Mortgage insurance is one of those terms that can feel confusing, but the concept is actually pretty simple. It's an insurance policy that protects your lender—not you—if you stop making payments on your home loan.

Lenders typically require it when you put down less than 20% of the home's purchase price. Think of it as a safety net for them, which in turn makes it possible for you to buy a home without having to save up a massive down payment.

What Is Mortgage Insurance in Simple Terms

Let's cut through the financial jargon. Imagine mortgage insurance as a temporary "co-signer" that vouches for the riskiest portion of your loan. From a lender's perspective, a smaller down payment means higher risk.

By requiring mortgage insurance, the lender brings in a third party (the insurance company) to cover their potential losses if things go south. You're the one paying the premium for this "co-signer," but that monthly payment is what gives the lender the confidence they need to hand you the keys to your new home.

This setup is exactly what unlocks homeownership for millions of people who might otherwise be stuck renting for years. It bridges the gap between what you have saved and what the lender needs to feel secure.

For a quick reference, here’s a simple breakdown of the key ideas.

Mortgage Insurance at a Glance

| Concept | Simple Explanation |

|---|---|

| Who it protects | The lender, not the homeowner. |

| Why it's needed | You made a down payment of less than 20%. |

| Who pays for it | You, the borrower, as part of your monthly payment. |

| Is it permanent? | No, it can usually be removed once you have enough equity. |

This table captures the essence of mortgage insurance, but let's dive a little deeper into who really benefits.

Who Benefits From Mortgage Insurance

Even though you’re footing the bill, the lender is the direct beneficiary of the policy. This is a common point of confusion. Mortgage insurance won't cover your payments if you lose your job or hit a financial rough patch. Its sole purpose is to make sure the lender gets its money back if the loan ends in foreclosure.

So, what's in it for you? The indirect benefits are huge:

- Faster Path to Homeownership: It lets you buy a home now instead of waiting years to save up a 20% down payment.

- Get in the Market: You can start building equity and benefit from potential home value appreciation much sooner.

This tool is a fundamental part of making housing accessible, especially for first-time homebuyers. It’s a specific type of risk management that mirrors principles found across the broader insurance industry.

Navigating Your Options With an Expert

The first step to controlling this cost is understanding what it is and why you're paying it. The best news? It's not forever. As you pay down your mortgage and your home's value increases, you build equity and can eventually get rid of the insurance payment.

This is where working with an experienced mortgage broker from Mortgage Seven LLC gives you a real advantage. We can help you explore loan programs that might not require mortgage insurance at all, or we can map out a clear strategy to eliminate it as quickly as possible. A solid plan from day one can save you thousands over the life of your loan.

The Different Types of Mortgage Insurance Explained

While all mortgage insurance protects the lender, it isn't a one-size-fits-all product. The kind of policy you'll have is tied directly to the type of loan you get. For the most part, you'll run into one of two main varieties: Private Mortgage Insurance (PMI) for conventional loans or the Mortgage Insurance Premium (MIP) that comes with government-backed FHA loans.

It’s incredibly important to know the difference between them. The costs, how you pay, and—most importantly—how you can eventually stop paying vary wildly. Think of it like choosing between two different highways to get to the same destination. Both get you to homeownership, but they have different tolls and rules of the road.

Understanding Private Mortgage Insurance for Conventional Loans

If you get a conventional mortgage—that is, one not backed by a government agency like the FHA or VA—and you put down less than 20%, you’re almost certainly going to pay for Private Mortgage Insurance, better known as PMI. This is the version most homeowners are familiar with.

One of the upsides to PMI is its flexibility. Unlike the government-mandated alternative, you often have a few different ways to handle the payments.

- Borrower-Paid Mortgage Insurance (BPMI): This is the classic setup. Your PMI premium is simply added as a line item to your monthly mortgage payment. It's straightforward and easy to track.

- Single-Premium Mortgage Insurance (SPMI): With this option, you pay the entire PMI premium in one lump sum at closing. It costs more upfront, but it keeps your monthly mortgage payment lower.

- Lender-Paid Mortgage Insurance (LPMI): Here, the lender "pays" the insurance premium for you. Of course, there's no free lunch—they do this by giving you a slightly higher interest rate for the entire life of the loan.

Which one is right for you? It really comes down to your financial strategy. BPMI is easy and can be canceled down the road. SPMI is great if you have the cash and want the lowest possible monthly bill. LPMI can also reduce your monthly payment, but that higher interest rate often means you'll pay more over the long haul. We dive much deeper into this in our guide, and you can learn more about private mortgage insurance in our article.

The Details of FHA Mortgage Insurance Premium

If you go with a loan insured by the Federal Housing Administration (FHA), you'll deal with a completely different animal called the Mortgage Insurance Premium, or MIP. FHA loans are a huge help for first-time homebuyers because they let you buy a house with as little as 3.5% down. But that low barrier to entry comes with a very rigid, two-part insurance cost.

First, you’ll have an Upfront Mortgage Insurance Premium (UFMIP). This is a one-time charge, currently 1.75% of your total loan amount, that’s due at closing. Most people don't pay this out of pocket; instead, they roll it into the loan balance.

Second, you'll have an Annual MIP. This premium is paid in monthly installments for as long as you have the insurance, tacked right onto your mortgage payment.

Key Difference: Unlike PMI, FHA MIP is famously difficult to get rid of. For the vast majority of FHA borrowers today, that annual MIP sticks around for the entire life of the loan unless you sell the house or refinance into a different loan type.

This long-term commitment is a massive factor to consider when you're weighing an FHA loan against a conventional one. According to DataIntelo, FHA-insured loans now account for 12% of all new mortgages—a significant jump from the pre-pandemic figure of 8%. This surge is largely fueled by younger buyers using that 3.5% down payment option to get into a market where median home prices are hovering around $420,000.

How Much Does Mortgage Insurance Actually Cost?

So, what's the bottom line? How much will mortgage insurance actually take out of your pocket each month?

There’s no single, flat fee. Think of it more like a sliding scale based on how much risk the lender is taking on. The cost is quoted as an annual percentage of your loan amount, but you'll pay it in monthly installments.

Typically, you can expect the rate to be somewhere between 0.5% and 2.0% of your total loan each year. On a $400,000 mortgage, that works out to an extra $167 to $667 tacked onto your monthly payment. That's a serious chunk of change, so understanding what drives that cost is key to keeping it as low as possible.

The Main Factors That Determine Your Premium

Lenders don't just pick a number out of thin air. They look at a few key pieces of your financial picture to figure out how likely you might be to default on the loan. The higher they think that risk is, the more you'll pay for the insurance that protects them.

It really boils down to three big things:

- Your Credit Score: This is the heavyweight champion, especially for Private Mortgage Insurance (PMI). A high credit score is proof of your track record with debt, telling insurers you're a reliable borrower. Someone with a 760 score is going to get a much friendlier rate than someone with a 640.

- Your Down Payment and LTV: How much skin you have in the game matters. A small down payment means a higher Loan-to-Value (LTV) ratio, which is a riskier position for the lender. Putting down 5% (a 95% LTV) will cost you more in insurance than putting down 15% (an 85% LTV). To get a better handle on this crucial metric, check out our guide on what the loan-to-value ratio is.

- Your Loan Type: As we've discussed, conventional loans have PMI and FHA loans have MIP. Their cost structures are worlds apart. PMI rates are highly customized to your risk profile, while FHA MIP rates are standardized across the board by the government.

Improving your credit score by just 20 points can significantly lower your PMI rate, saving you thousands over the life of your loan.

This just goes to show how much influence you have. A little prep work on your finances before you apply can translate into huge long-term savings.

Example 1: Calculating PMI on a Conventional Loan

Let's put some real numbers to this. Say you're buying a $450,000 home with 10% down and you've got a solid credit score of 740.

- Home Price: $450,000

- Down Payment: 10% ($45,000)

- Loan Amount: $405,000

- PMI Rate: With your strong credit and 90% LTV, the insurer gives you a PMI rate of 0.58% per year.

To get the annual cost, we'll multiply the loan amount by your rate: $405,000 x 0.0058 = $2,349 for the year.

Divide that by 12, and your monthly PMI payment is $195.75. That’s the amount that gets added to your mortgage bill every month until you've built up enough equity to get rid of it.

Example 2: Breaking Down MIP for an FHA Loan

Now, let's run the numbers for that same $450,000 house, but this time with an FHA loan—a popular choice for buyers with a smaller down payment.

- Home Price: $450,000

- Down Payment: 3.5% ($15,750)

- Base Loan Amount: $434,250

- Upfront MIP (UFMIP): First, FHA loans have an upfront premium of 1.75% of the loan amount. That's $434,250 x 0.0175 = $7,600. Most people roll this cost into the loan, which would bring the total loan amount to $441,850.

- Annual MIP Rate: For FHA loans with less than 5% down, the current annual rate is 0.55%.

To find the annual MIP payment, you multiply the base loan amount by this rate: $434,250 x 0.0055 = $2,388.38 per year.

That breaks down to a monthly MIP payment of $199.03.

PMI vs FHA MIP Cost Comparison

It's helpful to see these two scenarios side-by-side to really understand the financial trade-offs. While the monthly payments in our example look similar, the long-term cost and structure are very different.

| Factor | Conventional Loan with PMI | FHA Loan with MIP |

|---|---|---|

| Home Price | $450,000 | $450,000 |

| Down Payment | 10% ($45,000) | 3.5% ($15,750) |

| Base Loan Amount | $405,000 | $434,250 |

| Upfront Cost | $0 | $7,600 (UFMIP, usually financed) |

| Monthly Insurance | $195.75 (PMI) | $199.03 (Annual MIP) |

| Duration | Cancellable at 22% equity | Often for the life of the loan |

The key takeaway here is that while the monthly figures might be close, the FHA loan starts with a higher financed balance due to the UFMIP, and its monthly MIP payment is usually permanent. This is why it’s so critical to not just look at the monthly number, but to understand the full picture of what you’re paying over time.

Your Game Plan for Removing Mortgage Insurance

Think of mortgage insurance as a temporary cost, not a permanent part of your house payment. It's a stepping stone to homeownership, but the good news is you don't have to pay it forever. With the right strategy, you can get rid of this extra monthly expense and put that money toward something more important.

The path to ditching mortgage insurance depends almost entirely on the type of loan you have. Conventional loans with Private Mortgage Insurance (PMI) have several clear-cut exit ramps. On the other hand, government-backed FHA loans and their Mortgage Insurance Premium (MIP) have much stricter, longer-lasting rules.

Let’s break down the playbook for your specific loan.

Canceling PMI on Conventional Loans

For homeowners with a conventional loan, getting rid of PMI is a matter of "when," not "if." The key is building equity—the difference between your home's value and what you owe on the mortgage. You have three main ways to make this happen.

Request Cancellation: Under the Homeowners Protection Act, you have the right to ask your lender to remove PMI as soon as your mortgage balance hits 80% of your home's original value. This means you’ve paid down your loan enough to have 20% equity. You’ll need a solid payment history, and the lender may ask for a new appraisal to confirm your home’s current value hasn't dropped.

Automatic Termination: This one’s easy. Lenders are legally required to automatically cancel your PMI on the date your loan balance is scheduled to reach 78% of the original home value. This is when you have 22% equity, and it happens without you having to lift a finger, as long as your payments are current.

Refinance Your Mortgage: If your home's value has shot up or you've been aggressively paying down your loan, you might have more than 20% equity based on the new market value. Refinancing into a new loan can wipe out PMI entirely. Our team can run the numbers to see if this makes sense for you—learn more in our guide on how to refinance to remove PMI.

Dealing with MIP on FHA Loans

FHA loans are fantastic for getting your foot in the door with a small down payment, but their mortgage insurance rules are a different story. If you took out an FHA loan after June 2013 with a down payment of less than 10%, you’re stuck paying the annual MIP for the entire life of the loan.

The only way out is to sell the home or refinance into a conventional mortgage. Once you've built up at least 20% equity, refinancing becomes a powerful strategy to switch into a loan that has no mortgage insurance at all.

Your Equity Checklist: To get on the fast track to PMI removal, keep a close eye on your loan statements to watch your principal balance drop. It's also smart to monitor home values in your neighborhood. If you think your property's value has climbed significantly, investing in a home appraisal could be your ticket to canceling PMI sooner.

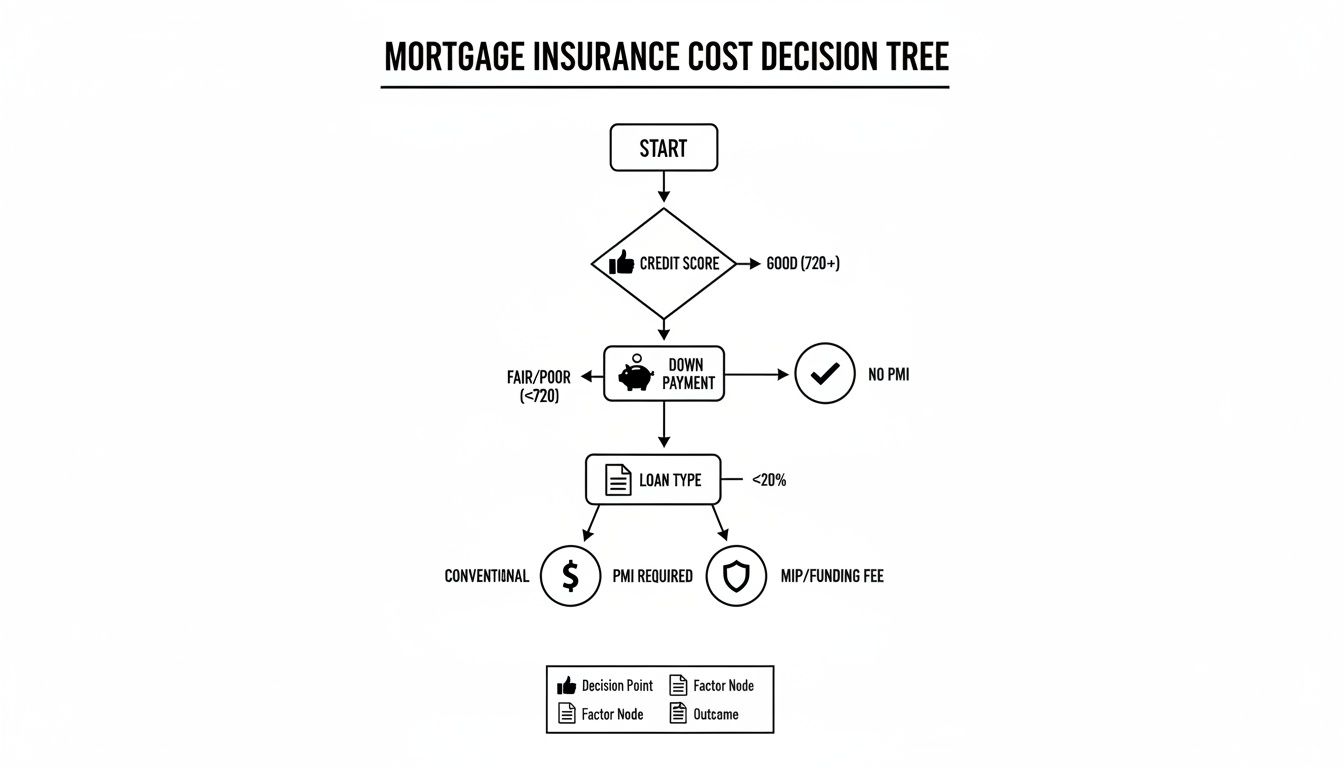

This decision tree gives you a great visual of how your finances shape your mortgage insurance costs from the start.

As the flowchart shows, things like your credit score and how much you put down are the biggest factors in determining what kind of mortgage insurance you'll have and how much it will cost.

The Power of Refinancing and Time

Ultimately, building equity is your core strategy, whether you do it through steady monthly payments or by letting the market boost your home's value. The good news is that most homeowners don't pay mortgage insurance for long.

Most policies are gone within 5-7 years as equity naturally builds. In fact, refinancing is such a common tool that it helped U.S. borrowers save an estimated $5.5 billion on mortgage insurance in 2024 alone. It’s just a matter of time and a solid plan.

How to Avoid Mortgage Insurance Entirely

While mortgage insurance is a fantastic tool that opens the door to homeownership for millions, the ideal scenario is to skip this extra monthly cost altogether. Think of it as a proactive strategy—one that saves you a serious amount of money over the life of your loan and keeps your monthly payment lower right from the start.

Most people know about making a big down payment, but that's not the only way. There are a few other clever financial moves and even specialized loan programs that can help you sidestep the expense. This isn't just about saving a few bucks; it's about smart planning and understanding all your options before signing on the dotted line.

The Classic Route: The 20 Percent Down Payment

The most straightforward way to avoid private mortgage insurance (PMI) on a conventional loan is to put down 20% of the home's purchase price. Simple as that. When you have at least 20% equity from day one, lenders don't view your loan as high-risk, so they waive the insurance requirement.

Hitting that 20% target takes discipline and a solid savings plan. Here are a few ways to get there faster:

- Make Saving Automatic: Set up recurring transfers from your checking to a high-yield savings account every payday. Out of sight, out of mind.

- Use Gift Funds: It’s common for family members to contribute gift funds toward a down payment. You just need to document it properly.

- Look for Down Payment Assistance: Check out state and local programs that offer grants or low-interest loans to help you bridge the gap.

The Piggyback Loan: A Strategic Alternative

What if you don't quite have 20% but are determined to avoid PMI? This is where a "piggyback loan," sometimes called an 80-10-10 loan, comes into play. It’s a smart strategy that involves splitting your financing into two loans instead of one.

Here’s how it breaks down:

- First Mortgage: You get a primary mortgage for 80% of the home's value.

- Second Mortgage: You take out a smaller, second loan (often a home equity line of credit, or HELOC) for 10% of the home's value.

- Your Down Payment: You pay the remaining 10% in cash.

Because your main loan is at that magic 80% loan-to-value ratio, you completely sidestep PMI. You will have two monthly payments to make, but the combined total can often be less than a single loan plus PMI. As a bonus, the interest on that second mortgage might even be tax-deductible.

This approach requires a strong credit score and a bit of math to ensure the combined payments are affordable and actually save you money. An expert at Mortgage Seven LLC can run the numbers and see if a piggyback loan is the right move for your situation.

Specialized Loan Programs That Skip Insurance

Beyond the usual strategies, some loan programs are specifically designed without a mortgage insurance requirement, even if you have a small (or no) down payment. These are often geared toward certain groups and can be a huge benefit if you qualify.

- VA Loans: Available to eligible veterans, active-duty service members, and surviving spouses, VA loans are hands-down one of the best mortgage options out there. They feature $0 down payment and no monthly mortgage insurance.

- Portfolio Loans: Some lenders, including many that Mortgage Seven LLC partners with, offer their own unique in-house "portfolio loans." Because these loans don't have to follow standard industry rules, some are designed to waive mortgage insurance for well-qualified borrowers, even with less than 20% down.

Exploring these less-common options really requires an expert guide. A great mortgage broker can help you navigate these niche programs and find one that fits your financial profile, potentially unlocking a path to homeownership with less cash and no extra insurance fees.

Your Top Mortgage Insurance Questions, Answered

Alright, let's tackle some of the most common questions that pop up about mortgage insurance. Even after you get the basics down, these specific details can be tricky. Here are some quick, straight-to-the-point answers to clear up any lingering confusion.

Is Mortgage Insurance Tax Deductible?

This is a real "it depends" situation, and the answer changes all the time. For a while, homeowners could deduct their mortgage insurance premiums, but tax laws are constantly in flux.

As of right now, that deduction has expired for most people. The key thing to remember is that tax codes get tweaked every year. Your best move is always to talk to a tax professional who can give you advice based on the current laws and your specific financial picture.

How Much Does My Credit Score Really Affect My Mortgage Insurance?

It’s a massive factor, especially for Private Mortgage Insurance (PMI) on conventional loans. Lenders live and breathe risk assessment, and your credit score is their number one tool.

A higher score tells them you're a low-risk borrower, and they'll reward you with a lower PMI rate. Think of it as getting a good-driver discount on your car insurance. While the impact isn't as direct with the MIP on an FHA loan, a great credit score always helps you land better loan terms overall.

What’s The Difference Between Mortgage Insurance And Homeowners Insurance?

This is a big one, and it's easy to get them mixed up. The simplest way to think about it is this: mortgage insurance protects the lender, while homeowners insurance protects you.

If you can't make your payments and the loan goes into default, mortgage insurance pays the bank. If a tree falls on your roof or someone gets hurt on your property, homeowners insurance covers your repair costs and liability. They serve two totally different purposes, but both are usually required.

For the clients we work with at Mortgage Seven LLC—like self-employed professionals using P&L loans or investors looking at jumbo refinancing—getting these details right is crucial. We find custom ways to ditch PMI early, whether it's through hitting 20% equity or finding a lender-paid option. This strategy alone can save you $10,000 or more over the life of the loan. You can dive deeper into these kinds of mortgage insurance insights from the Urban Institute.

Navigating these rules isn't something you should have to do alone, especially when your income or investment strategy is unique. A good broker knows how to find opportunities that a typical bank lender might overlook, building a plan that cuts out unnecessary costs and fits perfectly with your financial goals.

Ready to explore your mortgage options and find a loan that fits your financial goals? The expert team at Mortgage Seven LLC is here to guide you through every step, from understanding insurance requirements to securing the best possible terms. Schedule your free consultation today at https://mtg7.com.

Leave a Reply