Navigating the home buying process can feel like a rollercoaster, especially when it comes to interest rates. A mortgage rate lock is your secret weapon, designed to bring some much-needed calm to the chaos. Think of it as a promise from your lender, like us here at Mortgage Seven LLC, to guarantee you a specific interest rate for a set amount of time while your loan gets finalized.

This agreement, which usually lasts for 30 to 60 days, is all about giving you peace of mind and, more importantly, budget certainty.

Understanding Your Mortgage Rate Lock

Picture this: you’ve found the perfect home, run the numbers, and everything fits. But then, overnight, the market shifts, and your estimated monthly payment suddenly shoots up. It's a stressful scenario that a rate lock is designed to prevent. It effectively takes market volatility out of the equation for your loan.

Before getting too deep into the mechanics of locking, it’s always a good idea to understand your mortgage from a big-picture perspective. Having that foundational knowledge makes every other decision, including when to lock, much more straightforward.

Why a Rate Lock Matters in Volatile Markets

A rate lock is essentially insurance for your buying power. Let's say a first-time homebuyer in Fairfax, Virginia, is thrilled about a property but anxious watching the daily news about mortgage rates. By locking their rate, they get a firm commitment from their lender to hold that interest rate steady while the loan is processed, protecting them from any sudden spikes.

The real-world impact is huge. In a recent year, the average U.S. 30-year fixed mortgage rate shot up from 3.11% to a peak of 7.08%. Homebuyers who had the foresight to lock their rates early saved themselves potentially thousands of dollars over the life of their loans.

A mortgage rate lock isn't just a technical step; it's a strategic move that secures your budget. It transforms an unpredictable variable—the interest rate—into a known constant, allowing you to plan your finances with confidence from application to closing.

Ultimately, this agreement ensures the rate you were quoted is the rate you get at the closing table, as long as you close within the lock period. In a dynamic market like Northern Virginia, that kind of stability is priceless. It means no last-minute surprises or budget-busting payment hikes.

How the Mortgage Rate Lock Process Works

So, you've found the perfect house and you're ready to make your interest rate official. Locking it in is a huge milestone, and thankfully, it's a pretty straightforward process. Think of it as taking control of a major variable—your interest rate—so you can focus on everything else.

The starting pistol for a rate lock usually fires once you have a specific property under contract. Why? Because lenders need a physical address to finalize your rate, as things like property type and location can play a small role. Once you have that signed purchase agreement in hand, you can officially ask your lender to lock it in.

Your Official Lock Agreement

Once you give the green light, your lender will provide a formal Loan Estimate. This is the single most important document in the process. It's a standardized form that lays out all the terms of your loan in black and white, including the specifics of your rate lock.

This document is your proof. It turns a conversation into a commitment. Inside, you'll find the details that matter most:

- The Locked Interest Rate: The exact interest rate your lender is guaranteeing you.

- The Lock-in Period: This is the expiration date for your lock, usually 30, 45, or 60 days.

- Associated Points or Fees: Any costs tied to the lock itself or any discount points you've chosen to pay will be clearly listed here.

A verbal promise is nice, but the Loan Estimate makes it real. This document is your official contract for the rate lock, clearly stating your interest rate, how long it's good for, and any costs involved. It's your peace of mind on paper.

Choosing the right lock period is a strategic decision. If you're expecting a smooth, quick closing, a 30-day lock might be all you need. But if there are any hints of complexity—like a tricky appraisal or a seller who needs more time—a 60-day lock provides a much-needed safety net.

We'll help you figure out the best timeline for your specific loan, factoring in everything from appraisal turn-times to the time needed to complete the underwriting. You can learn more about the mortgage underwriting process in our guide to get a better feel for how long things might take.

Now, let's break down the key parts of that agreement you'll be signing.

Key Components of Your Rate Lock Agreement

This table breaks down the essential elements you'll find in a typical mortgage rate lock agreement, helping you understand exactly what you are agreeing to.

| Component | What It Means | What to Look For |

|---|---|---|

| Loan Program | The type of mortgage (e.g., 30-Year Fixed, FHA, VA). | Confirm it matches the loan you discussed with your loan officer. |

| Interest Rate | The specific rate you are locking in for the term of the loan. | Double-check that this number is exactly what you were quoted. |

| Lock-in Date | The date your rate lock officially begins. | This is "Day 1" of your lock period. |

| Expiration Date | The last day your locked rate is valid. You must close by this date. | Ensure this date provides enough buffer for your estimated closing date. |

| Lock Period | The total number of days your rate is protected (e.g., 30, 45, 60 days). | Make sure it's a realistic timeframe for your specific situation. |

| Discount Points | Any fees paid upfront to "buy down" your interest rate. | This should show the cost and confirm the rate reduction you're receiving. |

Understanding these components means there are no surprises. It transforms your estimated monthly payment into a solid number you can plan your budget around, letting you move forward with confidence.

Lock Your Rate or Let It Float? Making the Call

So, you've found a house and you're moving forward with your mortgage. Now comes one of the most nerve-wracking decisions in the entire process: do you lock in your interest rate, or do you let it “float” with the market?

Think of it as certainty versus opportunity. There’s no single right answer, just the one that’s right for you.

Locking your rate is like taking the sure thing. You grab the interest rate available today and hold onto it all the way to closing. This means your monthly payment is set in stone, which makes budgeting a whole lot easier. For anyone who likes predictability (and who doesn't?), locking provides incredible peace of mind.

Floating your rate, on the other hand, is a bit of a gamble. You’re essentially betting that rates will drop between now and when you need to finalize the loan. If you're right, you could snag a lower payment and save a bundle over the years. But if you’re wrong, rates could creep up, leaving you with a higher payment than you were first quoted.

When to Lock vs. When to Float

The right move really boils down to two things: your personal comfort with risk and what the economy is doing.

If you’re the type who loses sleep over financial unknowns, locking your rate early is probably the way to go. It just takes the stress out of the equation. This is especially true when rates are on the rise—waiting could literally cost you money every single day.

But if you have a bit more appetite for risk and the market chatter suggests rates might dip, floating could pay off. This strategy can be a good fit for experienced buyers or those with some wiggle room in their budget who are willing to play the odds for a better deal.

Your decision to lock or float is a personal one that balances financial goals with emotional comfort. There's no single right answer, only the best answer for your specific situation and the current market conditions.

The key is to be honest with yourself about what you value more: the security of a guaranteed payment or the potential for a lower one. It's also worth thinking ahead; understanding the best time to refinance your mortgage might influence how you approach this initial decision.

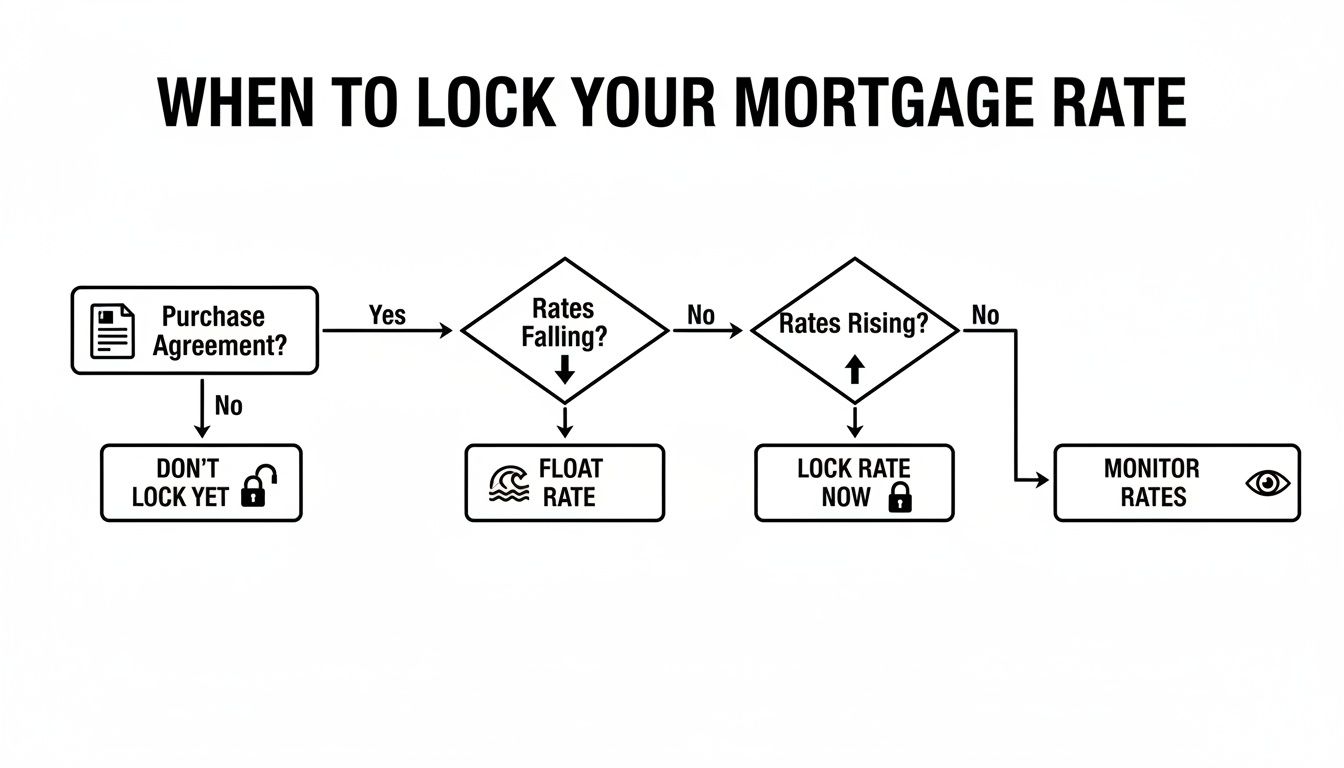

This flowchart gives you a simple framework for thinking through the lock vs. float decision based on market trends and where you are in the homebuying journey.

As you can see, once you have a signed purchase agreement and rates are climbing, the smart move is almost always to lock it in and protect your budget.

Real-World Scenarios: Who Does What?

Let's break this down with a couple of real-world examples.

The Budget-Conscious First-Time Buyer: Imagine you're buying your first home. Every penny counts, and surprises are not welcome. In this case, locking your rate the moment you have a signed contract is a no-brainer. It eliminates all the guesswork and ensures the affordable payment you planned for is the one you actually get.

The Seasoned Real Estate Investor: Now, picture an investor who’s done this a few times. They might be more comfortable floating the rate, especially on a property they don't plan to hold for 30 years. They tend to follow market news closely and might risk a small rate hike for the chance at a significant drop that could boost their return on investment.

Ultimately, deciding to lock or float is a strategic move. It requires a clear-eyed look at your finances and the market's direction. Here at Mortgage Seven LLC, our job is to walk you through these factors so you can make a confident choice that perfectly matches your goals.

Exploring Your Rate Lock Options and Flexibility

A standard rate lock gives you certainty, which is a huge relief in the home-buying process. But what if you could have that security and still have a chance to benefit if rates drop? The good news is, you're not stuck with a simple lock-it-and-forget-it deal. There are a few specialized options that can add some valuable flexibility.

Think of these as powerful tools in your home-buying toolkit. Getting to know them helps you ask the right questions and ultimately land a better deal on your mortgage. They give you the power to react to a changing market, even after you've already secured your rate.

The Float-Down Option: Your Safety Net

By far the most common flexible feature is the float-down option. I like to describe it as an upgrade to your standard rate lock. It does the main job of protecting you if rates climb, but it also leaves the door open to snag a lower rate if the market happens to dip before you close.

Here's the gist of how it works: you lock in your rate just like normal. But if market rates drop by a certain amount (your lender will have a set threshold, often around 0.25%), you can trigger your one-time option to "float down" to that new, better rate. That single adjustment can literally save you thousands of dollars over the life of your loan.

The float-down option is your best defense against "rate lock regret." It takes away that nagging fear of locking in your rate, only to watch the market take a nosedive the very next day.

Now, this feature isn't usually free. It typically comes with an upfront fee, either a flat cost or a small percentage of your loan. The trick is to weigh that cost against the potential reward. For instance, if rates were to fall—say, a 0.37% drop from one quarter to the next—a standard lock leaves you on the sidelines. But since about 25% of lenders offer paid float-downs (often costing between $500-$1,500), you could pay the fee and capture those savings. You can find more details in these mortgage rate lock findings on Bankrate.com.

When You Need a Rate Lock Extension

Another critical option to know about is the rate lock extension. Let's be honest, life happens, and closings don't always go according to plan. All sorts of things can cause delays:

- Appraisal Problems: The appraisal might take longer than expected or come in with a value that needs to be addressed.

- Documentation Hiccups: Underwriting might need one more document that takes a few days to track down.

- Seller Delays: Sometimes the seller needs a bit more time to move out or fix an inspection issue.

If your lock is nearing its expiration date but your closing gets pushed back, you can ask for an extension. Most lenders will grant one for a fee, which might be a daily charge or a flat cost for a set period, like 15 or 30 days. While nobody loves paying extra fees, it's often a small price to pay to hold onto a great rate you locked in, especially if current rates have shot up. Staying in close contact with your loan officer here at Mortgage Seven LLC is the key to getting ahead of these issues and understanding the costs involved.

How Rate Lock Strategies Change for Different Loans

A rate lock strategy isn't a one-size-fits-all deal. Far from it. The right move really depends on the type of loan you’re getting, because each one has its own unique rhythm and timeline.

Think about it this way: a standard conventional loan for someone with a W-2 job might sail through to closing in 30 days. A shorter lock period works just fine there. But if you're self-employed and using a bank statement loan, the lender needs to do a much deeper dive into your finances. In that scenario, grabbing a longer 60- or 90-day lock gives you a necessary safety net, so you’re not scrambling to pay for an extension at the last minute.

The more specialized the financing, the more you need to think ahead.

Specialized Loans Need Specialized Strategies

When your financial picture or the loan itself is a bit more complex, your rate lock strategy has to be smarter. A "wait and see" approach can be a recipe for disaster. Let's walk through a few common situations where the standard playbook just won't cut it.

For real estate investors using DSCR loans or ITIN borrowers relying on bank statements, a rate lock is like armor against market swings. In a market where 30-year rates are hovering around 6.95%, we've seen investors who secured 60-day locks on $750,000 jumbo loans save an average of 0.5% compared to those who decided to float. That half-a-percent translates into massive interest savings over the life of the loan.

Here are a few specific examples of when to be extra careful:

- Jumbo Loans: We're talking about huge loan amounts here. Even a tiny rate hike can add hundreds of dollars to your monthly payment. Locking in your rate as soon as you can is almost always the wisest path to protect your budget.

- ITIN Borrower Loans: This process often involves extra verification steps, which can easily stretch out the closing timeline. A longer lock gives you the breathing room to get everything done without the stress of an expiring rate.

- Adjustable-Rate Mortgages (ARMs): The game is a little different with an ARM. You’re only locking the rate for the initial fixed period, not the whole loan term. If you have a strong feeling that rates might dip right before you close, you might wait a bit longer to lock. You can check out our guide on adjustable-rate mortgages to learn more about how they work.

A savvy rate lock strategy is proactive, not reactive. It anticipates the specific timeline of your loan program—whether it's a bank-statement, DSCR, or jumbo loan—and builds in the necessary time to close without costly extensions or surprises.

Ultimately, making the right call comes down to understanding the nuances of your specific loan. This is where getting expert guidance from a brokerage like Mortgage Seven LLC really pays off. We help you look at the whole picture—from your loan program to your personal comfort with risk—to build a rate lock strategy that protects your wallet all the way to the closing table.

Answering Your Top Rate Lock Questions

Even when you have a good handle on the basics, a few specific questions always seem to pop up as you get closer to locking in your rate. Running through these "what-if" scenarios ahead of time can clear up any confusion and give you the confidence to make the right move.

Let's tackle some of the most common questions we hear from our clients every day.

What Happens If My Loan Doesn’t Close Before My Lock Expires?

This is a big one, and it's a totally valid concern. Sometimes, unexpected delays happen. If your closing date gets pushed past your lock’s expiration, you’ll most likely need to get a rate lock extension.

Most lenders, including our partners here at Mortgage Seven LLC, can grant an extension, but it usually comes with a fee. The cost might be a flat amount or a small percentage of your loan. The key is to stay in close contact with your loan officer. If a delay seems possible, you can get ahead of it and understand the costs involved long before the deadline hits.

Can I Switch Lenders After I Lock My Rate?

In short, no. A rate lock is an agreement you make with one specific lender, and it’s not transferable. If you decide to jump ship to a different lender after you've already locked, you'll have to start the rate lock process from scratch with the new company.

This means you’ll be getting whatever interest rates are on the table that day, which could easily be higher than the rate you had locked in.

Think of a rate lock like a reservation at your favorite restaurant. It guarantees you a table there, at that specific time, but you can't just take that reservation and use it at the place across the street.

Does a Rate Lock Guarantee Loan Approval?

This is a common misconception. A rate lock does not, in any way, guarantee your loan will be approved. It has one very important job: to secure your interest rate while your application moves through the final underwriting stages.

Your loan still has to clear the full underwriting process, where your credit, income, assets, and the property itself are all carefully reviewed. The lock is simply a shield, protecting you from rate hikes while all that necessary work is being done.

How Soon Can I Lock My Mortgage Rate?

You can typically lock your rate as soon as you have a property under a signed purchase contract. Lenders need a specific address to formalize the lock because the property's location and type can actually affect the final rate.

While some lenders have "lock and shop" programs that let you lock a rate before finding a home, they aren't as common and often have their own set of rules and fees. For the vast majority of homebuyers, the lock happens right after your offer on a house is accepted.

Navigating these details is so much easier when you have an expert in your corner. The team at Mortgage Seven LLC is here to answer every one of your questions and help you build the perfect rate lock strategy for your situation. Start your journey to homeownership with us today.