Refinancing your mortgage isn't just about chasing a low number; it's a strategic financial decision. At its core, it makes sense when you can lower your interest rate, shorten your loan term, or tap into your home's equity to achieve other life goals. If the long-term savings or immediate benefits outweigh the upfront costs, you've likely found a smart move.

Seven Signals It's Time to Refinance Your Mortgage

Trying to decide when to pull the trigger on a refinance can feel a lot like timing the stock market. But it doesn’t have to be a guessing game. Instead of trying to predict the future, you can look for clear, actionable signals that tell you the conditions are right for your situation. These are the "refinance triggers" that take the guesswork out of the equation.

Think of your current mortgage like an old cell phone plan. It worked great when you got it, but now there are better deals out there. Refinancing is simply swapping that outdated plan for a new one that fits your current financial life and the current economic climate much better.

Key Refinancing Triggers to Watch For

The most obvious signal is a drop in market interest rates. You’ve probably heard the old rule of thumb—the “1% rule”—which suggests refinancing if you can lower your rate by at least one full percentage point. It’s a decent starting point, but even a smaller reduction can save you a surprising amount of cash over the life of your loan.

For example, say you locked in your mortgage at 7.5% a few years ago. If rates suddenly dip to around 6.79%, that's the kind of trigger that gets homeowners moving. On a $400,000 loan, that drop could slash your monthly payment by over $150. That’s a no-brainer if you plan to stay in the home long enough to recoup the closing costs. In fact, under similar conditions, one recent report showed that refinance activity surged 63% year-over-year. You can find more details in Milliman's mortgage market report.

Another powerful indicator is your home equity. As you make payments and your property value appreciates, that equity grows into a powerful financial tool. A refinance can let you put that leverage to work for you in several strategic ways.

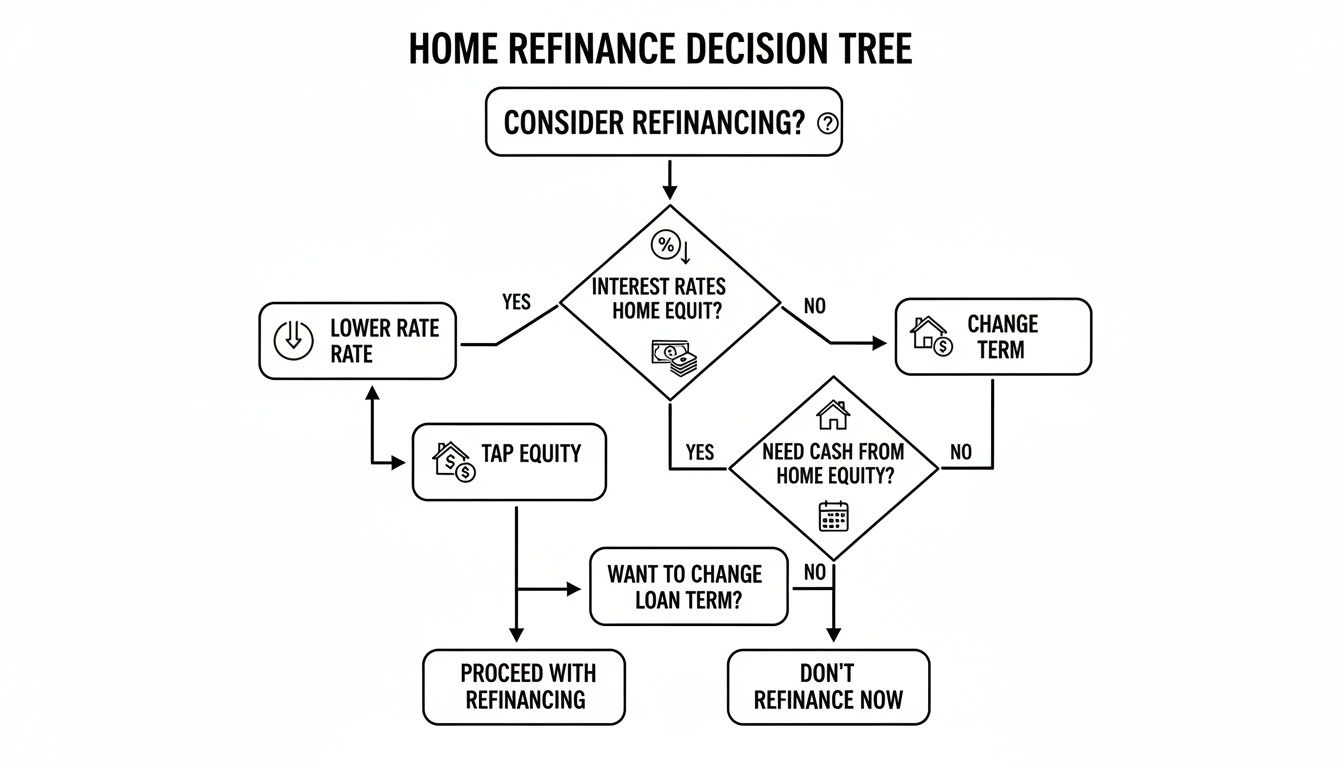

This decision tree gives you a great visual for the different paths and goals you might have when considering a home loan refinance.

As the flowchart shows, the whole process starts by figuring out what you want to accomplish—is it a lower payment, access to cash, or a different loan structure?

Is Your Situation Ideal for a Refinance?

Market conditions are only half the story. Your personal financial health and future plans are just as critical. Has your credit score jumped significantly since you first got your loan? A big improvement could qualify you for much better rates, creating a refinance opportunity all on its own, regardless of what the broader market is doing.

Ultimately, the best time to refinance is when your personal goals align with the right market opportunity. The table below breaks down the most common reasons people refinance and what to look for in each scenario.

Quick Guide to Refinancing Decisions

This table is a handy cheat sheet. Use it to quickly see if your goals line up with the common signals that point to a successful refinance.

| Your Goal | Key Signal to Look For | Best For Homeowners Who… |

|---|---|---|

| Lower Monthly Payment | Market rates are 0.75% to 1% lower than your current rate. | Plan to stay in their home long enough to pass the break-even point. |

| Shorten Loan Term | You have increased income and can afford a higher monthly payment. | Want to pay off their home faster and save thousands in long-term interest. |

| Tap into Home Equity | Your home's value has significantly increased. | Need cash for major expenses like renovations, debt consolidation, or education. |

| Eliminate PMI | You have reached 20% equity in your home. | Want to reduce their monthly housing cost by dropping mortgage insurance. |

Every homeowner's situation is unique, but these scenarios cover the vast majority of reasons why refinancing can be a game-changing financial move. If one of these sounds like you, it’s probably time to take a closer look.

How to Calculate Your Refinance Break-Even Point

When it comes to refinancing, the most important question isn't just "Can I get a lower rate?" but "When will this actually start saving me money?" The answer lies in finding your break-even point.

Think of it this way: you're making an upfront investment (the closing costs) to unlock a stream of future savings (your lower monthly payment). The break-even point is simply the amount of time it takes for those savings to completely pay back your initial investment.

If you plan on staying in your home long after you hit that break-even point, you’re in the green. It’s a clear financial win.

Step 1: Understand Your Closing Costs

First things first, a refinance isn't free. You'll have closing costs, which are the fees required to set up your new loan. These typically run between 2% to 5% of the new loan amount.

These costs aren't random; they cover essential services like:

- Origination Fee: What the lender charges for creating and processing the loan.

- Appraisal Fee: Pays for a professional to confirm your home's current value.

- Title Insurance: Protects you and the lender from any claims against the property's title.

- Credit Report Fee: The cost for the lender to pull your credit file.

Knowing this total cost is the first piece of the puzzle.

Step 2: Calculate Your Monthly Savings

This part is simple. Just subtract your new, lower monthly mortgage payment from your current one. That difference is what you'll be saving every single month.

Let's say your current payment is $2,300. Your new refinanced payment is $2,000. Easy math: you’re saving $300 a month. This is the cash that will chip away at your closing costs.

The Core Idea: The whole point of this calculation is to see how many months it takes for your new, lower payment to "earn back" the fees you paid to get it. A shorter break-even period is a fantastic sign that refinancing is the right move.

Step 3: Put It All Together: A Break-Even Example

Okay, let's connect the dots. The formula is refreshingly simple:

Total Closing Costs ÷ Monthly Savings = Break-Even Point in Months.

Here’s a real-world scenario for a $400,000 mortgage refinance:

- Get Your Total Closing Costs: Let's assume your costs are 3% of the loan. That comes out to $400,000 x 0.03 = $12,000.

- Find Your Monthly Savings: Your refi drops your payment from $2,400 down to $2,000. You're saving $400 every month.

- Calculate the Break-Even Point: Now, just divide the two.

$12,000 (Closing Costs) ÷ $400 (Monthly Savings) = 30 Months

In this case, it will take 30 months—or two and a half years—to recoup your refinancing costs. If you know you'll be in the house for at least three, four, or five more years, every payment after that 30-month mark is pure savings going straight into your pocket.

This straightforward math is the most reliable tool you have for making a smart decision. To play with your own numbers, try our easy-to-use mortgage calculators and see how the savings could stack up for you.

Choosing Your Refinance: Rate-and-Term vs. Cash-Out

When you decide it's time to refinance, you'll find yourself at a fork in the road with two main options. It helps to think of it like managing your car.

One path is a rate-and-term refinance. This is like giving your car a professional tune-up. The sole purpose is efficiency—to get the engine running smoother to lower your monthly fuel costs (your mortgage payment) without fundamentally changing what the car is.

The other path is a cash-out refinance. This is more like adding a powerful cargo trailer. You're not just tuning the engine; you're tapping into your car's power (your home equity) to haul something new, like a home renovation project or high-interest debt you want to consolidate. Both are great tools, but they solve very different problems.

What Is a Rate-and-Term Refinance?

A rate-and-term refinance is the most common and straightforward of the two. Its mission is simple: replace your current home loan with a new one that offers a better deal. It’s all about optimizing your mortgage for long-term savings and financial stability.

With this type of refinance, you’re usually trying to:

- Grab a lower interest rate to shrink your monthly payment.

- Change your loan term, like switching from a 30-year to a 15-year loan to pay off your home faster.

- Move from an unpredictable adjustable-rate mortgage (ARM) to a stable fixed-rate loan.

In short, you're just swapping your old loan for a better one. The new loan amount is only big enough to cover the old mortgage balance plus any closing costs rolled into the loan. This is the go-to strategy when you see interest rates drop.

This approach is incredibly popular for a reason. Recent refinance retention hit a 3.5-year high of 28%. An ICE Mortgage Technology report showed that servicers kept over half of their refinancing customers, with rate-and-term retention soaring to 37%—the highest in a decade. Homeowners were clearly motivated: rate-and-term refis made up a massive 62% of all refinance activity during that period. You can read more about these mortgage trends to get a sense of how homeowners are responding to the market.

When Does a Cash-Out Refinance Make Sense?

A cash-out refinance is a totally different financial tool. With this option, you take out a new, larger mortgage than what you currently owe and pocket the difference in cash. It's a strategic way to turn your home's equity—the value you've built up over years of payments and appreciation—into liquid funds for big-ticket expenses.

Key Insight: With a cash-out refinance, you are borrowing against your home. This is a powerful move but requires careful consideration, as your home is the collateral for a larger loan amount.

So, what do people use this cash for? Most commonly, it's for things like:

- Home Renovations: Funding that dream kitchen or adding a new bedroom, which can also boost your home's value.

- Debt Consolidation: Paying off high-interest credit cards or personal loans with your new, lower-interest mortgage.

- Education Costs: Covering college tuition or other major educational expenses for yourself or your family.

- Investment Opportunities: Using the funds for a down payment on a rental property or another investment.

While incredibly flexible, this option usually comes with a slightly higher interest rate than a rate-and-term refinance. And, of course, you're increasing your total mortgage debt.

Comparing Your Options Side-by-Side

To help you decide which path is right for you, it helps to see the two options laid out clearly. This table breaks down the core differences in their purpose, how they affect your equity, and what they're typically used for.

Rate-and-Term vs. Cash-Out Refinance At a Glance

This table compares the two main types of refinancing to help you decide which is right for your financial situation.

| Feature | Rate-and-Term Refinance | Cash-Out Refinance |

|---|---|---|

| Primary Goal | Lower your interest rate or change your loan term for better monthly payments or a faster payoff. | Access the equity in your home as cash for large expenses. |

| New Loan Amount | Roughly equal to your existing mortgage balance plus closing costs. | Greater than your existing mortgage balance, with the difference paid to you in cash. |

| Equity Impact | Your home equity percentage generally stays the same or increases slightly. | Your home equity is reduced because you are borrowing against it. |

| Common Uses | Taking advantage of lower market interest rates, shortening a loan term, or switching from an ARM to a fixed rate. | Funding home improvements, consolidating high-interest debt, or paying for college. |

Ultimately, choosing between these two depends entirely on your financial goals. Are you trying to optimize your existing debt, or do you need to tap into your home's value for a new purpose? Answering that question will point you in the right direction.

More Ways a Refi Can Save You Money

Refinancing isn't just about chasing a lower interest rate. It's a powerful financial tool that can reshape your mortgage to fit your current life. Two of the smartest plays we see homeowners make involve getting rid of unnecessary insurance payments and swapping out a risky loan for one with rock-solid stability.

Let's dig into how you can use a refinance to ditch Private Mortgage Insurance (PMI) and how to shield yourself from the wild swings of an Adjustable-Rate Mortgage (ARM).

Ditching Private Mortgage Insurance for Good

Remember Private Mortgage Insurance (PMI)? It's that extra fee tacked onto your monthly payment because you put down less than 20%. It’s basically insurance you pay for your lender's benefit, and it does absolutely nothing to build your own equity.

A lot of people think they're stuck with PMI until they chip away at their loan balance for years, eventually hitting that magical 80% loan-to-value mark. But there's a shortcut: a refinance can get you out of it much sooner, especially if your home's value has gone up.

Here’s when refinancing to eliminate PMI is a no-brainer:

- Your Home Value Has Surged: If the local market has been hot, your home might be worth a lot more than when you bought it. A new appraisal could show you now have more than 20% equity, allowing you to refi into a new loan without PMI.

- You've Paid Down Your Loan: Combine the principal you've paid with your home's appreciation, and you might have crossed the 20% equity threshold without even realizing it.

- You Have an FHA Loan: This is a big one. Unlike conventional loans, the mortgage insurance on many FHA loans sticks around for the entire life of the loan. Refinancing into a conventional loan is often the only way to get rid of it.

By getting a fresh appraisal during the refi process, you can prove your newfound equity and kiss that PMI payment goodbye for good. That's pure savings in your pocket every month.

Swapping an ARM for a Fixed-Rate Loan

Having an Adjustable-Rate Mortgage (ARM) can feel a bit like gambling. Sure, you get a great low "teaser" rate for the first few years, but what happens when that introductory period ends? Your rate starts adjusting to the market, and your payment could jump significantly.

Refinancing from an ARM to a fixed-rate loan is about taking control. You're trading uncertainty for predictability by locking in a single interest rate that will never change.

Key Takeaway: Moving from an ARM to a fixed-rate loan is a defensive move. It isn't just about the immediate savings; it's about protecting your household budget from the risk of future rate hikes.

This switch makes the most sense in a few key situations:

- Your Introductory Period is Ending: If your low-rate period is about to expire, it's time to act. Refinancing now can lock in a stable payment before you get hit with a potentially nasty surprise.

- You Value Budget Stability: If you see yourself in your home for the long haul, a fixed rate makes financial planning simple. No more sleepless nights wondering what the Federal Reserve is going to do next.

- Interest Rates are Trending Upward: Sometimes it's smart to lock in a fixed rate, even if it's a bit higher than your current ARM rate. You're playing the long game, protecting yourself from much higher rates down the road.

At the end of the day, these strategies show just how flexible a refinance can be. It's about making your mortgage work for you, whether that means cutting dead-weight costs like PMI or securing the financial peace of mind your family deserves.

Specialized Refinancing for Investors and Entrepreneurs

Standard mortgage refinancing works great if you have a W-2 job, but what about when your income doesn't fit into a neat little box? For entrepreneurs and real estate investors, a conventional loan application can feel like trying to force a square peg into a round hole. This is where knowing when to refinance takes on a new meaning, because specialized loan products can make all the difference.

These alternative financing options are designed for people whose financial profiles are strong but non-traditional. They look beyond standard tax returns to see the real financial health of your business or investment portfolio, opening doors that are often slammed shut by big-box lenders.

Loans for the Self-Employed Borrower

If you're an entrepreneur, proving your income is often the biggest hurdle. Years of smart, legal tax write-offs can make your net income on paper look much smaller than your actual cash flow. This is exactly where Bank Statement loans come into play.

Instead of putting your tax returns under a microscope, lenders will look at your business bank statements—usually for the last 12 or 24 months—to verify your revenue. They calculate your qualifying income based on consistent deposits, giving them a much more accurate picture of your ability to handle the loan. A P&L (Profit and Loss) loan works similarly, but it allows a certified public accountant (CPA) to prepare a P&L statement that validates your business's true profitability.

Financing for the Real Estate Investor

Real estate investors often hit a different kind of wall. Your personal debt-to-income ratio might not support adding another property, even if that new property is a cash-flowing machine. This is the exact problem a Debt Service Coverage Ratio (DSCR) loan was designed to solve.

A DSCR loan qualifies you based on the investment property's income, not your personal salary. The lender analyzes the property's rental income versus its expenses (principal, interest, taxes, and insurance). If the income covers the debt, you can often get approved.

This is an absolute game-changer for anyone looking to scale their real estate portfolio. Savvy investors can explore our guide on financing options for investment properties to see how these products fit into a larger growth strategy.

On top of that, non-resident investors can use ITIN (Individual Taxpayer Identification Number) loans, which create a path to financing without requiring a Social Security Number. Understanding the full scope of commercial loans for investment property can further clarify the options available for expanding a portfolio.

This specialized approach is becoming more important as the market shifts. Looking ahead, forecasts predict a 24% surge in refinance lending as rates come down, which is expected to push total loan volume up by 13%. For all types of borrowers—from first-time buyers to seasoned investors or ITIN users—this signals a prime opportunity. Working with a skilled broker like Mortgage Seven LLC ensures you're connected with lenders who actually understand and offer these unique solutions.

Your Next Steps to a Successful Refinance

Feeling pretty good that a refinance might be the right call? Just understanding when it makes sense is a huge first step. Now, let's turn that knowledge into a concrete plan. This part is all about getting your financial ducks in a row and connecting with the right expert to see it through.

Think of it like planning a trip. You don't just jump in the car; you pack your bags and check the map. For a refinance, your financial documents are your "bags," and a trusted guide is your "map."

Gather Your Key Financial Documents

Lenders need a complete snapshot of your financial health to say "yes" to your new loan. Getting organized upfront makes everything go faster and smoother. Seriously, a little prep work here saves a ton of headaches later.

Here's what you'll want to start pulling together:

- Proof of Income: Typically, this means your last 30 days of pay stubs and your W-2s from the past two years.

- Asset Information: Lenders need to see you have some reserves. Grab your last two months of bank statements for your checking and savings accounts.

- Existing Mortgage Details: Your current mortgage statement is key. It has all the important details like your loan number, balance, and what you’re paying now.

- Personal Identification: Just a copy of your driver's license or another government-issued ID.

Having this folder ready to go signals to lenders that you're an organized and serious applicant. For a complete rundown, our home loan application checklist has everything you need.

Partner with an Experienced Mortgage Broker

Once your paperwork is handy, the single most important step is finding the right guide for your journey. You could walk into your bank, but partnering with a mortgage broker like Mortgage Seven LLC gives you a massive leg up. A broker works for you, not for one specific bank. We shop your loan application around to a whole network of lenders to hunt down the best rate and terms for your unique situation.

The Broker Advantage: A mortgage broker is your personal navigator in the often-confusing world of home loans. We cut through the jargon, compare dozens of loan options for you, and fight for your best interests all the way from application to closing day.

This partnership becomes absolutely essential if your financial picture isn't a simple W-2 and a 9-to-5 job. For self-employed borrowers or real estate investors who need specialized loan products, a good broker is invaluable. We already know which lenders are best for those scenarios, saving you the time and rejection of knocking on the wrong doors.

Ready to see what's actually possible for you? The only way to know for sure is with a personalized analysis. Let's run the numbers and give you a clear, no-nonsense recommendation based on your goals. This is how you make sure your refinance decision isn't just a good one—it's the perfect one for your financial future.

A Few Common Refinancing Questions

The world of refinancing can feel a little confusing, and it's totally normal to have questions. Let's tackle some of the most common ones we hear from homeowners just like you.

How Will Refinancing Affect My Credit Score?

This is a big one. It's true that refinancing can cause a small, temporary dip in your credit score. This happens because the lender runs a hard credit inquiry when you apply, and you're essentially closing one loan to open another.

But here's the good news: this minor drop is usually short-lived, often bouncing back in just a few months. Over the long haul, making steady, on-time payments on your new loan can actually help build your credit. Think of it as one small step back for a giant leap forward in savings.

The Big Picture on Credit: Don't let a temporary dip of a few points scare you away from significant long-term savings. A strong payment history on your new loan will quickly erase the impact of the initial inquiry.

A quick pro-tip: try to avoid applying for other types of credit, like a new car loan or credit card, around the same time you're refinancing. This keeps the impact on your score as minimal as possible.

Can I Refinance If My Credit Score Isn't Perfect?

Yes, absolutely. While a lower score might mean you won't snag the absolute lowest interest rate on the market, you still have options. It’s all about finding the right fit.

Government-backed programs, like FHA or VA loans, are often more flexible with their credit requirements, making them a great route for many homeowners. Lenders also look at your entire financial picture, not just that one number. A strong application can be built on other factors, such as:

- A steady job and reliable income

- A good amount of equity built up in your home

- A healthy debt-to-income ratio

Even if your options seem limited right now, a mortgage pro can help you map out a strategy to boost your score and get you into a much better loan down the road.

How Many Times Can I Refinance My Home?

Technically, there’s no legal limit on how many times you can refinance. But from a practical standpoint, it’s not something you want to do without a very good reason.

Every refinance comes with closing costs. The real question isn't "can I?" but "should I?" The answer always comes down to the break-even point. If your monthly savings will cover the new loan's costs long before you plan to sell the house, it's a smart move. Refinancing over and over again without a clear financial gain is just spinning your wheels and paying unnecessary fees.

Ready to get answers that apply directly to your situation? The team at Mortgage Seven LLC can run the numbers and show you exactly what's possible. Let us help you make a smart, confident decision.