Private Mortgage Insurance, or PMI, is a type of insurance policy that lenders require on conventional home loans if your down payment is less than 20% of the house's price. At its core, PMI is a safety net—but it's for your lender, not for you. It's the tool that makes it possible for you to buy a home with less cash upfront.

Decoding Private Mortgage Insurance in Simple Terms

If you've ever felt overwhelmed by mortgage jargon, you're in good company. Terms like "PMI" can sound complex, but the idea behind it is actually pretty simple.

Think of it from the lender's perspective. When a borrower puts down less than 20%, the lender is taking on more risk. If something goes wrong and the borrower can't make their payments, the lender stands to lose more money. PMI is there to protect the lender from that potential loss.

This insurance premium is usually added right into your monthly mortgage payment, so while it's a noticeable extra cost, it’s also conveniently bundled.

So, Why Does PMI Even Exist?

The main purpose of Private Mortgage Insurance is to open the door to homeownership for millions of people who might otherwise be locked out. Without it, lenders would be far less likely to approve loans for buyers who haven't saved up a massive 20% down payment.

By paying for PMI, you're basically covering the lender for taking on that extra risk. This allows them to say "yes" to loans with down payments as low as 3-5%, letting you get into a home much sooner.

PMI isn’t a penalty; it’s a tool. It bridges the gap between the down payment you have and the one lenders traditionally require, making homeownership accessible to a wider range of buyers.

It's a very common part of the homebuying journey, especially for first-time buyers. It's also crucial to know that PMI for conventional loans is different from the insurance on government-backed mortgages. For instance, you can learn more about the specifics of FHA loan insurance requirements to see how they compare.

To give you a quick cheat sheet on PMI, here's a simple breakdown of the key points.

PMI at a Glance

| Key Aspect | Simple Explanation |

|---|---|

| What It Is | An insurance policy that protects your lender, not you. |

| When It's Required | On conventional loans with a down payment under 20%. |

| Who It Protects | The lender, in case you default on the loan. |

| Is It Permanent? | No, it's temporary and can be removed later. |

| How You Pay | Usually as part of your monthly mortgage payment. |

Ultimately, understanding PMI is the first step toward managing it. It’s not a forever cost—it’s just a temporary expense on your path to building equity and securing your dream home.

Why Lenders Require PMI and How It Works

To get a real handle on private mortgage insurance, it helps to step into a lender’s shoes for a moment. When they look at a mortgage application, they’re essentially sizing up risk. The biggest piece of that puzzle is your down payment, which they use to calculate something called the loan-to-value (LTV) ratio.

LTV is just a fancy way of comparing the loan amount to the home's price. Let's say you want to buy a $400,000 house and you have $40,000 for a down payment (10%). That means your loan will be $360,000, and your LTV is 90% ($360,000 ÷ $400,000). From a lender's perspective, a higher LTV means higher risk.

Why? Because a borrower with less of their own cash invested—less "skin in the game," so to speak—is seen as more likely to default if financial troubles pop up. This is exactly where PMI enters the picture.

The Lender's Safety Net

Think of PMI as an insurance policy that protects the lender, not you. If you can't make your payments and the home ends up in foreclosure, the PMI policy pays the lender to cover a chunk of their losses.

Without this protection, lenders would be extremely hesitant to approve loans with less than the classic 20% down payment. PMI is the tool that gives them the confidence to say "yes" to a much wider range of buyers. It effectively bridges the gap between what you've saved and the lender's comfort level with risk. The way lenders handle these requirements is also evolving, with many using AI mortgage platforms to manage the loan process more efficiently.

Key Takeaway: PMI isn't a penalty for having a small down payment. It's an insurance premium you pay that allows the lender to take on the extra risk of a low-down-payment loan, ultimately making homeownership accessible to millions more people.

This system is a huge part of how housing finance works in the U.S. In a single recent year, private mortgage insurance backed almost $300 billion in mortgages, helping over 800,000 families buy a home. About 65% of those were first-time homebuyers. Since its inception in 1957, private MI has helped nearly 40 million households achieve homeownership, proving just how critical it is.

How PMI Gets Added to Your Loan

You don’t have to go out and shop for a PMI policy. When you get approved for a conventional loan with less than 20% down, your lender handles everything. They set up the policy with a private insurance company on your behalf.

Here’s a quick rundown of how it works in practice:

- The cost is figured out as a small percentage of your total loan amount.

- This premium is then rolled into your single monthly mortgage payment.

- You'll see it clearly listed as a separate line item on your official loan documents.

This makes paying for it simple, but it’s still crucial to know exactly what that number is and how it impacts your budget. Getting familiar with different conventional loan options can also give you a better feel for how PMI fits into the overall picture.

How Your PMI Costs Are Calculated

So, what does PMI actually cost? The honest answer is: it depends. There’s no flat fee. Lenders and their insurance partners look at your specific situation to figure out your premium, which is always a percentage of your total loan amount.

It's a lot like car insurance. A driver with a clean record and a safe car gets a better rate than someone with a history of accidents. In the mortgage world, the lender is assessing how risky your loan is. The less risk they see, the less you'll pay in PMI each month. It’s that simple.

Key Factors Influencing Your PMI Rate

When a lender calculates your PMI rate, they’re essentially looking at your financial snapshot to gauge risk. A few key pieces of that picture matter more than others.

- Your Credit Score: This is the big one. A high credit score is proof of your track record with debt, telling the lender you're a reliable borrower. That reliability earns you a lower PMI payment.

- Down Payment Size: While any down payment under 20% triggers PMI, there's a big difference between putting down 5% versus 15%. A larger down payment lowers your loan-to-value (LTV) ratio, which directly reduces your premium.

- Loan Amount: Since your PMI rate is a percentage, the total size of your loan naturally plays a role. The same rate on a larger loan will result in a higher dollar amount paid each month.

- Loan Type: The kind of mortgage you have matters, too. Lenders often view fixed-rate and adjustable-rate mortgages differently when it comes to risk, and that can be reflected in your PMI cost.

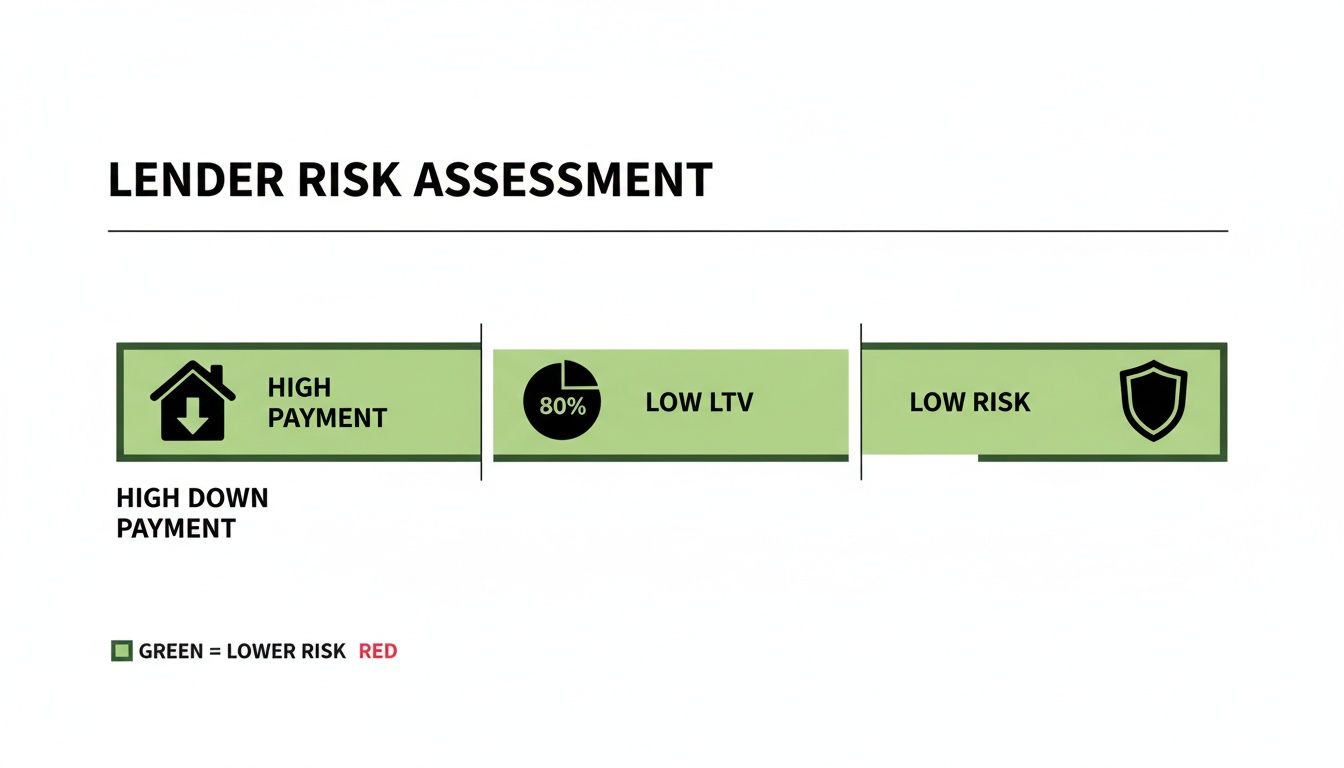

This image really drives home how a bigger down payment reduces the lender's risk.

As you can see, the less you have to borrow compared to the home's value (a lower LTV), the safer the loan looks in the lender's eyes.

How You Pay For PMI

You've got a few different ways to handle the payments, though one is far more common than the others.

- Borrower-Paid Monthly Premium: This is the classic approach. The annual cost is simply broken down into 12 installments and added to your monthly mortgage payment.

- Single Upfront Premium: You also have the option to pay for the entire PMI policy in one go at closing. This means higher upfront costs but frees you from that extra monthly charge.

- Split Premium: This is a hybrid model. You pay a portion of the premium at closing and the rest is spread out over your monthly payments, which will be smaller than with the standard monthly option.

Curious how these different options could impact your budget? You can play around with the numbers and see what works for you by using our mortgage calculators.

The Bottom Line: Your PMI cost isn't set in stone. Things you do—like boosting your credit score or saving for a slightly larger down payment—give you real control over how much you'll end up paying.

To see just how much of a difference this can make, let's look at how your credit score alone can dramatically change the numbers.

The Impact of Credit Score on PMI

Your FICO score has a massive effect on your PMI premium. To put it in perspective, we've put together a quick example.

Estimated Annual PMI Cost by Credit Score (Example)

This table illustrates how a borrower's FICO score can significantly affect their PMI premium on a $350,000 loan with a 5% down payment.

| Credit Score Range | Typical PMI Rate | Estimated Monthly PMI | Estimated Annual PMI |

|---|---|---|---|

| 760+ (Excellent) | 0.41% | $120 | $1,440 |

| 700-759 (Good) | 0.61% | $178 | $2,135 |

| 660-699 (Fair) | 0.96% | $280 | $3,360 |

| 620-659 (Poor) | 1.41% | $411 | $4,935 |

The difference is staggering. A borrower with an excellent credit score in this scenario could save over $3,000 a year compared to a borrower with a lower score. That's a real financial impact that shows just how much your credit history matters.

A Homeowner's Guide to Removing PMI

Paying for private mortgage insurance isn't a life sentence for your loan. Think of it as a temporary cost that you can—and should—get rid of as soon as you're able. Federal law provides clear pathways to shed this extra expense once you've built enough equity in your home. The key is simply knowing when and how to make your move.

There are two main ways to cancel PMI: you can request it yourself, or your lender will eventually have to do it for you automatically. Knowing how both options work puts you in the driver's seat.

Requesting PMI Cancellation Yourself

The Homeowners Protection Act (HPA) is the law that works in your favor here. This act gives you the right to formally ask your lender to drop PMI once your mortgage balance falls to 80% of your home’s original value. What’s "original value"? It’s simply the purchase price or the appraised value from when you first bought the home, whichever was lower.

To get the ball rolling, you’ll need to meet a few simple conditions:

- Make a Written Request: You have to start the process officially by sending a cancellation request to your lender in writing.

- Have a Good Payment History: Your lender will want to see that you're current on your payments and have a strong track record of paying on time.

- No Other Liens: Generally, you can't have other loans, like a home equity line of credit or a second mortgage, on the property.

Now, what if your home's value has shot up because of a hot market or some major renovations you've done? You might hit that 20% equity mark much sooner than your payment schedule would suggest. In this scenario, you can ask your lender to cancel PMI based on your home's current value, but be prepared—you'll almost certainly have to pay for a new appraisal to prove it.

By proactively monitoring your equity and your local market, you can often speed up the PMI cancellation process. This simple step could save you thousands of dollars over the life of your loan.

Automatic PMI Termination

If you forget to request cancellation or just never get around to it, don't worry. The HPA has a safety net built right in.

Your lender is legally required to automatically terminate your PMI on the date your principal balance is scheduled to reach 78% of your home's original value.

This automatic cancellation is a crucial protection for homeowners. As long as you keep up with your payments, it will happen without you having to lift a finger. It guarantees a finish line for those PMI payments, ensuring you don't overpay by a single dime.

Smart Strategies to Avoid PMI From the Start

While getting rid of PMI down the road is a fantastic feeling, avoiding it entirely from the beginning is even better. For homebuyers aiming to sidestep this extra monthly cost right out of the gate, there are a few powerful strategies you can use.

The most obvious path, of course, is saving up for a 20% down payment. It’s the classic approach that completely sidesteps the need for PMI on a conventional loan. But let's be realistic—in today's housing market, that can feel like a monumental task. Thankfully, it's not the only way.

Use a Piggyback Loan

One popular strategy is the "piggyback" loan, which you'll often see structured as an 80-10-10 loan. It sounds a bit complicated, but the idea is simple: instead of taking out one massive mortgage, you split your financing into two separate loans.

Here’s a quick look at how it works:

- 80% of the home's price is covered by your main mortgage.

- 10% is covered by a second, smaller loan that "piggybacks" on the first one.

- 10% comes from you as a cash down payment.

Because your primary mortgage has an 80% loan-to-value ratio, you completely avoid the PMI trigger. You will have two monthly loan payments to manage, but the combined total is often less than a single mortgage payment plus a hefty PMI premium.

Consider Lender-Paid Mortgage Insurance

Another route to explore is lender-paid mortgage insurance (LPMI). With this setup, the lender pays for the insurance policy on your behalf, so you don't have a separate PMI line item on your monthly statement. The catch? You pay a slightly higher interest rate on your mortgage for the life of the loan.

This trade-off can make sense if you don't plan on staying in the home long-term, as your total out-of-pocket costs over a few years might be lower. The big thing to remember is that, unlike standard PMI, LPMI can't be canceled once you reach 20% equity. That higher interest rate is locked in unless you refinance.

Important Note: Don't let the name fool you—LPMI isn't free. You're simply paying for it in a different way, through a permanently higher interest rate. Always run the numbers and compare the total cost of an LPMI loan versus a loan with traditional PMI to see which is the better deal for your specific situation.

Explore Government-Backed Loan Programs

Finally, don't overlook government-backed loans that offer a direct path to avoiding PMI. The best example is the VA loan, a benefit available to eligible veterans, active-duty service members, and surviving spouses. These loans are a game-changer because they typically require no down payment and have no monthly mortgage insurance.

With the private mortgage insurance market projected to grow to $9.71 billion by 2029, it’s clear that low-down-payment options are here to stay. You can learn more about the PMI market's expansion to understand its industry impact. Knowing how to navigate these PMI avoidance strategies gives you a serious advantage.

By exploring all your alternatives, you can find a path to homeownership that not only fits your budget but also potentially saves you thousands over the life of your loan.

Your Top PMI Questions, Answered

Once you get the hang of what PMI is, a whole new set of questions usually pops up. That's completely normal. Think of this as the next level of understanding—where we tackle the specific situations you're likely to run into.

Let's dive into some of the most common questions we hear from homebuyers and homeowners just like you.

Is PMI the Same as FHA Mortgage Insurance?

This is a big one, and the short answer is no, they're not the same, even though they do a similar job.

Private Mortgage Insurance (PMI) is what you'll find on conventional loans—the ones that aren't backed by the government. On the other hand, Mortgage Insurance Premium (MIP) is the version required for FHA loans.

The most important difference? How long you're stuck paying for it. You can eventually cancel conventional PMI once you've built up enough equity in your home. But with FHA MIP, if you put down less than 10%, you could be paying it for the entire life of the loan. That's a huge distinction.

Are My PMI Payments Tax Deductible?

Ah, the million-dollar question. The tax deductibility of mortgage insurance premiums is something homeowners always want to know about, and for good reason—it could lower your tax bill.

Historically, Congress has allowed homeowners to deduct their PMI payments, but this tax break isn't permanent. It often expires and then gets renewed, sometimes retroactively. So, what was deductible one year might not be the next.

Expert Tip: Don't assume you can write off your PMI. Tax laws are always in flux. Your best bet is to talk to a qualified tax advisor or check the latest IRS guidelines to see if the deduction is available for the current tax year.

Can I Refinance My Mortgage to Get Rid of PMI?

Absolutely. In fact, refinancing is one of the most popular ways to ditch PMI for good.

Here’s how it works: If your home's value has shot up—thanks to a hot market or some smart renovations—you might find that your loan-to-value (LTV) ratio is now below 80%. Refinancing into a new loan at that point means you won't need PMI anymore.

But before you jump in, you need to do the math. Refinancing isn't free.

- Closing Costs: You'll have to pay for things like appraisals, title fees, and origination fees, which can add up quickly.

- New Interest Rate: Make sure you’re getting a new interest rate that actually helps your financial situation.

- Break-Even Point: Figure out how many months it will take for your savings (from dropping PMI and maybe a lower rate) to cover the upfront closing costs.

This strategy is a home run when you can get rid of your PMI and lock in a lower interest rate at the same time.

What Happens if I Miss a Mortgage Payment That Includes PMI?

Your PMI premium isn't a separate bill you pay. It’s rolled right into your single monthly mortgage payment. So, if you miss a payment, the consequences are the same whether you have PMI or not.

You’ll likely get hit with a late fee from your lender, and it can ding your credit score. Remember, PMI protects the lender in case you default—it offers zero protection for you if you fall behind on payments. It's critical to make that full payment on time, every single month.

At Mortgage Seven LLC, we believe that understanding every aspect of your mortgage is the key to financial confidence. Whether you're trying to avoid PMI from the start or looking for the right time to remove it, our team is here to provide the clear, personalized guidance you need.

Ready to explore your options? Schedule your consultation with a Mortgage Seven LLC expert today and take the next step toward a smarter home loan.