When you apply for a mortgage, your lender zeroes in on one number above all others: the Loan-to-Value (LTV) ratio. In simple terms, it's a percentage that shows how much of the home's price you're borrowing versus how much you're paying upfront.

Think of it as the bank's risk gauge. A lower LTV means less risk for them and more financial benefits for you.

What Is Loan to Value Ratio and Why It Matters

Let's use a seesaw analogy. Your down payment sits on one end, and the loan amount sits on the other. The LTV ratio simply measures the balance between the two.

A bigger down payment pushes your side down, creating a lower LTV. Lenders see this and breathe a sigh of relief. It shows you have more "skin in the game," making you a much safer bet. After all, you have more of your own money invested in the property.

On the other hand, a small down payment means the seesaw tips heavily toward the lender's side. This is a high LTV, and it signals more risk for them since they're fronting a much larger share of the home's value.

Understanding the Lender's Perspective

So, why are lenders so obsessed with this number? From their chair, LTV is the clearest indicator of their potential loss. If a borrower with a high-LTV loan defaults, the bank has more capital at risk and less of a buffer if the home's value drops. This is exactly why your LTV has a direct impact on the kind of mortgage you can get.

A lower LTV can be a game-changer, unlocking some serious perks:

- Better Interest Rates: Lenders reward low-risk borrowers with their best interest rates. This can save you tens of thousands of dollars over the life of your loan.

- Avoiding Private Mortgage Insurance (PMI): On a conventional loan, if your LTV is over 80%, you’ll almost always have to pay PMI. It's an extra monthly fee that protects the lender, not you.

- Easier Loan Approval: A healthy down payment and a low LTV make your application shine, often leading to a much smoother path to getting approved.

To get a clearer picture, let's break down the key parts of LTV.

Quick Guide to Loan to Value (LTV)

This table simplifies the core ideas behind LTV and shows how it directly affects you as a borrower.

| Concept | Simple Explanation | Impact on Borrower |

|---|---|---|

| Loan Amount | The total money you borrow from the lender to buy the home. | The larger the loan, the higher your LTV and monthly payment. |

| Property Value | The lesser of the home's appraised value or its sale price. Lenders always use the lower number. | A higher home value can help lower your LTV, assuming your loan amount stays the same. |

| Down Payment | Your initial contribution from your own funds. This is your "skin in the game." | The more you put down, the lower your loan amount and your LTV. This is the fastest way to get a better deal. |

| LTV Percentage | (Loan Amount / Property Value) x 100 | A high LTV (>80%) often means PMI and higher rates. A low LTV (<80%) means better terms and no PMI. |

Understanding these components puts you in the driver's seat during the mortgage process.

The loan-to-value ratio is a fundamental concept that every homebuyer should grasp, whether you're a first-timer or a seasoned investor working with us at Mortgage Seven LLC. Getting a handle on LTV helps you secure better rates and avoid unnecessary costs like PMI. For those interested in how market swings can affect property values, you can find great analysis at Stewart Valuation Services.

At the end of the day, knowing what LTV is and how it works empowers you to make smarter, more confident financing decisions.

Calculating Your Loan-to-Value Ratio Step by Step

Knowing what LTV means is one thing, but being able to calculate it yourself is where the real confidence comes from. The great news is you don't need a math degree to figure it out. The formula is surprisingly simple and gives you a powerful snapshot of your financial position before you even talk to a lender.

At its core, the LTV calculation is just a straightforward division problem.

Loan Amount ÷ Property Value = Loan-to-Value Ratio (LTV)

To get the percentage that lenders actually use, just multiply that result by 100. This simple math instantly shows the relationship between how much you’re borrowing and what the home is worth.

Putting the LTV Formula into Action

Let’s walk through a typical home-buying scenario to see how this plays out in the real world. You’ll see exactly how your down payment directly shapes your LTV.

Example 1: A First-Time Homebuyer

Imagine you're ready to buy your first place, and it has a purchase price of $500,000. You’ve worked hard to save a $100,000 down payment.

-

Find Your Loan Amount: First, subtract your down payment from the home’s price.

- $500,000 (Property Value) – $100,000 (Down Payment) = $400,000 (Loan Amount)

-

Calculate the LTV: Next, plug those numbers into the formula.

- $400,000 ÷ $500,000 = 0.80

-

Turn It Into a Percentage: Finally, multiply by 100 to get the number your lender will see.

- 0.80 x 100 = 80% LTV

In this situation, that 80% LTV is a fantastic target. For conventional loans, it's the key threshold to avoid paying for Private Mortgage Insurance (PMI), which saves you money every single month. Feel free to play around with different numbers on our mortgage calculators to see how changing your down payment affects your LTV.

How LTV Works for a Refinance

The process for a refinance is almost identical, but we're just swapping out a few of the terms. Instead of a purchase price, you'll use the home's newly appraised value, and your loan amount is simply what you still owe on your mortgage.

Example 2: Refinancing Your Current Home

Let's say a new appraisal values your home at $600,000, and you have a remaining mortgage balance of $420,000.

- Loan Amount: This is your current mortgage balance, so $420,000.

- Property Value: This is the new appraised value, $600,000.

- Calculate the LTV: $420,000 ÷ $600,000 = 0.70

- Convert to a Percentage: 0.70 x 100 = 70% LTV

A 70% LTV is a rock-solid position to be in. It means you’ll almost certainly qualify for the most competitive interest rates available and can drop PMI for good if you haven't already, potentially knocking a significant amount off your monthly payment.

How Lenders See Your LTV Ratio

When a lender looks at your mortgage application, your Loan-to-Value (LTV) ratio tells them a story. It’s not just another piece of data; it’s the clearest indicator of their risk. In one quick percentage, they see how much of their money is at stake versus how much of your own you’ve put on the line.

A high LTV means you have less of your own cash invested in the property. In a lender’s eyes, that’s less "skin in the game," which translates to a riskier loan.

Think of it this way: you’re backing a friend’s new business. If they put in $20,000 of their own money and ask you for an $80,000 loan, you’d probably hesitate. But what if they invested $80,000 and only needed $20,000 from you? That feels like a much safer bet. Lenders work off the very same logic—borrowers with more equity are seen as more committed and far less likely to walk away if times get tough.

The Magic Number: 80%

In the mortgage industry, an 80% LTV is the gold standard. Hitting that number (or getting below it) signals to lenders that you're a low-risk borrower. You’ve put down a solid 20%, showing a serious financial commitment. That simple fact opens up the door to the best interest rates and loan terms available.

The moment you cross above the 80% LTV threshold, the game changes. Your loan is now officially considered higher-risk, and lenders will take steps to protect their investment. This is where you start seeing extra costs and tougher qualification rules that directly hit your wallet.

This intense focus on LTV isn't new. During the housing boom leading up to the 2008 financial crisis, LTV ratios climbed to dangerously high levels, which many experts agree fueled the crash. After 2008, regulations were tightened significantly. By the second quarter of 2023, the median LTV for new mortgages at large banks was a much more stable 75%. This shows just how crucial LTV is to maintaining a healthy housing market. To dig deeper, you can explore the historical impact of LTV on market volatility and its broader economic significance.

How LTV Directly Shapes Your Loan Terms

Your LTV ratio is one of the most powerful factors influencing your mortgage. It has a direct impact on your interest rate, your insurance costs, and even whether you get approved in the first place. Getting a handle on this connection is key to building a strong application.

Here’s exactly how it works:

-

Interest Rates: A lower LTV usually means a lower interest rate. Lenders save their best rates for the safest bets. Even a fraction of a percentage point saved on your rate can add up to tens of thousands of dollars over the 30-year life of your loan.

-

Private Mortgage Insurance (PMI): This is a big one. For conventional loans, an LTV above 80% requires you to pay PMI. This is an insurance policy that protects the lender—not you—if you can't make your payments. It’s an extra monthly fee tacked onto your mortgage until your equity grows and your LTV drops to a safer level, usually 78%.

-

Loan Approval: While a high LTV won’t get you an automatic denial, it definitely makes getting approved harder. To offset the higher risk, a lender might require a stronger credit score or a lower debt-to-income ratio. Certain loan programs also have strict LTV ceilings you simply can't go over.

A low LTV is your strongest negotiating tool. It demonstrates financial stability and responsibility, making you the type of borrower every lender wants to work with.

At the end of the day, knowing how lenders see your LTV gives you power. You can take strategic steps to present the best possible application, aiming for a ratio that not only secures your approval but also locks in the most favorable terms for your new home.

Comparing LTV Rules For Different Loan Programs

When it comes to mortgages, there's no "one-size-fits-all" playbook, especially with Loan-to-Value (LTV) ratios. The maximum LTV a lender is comfortable with is directly tied to the type of loan you're getting. Figuring out these differences is the first step in knowing how to choose the right home loan that fits your financial picture.

Some loans, particularly those backed by the government, are built to make buying a home more accessible by allowing for smaller down payments and, therefore, higher LTVs. On the other hand, conventional and jumbo loans usually play by a stricter set of rules.

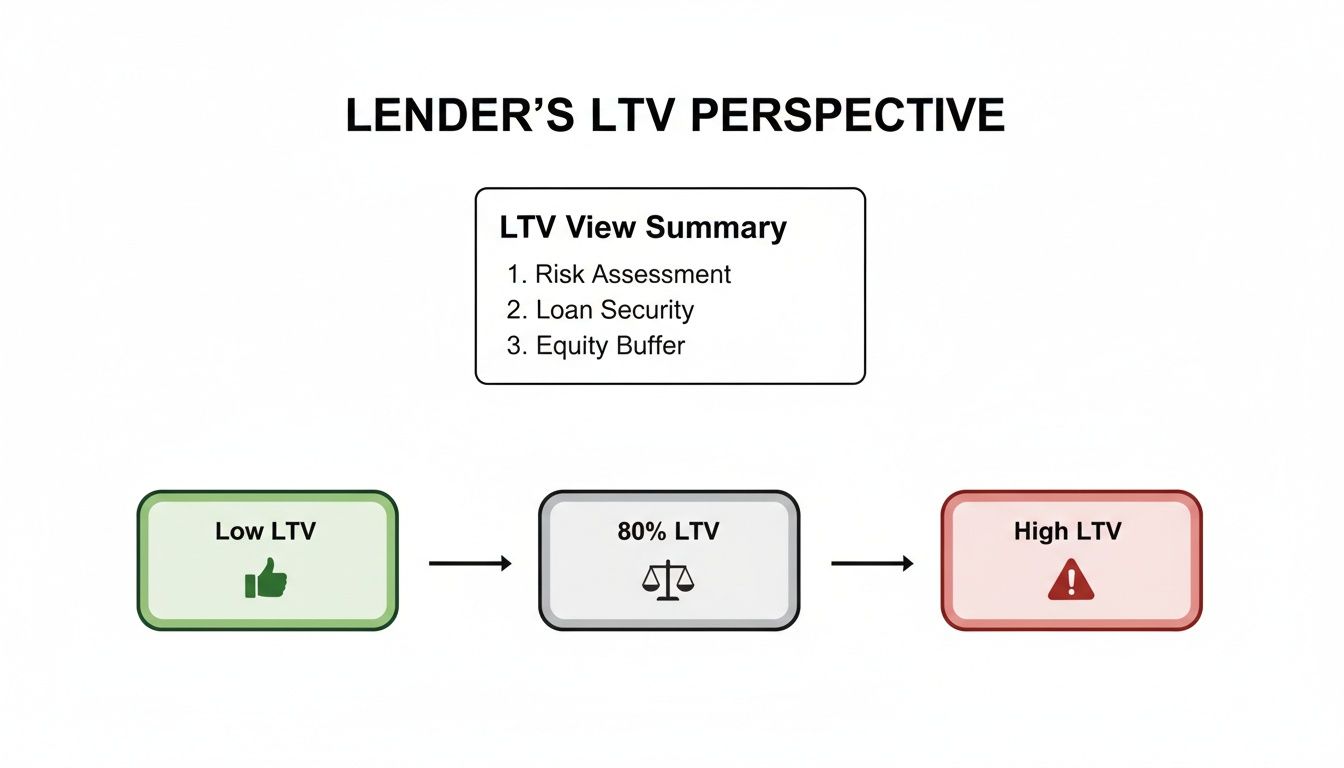

The image below gives you a peek into a lender's mindset, showing how they view risk at different LTV levels.

It’s easy to see why hitting an LTV of 80% or lower is the sweet spot. It signals to a lender that you have significant skin in the game, making your loan a much safer bet for them.

Conventional Loans

Conventional loans are the bread and butter of the mortgage world, but they don't come with a government guarantee. This means the lender takes on all the risk, so they naturally prefer a lower LTV.

You can technically get a conventional loan with just 3% down (a 97% LTV), but it comes with a catch: you'll have to pay Private Mortgage Insurance (PMI). To dodge that extra monthly cost, you'll need to bring your LTV down to 80% or less, which means putting 20% down.

Government-Backed Loan Programs

This is where things get interesting for many buyers. These loans are insured by federal agencies, which gives lenders the confidence to offer fantastic terms, including much higher LTVs.

- FHA Loans: Backed by the Federal Housing Administration, these are a go-to for many first-time buyers. They allow for a maximum LTV of 96.5%, which translates to a down payment of just 3.5%.

- VA Loans: Guaranteed by the Department of Veterans Affairs, this is one of the best benefits for eligible veterans and service members. It allows for a 100% LTV, meaning you can buy a home with zero down payment. Seriously.

- USDA Loans: The U.S. Department of Agriculture backs these loans to encourage homeownership in designated rural and suburban areas. Just like VA loans, USDA loans offer up to 100% LTV, opening the door for buyers without a hefty savings account.

The Bottom Line: Government-backed loans like FHA, VA, and USDA are game-changers. They are specifically designed to help people who might not have a big down payment get into a home.

Specialized And Jumbo Loan Programs

The LTV rules also shift when you step into the world of larger or non-traditional mortgages.

For high-value properties, Jumbo Loans are needed when the loan amount is above the conforming limits set by Fannie Mae and Freddie Mac. Since the lender is putting more money on the line, they’re more cautious. LTVs for these are often capped around 80-90%.

For investors, Debt Service Coverage Ratio (DSCR) loans are a popular tool. Instead of looking at your personal W-2, these loans qualify you based on the property’s rental income. LTVs here usually fall between 75% and 85%.

And for the self-employed, Bank Statement Loans offer a path to homeownership without traditional tax returns. Lenders analyze your bank deposits to verify your income. Because this is a more specialized way of qualifying, LTVs are a bit more conservative, typically topping out around 80% to 90%. For a deeper dive on how some of these options stack up, check out our guide on FHA versus Conventional loans.

Loan Program LTV Requirements At A Glance

To make it easier to compare, here's a quick breakdown of the typical LTV and down payment requirements for the most common loan types.

| Loan Program | Maximum LTV | Minimum Down Payment | Ideal For |

|---|---|---|---|

| Conventional | 97% | 3% | Borrowers with strong credit who want to avoid PMI by putting 20% down. |

| FHA | 96.5% | 3.5% | First-time buyers or those with less-than-perfect credit. |

| VA | 100% | 0% | Eligible veterans, active-duty service members, and surviving spouses. |

| USDA | 100% | 0% | Buyers in designated rural or suburban areas with moderate income. |

| Jumbo | 80-90% | 10-20% | Buyers purchasing high-value properties that exceed conforming loan limits. |

This table shows just how much your options can open up depending on your personal circumstances and the property you're eyeing.

Proven Strategies to Lower Your LTV

Knowing your Loan-to-Value (LTV) ratio is one thing, but actively lowering it is how you actually land a better mortgage deal. A lower LTV shows lenders you have more skin in the game, which makes you a much more attractive borrower and opens the door to better loan terms.

The good news is you have a few powerful strategies to get that number down.

The most straightforward way to slash your LTV is to make a bigger down payment. Every single dollar you put down reduces the amount you need to borrow, which directly lowers your LTV. This one move can be the difference between paying for private mortgage insurance (PMI) and keeping that money in your pocket. It can also lead to a noticeably lower interest rate.

Boosting Your Down Payment

Of course, "just save more money" is easier said than done. But there are a few practical ways to beef up your initial investment.

- Down Payment Assistance (DPA) Programs: Don't overlook these. Many state and local programs offer grants or low-interest loans specifically to help with down payments and closing costs. They can give you the push you need to hit that magic 20% down payment mark.

- Financial Gifts from Family: Lenders are perfectly fine with you using gifted money for a down payment. You'll just need a formal gift letter confirming the funds are a true gift, not a loan. This can be a huge help in lowering your LTV without draining your own savings.

As you look into these options, it's smart to grasp the full financial picture. A lower LTV helps you sidestep expensive mortgage insurance premiums, which come with their own rules and tax implications.

Strategies for Current Homeowners

If you already own a home and are thinking about refinancing, your game plan for lowering LTV is a little different. Your focus isn't on a down payment but on the equity you've already built up over time.

One of the best moves you can make is to pay down your loan principal. Making extra payments—even small ones—adds up faster than you’d think, growing your equity and shrinking your loan balance. This strategy becomes even more powerful when the real estate market is on your side.

A rising tide lifts all boats, and a strong housing market can lift your home's value. When your property's appraisal comes in higher, your LTV automatically drops, even if your loan balance stays the same.

Let's say your home was worth $400,000 and you owed $340,000 (an 85% LTV). If a new appraisal values it at $450,000, your LTV suddenly drops to just 75.5%. That kind of drop could easily qualify you for a better interest rate or finally let you cancel PMI. You can dig deeper into how refinancing strategies can improve your financial position.

In the end, whether you're buying for the first time or refinancing, it all comes down to planning. By taking deliberate steps to lower your LTV, you put yourself in the driver's seat during mortgage negotiations, making sure you walk away with the best terms possible.

Going Beyond LTV with CLTV and HCLTV

Once you've wrapped your head around the basic Loan-to-Value (LTV) ratio, you're ready for the next level. Lenders don't just stop at LTV; they often look at two related metrics: Combined Loan-to-Value (CLTV) and Home Equity Combined Loan-to-Value (HCLTV).

These numbers come into play the moment you have more than one loan attached to your property. Think of your primary mortgage LTV as a single snapshot. CLTV and HCLTV are like the panoramic photo, giving the lender a full view of every lien and all the debt tied to your home. This is especially critical if you're thinking about getting a home equity loan or a Home Equity Line of Credit (HELOC).

So, What's Combined Loan to Value (CLTV)?

CLTV is the go-to metric when you already have a first mortgage and you're adding a second one, like a home equity loan. It simply adds all your loan balances together and measures that total against your home's value. The lender gets a clear percentage of how much of your home's worth is financed.

The math is pretty straightforward.

(First Mortgage Balance + Second Mortgage Amount) ÷ Property Value = CLTV

Let's walk through an example. Say your home is appraised at $500,000, your current mortgage balance is $300,000, and you need a $50,000 home equity loan to finally build that new deck.

- Total Loan Amount: $300,000 + $50,000 = $350,000

- Calculation: $350,000 ÷ $500,000 = 0.70

- Your CLTV: That comes out to 70%.

Most lenders cap their maximum CLTV somewhere around 80-85%. They need to see that you still have a solid equity cushion in the property, which protects both you and them.

And Then There's Home Equity Combined Loan to Value (HCLTV)

HCLTV takes things one step further, and it’s all about HELOCs. Unlike a fixed loan, a HELOC is a revolving line of credit. You can draw money, pay it back, and draw it again, much like a credit card. Because of this, lenders need to account for their total potential risk.

Instead of just looking at what you've used from your HELOC, HCLTV factors in the entire credit limit.

Here’s the formula:

(First Mortgage Balance + Full HELOC Credit Limit) ÷ Property Value = HCLTV

Let’s stick with our previous scenario. Your home is worth $500,000 and you owe $300,000. This time, you get a HELOC with a $75,000 credit limit. Even if you've only drawn $10,000 to start, the lender's calculation uses the full $75,000.

- Total Potential Debt: $300,000 + $75,000 = $375,000

- Calculation: $375,000 ÷ $500,000 = 0.75

- Your HCLTV: This lands you at 75%.

Getting comfortable with these ratios isn't just a mental exercise—it directly impacts your financial planning. In fact, on a macro level, LTV ratios have historically been a surprisingly strong predictor of housing market trends. Research has consistently shown that periods of very high LTVs often lead to market downturns, a pattern seen for decades in the U.S. market. If you're curious about the economics, you can dive into the research on LTV's predictive power for a much deeper look.

By mastering LTV, CLTV, and HCLTV, you’re no longer in the dark. You have a complete picture of your home equity, which is exactly what you need to make smart, strategic moves with your biggest asset.

Common Questions Borrowers Ask About LTV

Diving into home financing can feel like learning a new language, so it's only natural to have a few questions. Let's tackle some of the most common things borrowers ask about the Loan-to-Value ratio, with clear answers to help you move forward.

Can I Get a Mortgage with an LTV Over 80 Percent?

Yes, absolutely. In fact, many of today's most popular loan programs were created specifically to help buyers who don't have a 20% down payment. This flexibility has opened the door to homeownership for millions.

Government-backed loans are often the first place people look when they have a higher LTV.

- FHA Loans: A great option that allows for a maximum LTV of 96.5%. That means you only need to bring a 3.5% down payment to the table.

- VA and USDA Loans: It doesn't get much better than this. For eligible veterans and rural homebuyers, these programs permit a 100% LTV—which means no down payment is required at all.

Even with conventional loans, you can secure a mortgage with an LTV over 80%. The key difference is you'll almost certainly have to pay for Private Mortgage Insurance (PMI). This is an extra monthly fee that protects your lender, so it's a cost you'll want to factor into your budget when you're weighing your options.

How Does My Home Appraisal Affect My LTV?

The home appraisal is a make-or-break moment in the LTV calculation. When figuring out the "value" part of the equation, lenders will always use the lower of two figures: your agreed-upon purchase price or the home's official appraised value.

This rule is in place to protect the lender from loaning out more money than a property is actually worth. If an appraisal comes in lower than what you offered, your LTV automatically goes up. This can create a funding gap that might mean bringing more cash to closing or heading back to the negotiating table with the seller.

On the flip side, a strong appraisal is your best friend when refinancing. A higher home value can push your LTV down, which could be your ticket to eliminating PMI and locking in a much better interest rate.

Does LTV Matter for a Cash-Out Refinance?

LTV is especially critical when you're looking to pull cash out of your home's equity. For most lenders, this is one of the most important qualifying factors, and they typically set a firm maximum LTV, often capped at 80%.

What this means is that your new, larger loan amount—which includes both your old mortgage balance and the cash you're taking out—can't be more than 80% of your home's current appraised value. This guideline is designed to ensure you keep a healthy 20% equity cushion in your property, protecting both you and the lender.

When Is the Best Time to Discuss My LTV Situation?

The sooner, the better. The ideal time to talk about your LTV is right at the very beginning of your homebuying or refinancing journey. An early conversation with a mortgage pro gives you a clear, upfront look at where you stand.

A good mortgage broker can assess your savings, income, and overall goals to give you a realistic idea of your potential LTV. This helps you set the right budget, understand your true purchasing power, and zero in on the loan programs that actually make sense for you.

This is especially true for real estate investors. Those using DSCR loans need to be aware of how LTV caps, which often fall between 75-90%, can shield their portfolios from market swings. As you can read more about how LTV ratios affect market stability, you'll see that smart LTV management is crucial. An early consultation is the best way to navigate these rules and find the right lender.

Feeling more confident about LTV but still have questions about your unique situation? The team at Mortgage Seven LLC is here to provide the clear, personalized guidance you need. We'll help you understand your options and find the perfect loan for your goals. Schedule your free consultation today.