A cash-out refinance is a way to tap into the value you've built up in your home. It works by replacing your current mortgage with a new, larger one, and you get to pocket the difference in cash. It's one of the most common ways homeowners turn their property's equity into usable money for other goals.

Think of it this way: the equity in your home is like a savings account that grows every time you make a mortgage payment or when your property value goes up. A cash-out refi is like making a withdrawal from that account. You're not adding a second loan on top of your existing one; you're simply resetting your primary mortgage to pull some of that value out.

This is a totally different ballgame than a personal loan or a credit card. Because the new loan is secured by your house, you can often lock in a much lower interest rate, which is why it's such an attractive option for homeowners looking to fund big projects or consolidate debt.

To give you a quick overview, here’s a simple table that breaks down the key ideas.

Cash Out Refinance at a Glance

| Concept | What It Means for You |

|---|---|

| New, Larger Loan | Your old mortgage is gone, replaced by a new one with a higher balance. |

| Old Mortgage Payoff | The first thing the new loan does is pay off your original mortgage in full. |

| Equity Conversion | You turn a portion of your home's value into a lump sum of tax-free cash. |

| Closing Costs | Like any mortgage, there are fees involved, which are often rolled into the new loan. |

This table shows how the pieces fit together to unlock your home's equity.

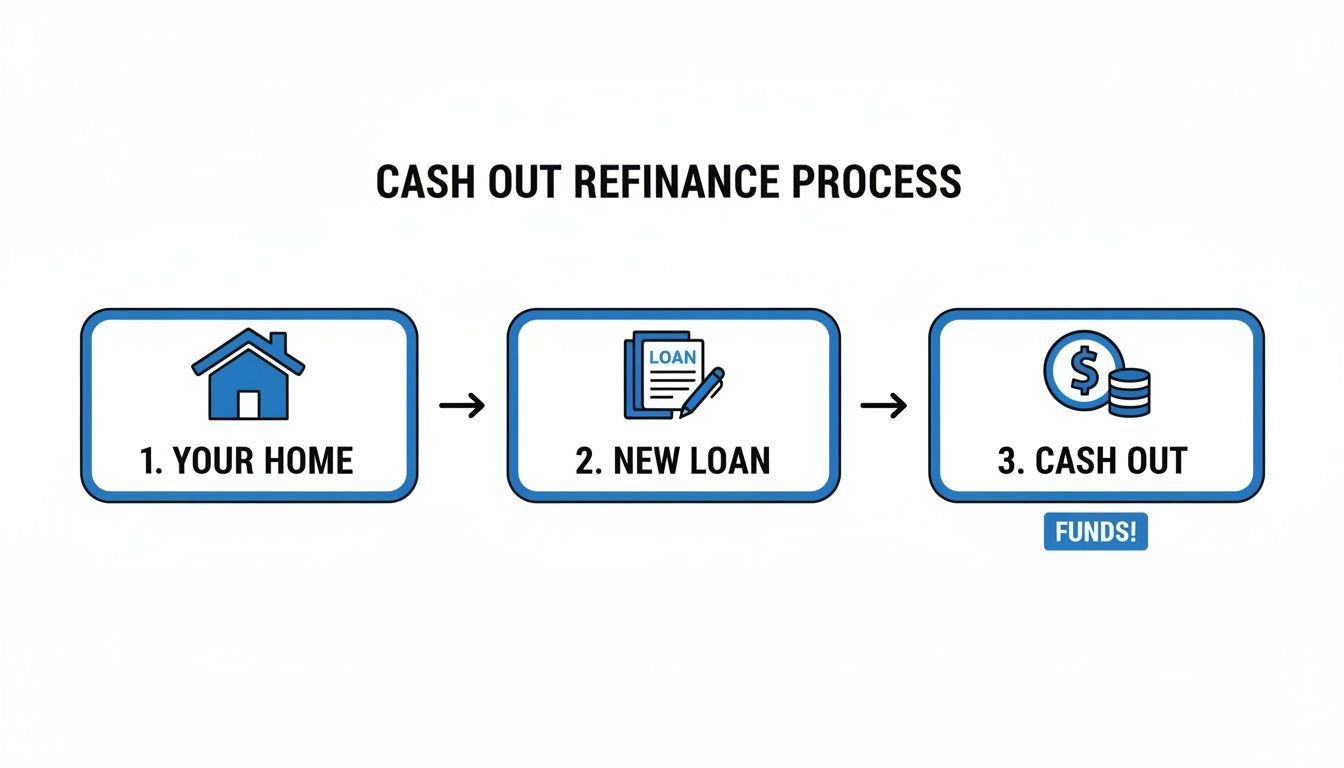

How Does It Turn Equity Into Cash?

So, how does this actually work? The process itself is pretty straightforward. You get a new mortgage for more than you currently owe. That new loan pays off your existing mortgage balance first, and whatever is left over (minus closing costs) is paid directly to you in a lump sum.

Here’s a simple breakdown:

- You get a new, larger loan to replace your old one.

- Your existing mortgage is paid off completely with funds from the new loan.

- You receive the remaining cash to use however you want.

In short, a cash-out refinance lets you borrow against your home's value by taking out a new mortgage that's larger than your current one. You pay off the old loan and keep the extra cash, turning your home equity into liquid funds.

A Practical Example in Fairfax, Virginia

Let's put some real numbers to this. Imagine you own a home in Fairfax, Virginia, that’s now worth $400,000. You've been paying down your mortgage for a while and now only owe $220,000. That leaves you with a solid $180,000 in home equity.

You decide you want to do a major kitchen remodel and need cash to fund it. You apply for a cash-out refinance and get approved for a new loan of $300,000.

From that $300,000, the first $220,000 goes directly to pay off your old mortgage. The remaining $80,000 is the cash you get to take home (less any closing costs).

Most lenders, as a rule of thumb, will want you to keep at least 20% equity in your home after the transaction. It's a way for them to manage their risk. You can learn more about the different types of refinancing in general on our website. For a closer look at the market, you can find more insights about current refi mortgage rates at Fortune.com. Now that you have the basics down, we can dive into the step-by-step process.

The Cash-Out Refinance Process Step by Step

Knowing the definition of a cash-out refinance is a good start, but what does the process actually look like from beginning to end? It can feel a little intimidating, but when you break it down, it’s really just a series of clear, predictable stages.

Think of it as a roadmap. Each step gets you closer to unlocking that home equity and putting it to work. Let’s walk through what you can expect, from the initial planning all the way to closing day.

This diagram shows the basic flow: your home equity is converted into a new, larger loan, which then provides you with a lump sum of cash.

At its heart, you're just transforming a non-liquid asset—your house—into cash you can use today.

1. Calculate Your Equity and Set Your Goals

First things first, you need to get a handle on your numbers and figure out exactly what you want to accomplish. Start with a ballpark estimate of your home's current market value and subtract what you still owe on your mortgage. That number is your equity.

Most lenders will want you to keep at least 20% equity in your home after the refinance, so this back-of-the-napkin math will give you a realistic idea of how much you can actually pull out. At the same time, get specific about your "why." Is this for a kitchen remodel, consolidating high-interest credit cards, or covering college tuition? A clear goal helps you stay focused.

2. Shop for Lenders and Compare Offers

You wouldn’t buy the first car you test drive, and you shouldn’t take the first loan offer you get. This is your chance to compare interest rates, closing costs, and terms from different places—big banks, local credit unions, and mortgage brokers like us at Mortgage Seven LLC.

Make sure you get an official Loan Estimate from each one. This standardized document makes it much easier to compare apples to apples. Look past the flashy interest rate and focus on the Annual Percentage Rate (APR), which rolls in most of the fees and gives you a truer sense of the loan's cost. A good loan officer will walk you through every line item without making you feel rushed.

3. Submit Your Formal Application

Once you’ve picked a lender, it's time to get down to business. The formal application is where you provide all the documents needed to prove you can handle the new, larger loan.

Get ready to gather some paperwork:

- Recent pay stubs and W-2s to show your income.

- Bank statements to confirm you have assets and savings.

- The last two years of your tax returns for a full financial overview.

- Statements for other debts like car loans, student loans, or credit cards.

Think of this stage as building your case. The lender needs to verify everything, so having your documents organized and ready to go will make the whole process smoother and faster.

4. The Crucial Home Appraisal

Since your home is the collateral, your lender will order a professional appraisal. An independent, licensed appraiser will visit your property to assess its condition, size, and features. They’ll also analyze recent sales of similar homes in your neighborhood to determine its current fair market value.

This is a make-or-break moment. The amount of cash you can take out is directly tied to the appraiser's valuation. If the value comes in lower than you hoped, it could limit how much you’re able to borrow.

5. Navigate Underwriting and Get Approved

With the appraisal complete, your entire loan package lands on an underwriter's desk. The underwriter is the final decision-maker. They'll meticulously comb through your application, credit report, income documents, and the appraisal to make sure you tick all the lender's boxes.

It's common for an underwriter to come back with a few questions or a request for one more document. Don't panic! Just respond as quickly as you can to keep things moving. If everything aligns, you’ll get the green light: a "clear to close." Your loan is officially approved.

6. Close the Loan and Get Your Cash

You’re at the finish line. At closing, you'll sit down to sign a pile of legal documents. The most important one is the Closing Disclosure, which spells out the final, exact details of your loan—rate, monthly payment, and total closing costs.

After you sign everything, a mandatory three-day "right of rescission" period begins. This is a cooling-off period where you can legally change your mind. Once that passes, your new loan funds, paying off your old mortgage. The "cash-out" portion is then sent to you, usually as a wire transfer or check. Now, that money is yours to use.

What Lenders Look For When You Apply

Before any lender hands over a check, they need to feel confident you can handle the new, larger mortgage. It's basically a financial health checkup. They’ll dig into a few key areas to figure out if you're a good candidate, what interest rate you qualify for, and how much cash you can actually pull out.

Knowing what they’re looking for ahead of time is a huge advantage. It gives you a chance to get your financial house in order, gather your paperwork, and go into the process with your eyes wide open.

The Equity in Your Home

First things first: you can't take cash out if you don't have enough equity built up. Equity is simply the difference between what your home is worth today and what you still owe on it. Think of it as the portion of your home you own free and clear—that's the piggy bank you'll be tapping.

The industry has a pretty firm rule of thumb here: the 80% Combined Loan-to-Value (CLTV) limit. This means that most lenders won't let your new, total loan amount exceed 80% of your home's appraised value. This leaves a 20% equity cushion in the property, which protects both you and the lender if home values dip. You can see this standard explained in more detail in guides about what a cash-out refinance is at NerdWallet.com.

Let’s run the numbers: Imagine your home gets appraised for $500,000. The absolute maximum your new loan could be is $400,000 (that's 80% of $500,000). If your current mortgage balance is $250,000, you could potentially walk away with up to $150,000 in cash, minus closing costs.

Your Credit Score and Payment History

In the mortgage world, your credit score speaks volumes. It’s a quick-and-dirty summary of how you’ve managed debt in the past. A higher score tells lenders you’re a reliable borrower, and they’ll reward that lower risk with a better interest rate.

While the exact number can vary by lender, you'll generally need a credit score of at least 620 to qualify for a conventional cash-out refinance. To really lock in the most competitive rates, though, you’ll want to be in the 700s. A strong score can easily save you tens of thousands in interest over the life of the loan. If you're curious about the specifics, check out our guide on how your credit score affects your mortgage options.

Your Debt-to-Income Ratio

Your credit history is only half the story. Lenders also need to know that you aren't stretched too thin financially. They measure this with your Debt-to-Income (DTI) ratio.

DTI is a simple percentage that shows how much of your gross monthly income goes toward paying debts—things like your new proposed mortgage payment, car loans, student loans, and credit card payments.

Most lenders draw the line at a DTI of 43% or lower. Some programs might be a little more flexible, but only if you have other strengths, like a fantastic credit score or a lot of cash in savings. A low DTI proves you have enough breathing room in your budget to comfortably handle all your obligations.

Finally, you’ll need to show proof of stable income. Lenders want to see that you have a reliable paycheck to cover the mortgage payments for the long haul. Be prepared to provide at least two years' worth of documents like pay stubs, W-2s, and tax returns to verify your employment and income.

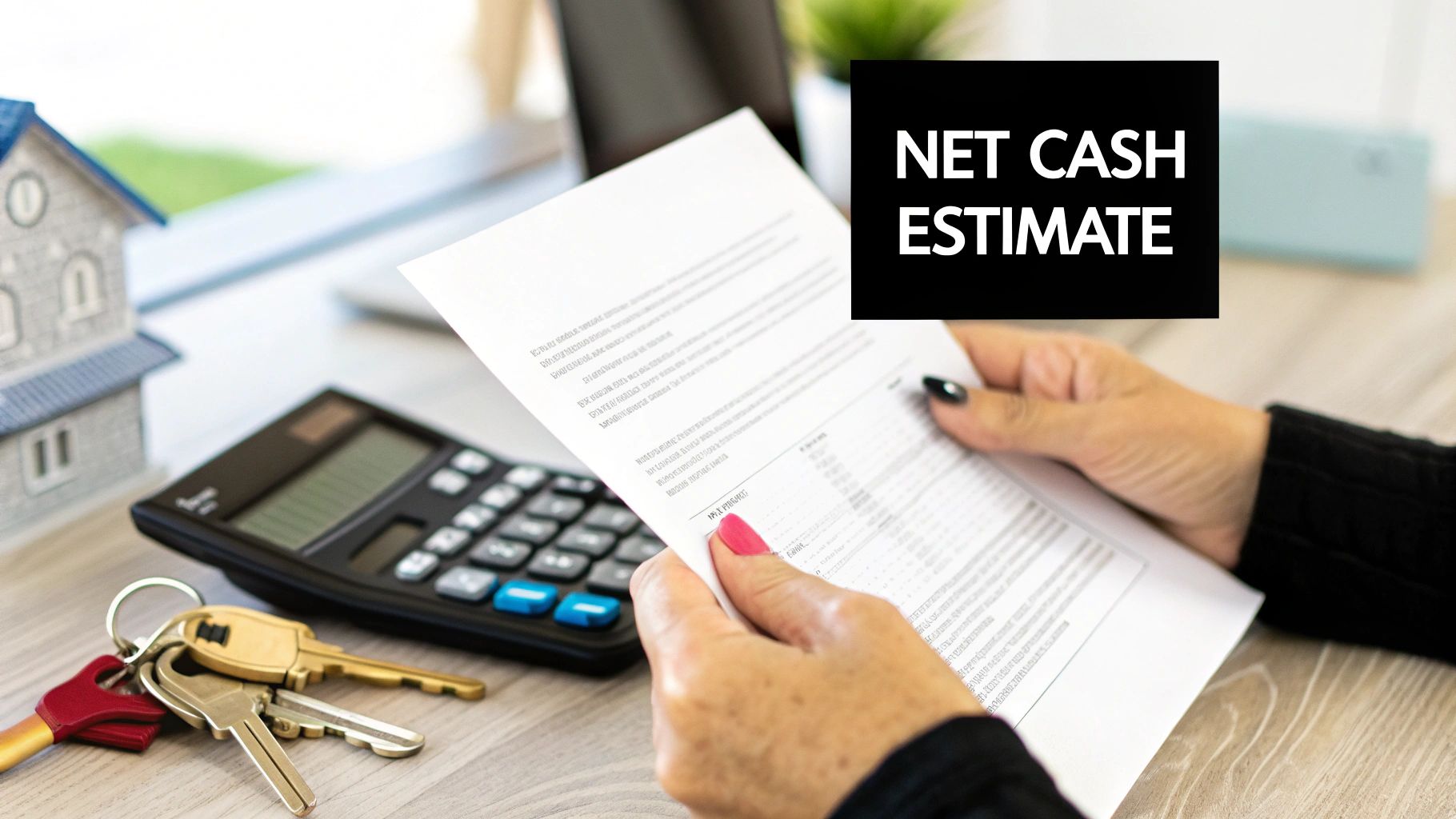

Calculating the Real Costs and Your Net Cash

The big-picture idea of a cash-out refinance is straightforward. But let's be honest, the only question that really matters is: how much money will I actually get? The initial number can sound great, but it’s the final, take-home amount after all the fees that counts.

Just like when you first bought your house, a refinance comes with closing costs. These are the standard fees for all the work that goes into creating and finalizing your new mortgage, and they're taken out before you get your check.

A Transparent Look at Closing Costs

Typically, you can expect closing costs for a cash-out refinance to be between 2% to 5% of the new loan amount. It’s a pretty wide range, and these fees are a major factor in figuring out your final cash disbursement.

You’ll see some familiar items on the list:

- Origination Fee: This is the lender’s fee for processing and underwriting the loan.

- Appraisal Fee: You’ll need a new appraisal to confirm your home's current market value, and this pays the appraiser.

- Title Insurance and Search: This protects you and the lender from any surprises or claims against your property’s title.

- Attorney or Closing Fees: Covers the legal and administrative work to finalize the loan.

- Recording Fees: The fee paid to your local government to officially record the new mortgage.

You generally have a choice: pay these costs out of pocket or roll them into the new loan. Rolling them in is convenient because you don't need cash upfront, but remember, you'll be paying interest on those costs for years to come.

Step-by-Step Example Calculation

Let’s run through a real-world scenario to see how all these numbers fit together. This breakdown shows exactly how we get from your home's value to the cash in your hand.

The Scenario:

- Your Home's Appraised Value: $500,000

- Your Current Mortgage Balance: $250,000

Here's a sample calculation to illustrate how the net cash is determined.

Sample Cash Out Calculation

| Calculation Step | Example Value |

|---|---|

| 1. Home's Appraised Value | $500,000 |

| 2. Maximum Loan-to-Value (80%) | $400,000 |

| 3. Subtract Old Mortgage Balance | -$250,000 |

| 4. Gross Cash Available | $150,000 |

| 5. Estimate Closing Costs (3%) | -$12,000 |

| 6. Estimated Net Cash in Hand | $138,000 |

This example gives you a solid framework for your own situation. Of course, the best way to get a precise estimate is to plug your own numbers into a calculator. You can run the numbers with our mortgage calculators right on our site.

Why Shopping Around Is So Important

The rates and fees you’re quoted can vary dramatically from one lender to the next, which is why it pays to compare. In fact, recent data shows just how serious homeowners are about getting the best deal.

The retention rate for cash-out refinances—the percentage of people who stick with their current lender—is only about 23%. That's way lower than the 37% retention for a standard rate-and-term refi. It tells you that savvy homeowners are actively shopping around for better terms when they’re tapping their equity.

This competition is good news for you. It puts the power in your hands to find the loan that keeps costs low and puts the most cash possible back in your pocket.

Weighing the Pros and Cons

A cash-out refinance can be a powerful financial move, letting you tap into the equity you’ve built in your home. But just like any powerful tool, you need to know how to handle it. It comes with some real benefits, but also some serious risks you need to understand completely.

Making the right choice means looking past the immediate appeal of getting a big check. You have to consider what this means for your mortgage, your monthly budget, and your home in the long run. Let’s walk through both sides of the coin so you can get a clear, balanced picture.

The Upside: What a Cash-Out Refi Can Do for You

The main draw of a cash-out refinance is simple: you can get your hands on a lot of cash at a much lower interest rate than most other types of loans. This opens up some pretty compelling opportunities.

One of the smartest ways people use this money is for debt consolidation. Think about it—if you have credit card debt, you might be paying interest rates over 20%. By taking cash out of your home, you can wipe out those high-interest balances and roll them into your new mortgage. For a deeper dive on this, check out the information on what a cash-out refinance loan is at ConsumerFinance.gov.

Swapping a 22% APR on $40,000 of credit card debt for a 6.5% mortgage rate could literally save you hundreds of dollars every single month.

By trading expensive, unsecured debt for cheaper, secured mortgage debt, you’re not just saving money. You’re simplifying your life with a single, manageable payment and getting on a faster track to being debt-free.

Another huge plus is the flexibility. Unlike a car loan or student loan, the cash you get is yours to use however you see fit. The possibilities are wide open:

- Fund major home improvements: This is a classic. You can finally tackle that kitchen renovation or add a new deck. The key is to assess the return on investment for projects like a bathroom remodel to make sure your money is working for you.

- Cover educational expenses: Paying for college or vocational school without taking on high-interest student loans is a game-changer for many families.

- Handle unexpected costs: Life happens. A cash-out refi can provide a safety net for medical emergencies or other big, unplanned bills.

- Make a down payment: You can even use the funds to buy a second home or an investment property, building your wealth even further.

The Risks: What You Need to Watch Out For

While the benefits look great on paper, you absolutely have to go into this with your eyes wide open. A cash-out refinance isn’t free money, and the stakes are high.

The single biggest risk is that you're increasing the total amount of debt secured by your house. Your new loan is bigger than your old one, which means your home is on the line for more money. If you hit a rough patch financially and can't make the new, potentially higher payments, you could be at risk of foreclosure. This is the most critical factor to consider.

Next up, you have to remember the closing costs. Just like when you first bought your home, a refinance comes with its own set of fees. Expect to pay anywhere from 2% to 5% of the new loan amount. These costs are either paid out of pocket, taken from the cash you receive, or rolled into the new loan balance—meaning you'll be paying interest on them for years.

Finally, think about your loan term. It’s very common for people to refinance into a new 30-year loan. That means the clock on your mortgage starts all over again. Even if your monthly payment feels lower or more manageable, resetting your loan term could mean you pay far more in total interest over the life of the loan. It's a classic trade-off: cash now versus higher long-term costs.

Exploring Your Other Home Equity Options

While a cash-out refinance is a fantastic tool for getting a large lump sum of cash, it’s not the only way to tap into your home's value. Honestly, the best choice always depends on your specific goals, so it pays to understand the alternatives.

Each option comes with a different structure, repayment style, and ideal use case. Let's compare a cash-out refinance to its two main competitors: the Home Equity Line of Credit (HELOC) and the Home Equity Loan.

The Flexible HELOC

Think of a Home Equity Line of Credit (HELOC) less like a traditional loan and more like a credit card that's secured by your house. Instead of getting all the money at once, you’re approved for a revolving line of credit that you can draw from as needed. This "draw period" typically lasts for 5 to 10 years.

This flexibility is perfect for ongoing projects where costs aren't set in stone, like a home renovation, or for covering unpredictable expenses. You only pay interest on what you actually borrow, which can be a huge advantage.

The main thing to watch for is that HELOCs almost always have variable interest rates. This means your payments can go up or down over time, which adds a bit of uncertainty to your monthly budget.

A HELOC is a second mortgage. You'll have two separate payments each month: your original mortgage and your new HELOC payment.

The Predictable Home Equity Loan

A Home Equity Loan also works as a second mortgage, but it functions more like a classic installment loan. You borrow a specific lump sum and then pay it back over a set term with fixed monthly payments.

The biggest benefit here is predictability. Your interest rate is fixed, so your payment never changes. This makes it a great option when you know exactly how much you need for a single, large expense, like a wedding or paying off high-interest credit cards. Many people use this strategy for debt management; understanding what debt consolidation is can help you decide if it's the right move for you.

Just like a HELOC, a home equity loan is a separate lien on your home, meaning you'll be managing two distinct monthly payments. This is a key difference from a cash-out refinance, which rolls everything into a single, new loan.

Comparing Your Choices

So, how do you decide which path is right for you? It really comes down to what you need the money for and your comfort level with different payment structures. Here’s a quick breakdown to help you see the differences at a glance.

| Feature | Cash-Out Refinance | HELOC | Home Equity Loan |

|---|---|---|---|

| Loan Structure | Replaces your primary mortgage with a new, larger one. | A separate, revolving line of credit (second mortgage). | A separate, lump-sum loan (second mortgage). |

| Funds Received | One large lump sum at closing. | Draw funds as needed during a set period. | One large lump sum at closing. |

| Interest Rate | Typically a fixed rate for the entire loan term. | Usually a variable rate that can change over time. | Typically a fixed rate for the entire loan term. |

| Payments | One single, predictable monthly mortgage payment. | Two payments; interest-only at first, then principal and interest. | Two payments; fixed principal and interest from the start. |

Ultimately, choosing between these options is a personal decision. A cash-out refinance simplifies your finances into one payment, but a HELOC or home equity loan allows you to keep your great primary mortgage rate untouched.

Answering Your Top Questions

It's natural to have a few lingering questions when you're thinking about a big financial move like a cash-out refinance. Getting straight answers is the best way to feel confident about your decision. Let's walk through some of the most common things homeowners ask us.

How Long Does the Process Take?

A cash-out refinance moves at about the same pace as your original home loan. You can generally expect the whole process, from the day you apply to the day you sign the final papers, to take somewhere between 30 and 60 days.

The exact timeline really depends on a few moving parts: how fast you can gather your documents, when the appraiser can visit your home, and how busy the lender’s underwriting team is. Staying organized and responding quickly to requests is the best way to keep things on track.

Can I Qualify with Imperfect Credit?

You don't need a flawless credit history to get approved. While a top-tier score will always get you the most competitive rates, many conventional loan programs work with borrowers who have a credit score of 620 or higher.

Lenders are trained to look at the whole picture, not just one number. If you have a steady income and your other debts are well-managed, that can often make up for a credit score that’s less than perfect.

Is the Cash I Receive Taxable?

This is a great question, and we get it all the time. The good news is that in most situations, the cash you get from a cash-out refinance is not considered taxable income.

Why? Because it's not a paycheck or a profit—it's a loan. The IRS sees it as borrowed money that you have to pay back, not as earnings. That said, everyone's financial situation is unique, so it's always a smart move to run it by your tax advisor just to be sure.

The funds from a cash-out refinance are essentially an advance on your home's equity, which you are borrowing against. This loan structure is why the proceeds are generally not taxed.

What Are the Smartest Ways to Use the Funds?

You can use the money for just about anything, but the smartest homeowners use it to improve their overall financial standing. Some of the most popular and effective strategies include:

- Home Improvements: Making renovations that boost your property's value is a classic win-win.

- Debt Consolidation: Wiping out high-interest credit card or personal loan debt can save you a ton of money on interest.

- Education Expenses: It can be a much cheaper way to fund a college education than taking on separate high-rate student loans.

- Building an Emergency Fund: Setting up a solid financial cushion gives you incredible peace of mind for life's surprises.

Tapping into home equity is a strategy that continues to resonate with homeowners. In the first quarter of 2025 alone, U.S. banks originated about $6.61 billion in cash-out refinances, showing just how valuable this tool can be. You can dive deeper into top mortgage trends at FoundationMortgage.com.

Ready to see what your home's equity can do for you? The team at Mortgage Seven LLC is here to give you a clear, no-obligation consultation, answer your specific questions, and map out your best options.