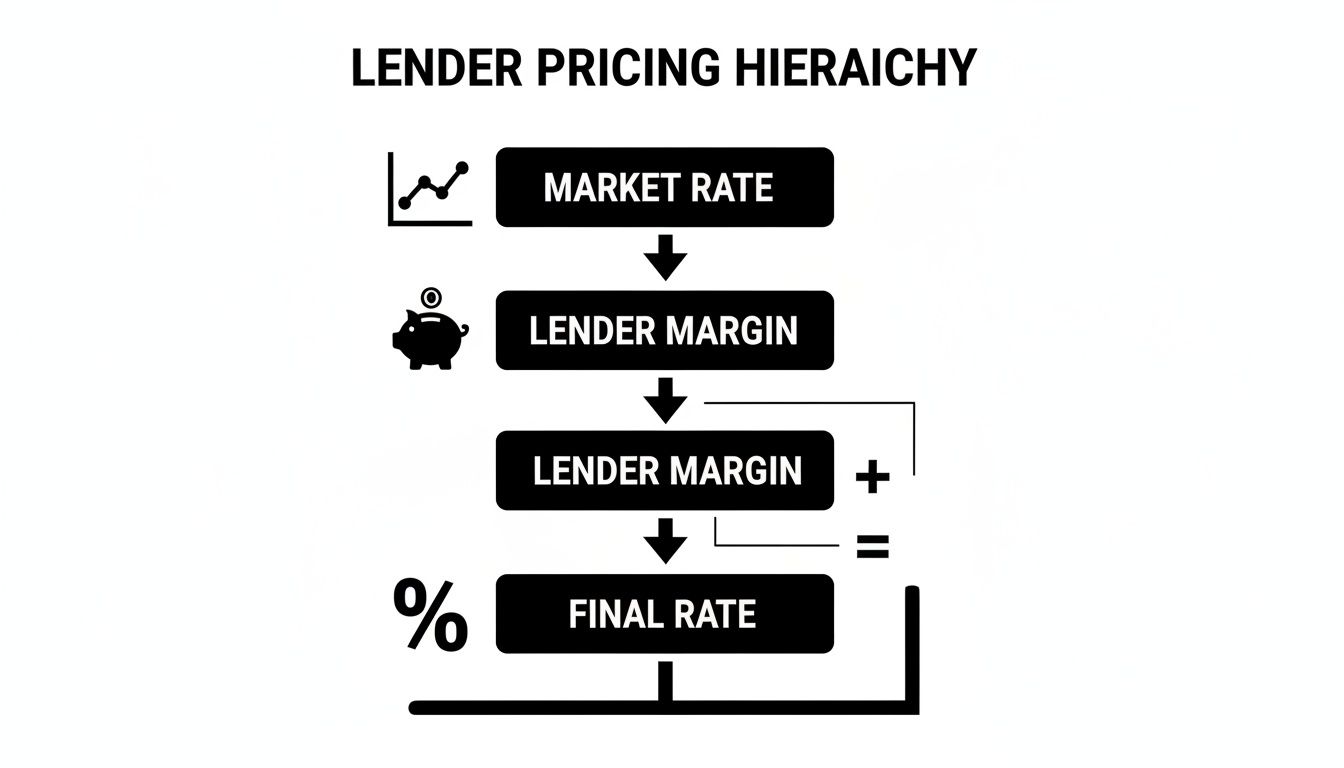

How Lenders Set Their Prices (And Make a Profit)

While the big-picture economy sets the stage, lenders aren't just passing along their "wholesale" cost of money directly to you. They're businesses, after all. They have salaries to pay, lights to keep on, and a need to turn a profit.

This is the second layer of what determines your final rate: the lender's own pricing and profit margin.

Think of a mortgage lender like a local bakery. The bakery buys flour, sugar, and butter at a wholesale price. But the price of a croissant isn't just the cost of its ingredients. The final price has to cover the baker's salary, the rent for the shop, and a little bit of profit. Mortgage lenders do the exact same thing with money.

What Is the Lender's Margin?

The gap between the rock-bottom market rate and the actual rate you're quoted is often called the lender's margin or "spread." This isn't just pure profit. It's a carefully calculated number that covers the real costs of doing business.

- Operational Costs: This is the big one. It covers everything from loan officer commissions and underwriter salaries to marketing budgets and office rent.

- Risk Management: Lenders might add a tiny premium for certain loan types they see as slightly riskier, even before they’ve looked at your personal financial profile.

- Profit: At the end of the day, lenders are for-profit companies. A slice of that margin is their return for lending you a huge sum of money for up to 30 years.

This is precisely why you can apply at two different banks on the exact same day and get two totally different rate quotes. One lender might have higher overhead or a more conservative approach to risk, forcing them to build a larger margin into their pricing.

The Hidden Engine: Mortgage-Backed Securities

So, where does a lender get the hundreds of thousands of dollars to fund your loan in the first place? They don't typically just pull it from a vault. Instead, they tap into a massive financial engine built on Mortgage-Backed Securities (MBS).

It's a constant cycle:

- Your lender gives you a mortgage.

- They then pool your loan together with thousands of others.

- This giant pool of mortgages is then sold to investors on the secondary market as an MBS.

This process is what keeps the whole system moving. It gives the lender fresh capital to turn around and fund the next person's home loan. When investors are hungry for these MBS, lenders can sell their loans easily, which boosts the supply of mortgage money and helps keep rates competitive for borrowers like you.

But when investor demand for MBS dries up, it gets more expensive for lenders to sell off their loans. That tightens the supply of capital, and they have no choice but to charge higher interest rates to make up for it.

Why You Absolutely Must Shop Around

Once you understand that every lender adds their own unique margin, you realize why getting just one quote is a huge financial mistake. Lenders will dig deep into your application, sometimes using complex metrics like the Debt Service Coverage Ratio (DSCR) to measure an investment property's cash flow, which can directly influence your rate.

This is where a good mortgage broker really shines. A broker isn't tied to a single bank's pricing model. They can take your one application and shop it to dozens of different lenders, pitting them against each other to find the one with the slimmest margin for your specific situation. This can unlock savings you’d never find on your own.

Your Financial Profile: The Factors You Actually Control

While the big-picture economy sets the stage for interest rates, the factors you can personally influence are what truly drive the final number you're offered. This is where your financial habits pay off. Lenders are looking at more than just the market; they’re sizing you up to see how much risk you bring to the table.

Think of it like getting a quote for car insurance. The make and model of the car set a baseline cost (the market rate), but your driving record, age, and where you live (your financial profile) determine your final premium. A clean record shows you're a safe bet, earning you a much better price.

For lenders, a stronger financial profile signals reliability and lower risk, which translates directly into a lower, more favorable interest rate.

As you can see, the rate you're quoted isn't just the market rate. It’s the market rate plus a margin the lender adds based on their assessment of you. Let's break down exactly what they're looking at.

Your Credit Score: The Ultimate Trust Signal

Of all the numbers in your financial life, your credit score is the most critical when it comes to getting a mortgage. It’s a snapshot of your entire history with debt, and for a lender, it’s the clearest signal of whether you’ll pay your mortgage on time.

A higher score screams "low risk," and lenders will compete to win your business with their best rates.

FICO scores, the industry standard, run from 300 to 850. Lenders typically sort these scores into tiers, with each tier getting a different pricing adjustment.

- Excellent (740-850): You're in the driver's seat. Borrowers here get the lowest interest rates lenders have to offer.

- Good (670-739): You’ll still land a very competitive rate, but it will be a touch higher than what the top-tier folks get.

- Fair (580-669): As the perceived risk goes up, so do the rates. You’ll see a noticeable bump in your rate in this range.

- Poor (Below 580): It's tough to qualify for a conventional loan here, and if you do, the rate will be significantly higher to compensate for the risk.

Even a handful of points can make a massive difference. Someone with a 760 score might be offered a rate 0.5% lower than a borrower with a 670. That small percentage can add up to tens of thousands of dollars in savings over the life of the loan. You can learn more by reading our guide on the ideal credit score for a mortgage.

Loan-to-Value (LTV) Ratio and Your Down Payment

Next up is your Loan-to-Value (LTV) ratio. This is a simple but powerful metric that compares your loan amount to the home's appraised value. A bigger down payment gives you a lower LTV, which every lender loves to see.

Put yourself in the lender's shoes. If you put 20% down, you have serious "skin in the game." You're far less likely to walk away from that investment. But if you only put 3% down, the lender is taking on almost all the risk.

Lenders reward a lower LTV with better pricing. An LTV of 80% or less (meaning a 20% down payment or more) will not only help you secure a better rate but also lets you avoid the extra cost of Private Mortgage Insurance (PMI).

Debt-to-Income (DTI) Ratio and Your Monthly Budget

Your Debt-to-Income (DTI) ratio shows lenders how much of your monthly income is already spoken for by other debts—things like car payments, student loans, and credit card bills. It’s a quick check on your financial breathing room.

A high DTI is a red flag that you might be stretched too thin to comfortably handle a new mortgage payment. Most conventional loan programs prefer a DTI of 43% or less, though some can go as high as 50%. A lower DTI proves you have a healthy cash flow, making you a much safer bet for a loan and helping you nab a better rate.

To give you a clearer picture, here’s how these key metrics can influence the rate a lender might offer you.

How Your Financial Profile Impacts Your Mortgage Rate

| Financial Metric | Good | Average | Needs Improvement | Impact on Rate |

|---|---|---|---|---|

| Credit Score | 740+ | 670 – 739 | Below 670 | The single biggest factor; higher scores get the lowest rates. |

| Loan-to-Value | 80% or less | 81% – 95% | 96%+ | Lower LTV means less risk and a better rate. |

| Debt-to-Income | Below 36% | 37% – 43% | Above 44% | Lower DTI shows you can comfortably afford the payment. |

As you can see, being in the "Good" column across the board puts you in the strongest possible position to secure the best mortgage terms.

Loan and Property Characteristics

Finally, a few other details about the loan and the property itself can nudge the rate up or down.

- Loan Term: A 15-year mortgage almost always has a lower rate than a 30-year loan. Why? The lender gets their money back twice as fast, reducing their long-term risk.

- Loan Type: Government-backed loans (like FHA) can be a great option for borrowers with less-than-perfect credit but often include mortgage insurance for the life of the loan. Jumbo loans (for amounts above conforming limits) have their own separate pricing.

- Property Type: Rates are best for your primary residence. Lenders see investment properties and second homes as higher risk, so they typically come with slightly higher interest rates.

Taking control of these factors is your most powerful strategy for locking in a fantastic mortgage rate, no matter what the markets are doing.

The Strategic Moves That Can Change Your Final Rate

Beyond your financial history, the specific choices you make when setting up your mortgage can have a huge impact on the final rate you get. These are the tactical decisions you make right before you sign on the dotted line.

Two of the most powerful tools you have are the rate lock and mortgage points. Getting a handle on these two concepts gives you a ton of control, helping you sidestep market volatility and shape your loan to fit your bigger financial picture. Let's break down how each one works.

Locking in Your Rate for Peace of Mind

Think about booking a flight. When you find a great price, you don't just leave it in your cart for a week and hope for the best, right? You grab it immediately to lock in that deal. A mortgage rate lock is the exact same idea.

A rate lock is basically a promise from your lender to give you a specific interest rate for a set amount of time, usually 30 to 60 days, while they finish up the paperwork and underwriting. This is your shield against market swings. If rates suddenly shoot up the week before you close, you’re protected—your locked rate isn't going anywhere.

Key Takeaway: A rate lock takes the guesswork out of the final stretch of buying a home. It turns a moving target into a fixed number, so you can budget with total confidence.

This is more important than ever in a market where economic news and bond market jitters can make rates jump around daily. For example, a report showing strong economic growth could cause the Fed to signal a policy change, sending rates climbing without warning. Having your rate locked protects you from that chaos.

Using Mortgage Points to Buy a Lower Rate

While a rate lock defends you against future rate hikes, mortgage points let you go on the offense and actively lower your rate from the start. It’s like pre-paying some of your interest at closing in exchange for a lower interest rate for the entire life of your loan.

One "point" costs 1% of your total loan amount. By paying for points at closing, you can "buy down" your interest rate. How much it drops varies by lender and what the market is doing, but a good rule of thumb is that one point might lower your rate by about 0.25%.

Running the Numbers: The Break-Even Point

Buying points is a strategic investment, but it's definitely not for everyone. The whole game is figuring out your break-even point—that's the moment when the money you've saved each month from the lower rate has completely paid back what you spent on the points upfront.

Let's walk through a quick example:

- Loan Amount: $400,000

- Original Rate (No Points): 6.50% (Monthly P&I: $2,528)

- Cost of 1 Point (1%): $4,000

- New Rate (With 1 Point): 6.25% (Monthly P&I: $2,462)

Now, let's find that break-even point:

- Find Your Monthly Savings: $2,528 – $2,462 = $66 per month

- Calculate the Break-Even Point: $4,000 (Cost of Point) ÷ $66 (Monthly Savings) = 60.6 months

In this scenario, it would take you just over five years to make back the initial $4,000 cost. If you're planning on staying in the home well beyond that, buying the point is a smart financial move that will save you money for years to come. But if you think you might sell or refinance in just a few years, you'd end up losing money on the deal. This is why knowing how to compare mortgage lenders is so crucial when you're weighing these kinds of offers.

A Few Common Questions About Mortgage Rates

When you're diving into the world of mortgages, a few key questions always seem to pop up. Getting straight, practical answers is the best way to move forward with confidence. Let's tackle some of the most common ones borrowers ask about what really drives their interest rate.

What's the Real Difference Between "Interest Rate" and "APR"?

This is probably one of the most important—and confusing—distinctions for a homebuyer. It's crucial to get this right.

Your interest rate is simply the cost of borrowing the money, expressed as a percentage. It’s the number that’s used to calculate the principal and interest portion of your monthly payment.

The Annual Percentage Rate (APR), however, gives you the bigger picture. Think of it as the "all-in" cost. The APR takes your interest rate and bundles in most of the other lender fees required to get the loan, like origination charges, discount points, and certain closing costs. This is why the APR is almost always a bit higher than the interest rate.

Here’s a simple way to think about it:

- The interest rate is like the price on the menu.

- The APR is the final bill after all the taxes and service fees are added.

Lenders are legally required to show you the APR for a very good reason: it lets you make a true apples-to-apples comparison between different loan offers. A loan that looks tempting with a super-low interest rate might actually be more expensive overall if it's loaded with fees, and the higher APR will reveal that.

When Should I Lock My Mortgage Rate?

Trying to time your rate lock can feel a lot like trying to time the stock market, but you can be strategic about it. A rate lock is a lender's promise to hold a specific interest rate for you for a set time, usually 30 to 60 days. It’s your shield against the daily ups and downs of the market while your loan is being finalized.

The best time to lock is usually when you have a signed purchase contract on a house and you're comfortable with the rate being offered. If you're seeing headlines about inflation or the Fed hinting at rate hikes, locking sooner rather than later can save you a lot of money and stress.

On the flip side, what if you think rates might drop? You could "float" your rate, which means you hold off on locking it in. This is a gamble, plain and simple. You might snag a lower rate, but you’re also completely exposed if rates suddenly jump. Some lenders offer a "float-down" option, which costs a bit extra but gives you the best of both worlds: you can lock your rate but still capture a lower one if the market moves in your favor before you close.

Your mortgage advisor's insight is golden here. They live and breathe this stuff and can offer expert analysis on market signals to help you decide whether locking or floating makes more sense for you.

How Much Does My Choice of Loan Affect My Rate?

The type of loan you choose has a massive impact on your interest rate. Different loan programs are built for different borrowers and carry different risk profiles for the lender, which is always reflected in the rate.

Fixed-Rate vs. Adjustable-Rate: The classic 30-year fixed-rate mortgage is popular for a reason—it offers predictability and stability for the long haul. An Adjustable-Rate Mortgage (ARM), however, typically starts with a lower, introductory "teaser" rate for a few years (like 5 or 7) before it starts adjusting with the market. An ARM can be a great tool if you know you'll likely sell the home before the fixed period ends.

How Long You're Borrowing For: A 15-year fixed-rate loan will almost always have a lower interest rate than a 30-year loan. The logic is straightforward: the lender gets their money back twice as fast, which dramatically cuts their risk. Your monthly payments will be higher, of course, but you'll build equity like crazy and save a fortune in total interest over the life of the loan.

Government-Backed vs. Conventional: Loans insured by the government, like FHA and VA loans, can open doors for borrowers with less-than-perfect credit or smaller down payments, often with very competitive rates. Just be aware they come with their own rules and costs, like the FHA's mandatory Mortgage Insurance Premium (MIP).

Other Specialized Loans: There are all sorts of loan products out there. Jumbo loans (for loan amounts above the conforming limit) are priced a bit differently. And loans for investment properties, like DSCR loans, are priced based on the property’s rental income potential, not your personal W-2, which means a totally different risk calculation for the lender.

Finding the right loan program for your specific financial DNA is one of the most powerful ways to secure a great rate. A good mortgage broker who can shop dozens of lenders on your behalf is an invaluable partner in this process.

At Mortgage Seven LLC, our job is to make all of this clear and simple. Our team provides the expert guidance you need to understand every factor affecting your rate, ensuring you find the perfect loan for your situation. To start your journey with a team dedicated to your success, schedule a consultation with us today.