The mortgage underwriting process is where the rubber really meets the road in your home loan application. It's the lender's official, in-depth analysis to make sure you're a good risk before they hand over hundreds of thousands of dollars. Think of it as a comprehensive financial health checkup.

What Does a Mortgage Underwriter Actually Do?

Imagine you’re asking a good friend to lend you a huge sum of money. Before they’d even consider it, they'd want to feel confident you could pay it back. They’d probably ask about your job, how much you have saved, and any other big debts you’re carrying.

A mortgage underwriter does the exact same thing, just on a professional level. Their job isn’t to be a gatekeeper but a risk analyst for the lender. They're the financial detectives who meticulously review your entire loan file—from your application all the way down to your bank statements—to verify everything checks out. This crucial step is what stands between your pre-approval and the final green light to close on your home.

The Four Pillars of Mortgage Underwriting

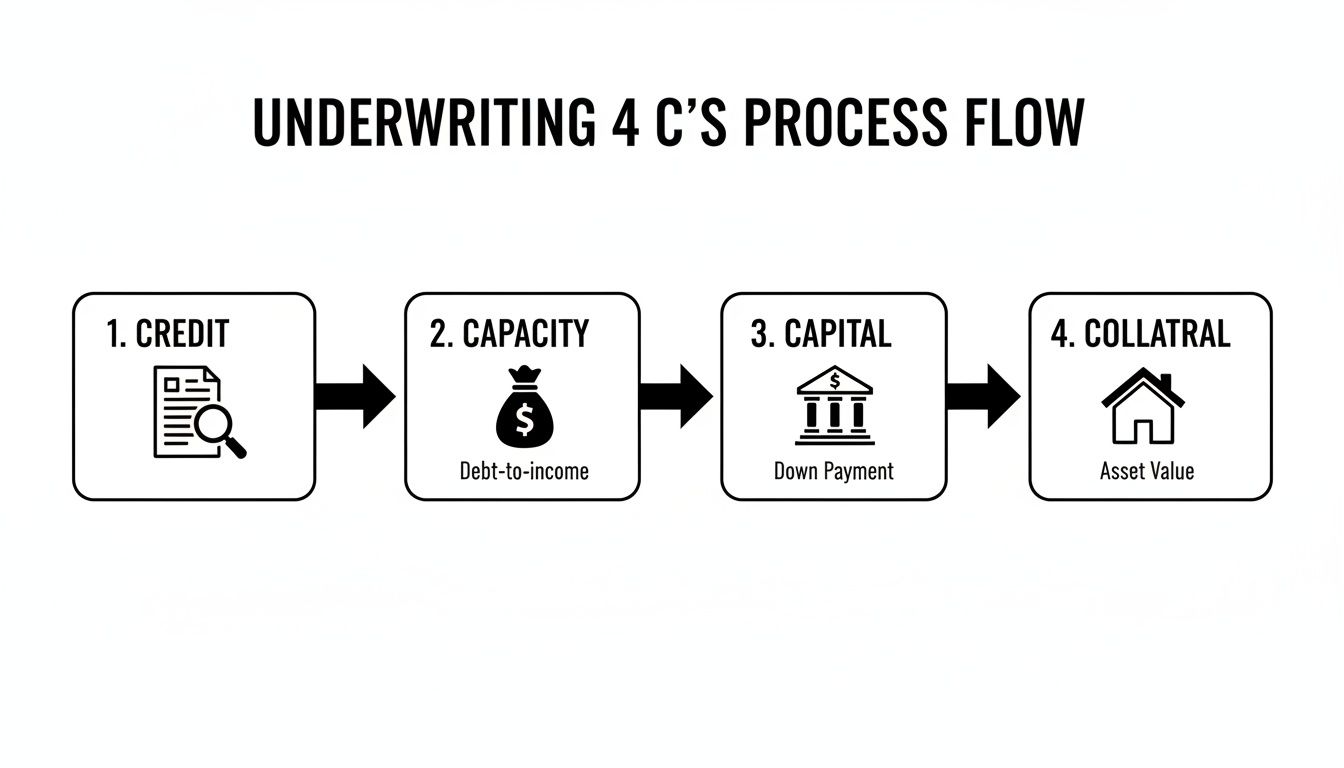

To make their decision, underwriters systematically evaluate your application against four core principles. You might hear them called the "Four C's," and knowing what they are is key to a stress-free process.

-

Credit: This is all about your track record with debt. The underwriter will pull your credit report to check your score, look for any late payments, and see how you've managed loans and credit cards in the past.

-

Capacity: This simply means your ability to actually afford the new mortgage payment each month. They’ll calculate your debt-to-income (DTI) ratio to ensure the loan payment won't overstretch your budget.

-

Capital: This refers to the cash and other liquid assets you have on hand. It proves you have enough money for the down payment and closing costs, plus some reserves left over for a rainy day.

-

Collateral: The property you're buying is the collateral for the loan. The underwriter needs to see an appraisal showing the home is worth enough to secure the amount you want to borrow.

For a deeper dive into the whole evaluation, this guide on What Is The Mortgage Underwriting Process is a fantastic resource.

Here’s a quick breakdown of how these four pillars come together.

The Four Pillars of Mortgage Underwriting

| Pillar | What It Means for You | What Underwriters Are Looking For |

|---|---|---|

| Credit | Your reliability as a borrower based on past behavior. | A strong credit score, a consistent history of on-time payments, and a manageable amount of existing debt. |

| Capacity | Your financial ability to handle monthly mortgage payments. | Stable, verifiable income that keeps your debt-to-income (DTI) ratio within acceptable lender limits. |

| Capital | The liquid assets you have for the transaction and beyond. | Sourced and seasoned funds for the down payment and closing costs, plus cash reserves for emergencies. |

| Collateral | The value and condition of the property you want to buy. | An independent appraisal report confirming the home's value is equal to or greater than the loan amount. |

Ultimately, a strong application will demonstrate that you’re a reliable borrower with the financial stability to own a home, and that the property itself is a sound investment for the lender.

The 4 Stages of Mortgage Underwriting

The underwriting process isn't one giant step; it's a series of checkpoints. Thinking of it this way helps demystify what can feel like a black box. Each stage has a clear purpose, moving your application from the "submitted" pile to the "approved" pile. It’s basically the lender’s quality control system, designed to answer one crucial question: is this a reasonable risk?

This whole evaluation has gotten incredibly detailed—and expensive for lenders. A recent Freddie Mac study found that the average cost to originate a mortgage hit around $11,600 in late 2023. That number is largely driven by the meticulous, hands-on work underwriting requires. Lenders are always looking for ways to make it more efficient, and you can dive deeper into the numbers in their full cost-to-originate study.

Stage 1: The Initial Application Review

Once your loan officer hands over your complete application and all your documents, it lands with an underwriter. This first pass is all about checking for completeness and consistency. The underwriter is making sure every document they need is there and that the story you've told adds up.

For example, does the income on your pay stubs match what you put on the application? Do your bank statements show enough cash for the down payment and closing costs you’ve planned for? A clean, well-organized file will sail through this stage. Any missing paperwork or glaring inconsistencies, however, will trigger an immediate request for more information, which is your first potential delay.

Stage 2: The Automated Underwriting System (AUS)

Next, your application gets its first big test: the Automated Underwriting System (AUS). This is sophisticated software that acts as a first-pass filter, using powerful algorithms to do a preliminary risk check. The big names in the game are Fannie Mae's Desktop Underwriter (DU) and Freddie Mac's Loan Product Advisor (LPA).

The AUS crunches the key numbers—credit score, debt-to-income ratio, loan-to-value, and cash reserves—and compares them against the lender's rulebook. In just a few minutes, it spits out a recommendation:

- Approve/Eligible: Great news! Your file checks all the basic boxes and looks like a strong candidate.

- Refer/Caution: The system flagged something that needs a human to look at more closely.

- Ineligible: Your application doesn't meet the minimum requirements for that specific loan program.

Getting an "Approve/Eligible" is a fantastic start, but it's not the final approval. It just means you're on the right track. And a "Refer" isn't a "no"—it’s simply the system saying, "A human expert needs to weigh in on this."

Stage 3: Manual Underwriting and The Four Cs

This is where a real person’s experience and judgment come into play. A manual review is essential for any file flagged by the AUS, but it's also standard procedure for anyone with a more complex financial picture, like business owners or real estate investors. The underwriter takes a deep dive, meticulously vetting your file against the "Four Cs."

These four pillars—Credit, Capacity, Capital, and Collateral—are the foundation of every lending decision.

The underwriter uses this framework to build a complete picture of your financial health and the property’s value.

They'll look beyond the raw numbers to understand the story behind them. Why was there a large, out-of-the-ordinary deposit last month? Can you explain that recent job change? Their goal is to connect the dots and build a solid, defensible case for approving your loan. Seeing how a mortgage broker packages these files for underwriters can make a huge difference, something we detail in our guide on Mortgage Seven's streamlined processes.

An underwriter's job isn't to find reasons to say "no." A good underwriter’s real purpose is to find and document the valid reasons to confidently say "yes" while still protecting the lender from bad risk.

Stage 4: Conditional Approval and Clear to Close

If the underwriter is confident in your file, they'll issue a conditional loan approval. This is a huge milestone. It means your loan is approved, provided you can satisfy a few final requests.

These final requests, or "conditions," are usually pretty straightforward. They might include things like:

- Your most recent pay stub to show you're still employed.

- An updated bank statement proving the funds for closing are still available.

- A copy of the homeowner's insurance policy for the new property.

- A signed letter explaining where a large cash gift came from.

Once you and your loan officer send over these last items, the underwriter gives everything one final look. If it all checks out, they issue the two best words in the mortgage world: "Clear to Close" (CTC). That’s the official green light that tells everyone it's time to schedule your closing and fund your loan.

Your Essential Document Checklist for Underwriting

If there's one secret to a smooth mortgage underwriting process, it's being prepared. Think of your application documents as the raw materials the underwriter uses to build a case for your loan. When you hand them a complete, well-organized file from the start, you make their job easier and show you're a serious, on-the-ball borrower.

The whole point is to answer every question before they even think to ask it. Being proactive doesn't just speed things up; it builds confidence. A file that’s easy to verify is a file that moves quickly toward that final approval.

Verifying Your Income and Employment

First and foremost, the underwriter needs to know you can afford the loan. They aren't just looking at what you earn today, but for proof of a stable, consistent income that will continue long-term. This is where your job history tells a crucial part of your story.

To prove you have the income to back up your application, you'll need:

- Recent Pay Stubs: Typically, the last 30 days' worth. These show your current gross pay, what's being deducted, and your year-to-date earnings.

- W-2 Forms: You'll need W-2s from the last one to two years. This gives the underwriter a clear look at your annual earnings history with each employer.

- Federal Tax Returns: Two years of complete, signed tax returns are standard practice. They are especially important if you're self-employed or have income from commissions, bonuses, or side hustles.

- Employment Verification: Don't be surprised when the underwriter contacts your employer. They will call to confirm your job title, start date, and salary directly.

All this paperwork simply serves as hard evidence that you can comfortably handle your new monthly mortgage payment.

Documenting Your Assets and Capital

Next up: showing you have the cash to close the deal. The underwriter will verify that you have enough money for your down payment, all the closing costs, and a little extra in reserves. Just as importantly, they'll want to see where that money came from.

Big, mysterious cash deposits are a huge red flag. They need to know your funds are legitimate and not just a hidden loan from someone else.

Your asset checklist will include:

- Bank Statements: Plan on providing at least two months of statements for all your checking and savings accounts. Be ready to write a quick note explaining any large deposits that aren't from your regular paycheck.

- Investment Account Statements: If you have a 401(k), IRA, brokerage account, or mutual funds, you'll need to provide recent statements to show you have additional assets.

- Gift Letter: Getting help with the down payment? If any of the money is a gift, the person giving it to you must sign a gift letter. This document confirms the money is truly a gift, not a loan that you have to pay back.

Many of these documents, like bank statements, arrive as PDFs. It’s interesting how underwriters extract key information from these files. If you’re curious about the tech side of this, there’s a practical guide to converting PDF documents to structured data that breaks it all down.

Proving Your Credit and Liabilities

Your credit history is essentially your financial report card. It tells the underwriter how you've handled debt in the past. They'll pull your full credit report, but you might need to provide a little more color on some of the details.

Have these ready just in case:

- Letters of Explanation (LOX): If you have any dings on your credit—like a late payment or a bunch of recent inquiries—you'll need to write a short, factual letter explaining what happened.

- Proof of Debt Payment: Have an old collection account or judgment on your record? You’ll need to provide proof that it has been paid in full.

Tackling these issues head-on can save you a lot of back-and-forth later. For a complete rundown of everything you might need, our team at Mortgage Seven LLC put together a detailed home loan application checklist to help you get organized.

The level of detail they go into can feel intense, but there's a good reason for it. Lenders are careful. In 2023, the CFPB reported that out of 7.7 million mortgage applications, lenders only approved and originated 4.4 million loans. That means underwriting standards filtered out roughly 43% of all applicants. This just goes to show how critical a well-prepared, solid application file truly is.

How to Sidestep Common Underwriting Pitfalls

Getting through the mortgage underwriting process without a hitch really boils down to one golden rule: don't rock the boat. Once your application is in, the underwriter is working to verify the financial picture you presented. Any sudden changes can throw up a red flag, leading to serious delays or even a flat-out denial.

It’s surprisingly easy to cause problems, even if you have a rock-solid application. The time between applying for your loan and closing the deal is a financial "quiet period." Knowing what underwriters are looking for—and what spooks them—is the best way to avoid any last-minute drama.

Avoid Major Financial Moves

The biggest tripwires are almost always sudden shifts in your income, assets, or debt. Think of your loan file as a snapshot in time. If you change anything in that picture, the underwriter has to stop, reassess everything, and start their work all over again.

Here are the top three financial moves to avoid at all costs:

- Changing Jobs: A new job might seem like great news, especially if it comes with a raise, but it introduces a huge question mark for an underwriter. They want to see stability. A recent job change makes it tough to prove your long-term income, particularly if you’re switching to a new industry or a commission-based role.

- Taking on New Debt: This is a classic deal-killer. Financing a new car, opening a store credit card for furniture, or co-signing a loan for a relative will immediately increase your debt-to-income (DTI) ratio. If that new payment pushes your DTI over the lender's threshold, your approval can vanish in an instant.

- Making Large, Undocumented Deposits: A mysterious $10,000 deposit landing in your bank account will bring the entire process to a screeching halt. Underwriters are legally required to trace the source of all large deposits to make sure it’s not a hidden loan that would affect your DTI.

Key Takeaway: Fight the urge to make any big financial decisions until the keys are in your hand. The goal is to keep your financial profile looking exactly as it did the day you applied.

Maintain Your Credit and Be Transparent

Your credit score isn't set in stone. Lenders will almost always do a "soft pull" of your credit right before closing to make sure nothing has changed. A last-minute drop in your score can put the entire loan in jeopardy.

Missing a payment on a credit card or car loan during this time is a huge mistake. Your best bet is to put all your bills on autopay so nothing falls through the cracks. If you want a deeper dive, our guide on strengthening your credit for a mortgage has some great, practical tips.

Beyond just keeping things steady, honesty is crucial. If you know a potential complication is on the horizon—like a family member gifting you money for the down payment or a year-end bonus coming through—tell your loan officer immediately. They can help you document it the right way from the very beginning, avoiding headaches later.

Simple Rules for a Smooth Closing

To keep your loan moving toward the finish line, just stick to these simple rules during the underwriting phase.

- Don't Move Money Around: Shuffling large sums between your checking and savings accounts creates a confusing paper trail that you'll have to explain, document by document.

- Continue Paying Bills on Time: Every single one. Late payments can ding your credit score and signal financial instability to the underwriter.

- Stay in Communication: When your loan officer or underwriter asks for something, get it to them ASAP. Slow responses are one of the most common reasons closings get delayed.

- Keep Saving: Don't drain your accounts for other purchases before closing. The underwriter has already verified you have certain cash reserves, and they expect that money to still be there.

By keeping these potential pitfalls in mind, you can navigate the process like a pro and show the underwriter you’re the kind of reliable, low-risk borrower they love to approve.

Getting Your Loan Approved: A Look Through the Underwriter's Eyes

Mortgage underwriting isn't a simple pass/fail test; it’s a detailed evaluation of your unique financial story. Think of an underwriter as a financial detective. Their job is to look at your application through a specific lens, one shaped entirely by your situation.

Whether you're stepping into your first home, running your own business, or expanding your real estate portfolio, the secret to a smooth approval is knowing what that lens looks like for you. A salaried employee's file is pretty straightforward, but a self-employed applicant needs to tell a completely different kind of financial story. If you can anticipate the questions the underwriter will ask, you can have the right answers ready from the start.

For the First-Time Homebuyer

If this is your first time buying a home, underwriters are really looking for one thing: stability. They want to see solid proof that you understand the financial weight of homeownership and are ready for it. This means they'll zero in on your savings habits, your credit history, and where your down payment is coming from.

Are you getting a little help with the down payment? That's common, but you need the right paperwork to back it up.

- Gift Funds: If a family member is giving you money, you’ll need a signed gift letter from them. This is a simple document stating the money is a true gift, not a loan that has to be paid back.

- Assistance Programs: If you’re using a down payment assistance program, have all the official approval documents ready. The underwriter has to verify the program’s terms and make sure they align with the lender's rules.

Your main goal here is to show you’re a reliable borrower who has done their homework. A clean, organized file makes it incredibly easy for an underwriter to check off all the boxes and stamp their approval.

For the Self-Employed Borrower

When you work for yourself, verifying your income is the star of the show. Unlike a W-2 employee with a predictable paycheck, your income probably has its ups and downs. The underwriter's task is to find a stable, reliable average income they can count on for the future. This is where your record-keeping becomes your greatest asset.

While traditional tax returns are the go-to, many lenders now offer smarter options built for entrepreneurs:

- Bank Statement Loans: With these, underwriters analyze 12 or 24 months of your business bank statements. They look at deposits to figure out your average monthly revenue and calculate a qualifying income from there.

- Profit & Loss (P&L) Loans: You can also provide a P&L statement, usually prepared by a CPA, to show your business's profitability and document your personal income.

The good news is that technology is making this much faster. According to a 2023 study on AI adoption by Fannie Mae, 73% of lenders cited operational efficiency as their top reason for embracing new tech. Modern tools can now analyze bank statements or a P&L in days instead of weeks, which is a game-changer for self-employed borrowers.

Pro Tip for the Self-Employed: Keep your business and personal finances completely separate. Mixing them creates a messy paper trail that’s tough for an underwriter to follow, almost guaranteeing delays and a long list of questions.

For the Real Estate Investor

As an investor, the underwriting focus pivots. Your personal finances are still part of the equation, of course, but the property itself takes center stage. The big question the underwriter needs to answer is: can this property generate enough income to pay for itself, including the new mortgage?

This is where specialized loan products really shine.

A Debt Service Coverage Ratio (DSCR) loan is a favorite among investors. With a DSCR loan, the approval is based almost entirely on the property’s cash flow, not your personal debt-to-income ratio. The underwriter simply divides the property's net operating income by its total debt service (the mortgage payment). As long as that ratio is above 1.0, the property is bringing in more than it costs.

To get ready, you'll need to have a few things handy:

- A detailed lease agreement if the property is currently rented.

- A market rent analysis from the appraiser if it's vacant.

- A clear summary of your experience as a landlord, if you have any.

For an investor, the process isn't about proving you can afford the property. It's about proving the property can afford itself.

Why a Mortgage Broker Is Your Best Ally in Underwriting

Trying to get through mortgage underwriting on your own can feel like you're trying to crack a safe in the dark. Every part of your financial history gets put under a microscope, and one wrong move or missing document can bring the whole process to a screeching halt. While you can go it alone, having an expert mortgage broker from a firm like Mortgage Seven LLC in your corner changes the game completely.

A good broker is more than just a go-between; they're your strategist. They live and breathe this stuff every day, so they know exactly how underwriters think and what they look for. Long before your application ever lands on an underwriter's desk, your broker is already working to package your file to tell your financial story in the best possible light. They can spot potential red flags from a mile away and help you get ahead of them.

Your Advocate for Navigating Lender Conditions

When the underwriter comes back with a "conditional approval," it's often followed by a list of conditions—requests for more documents or explanations. This is where a broker really shines.

Instead of you trying to figure out what a vague request for a "letter of explanation" actually means, your broker knows precisely what the underwriter needs. They’ll help you draft a clear, concise response that checks all the boxes, preventing the frustrating back-and-forth that can delay your closing.

Think of them as the project manager for one of the biggest purchases you'll ever make. They handle the nitty-gritty details so you can stay focused on the exciting part—getting the keys to your new home.

The greatest advantage of a mortgage broker isn't just their expertise; it's their access. A single bank has one set of rules. A broker has a network of dozens of lenders, each with different guidelines and risk appetites.

Matching You with the Right Lender

This network is a broker's secret weapon. Let's say you're self-employed and need a bank statement loan, or maybe you're an investor looking for a DSCR program. Your local bank might not even offer those. A broker, however, knows exactly which lenders specialize in your specific scenario.

They won't waste your time submitting your loan to a lender who is almost guaranteed to say no. They play matchmaker, connecting your financial profile to the lender whose guidelines give you the highest chance of success.

By finding the right fit from the very beginning, a broker massively improves your odds of a smooth approval. They essentially pre-empt the denials by steering you down the path of least resistance, giving your application the best shot at a quick and painless "yes."

Your Top Underwriting Questions, Answered

Even after laying out the whole process, we know underwriting can feel like a bit of a black box. It’s that final, mysterious hurdle before you get the keys. Let’s clear up some of the most common questions we hear from borrowers, so you can head toward closing with confidence.

Knowing what to expect can make all the difference, turning anxiety into anticipation.

How Long Does Mortgage Underwriting Actually Take?

This is the million-dollar question, and the honest answer is: it depends. The timeline for underwriting isn't one-size-fits-all. If you have a straightforward file—say, you're a W-2 employee with great credit and a simple financial picture—your application might fly through an automated system in as little as 72 hours.

However, for more complex situations, like if you're self-employed or have unique income sources, underwriters will need to do a much deeper manual review. In those cases, you should realistically budget for one to three weeks. The final timing also hinges on the lender's current volume and, just as importantly, how quickly you can get them any extra documents they ask for.

What Does "Conditional Loan Approval" Mean?

Getting a conditional loan approval is fantastic news! It’s a huge step forward and a clear signal that you're on the home stretch. Essentially, it means the underwriter has given your file a thumbs-up, but they just need you to tie up a few loose ends before making it official.

Think of it as the underwriter handing you a short to-do list to cross the finish line. These final requests, or "conditions," are usually straightforward:

- Sending over your most recent pay stub to show you’re still employed.

- Writing a quick letter of explanation for a large deposit that wasn't from your paycheck.

- Providing proof that you have a homeowners insurance policy lined up for the new house.

Once you check off every item on their list, your loan moves to the final stage: clear to close.

A conditional approval is the underwriter's way of saying, "We're almost there. Just give us these last few pieces of the puzzle, and we can get this done."

Can a Loan Get Denied After I’ve Been Pre-Approved?

Yes, it absolutely can. This is a crucial point that catches many homebuyers by surprise. A pre-approval is a great start, but it's based on a preliminary look at your finances. Underwriting is the deep-dive, the fine-tooth-comb investigation where issues can surface.

So, why would a loan get denied at this stage? The most common reasons are things that happen after pre-approval: a sudden drop in your credit score, opening a new line of credit (like buying a car!), a change in your job, or if the underwriter can't fully verify your income or assets. It can also happen if the home appraisal comes in well below the agreed-upon price. That’s why it is so critical to keep your financial life as stable and unchanged as possible from the moment you apply until you have the keys in your hand.

Navigating the finer points of underwriting is much less stressful when you have a pro in your corner. At Mortgage Seven LLC, we’re your advocate, making sure your application is rock-solid and positioned for success. Schedule your free consultation today and let our team guide you to a smooth and successful closing.