When you get a mortgage, you'll almost certainly hear the term "escrow account." So, what is it? Think of it as a special savings account managed by your mortgage lender, set up to handle your property taxes and homeowners insurance premiums for you.

Instead of you getting hit with huge tax bills once or twice a year, your lender collects a little bit of that money with each monthly mortgage payment. They hold it in the escrow account and then pay those big bills on your behalf when they’re due.

Your Mortgage Escrow Account Explained

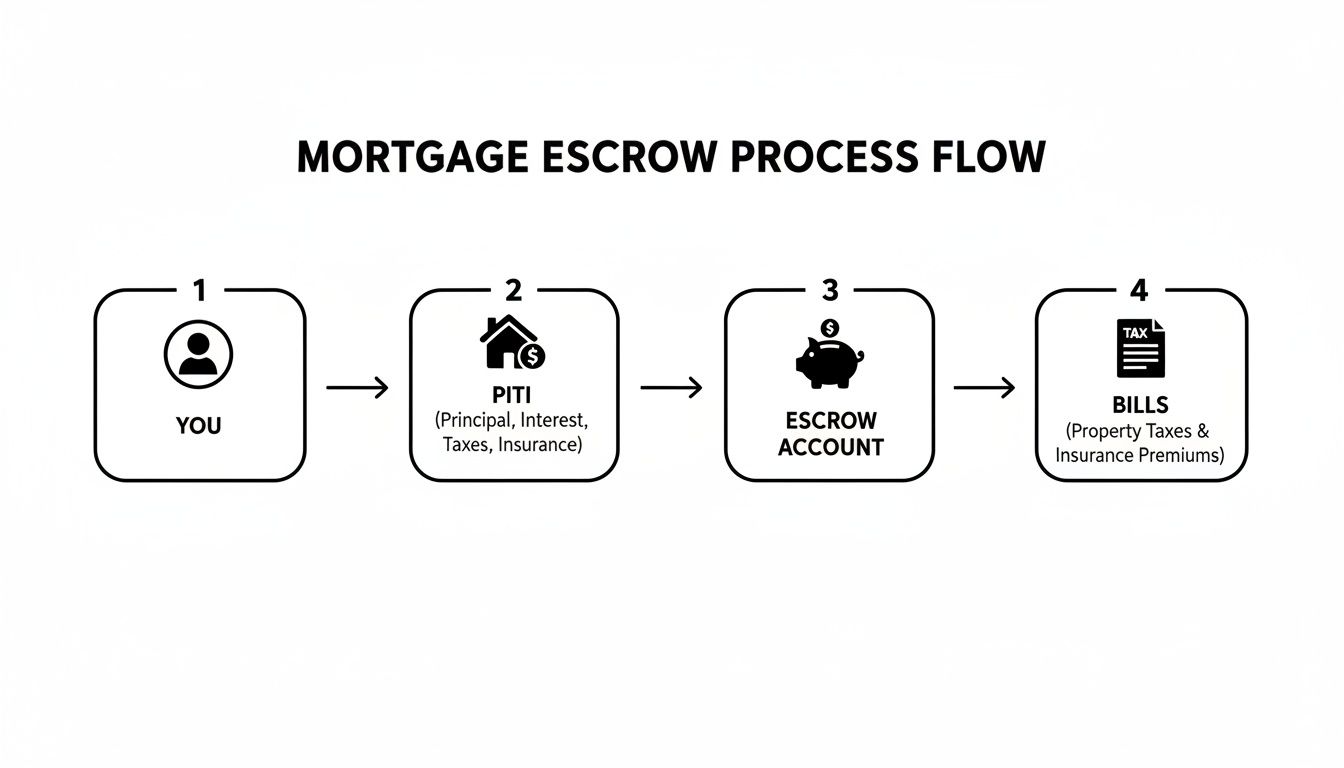

The easiest way to think about an escrow account is as a financial autopilot for two of your biggest, most predictable homeownership expenses. It bundles these costs into your main mortgage payment, making your life a whole lot simpler.

You'll often hear this all-in-one payment referred to as PITI: Principal, Interest, Taxes, and Insurance. The principal and interest portions go directly toward paying off your loan, while the "T" and "I" portions are funneled into your escrow account to cover property taxes and homeowners insurance.

This setup is a huge relief for many homeowners. It ensures your taxes and insurance are always paid on time, so you don't have to worry about missing a deadline. For anyone new to managing a home's finances, this brings incredible peace of mind. If you're just starting out, our resources for first-time homebuyers can help you feel much more prepared for the journey.

What Escrow Covers and What It Does Not

It’s really important to know exactly what this account handles and, more importantly, what it doesn't. Your escrow account is designed for very specific, recurring costs that are directly tied to the property itself—namely, taxes and insurance.

The core purpose of an escrow account is to protect both you and the lender. It prevents lapses in insurance coverage or the risk of a tax lien on the property, which could jeopardize the lender's investment.

This distinction is critical. New homeowners sometimes assume all their housing bills run through this account, but that's not the case. You'll still need to budget for and pay other regular costs like HOA dues, utilities, and maintenance directly.

For example, the funds in your escrow account will cover your homeowners insurance premiums. To get a better handle on what that involves, check out a complete guide to a homeowners insurance policy.

This isn't some niche feature; it's incredibly common. In fact, approximately 80% of all borrowers have an escrow account. For many loans, it's not even optional—they're required for most conventional loans where the down payment is less than 20%, and they are mandatory for all FHA loans.

To make it crystal clear, here’s a simple table showing what your escrow account typically pays versus what you'll need to handle yourself.

What Your Escrow Account Covers vs What It Does Not

This table provides a clear breakdown of typical expenses managed through an escrow account versus homeowner costs that are paid directly.

| Expense Type | Typically Paid from Escrow | Typically Paid Directly by Homeowner |

|---|---|---|

| Property Taxes | ✅ | |

| Homeowners Insurance | ✅ | |

| Private Mortgage Insurance (PMI) | ✅ (If applicable) | |

| Homeowners Association (HOA) Dues | ✅ | |

| Utility Bills (Water, Gas, Electric) | ✅ | |

| Home Maintenance and Repairs | ✅ | |

| Flood or Earthquake Insurance | ✅ (If required by lender) | ✅ (If optional) |

Understanding this split is key to building an accurate household budget and avoiding any surprise bills down the road.

How Lenders Figure Out Your Escrow Payment

Ever look at your mortgage statement and wonder where that escrow number comes from? It can seem like a mysterious figure plucked from thin air, but there’s actually a pretty simple formula behind it. Lenders aren't guessing; they're making a calculated estimate to make sure your future bills get paid on time.

The whole process starts with the two big, recurring costs of homeownership outside of your mortgage itself: your property taxes and your homeowners insurance premium. Your lender will get an estimate for what these two expenses will cost you over the next 12 months.

They take that total annual figure and divide it by 12. Voilà. That’s the core of your monthly escrow payment. It’s just a way to break down massive yearly bills into smaller, more manageable monthly bites.

Adding a Safety Net: The Escrow Cushion

But wait, there's a little more to it. Most lenders will add a small buffer to that monthly payment. This is what's known as an escrow cushion, and it's there to protect both you and the lender.

Think of it as a small rainy-day fund for your escrow account. If your property taxes unexpectedly jump up or your insurance premium increases, this cushion helps absorb the shock so your account doesn't immediately go into the red. Federal law (specifically the Real Estate Settlement Procedures Act, or RESPA) keeps this in check, limiting the cushion to no more than two months' worth of escrow payments.

A Real-World Calculation Example

Let's walk through an example for a home in Northern Virginia to see how this plays out in real numbers.

- Estimated Annual Property Taxes: $6,000

- Estimated Annual Homeowners Insurance: $1,800

First, your lender adds those two figures together to get your total annual escrow obligation.

$6,000 (Taxes) + $1,800 (Insurance) = $7,800 per year

Next, they divide that by 12 to find the base monthly payment.

$7,800 / 12 months = $650 per month

Finally, they'll calculate the maximum allowable cushion, which is simply two times that monthly payment.

$650 x 2 = $1,300 cushion

So, your monthly PITI payment would include that $650 going toward escrow. The initial cushion amount is typically collected from you at closing. Want to see how different tax and insurance scenarios might affect your own bottom line? Feel free to play around with the numbers on our mortgage calculators.

This simple process is what keeps the wheels turning, ensuring money is always there when those big bills come due.

As the diagram shows, the escrow account is just a holding tank. You pay into it monthly, and your lender pays out of it when your tax and insurance bills are due. To get a better handle on the insurance side of things, it helps to understand what an insurance premium is in the first place. The more you understand each piece of the puzzle, the more confident you'll feel about your mortgage payment.

Navigating Your Annual Escrow Analysis

Once a year, you can expect a document in the mail from your mortgage servicer called an annual escrow analysis statement. Think of it as a report card for your escrow account. It breaks down what your lender projected you'd need for taxes and insurance, what they actually paid out, and what they're forecasting for the year ahead.

This yearly review isn't just a courtesy; it's a standard, legally required process. Its main job is to make sure your account has enough cash to cover your property tax and homeowners insurance bills, which almost always change from year to year. The analysis simply compares the money that went in with the money that went out, and the result is either a shortage or a surplus.

Understanding an Escrow Shortage

An escrow shortage is exactly what it sounds like: the actual cost of your taxes and insurance ended up being higher than what your lender had estimated and collected from you over the past 12 months. This is pretty common, especially if your county's property assessments went up or your insurance company raised its rates.

When a shortage happens, your lender has already paid the bills for you. The problem is, your escrow account now has a negative balance that you need to make up.

Don’t panic if you see a shortage. It’s a normal part of the process and just means costs went up. Your lender will give you clear options to get back on track.

To correct this, the lender will recalculate your payment. Most of the time, they’ll take the shortage amount, divide it by 12, and add that slice to your monthly mortgage payment for the next year. You might also have the option to pay the full amount in one go. For a deeper dive into these mechanics, you can explore how escrow works on matic.com.

You generally have two ways to handle a shortage:

- Pay it in a lump sum: You can simply write a check for the entire shortage amount to catch the account up immediately.

- Spread it out: Your lender will automatically divide the shortage by 12 and add that amount to your monthly mortgage payment over the next year.

Keep in mind, your new monthly payment will also be adjusted upwards to reflect the new, higher costs for the upcoming year. This is to prevent you from falling short all over again.

What Happens with an Escrow Surplus

On the flip side, an escrow surplus means your lender overestimated your tax and insurance costs. You've essentially paid more into your escrow account than was actually needed to cover the bills, leaving a little extra cash sitting in there.

This can happen for a few reasons, like if you shopped for a cheaper homeowners insurance policy or if your property taxes didn't increase as much as expected.

When there's a surplus, your lender typically has two ways to handle it, and it usually depends on the amount:

- Issue a Refund Check: If the extra amount is over $50, federal law requires your lender to mail you a check for the surplus within 30 days of completing the analysis.

- Apply it to Your Account: For smaller amounts (under $50), the lender can choose to keep the money in your account and use it as a credit toward your future escrow payments.

Getting a surplus check in the mail is always a nice surprise. Just remember that it also means your total monthly mortgage payment will likely go down for the next year, as your lender adjusts your escrow contribution to match the lower projected costs. This annual check-up is all about keeping your payments in sync with your real-world expenses.

Why Did My Mortgage Payment Change? It's Probably Your Escrow Account.

It’s a frustrating moment every homeowner dreads. You got a fixed-rate mortgage specifically so your payment would be predictable. Then, out of the blue, you get a notice that your monthly payment is going up. What gives?

Nine times out of ten, the culprit is your escrow account. While the principal and interest portion of your payment is locked in, the "T" and "I" in your PITI—your property taxes and homeowners insurance—are anything but. These expenses change, often annually, and your lender has to adjust what they collect from you to cover the new costs.

This isn't a mistake or your servicer trying to pull a fast one; it’s a normal part of the homeownership cycle. The annual escrow analysis is just the lender squaring up the books—comparing what they collected versus what they actually paid out—and then forecasting what you’ll need for the year ahead.

The Property Tax Rollercoaster

One of the most frequent reasons for an escrow payment hike is a jump in your property taxes. Your local county or municipality re-evaluates property values on a set schedule to fund everything from schools and roads to fire departments.

If your home's assessed value goes up, your tax bill usually follows. But even if your home's value doesn't change, your local government can simply raise the tax rate itself, which still results in you owing more.

Think of it this way: when your tax bill goes up, it’s a direct message that your escrow payments must increase to cover it. Your lender is just the middleman, adjusting your monthly payment to make sure that larger bill gets paid on time.

The Ever-Changing Cost of Homeowners Insurance

The other moving part in this equation is your homeowners insurance premium. Insurance costs aren't set in stone. They're influenced by a whole host of factors, many of which are completely out of your hands. This is a crucial piece of understanding what a mortgage escrow account is really for and how it works long-term.

Lately, these costs have been rising steeply across the country, causing escrow payments to jump and creating new affordability headaches for homeowners. This trend is a double whammy of rising property tax assessments and, even more significantly, soaring homeowners insurance premiums. You can dig deeper into these nationwide trends and the factors driving up homeownership costs on Fox Business.

So, what makes your insurance premium spike and your escrow payment follow?

- Inflation: Simply put, the cost to rebuild your home is higher today than it was last year. Rising prices for lumber, materials, and labor get passed on to you through higher premiums.

- Location, Location, Risk: If your region has seen an uptick in major weather events like hurricanes, wildfires, or hailstorms, insurers will raise rates across the board to cover their increased risk.

- Your Claims History: If you’ve had to file a claim or two, your provider may now view your property as a higher risk, which often translates into a higher renewal rate.

When your insurance company raises your premium, they send a notice to you and your mortgage lender. Your lender then has to recalculate your escrow contribution to cover that pricier policy, which directly leads to a bigger monthly mortgage payment for you.

Should You Consider Waiving Escrow?

While having an escrow account is the default for most homeowners—offering a set-it-and-forget-it approach to taxes and insurance—it's not your only choice. For some, waiving escrow and taking direct control of those payments is an attractive alternative. But it’s a path that comes with serious responsibilities and isn't open to just anyone.

Lenders are typically only willing to grant an escrow waiver to borrowers they see as low-risk. This usually means you need at least 20% equity in your home, which is also the threshold for avoiding Private Mortgage Insurance (PMI). If you have a government-backed loan, like an FHA or VA loan, waiving escrow generally isn't on the table. These programs mandate escrow to protect the lender’s investment.

Weighing the Pros and Cons

Deciding to manage your own property tax and insurance payments is a big deal. On the plus side, you get to keep more of your money working for you. Instead of parking thousands of dollars in a non-interest-bearing account with your lender, you could hold those funds in a high-yield savings account, earning interest right up until the bills are due.

But that freedom comes with a catch. The responsibility to budget for these massive, infrequent bills falls squarely on your shoulders. If you forget a due date or don't save enough, you could face hefty late fees, a lapse in your homeowners insurance, or even a tax lien on your property.

The core trade-off is simple: convenience versus control. Escrow automates payments for peace of mind, while waiving it gives you direct control over your funds but demands strict financial discipline.

Before you make a call, it’s smart to look at both options side-by-side. Seeing how they stack up against your own financial habits and comfort with risk is key.

Escrow Account vs Self Management A Comparison

This table weighs the advantages and disadvantages of having a lender-managed escrow account versus paying taxes and insurance on your own.

| Feature | With an Escrow Account | Without an Escrow Account (Waived) |

|---|---|---|

| Payment Method | Costs are bundled into your monthly mortgage payment. | You must save and pay large lump sums directly to the tax authority and insurance company. |

| Budgeting | Simple and predictable. Your lender handles the calculations. | Requires disciplined, long-term saving for bills that come due once or twice a year. |

| Financial Benefit | None. Funds typically do not earn interest for the homeowner. | You can earn interest on the money you save in a personal high-yield savings account. |

| Risk of Late Fees | Very low. The lender is responsible for making timely payments on your behalf. | Higher. You are solely responsible for tracking due dates and making payments on time. |

Ultimately, there’s no single right answer. An escrow account offers a reliable, hands-off system, which is perfect for anyone who values simplicity and security. On the other hand, if you're a meticulous budgeter who wants to maximize every dollar, the control (and potential interest earnings) of self-management might be worth the extra effort.

How Mortgage Seven Helps You Understand Escrow

Getting a handle on your escrow account is one of the best ways to make homeownership feel predictable and stress-free. This is exactly where we at Mortgage Seven LLC step in to make a real difference.

We believe that a truly great mortgage experience comes from understanding, not just number-crunching. That’s why we work hard to give our clients, especially first-time homebuyers in the Fairfax, VA area, clear and practical guidance right from the start.

More Than Just a Loan Application

Our team doesn't just push your application through a system. We actually take the time to walk you through every single piece of your mortgage payment.

We’ll break down exactly how your Principal, Interest, Taxes, and Insurance (PITI) add up, so you see the complete picture. This hands-on approach means you won't be caught off guard by your first mortgage statement or that first annual escrow analysis.

We are committed to total transparency. Our goal is to make you feel confident in your financial decisions long after you get the keys to your new home, positioning us as your go-to resource for home financing.

Figuring out the ins and outs of an escrow account can feel like a lot to take on. We make it simple. We’ll explain why your payment might change from year to year and what to expect, turning what seems complicated into straightforward, manageable information.

Ready to see what a mortgage process built on clarity and real support feels like? Contact Mortgage Seven today to schedule a time to chat. We'd love to show you how our personalized approach can help you reach your homeownership goals.

A Few Common Escrow Questions

Once you get the hang of escrow, a few practical questions almost always pop up. What happens if you sell? What if you refinance? Can you fight the lender's numbers? It's smart to think through these scenarios before they happen.

Let's walk through some of the most common questions we hear from homeowners about their escrow accounts.

What Happens to My Escrow Account When I Refinance?

This is a big one. When you refinance, you're essentially paying off your old mortgage completely, which means the escrow account tied to that loan gets closed out.

Your old lender will cut you a check for whatever money is left in that account. You can typically expect to see that refund within 30 to 60 days after your refinance closes. At the same time, your new loan will need its own, brand-new escrow account, and you'll fund that one as part of your new closing costs.

Can I Dispute My Annual Escrow Analysis?

Yes, absolutely. And you should! The money in your escrow account is your money, after all. If you get your annual statement and something looks off—maybe they've based their projections on last year's higher insurance premium—don't just accept it.

Get on the phone with your mortgage servicer right away. The key is to have your proof ready, like a copy of your new, lower insurance bill or an updated tax assessment. Lenders are required to investigate and fix legitimate errors.

Key Takeaway: Always give your annual escrow analysis a close read. It's your job to make sure the numbers are based on current, accurate tax and insurance figures. If they're not, speak up.

Does the Money in My Escrow Account Earn Interest?

For the vast majority of homeowners, the answer is no. Only a handful of states legally require lenders to pay interest on the funds they hold in escrow.

This is actually a major reason why some people, especially those who are great with their finances, choose to waive escrow once they have enough equity. They'd rather put that money into a high-yield savings account and earn some interest on it themselves. You can find answers to more common questions on our detailed mortgage FAQ page.

At Mortgage Seven LLC, we don't wait for you to run into problems. We believe in answering your questions before you even think to ask them. We want you to understand every line item and feel completely confident, especially when it comes to escrow. Let us show you a smoother way home—start your application online today.