When you're getting a mortgage, one of the first fees you'll encounter is the mortgage origination fee. So, what is it?

Think of it as the lender's fee for the service of creating your loan. It covers all the administrative and processing work needed to take your application from a pile of paperwork to an actual, funded mortgage.

Typically, this fee runs somewhere between 0.5% to 1% of your total loan amount. It’s a one-time charge you'll pay at closing.

Your Guide to Understanding the Mortgage Origination Fee

The price you see on a home listing is just the starting point. Closing costs are a whole other category of expenses, and the origination fee is often one of the biggest line items on that list. Many homebuyers see it on their documents but aren't totally sure what it's for.

At its core, the origination fee is how your lender gets paid for the work involved in setting up your loan. It’s not just about pushing a button; there’s a whole team and process working behind the scenes.

Mortgage Origination Fee At a Glance

To make it clearer, here’s a quick breakdown of what the mortgage origination fee really pays for.

| Component | What It Covers | Who Benefits |

|---|---|---|

| Loan Processing | Gathering your documents, running credit checks, and managing the application from start to finish. | The lender, for covering staff time and operational costs. |

| Underwriting | The in-depth financial review by an underwriter to assess risk and officially approve your loan. | The lender, as it ensures they are making a sound lending decision. |

| Document Preparation | Drafting, preparing, and managing all the necessary legal and closing documents for your loan. | Both you and the lender, ensuring the loan is legally compliant and secure. |

This table shows that the fee isn't just one thing but a bundle of services essential to making your home loan happen.

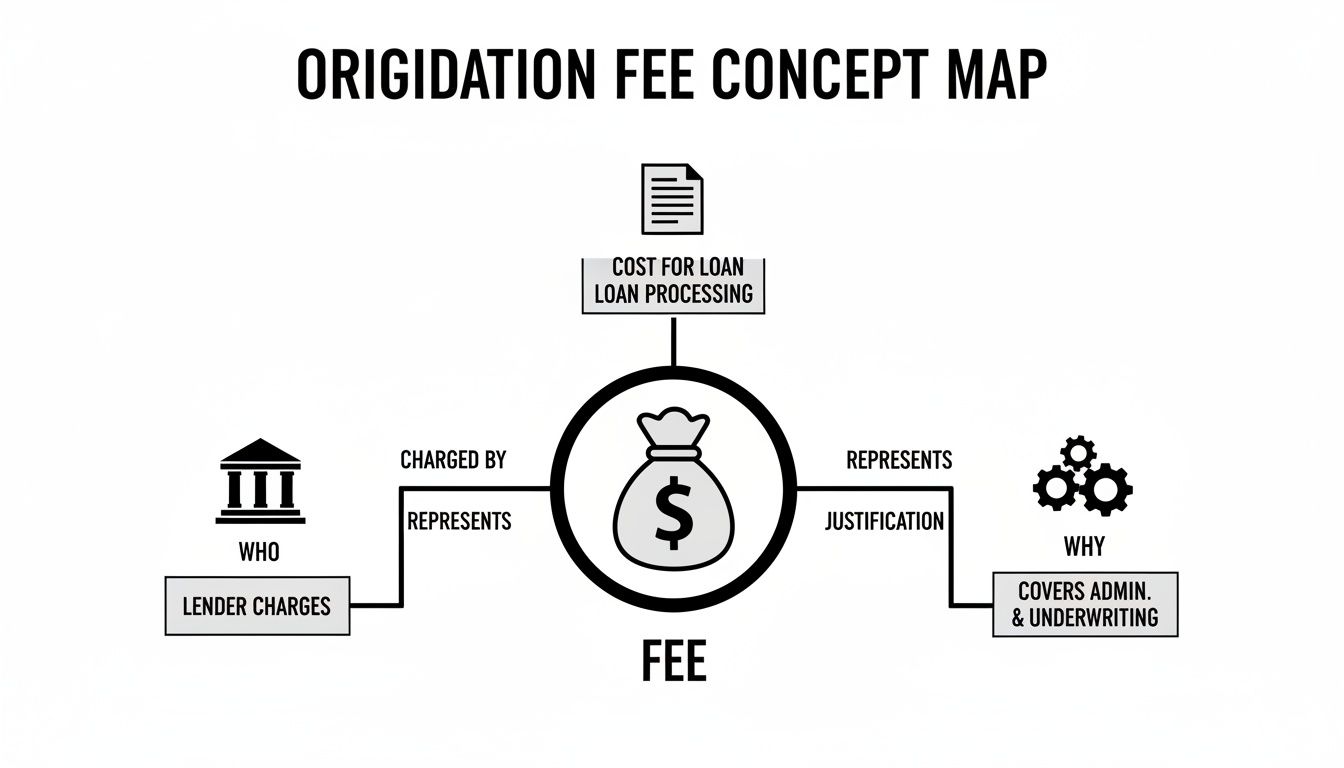

What This Fee Actually Covers

Let's dig a bit deeper into what you're paying for. This single fee usually combines several key services:

- Application Processing: This is the initial legwork—collecting your bank statements, tax returns, and pay stubs, then formally submitting your application into the lender's system.

- Underwriting: Here, a professional underwriter scrutinizes your entire financial profile. They verify everything to make sure you're a qualified borrower, which is the most critical step for getting final approval.

- Document Preparation: From the moment you apply until you sign the final papers, a mountain of legal documents is created. This fee covers the cost of preparing everything from your Loan Estimate to your Closing Disclosure.

This concept map helps visualize how these pieces fit together.

As you can see, the fee directly compensates the lender for the entire journey of creating your loan. Getting a handle on this is the first step toward becoming a more empowered borrower.

The Bottom Line: The origination fee isn’t an extra, tacked-on charge. It’s a standard cost in the mortgage world that pays for the expertise, time, and administrative systems needed to originate your loan correctly and legally.

Whether you're buying your first home or are a seasoned investor looking into a commercial real estate loan, understanding these fundamental costs is essential for navigating the financing maze.

How Lenders Calculate Your Origination Fee

So, how exactly does a lender land on the final number for your origination fee? Thankfully, it’s not some mysterious figure pulled out of thin air. The calculation is actually quite straightforward.

In almost every case, the origination fee is simply a percentage of your total loan amount. You’ll typically see this fee fall somewhere between 0.5% and 1% of the loan. While that might sound like a tiny fraction, on a home loan, it can easily add up to thousands of dollars.

The Standard Percentage-Based Model

The math here is simple multiplication. The lender takes the amount you're borrowing and applies their set percentage to figure out the fee.

Let's run the numbers with a couple of common scenarios:

Example 1: A $300,000 Loan

- With a 1% origination fee: $300,000 x 0.01 = $3,000.

- With a 0.5% origination fee: $300,000 x 0.005 = $1,500.

Example 2: A $500,000 Loan

- With a 1% origination fee: $500,000 x 0.01 = $5,000.

- With a 0.5% origination fee: $500,000 x 0.005 = $2,500.

As you can see, the fee grows right alongside your loan amount. A bigger loan generally means more work and more risk for the lender, and the origination fee reflects that. Want to see what your own costs might look like? Feel free to play around with the numbers on our mortgage calculators.

What Pushes the Percentage Up or Down?

Okay, so why isn't the percentage always the same across the board? A few key things can nudge that rate toward the lower or higher end of that typical 0.5% to 1% range.

Your credit score is a major driver. Think of it from the lender's perspective: a borrower with a stellar credit history is a lower risk. To win your business, a lender might offer a lower origination fee as a result of that confidence.

Other factors also come into play:

- The Complexity of Your Loan: A simple, conventional loan for your primary home is pretty standard. But if you’re self-employed or buying an investment property, the underwriting gets more complicated, and the fee might be a bit higher to compensate.

- The Lender's Business Model: Some lenders, especially the big online-only players, have lower overhead. They don't have to pay for brick-and-mortar branches, so they can sometimes pass those savings on to you with lower fees.

- Good Old-Fashioned Competition: When the market is hot and lenders are all competing for your business, they might lower their fees to make their offers more attractive.

This percentage model isn't a new trend, either. It’s been the industry standard for decades. For example, historical data shows that combined origination fees and discount points on a 30-year fixed-rate mortgage averaged around 0.9% in late 2022. This consistency just goes to show how baked into the process this calculation really is. If you're a data nerd, you can even dig into historical trends yourself on the St. Louis Fed's economic research site.

Why Lenders Charge This Upfront Fee

It’s easy to look at a mortgage origination fee on your loan estimate and just see another line item chipping away at your savings. But it's not just a random charge. It's the lender's way of covering the very real costs of putting your home loan together.

Think about it: the lender doesn't make a dime from your interest payments until after you've closed on the property. But weeks, sometimes months, of work happen before that closing day. The origination fee is how the lender gets paid for all that front-loaded effort.

Covering the Operational Nuts and Bolts

Creating a mortgage isn't a simple, one-person job. It takes a whole team and a lot of behind-the-scenes work. The origination fee you pay goes directly toward funding this machine.

Here's a quick breakdown of what it covers:

- Loan Officer Compensation: This is the salary or commission for the expert who helps you navigate the application and find the right loan program.

- Processor and Underwriter Salaries: These are the detail-oriented pros who verify all your paperwork, from bank statements to tax returns, and ultimately give the final approval.

- Administrative Overhead: This is the less glamorous but essential stuff—the rent for the office, the secure software that protects your financial data, and other day-to-day business costs.

If lenders didn't charge this fee, they'd have to find another way to cover these expenses. The most likely alternative? Baking those costs into a much higher interest rate for everyone.

The Cost of Doing Business in the Mortgage World

Originating a loan has gotten seriously expensive. In fact, the average cost for a lender to create a single mortgage hit around $11,600 in the third quarter of 2023. That’s a massive 35% jump in just three years, thanks to a tougher market and rising business expenses. If you're curious about the data, you can learn more about these origination cost trends in the full study.

In essence, the mortgage origination fee is the engine that powers the loan creation process. It ensures the lender has the resources to properly vet, approve, and finalize your mortgage, safeguarding both their investment and your path to homeownership.

Seeing the fee from this angle is important. It’s not a penalty; it’s a standard, transparent payment for the service of constructing your home loan from the ground up. Having this context is a huge help as you start looking at the steps involved in the mortgage approval process.

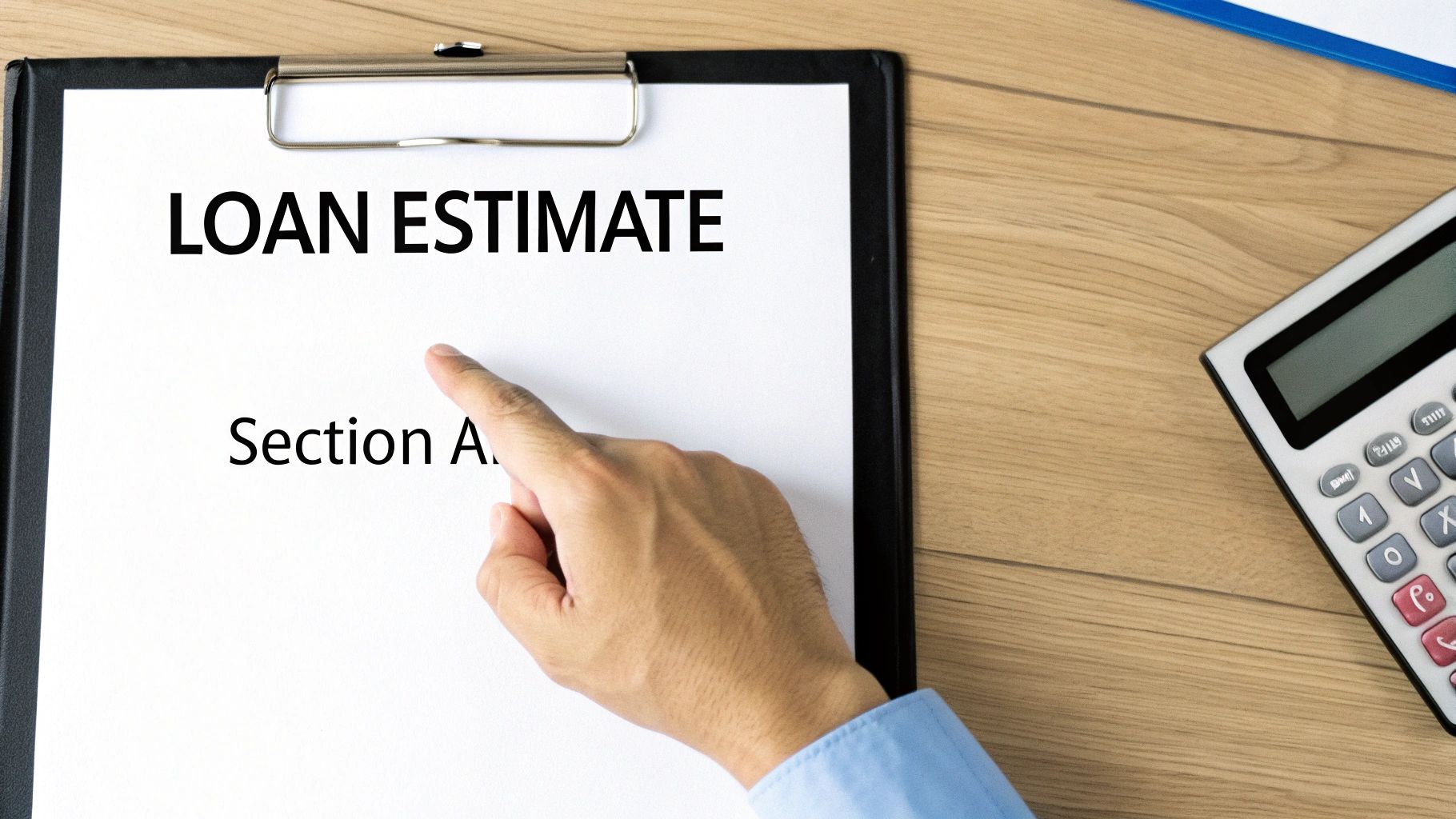

Navigating the mountain of paperwork that comes with a mortgage can feel a little overwhelming, but finding your origination fee is actually pretty straightforward. Lenders are required to be upfront about this cost, and it has a specific home on one of the most important documents you'll get: the Loan Estimate.

Once you have your Loan Estimate in hand, flip right to page two. You'll see a section called "Closing Cost Details," and within that, a line item labeled Box A: Origination Charges. This is exactly what you're looking for.

Breaking Down Box A

In this section, the lender breaks down exactly what they're charging to get your loan off the ground. You'll typically see the origination fee listed as a percentage of your total loan amount, along with the final dollar figure. No mystery, no hidden numbers—it’s all laid out for you.

Here’s a snapshot of a real Loan Estimate form with Box A highlighted so you know what to look for.

As you can see, the origination charge is clearly itemized, making it easy to spot among the other closing costs.

This document is your secret weapon when shopping for a loan. You can take the Loan Estimates from different lenders, put them side-by-side, and compare the numbers in Box A directly. A lower figure here means less cash you have to bring to the closing table.

Crucial Tip: Remember, the figure on your Loan Estimate is just that—an estimate. Before you sign on the dotted line, you'll get a final Closing Disclosure. The origination charge on that final document should match your Loan Estimate perfectly unless you've made a change to your loan, like locking in your interest rate.

Doing this final check is a critical step. It’s your best defense against last-minute surprises and ensures your lender has honored their initial offer. A quick comparison gives you the power to walk into your closing with total confidence.

How to Lower (or Even Eliminate) Your Origination Fee

Here’s a secret many homebuyers don’t realize: the mortgage origination fee isn't always set in stone. It's often negotiable. Lenders want your business, especially if you’re a strong applicant, which gives you more bargaining power than you might think.

Think of it like buying a car—the sticker price is rarely the final price. With the right strategy, you can chip away at that fee and keep more cash in your pocket at closing.

Come to the Table from a Position of Strength

The best negotiation tactic starts long before you ever speak to a loan officer. It begins with your financial health. Lenders see borrowers with high credit scores and low debt-to-income (DTI) ratios as less risky, and they’re willing to fight for that business.

So, what does that look like in practice? Work on paying down credit card balances and making every single payment on time. The difference between a 680 and a 740 credit score is huge in a lender's eyes. That jump alone can give you serious leverage to ask for a lower fee.

When you look like a top-tier applicant on paper, you're not just a borrower; you're a valuable customer. This simple shift in perception makes lenders much more willing to sweeten the deal to win you over, and that often includes trimming the origination fee.

Make Lenders Compete for Your Business

Never, ever take the first offer you get. Your most powerful tool is a competing offer from another lender. It’s absolutely essential to get a Loan Estimate from at least three different lenders.

Once you have those official documents, you can see exactly what each lender is charging. If your preferred lender has a higher origination fee, you can go back to them with proof and say, "I'd love to work with you, but can you match this competing offer?" This creates a competitive environment where you win.

Ask Your Broker to Go to Bat for You

This is one of the biggest advantages of working with a mortgage broker like Mortgage Seven. Instead of you having to do all the legwork, we do it for you. We have access to a huge network of lenders and can submit your application to dozens of them at once.

This process naturally finds the lenders offering the most competitive terms, including lower—or sometimes zero—origination fees. Plus, we can often use our established relationships to negotiate on your behalf and get a fee reduced even further.

Explore Different Ways to Pay the Fee

Finally, you can ask about different loan structures that change how the fee is paid. Some lenders offer what are called "no-closing-cost" mortgages. This sounds amazing, but it’s important to understand the trade-off.

The lender isn't just waiving the fee out of kindness. They typically roll the origination fee and other closing costs into your loan by giving you a slightly higher interest rate. This can be a great move if you're short on upfront cash, but it usually means you'll pay more in interest over the life of the loan.

To help you decide, here's a quick comparison of the different approaches.

Fee Reduction Strategies Compared

| Strategy | How It Works | Potential Trade-off |

|---|---|---|

| Direct Negotiation | You ask the lender to reduce or waive the fee, using your strong financials or a competing offer as leverage. | The lender might say no, or only offer a small reduction if your leverage isn't strong enough. |

| Pay a Higher Interest Rate | The lender agrees to cover the origination fee in exchange for you accepting a higher interest rate on your loan. | Your monthly payment will be higher, and you'll pay significantly more in total interest over the loan's term. |

| Use Seller Concessions | You negotiate for the seller to contribute a certain amount of money toward your closing costs. | The seller has to agree, and this may be difficult in a competitive seller's market. You may need to offer a higher purchase price to get it. |

| Work with a Broker | A broker shops your loan to multiple lenders to find one with naturally lower fees or negotiates for you. | There's no real trade-off here, as brokers are legally obligated to act in your best interest to find you the best deal available to them. |

Ultimately, the right strategy depends on your financial situation. Are you trying to minimize your upfront cash-to-close, or are you focused on getting the lowest possible monthly payment? Answering that question will help guide you toward the best option.

How Economic Trends Influence Origination Fees

Think of your mortgage origination fee as something that breathes with the economy. It’s not set in stone. Just like interest rates, it ebbs and flows with the broader housing market, which is why a quote you get today could look very different from one you might have received six months ago.

At its core, it all comes down to simple supply and demand. Every lender has fixed costs to keep the lights on—things like underwriter salaries, office space, and software. These bills have to be paid whether they’re closing a hundred loans or just ten.

The Impact of Loan Volume

When the economy is hot and everyone seems to be buying or refinancing, lenders are flooded with applications. With so much business coming in, they can spread their operating costs across a much larger number of loans. This high volume, combined with fierce competition for your business, often pushes origination fees down.

But what happens when the market cools off? Fewer people are applying for mortgages, but the lender's overhead stays the same. To stay profitable, they often have to charge a bit more on each loan they do close. It's a practical way to make sure their costs are covered with a smaller customer base.

A Look at Recent Market Swings

The last few years have been a perfect case study. U.S. mortgage origination volumes took a nosedive, dropping from a peak of $4.51 trillion in 2021 to just $1.50 trillion in 2023 when interest rates shot up. During a slowdown like that, lenders feel immense pressure to raise fees to cover their expenses.

As the market started to bounce back, reaching $512.15 billion in Q3 2024, that pressure began to ease, and competition could once again help lower those fees. If you're curious, you can dig into more of these mortgage market statistics on LendingTree.com.

Key Takeaway: Your origination fee isn't just a random percentage. It’s a living number influenced by market activity, competition, and the overall economy. This is why timing your application, if you have the flexibility, can make a real difference.

Once you see how these economic patterns work, you can better anticipate why fees might be higher or lower at any given time. This knowledge puts you in the driver's seat, empowering you to ask smarter questions and negotiate from a much stronger position.

Common Questions About Mortgage Origination Fees

As you get a handle on what is a mortgage origination fee, a few more specific questions usually pop up. Nailing down these details can clear up any lingering confusion and give you the confidence to compare loan offers like a pro.

Let's walk through some of the most common things borrowers ask.

Are Origination Fees and Discount Points the Same Thing?

Nope, they're two totally different things, even though you pay for both at the closing table.

Think of it this way: the origination fee is what you pay for the service of building your loan—all the paperwork, verification, and underwriting. Discount points, on the other hand, are basically prepaid interest. You're paying a little extra upfront to buy a lower interest rate for the entire life of your loan, which reduces your monthly payment.

Here’s the simple breakdown:

- Origination Fee: Pays the lender for the work they do to create your loan.

- Discount Points: An optional payment to secure a lower interest rate for long-term savings.

Can I Roll the Origination Fee into My Loan?

Yes, you can, and it's a pretty common move. Most lenders will let you finance the origination fee (and often other closing costs) by adding it to your total loan amount. The biggest plus here is needing less cash out-of-pocket to close on your home, which is a huge help when funds are tight.

But there's a trade-off to consider. When you finance the fee, your total loan balance goes up. That means you’ll be paying interest on that fee for the next 15 or 30 years, leading to a slightly higher monthly payment and more interest paid overall.

Are Mortgage Origination Fees Tax Deductible?

This is where things get a bit tricky. The short answer is, "it depends."

You generally can't just deduct the full origination fee in the year you buy your house. The IRS often treats these fees as part of the points you pay on the loan. That means you typically have to amortize them—deduct a small portion each year—over the entire term of your mortgage.

Important Note: Tax laws are complex and always subject to change. It's absolutely critical to talk to a qualified tax advisor about your specific financial situation. Never make tax decisions based on general advice you read online.

Do All Lenders Charge an Origination Fee?

Not every single one, but the vast majority do. You might see some lenders, especially online banks or credit unions, advertise "no origination fee" loans as a way to stand out.

While that sounds great on the surface, you have to look at the whole package. A lender who waives the origination fee often makes up for it by charging a slightly higher interest rate. The fee is still there, just baked into your rate instead of being a separate line item.

That's why you always need to compare the official Loan Estimate from each lender, not just a single fee.

For more answers to your mortgage questions, our comprehensive mortgage FAQ page has you covered.

Ready to navigate the mortgage process with a team that puts your questions first? At Mortgage Seven LLC, we provide clear, straightforward guidance from application to closing. Schedule your free consultation today!