Think of a mortgage broker as your personal shopper for a home loan. They are a licensed intermediary who connects you, the borrower, with a whole network of lenders to find the best possible mortgage for your situation. It's a huge advantage.

Unlike a bank employee who can only offer you their own institution's products, a broker shops your loan application around. This creates competition for your business, which is exactly what you want. It's the best way to increase your chances of securing a better rate and more favorable terms.

What Is a Mortgage Broker and How Do They Work for You?

Navigating the world of home loans can feel like trying to find one specific key in a room full of locked doors. Each door represents a different lender, and behind each one is a unique set of rules, rates, and requirements.

When you go directly to a bank, you only get to try the key for that one door. A mortgage broker, on the other hand, comes equipped with a master key ring.

Brokers are licensed financial professionals who live and breathe mortgages. Their job isn’t to lend you money directly. Instead, they act as your personal advocate and guide through the entire financing maze. They start by getting to know you—your financial picture, your credit history, and your goals for buying a home.

Armed with that knowledge, they tap into their extensive network of lenders. This network can include everything from large national banks to smaller, niche credit unions, allowing them to find loan options that truly fit your profile.

The Broker Advantage Unpacked

The real value of a good mortgage broker boils down to two things: access and expertise. They have established relationships with wholesale lending partners that the general public simply can't access on their own.

This creates a competitive marketplace where lenders are essentially bidding for your loan. The result for you? It can mean significant savings on your interest rate and closing costs over the 15 or 30 years you'll have that mortgage.

On top of that, brokers do a lot of the heavy lifting. They manage the application, help you gather and organize all the necessary documents, and handle the back-and-forth communication with lenders. This saves you a massive amount of time and cuts down on the stress that always comes with securing a home loan. If you're looking for more details, the brokermap Homepage offers a great overview of what brokers do.

A broker's loyalty is to you, the borrower, not to any single lending institution. Their goal is to match you with the most suitable loan, regardless of which lender provides it.

To really see the difference, it helps to compare the two main paths a homebuyer can take.

Mortgage Broker vs Direct Lender at a Glance

This table breaks down the key differences between working with a mortgage broker and going directly to a bank's loan officer.

| Feature | Mortgage Broker | Direct Lender (Loan Officer) |

|---|---|---|

| Loan Options | Access to multiple lenders and dozens of loan programs. | Limited to the products offered by one specific bank. |

| Allegiance | Works for you, the borrower, to find the best deal. | Works for the bank, motivated to sell that bank's products. |

| Rate Shopping | Shops your single application to many lenders at once. | You must apply individually to each bank to compare rates. |

| Expertise | Offers broad market knowledge and creative financing solutions. | Deep knowledge of their own bank's specific guidelines. |

As you can see, the biggest distinction is choice. A broker provides a wide-angle view of the market, while a direct lender can only show you what’s available from their own shelf.

How a Broker Differs from a Direct Lender

When you’re ready to get a home loan, you have a big decision to make right out of the gate: who do you go to? This choice is a huge deal, as it directly shapes your interest rate, the fees you'll pay, and the loan options you even get to see. Your two main paths are going to a direct lender—think a bank or a credit union—or teaming up with a mortgage broker.

The real difference boils down to who they work for. A loan officer at a bank is an employee of that bank. Their job is to sell you the mortgage products their employer offers. That’s it. You're only seeing one small, hand-picked menu from the vast world of mortgages.

A mortgage broker, on the other hand, works for you. Their loyalty isn't tied to a single lender's bottom line. Their mission is to sift through a huge network of lenders to find the absolute best loan for your specific financial picture.

The Power of Wholesale Access

A broker's secret weapon is their access to the wholesale lending market. This is a part of the industry that regular consumers just can't get into on their own. Lenders operating in this space can often offer more competitive rates and lower fees because they don't have the massive overhead of retail branches and expensive ad campaigns.

Here's an easy way to think about it: A direct lender is like a brand-name store that only sells its own products. A mortgage broker is like your own personal shopper who has an all-access pass to an exclusive, members-only wholesale club where the prices are better and the selection is massive. They take your application into that club and let the different vendors compete for your business.

That competition is what saves you money. Instead of you having to fill out application after application at different banks—and taking a credit hit each time—a broker does the heavy lifting. They use a single application to shop your loan around their entire network, essentially creating a bidding war where you come out the winner.

A direct lender tells you what they can offer. A mortgage broker finds out what the entire market can offer you. This simple shift is what gives borrowers a massive leg up in securing better rates and terms.

A Real-World Fairfax Scenario

Let's picture a homebuyer right here in Fairfax, VA. They head to their local bank, where they’ve had a checking account for years. The loan officer is pleasant and offers them a conventional loan with a 7.1% interest rate. It sounds okay, right?

But this buyer is savvy and decides to chat with a local mortgage broker, too. The broker takes one look at their file and knows they qualify for a program with a different wholesale lender that offers a 6.8% interest rate. That tiny difference saves the buyer thousands in just the first few years and more than $65,000 over the life of a 30-year mortgage on a $500,000 loan.

This is the broker's value in a nutshell. They aren't stuck with one company's rate sheet. Their job is to know the market inside and out, allowing them to pair your unique profile—whether you're a first-timer, a real estate investor, or self-employed—with the one lender who wants your business the most. You can explore this further in our article on the key differences between a mortgage broker and a bank.

Specialized Solutions for Every Borrower

Having access to so many lenders is a game-changer, especially for borrowers who don't fit into a neat little box. While conventional loans are common, plenty of buyers need something more specialized.

For example, real estate investors often use Debt Service Coverage Ratio (DSCR) loans, which qualify them based on the property’s rental income instead of their personal W-2s. Good luck finding that at a big-box bank. Mortgage brokers, however, live in this world and know exactly which lenders excel at these niche products. It's a growing market, too, projected to top $1.73 billion with specialized financing like DSCR loans paving the way.

Unlocking a World of Loan Options

One of the single biggest reasons to work with a mortgage broker is the incredible variety of loans they can offer. A direct lender or bank can only sell you their products from their own menu. A broker, on the other hand, gives you a backstage pass to a massive marketplace of lenders and financing solutions.

Think of it this way: a bank is like a shoe store that only sells one brand. If their styles don't fit your foot, you're just out of luck. A mortgage broker is like a personal shopper who takes you to a giant department store with every brand, style, and size imaginable—and then helps you find the perfect pair.

This access turns complex homeownership goals into something real and achievable, going far beyond the standard loans you see advertised on TV. A good broker provides a bridge to both traditional and highly specialized financing, making sure there’s a path forward for almost any borrower.

Traditional and Government-Backed Loans

For most homebuyers, the journey begins with the most common and widely used loan types. A seasoned broker knows these programs inside and out, and their job is to make sure you land the most competitive terms out there.

- Conventional Loans: These are the workhorses of the mortgage world. They're a great fit for borrowers with solid credit and a predictable financial picture. Brokers shop your application across dozens of lenders to find the one with the lowest rate and fees.

- FHA Loans: Backed by the Federal Housing Administration, these are a lifeline for first-time homebuyers or anyone with a smaller down payment. With more flexible credit rules, they open the door to homeownership for many people who might not otherwise qualify.

- Jumbo Loans: When you're buying a home in a high-cost area like Fairfax, Virginia, the loan amount you need might exceed the standard limits. That’s when you need a jumbo loan. Brokers have established relationships with the specific lenders who specialize in these bigger, more complex mortgages.

These loans cover a lot of ground, but a broker's true value often shines brightest when a borrower’s situation calls for a little more creativity.

Specialized Loans for Unique Borrowers

This is where a mortgage broker really earns their stripes and stands apart from a traditional bank. They have access to a whole toolkit of specialized loans designed for people whose financial lives don't fit neatly into a standard box.

A broker's superpower is their ability to solve complex financing puzzles. They can often find a way to get a 'yes' when a single lender has already said 'no.'

Let’s look at some of these powerful, non-traditional loan programs that create opportunities for entrepreneurs, investors, and other unique borrowers.

- DSCR (Debt Service Coverage Ratio) Loans: These are a game-changer for real estate investors. Instead of putting your personal W-2s under a microscope, the lender qualifies the loan based on the investment property's potential cash flow. If the projected rent covers the mortgage payment, you're in a great position to get approved.

- Bank-Statement or P&L Loans: A lifesaver for the self-employed. Business owners often have a hard time proving their income the traditional way. These loans solve that by using 12 or 24 months of business bank statements or a profit & loss statement (P&L) as proof of income, no W-2s required.

- ITIN (Individual Taxpayer Identification Number) Loans: This is for non-U.S. citizens who live, work, and pay taxes here but don’t have a Social Security Number. An ITIN loan makes homeownership possible. Most big banks don't touch these, but a broker knows exactly which lenders do.

- Construction Loans: Building your dream home from the ground up? A broker can connect you with lenders who specialize in construction-to-permanent financing, which streamlines what can otherwise be a very complicated process.

- Refinance Solutions: Whether you want to snag a lower rate, pay off your mortgage faster, or pull cash out of your home’s equity, a broker shops your refinance just like a purchase loan to find the absolute best deal available on the market.

In today's market, this kind of diversity is more critical than ever. As first-time homebuyers grab a record share of the market, many are turning to brokers for access to flexible options like FHA loans to navigate affordability challenges. In fact, younger buyers—those 35 and under—now make up one in every four of these first-time purchases. You can explore more data on homebuyer trends to see how the market is shifting.

When Does it Make Sense to Use a Mortgage Broker?

Figuring out whether to go with a direct lender or a mortgage broker is more than just a search for a low rate. It's about choosing the right guide for one of the biggest financial moves you'll ever make. While a broker can be a huge asset for just about anyone, there are a few specific situations where their expertise goes from "nice to have" to "absolutely essential."

Let's be honest, brokers thrive on complexity. They're the ones who can often turn a hard "no" from a big bank into a confident "yes" from a lender who actually gets your financial picture.

You're a First-Time Homebuyer and Feeling Lost

If this is your first time buying a home, the whole process can feel like you’re trying to read a foreign language. The jargon, the endless paperwork, the deadlines—it's a lot. This is precisely where a great mortgage broker proves their worth.

Think of them as your personal project manager. They don't just process a loan; they educate you, explaining your options in plain English and walking you through every single step. They deal with the lender, coordinate with the real estate agents, and basically act as a buffer, shielding you from the stress. It can make all the difference between a nightmare process and a genuinely exciting milestone.

For a first-time buyer, a broker isn't just a service; they are a strategic partner. Their guidance provides the confidence needed to navigate one of life's biggest financial decisions.

You're Self-Employed and Your Income Isn't "Standard"

Big banks are built for W-2 employees with straightforward, predictable paychecks. If you're an entrepreneur, freelancer, or small business owner, your tax returns probably don't tell the whole story. All those legitimate write-offs can make it tough for a traditional underwriter to see your real earning power.

This is a broker's home turf. They work with lenders who have specific programs for people just like you.

- Bank-Statement Loans: Forget tax returns. These loans use 12 or 24 months of your bank statements to prove your income. It's a game-changer.

- P&L (Profit & Loss) Loans: Some lenders will even qualify you based on a P&L statement prepared by your CPA.

Instead of hitting a brick wall at a bank that doesn’t understand your business, a broker connects you to a lender who not only gets it but actively looks for self-employed borrowers.

Your Credit Has a Few Blemishes

A credit score that isn't perfect can feel like a deal-breaker, especially if you've already talked to a bank with strict minimums. A few late payments from a couple of years ago or a high balance on a credit card can trigger an automatic rejection. But here's the thing: not all lenders see risk the same way.

A mortgage broker knows the lending landscape inside and out. While one lender might have a hard cutoff at a 680 credit score, another might be perfectly fine with a 620 for an FHA loan. It's their job to shop your scenario—not just your application—to the right lenders who have more flexible guidelines. They find you a path forward when you thought all the doors were closed.

You're a Real Estate Investor Looking to Grow

Building a real estate portfolio demands financing that is fast, flexible, and creative. The average retail bank just isn't set up for that. Investors need products designed for rental properties, not primary homes, and that's where a broker becomes a critical part of your team.

They have access to the investor's secret weapon: the DSCR (Debt Service Coverage Ratio) loan. This is a powerful tool that qualifies you based on the property's income potential, not your personal salary. As long as the rent covers the mortgage payment (and then some), your personal debt-to-income ratio is much less of a factor. This is how savvy investors scale their portfolios without getting tapped out, and it's a specialized product brokers bring to the table.

Your Step-by-Step Journey with a Mortgage Broker

Think of a mortgage broker as your personal guide through the home loan maze. Instead of you having to cold-call a dozen banks, fill out endless applications, and try to make sense of financial jargon, the broker does the heavy lifting. They manage the entire project, from your first questions to the day you get your keys.

This isn't just about convenience; it's a strategic process designed to find the right loan for you, save you a ton of time, and cut down on the stress that often comes with buying a home. The whole thing usually follows a few clear stages.

The Kick-Off: Consultation and Pre-Approval

It all starts with a conversation. This is your chance to lay it all out: your financial picture, what you're looking for in a home, and any unique circumstances you might have (like being self-employed or having a recent job change). A good broker just listens, asks smart questions, and gets the full story.

With that information, they’ll help you get pre-approved. This is a game-changer. It involves a preliminary review of your credit and finances to see what you can realistically afford to borrow. When you can show a seller a pre-approval letter, you’re not just a window shopper anymore—you’re a serious buyer.

Next Up: Getting Your Documents in Order

Once you're ready to make a move, it's time to gather your paperwork. For many people, this is the most tedious part of the process. But your broker will give you a simple, clear checklist so you know exactly what you need.

To keep things moving smoothly, it's smart to get a head start. You can review an essential mortgage document checklist to get familiar with what's required. In most cases, you'll need:

- Proof of Income: Your last few pay stubs, W-2 forms for the past two years, and your federal tax returns.

- Asset Verification: Recent statements from your bank and investment accounts, showing you have the funds for the down payment and closing costs.

- Identification: A valid driver's license or another government-issued photo ID.

- Credit History: Your broker will pull your official credit report, but it’s always a good idea to know your score beforehand.

From Application to the Closing Table

This is where your broker really shines. With your documents in hand, they handle the rest. They'll complete and submit your loan application to the lenders in their network that offer programs matching your specific needs. They know which lenders are friendly to certain borrower types and who is likely to give you the best deal.

Your Broker's NMLS License: The Gold Standard

Always check that your broker has a license number from the Nationwide Multistate Licensing System & Registry (NMLS). This isn't just a piece of paper; it's proof that they’ve met rigorous federal and state education, testing, and background check requirements. It’s your assurance that you're in capable, professional hands.

When the lenders respond, your broker will present you with their offers, laid out in a simple side-by-side comparison. They'll explain the interest rates, fees, and total closing costs so you can see the true cost of each loan and make a smart choice.

After you pick the best offer, the loan moves into the underwriting stage. This is where the lender's team verifies all your information one last time. We've got a great guide that explains exactly what is involved in the mortgage underwriting process.

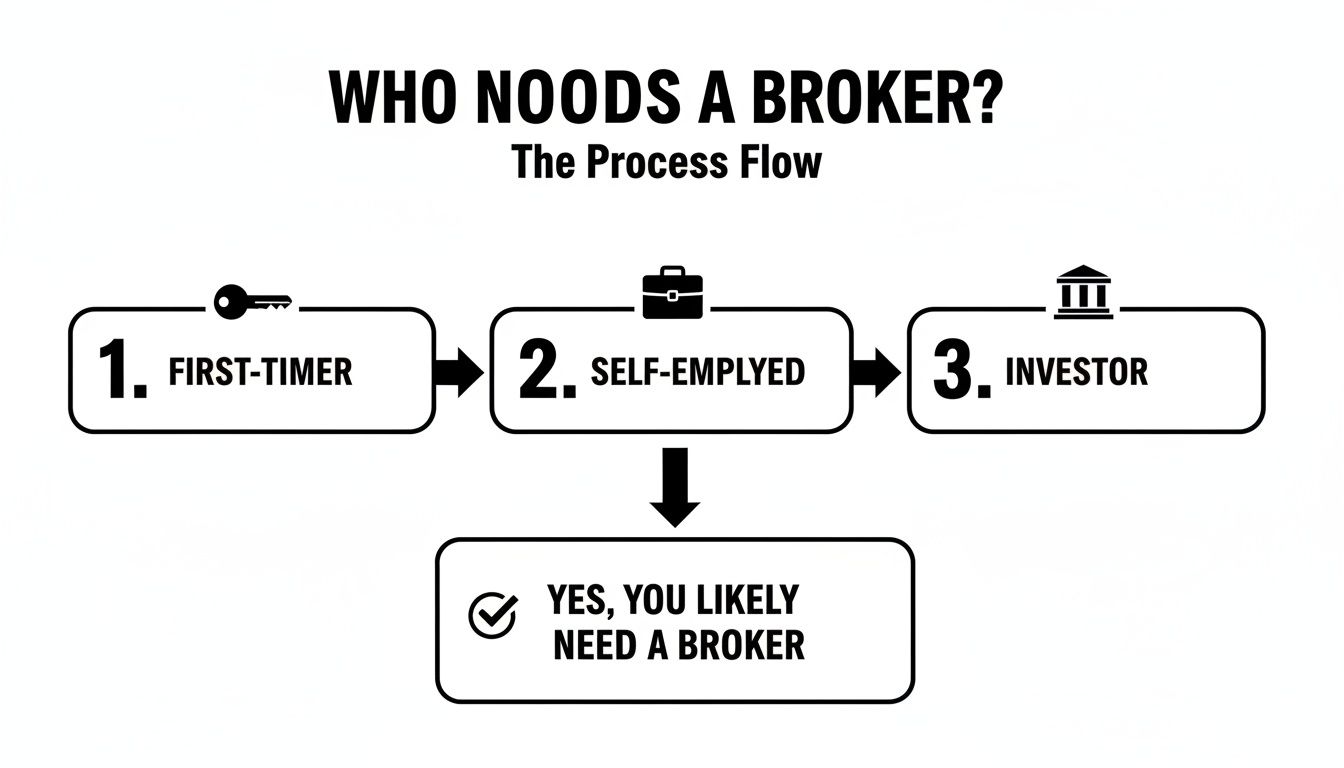

The infographic below shows just a few of the borrower types who get the most out of working with a broker.

As you can see, a broker's expertise is a huge asset whether you're new to homebuying, have a tricky income situation, or are growing your real estate investment portfolio.

Finally, your broker acts as the central coordinator, working with the lender, the title company, and the real estate agents to get your closing scheduled. They’ll be right there with you to tackle any last-minute questions, making sure your homebuying journey ends on a high note.

Ready to Find the Right Home Loan?

So, you've seen what a mortgage broker does and how we can open up a world of different loan options. But knowing what a broker is and actually partnering with one are two different things. This is where we move from theory to action, and find a real path to your new home.

Think of a good mortgage broker less as a middleman and more as your personal guide through the home financing maze. We're here to slice through the dense jargon and confusing paperwork, turning your homeownership dreams into a clear, step-by-step plan. The right partnership doesn't just save you time and stress—it often saves you a significant amount of money by securing better rates and lower fees.

Your Local Fairfax, Virginia Mortgage Experts

For anyone looking to buy a home here in the Fairfax, Virginia area, that's exactly what we do at Mortgage Seven. We bring our deep understanding of the local market and connect you with a huge network of lenders, making sure you get a look at the very best deals out there. We build everything we do on a simple foundation: clear communication and total transparency.

We truly believe that the more you know, the more confident you'll be. You can dive deeper into the key benefits of working with a mortgage broker to see just how much of a difference this approach makes.

Your home is one of the biggest, most important investments you'll ever make. Working with a licensed professional (NMLS #2124799) is the best way to make sure your financial interests are protected and your loan is set up for your long-term success.

Our goal is simple: make your journey to getting a mortgage as smooth and straightforward as possible. We do the heavy lifting—the rate shopping, the paperwork wrangling, the endless coordination—so you can focus on the exciting part: finding a house you love.

Curious to see what your options look like? The first step is just a conversation. Let's schedule a no-obligation consultation to talk about your goals. We'll explore your unique situation and map out a plan to help you buy your home with confidence.

Your Top Questions About Mortgage Brokers, Answered

You've got the basics down, but it's natural to still have some practical questions. Buying a home is a massive financial step, so digging into the details isn't just smart—it's essential. Let's walk through the questions I hear most often from borrowers trying to figure out if a broker is the right fit for them.

Getting these things straight is the key to moving forward with confidence.

How Does a Mortgage Broker Get Paid?

This is usually the first question on everyone's mind, and thankfully, the answer is pretty straightforward. By law, how a broker gets paid has to be crystal clear to you, and it generally happens in one of two ways.

- Lender-Paid Compensation: This is the most common setup by far. The wholesale lender you end up choosing pays your broker a fee for doing the legwork of finding and preparing a qualified borrower (that's you!). This fee is already factored into the wholesale interest rate the lender offers, so it's not a separate line item you have to pay at closing.

- Borrower-Paid Compensation: Less common, but sometimes it makes sense for you to pay the broker directly. This could be a flat fee or a small percentage of the loan, which is always disclosed upfront and included in your closing costs. A broker might go this route to secure a rock-bottom interest rate from a lender that doesn't offer the lender-paid option, potentially saving you a lot more money over the life of the loan.

The bottom line is simple: you’ll see exactly how your broker is being paid on your official Loan Estimate. No secrets, no hidden charges.

Is It Always Cheaper to Use a Broker?

It's not a 100% guarantee every single time, but using a mortgage broker very often leads to a better deal. Why? It all comes down to wholesale vs. retail.

Brokers have direct access to wholesale lenders who don't have the overhead of retail branches and big advertising budgets. These lenders offer lower wholesale rates that aren't available to the general public. Think of it like a Costco for mortgages—brokers bring them loans in bulk, so they get preferred pricing that an individual just can't access on their own.

Even after you account for the broker’s compensation, the all-in cost of your loan (the rate plus fees) is frequently lower than what you'd find walking into your local bank.

A broker makes dozens of lenders compete for your business with just one application. That competition is what forces rates and fees down, putting money back in your pocket.

How Do I Choose the Right Mortgage Broker?

This is a big one. The right partner can make all the difference, turning a stressful process into a smooth one. Here’s what to look for when you're trying to find a great broker.

- Check Their License: First thing's first. Every broker and loan officer must have a Nationwide Multistate Licensing System (NMLS) number. It's non-negotiable and proves they're licensed to operate. You can look them up easily online.

- Read Real, Recent Reviews: Don't just look at their website. Check third-party sites to see what actual clients are saying about their communication skills, their knowledge, and how they handled bumps in the road.

- Ask About Their Lenders: A great broker won't just have a lot of lender connections; they'll have the right connections. Ask if they work with lenders who specialize in your specific scenario, whether that's a DSCR loan for an investment property or a bank-statement loan because you're self-employed.

- Gauge the First Conversation: Are they asking you thoughtful questions about your goals, or are they just quoting rates? A true professional listens first. They need to understand your complete financial picture and what you want to achieve before they even think about recommending a loan.

A little due diligence upfront will help you find an advocate who will be in your corner from day one.

Ready to see how working with a dedicated mortgage broker can make your home financing journey clearer and less stressful? The team at Mortgage Seven LLC is here to offer the expert guidance and personalized loan options you deserve. Let's talk about your goals and map out a clear path to get you there.

Schedule Your Free Consultation with Mortgage Seven LLC Today